Summary:

- We have revised upwards our forecast for aggregate Tesla deliveries to 1.71 million units (-5% YoY) for 2024 and to 2.14 million units (+25% YoY) for 2025.

- We have revised upwards our forecast for the energy segment’s installed product volume to 34 GWh. (+132% YoY) for 2024 and to 51 GWh. (+48% YoY) for 2025. Tesla’s Q2 deliveries exceeded expectations, with a focus on energy segment growth.

- Tesla’s gross margin outlook was revised downwards due to the continued high costs of ramping up Cybertruck production as well as the expected negative impact of raw material tariffs.

- We have revised upwards our target price from $153 to $185. The rating is SELL.

bruev/iStock Editorial via Getty Images

Investment thesis

As we monitor the global state of the EV market, we see no improvement in long-term sales trends. The reasons are all the same (as we wrote in our previous article): weak charging infrastructure in the United States and other non-key regions for Tesla (NASDAQ:TSLA, NEOE:TSLA:CA), competition with Chinese automakers in China and Europe. In particular, due to these reasons, hybrid sales are growing faster in key regions of Tesla‘s presence.

The development of Tesla’s other businesses (e.g., energy segment) is not yet able to compensate for the weak prospects of the automotive segment and, in our opinion, will not be able to do so in the coming years, based on the data currently available. We maintain our SELL rating.

The price target was raised to $185 from $153 due to an increase in the company’s revenue forecast, partially offset by the downward revision to the company’s gross margin.

Tesla’s deliveries were above our expectations

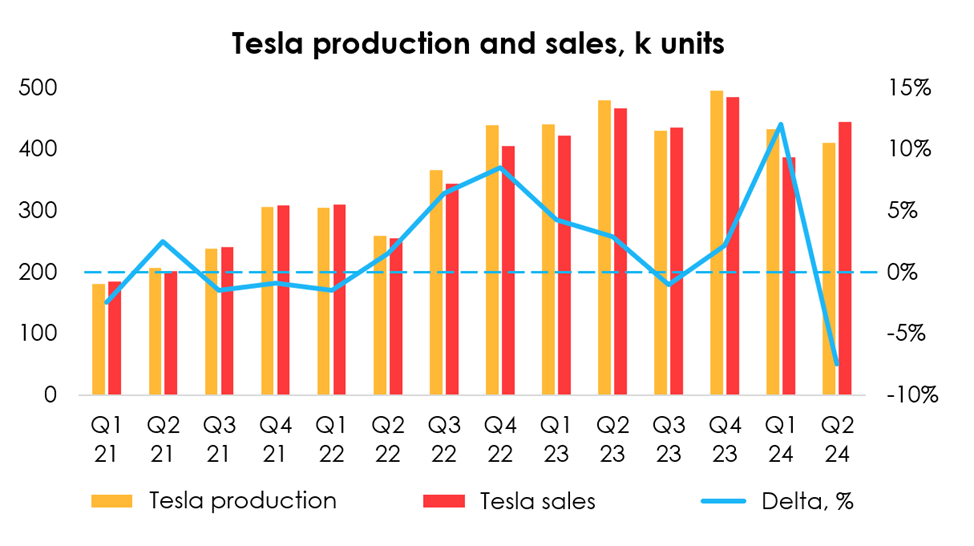

In Q2 2024, Tesla delivered ~444k electric vehicles (-5% YoY and +15% QoQ) vs. our forecast of 401k. By region, deliveries are as follows:

- US sales totaled 164k EVs vs. our forecast of 148k EVs, which was above our expectations;

- combined sales in Europe and China totaled 225k EVs, which was in line with our forecast of 225k EVs;

- Tesla deliveries in the remaining regions of operation amounted to 55k EVs vs. our forecast of 27k EVs, which was a key reason for the divergence between forecast and actual data.

It’s also worth noting that Tesla sold over 33k EVs from Q2 2024 inventory, although in recent years sales have not exceeded 5-10k EVs per quarter (once they occurred). This time, however, after a significant inventory accumulation in Q1 2024, more than 70% of them were sold in Q2 2024. In contrast, we expected the company to continue accumulating inventory through the end of 2024 due to weak demand for BEVs, particularly due to tightening incentive programs and still underdeveloped charging infrastructure in the US and the rest of the world except Europe and China.

Company data, Invest Heroes calculations

Sales of Tesla EVs were boosted by another round of purchase discounts. In Q2 2024, in many regions where the company operates, prices were reduced by an average of $1-$3 thousand, but there were also more significant reductions.

However, after the EU imposed tariffs on Chinese-made EVs, Tesla raised Model 3 prices in some European countries, which could negatively impact sales momentum in Q3 2024.

Tesla supply forecast

Despite the resumption of Tesla’s supply growth in Q2 2024, global trends remain unchanged: hybrid sales are growing faster in the company’s key regions of presence, while local challenges remain for BEVs, such as competition with Chinese automakers in China and Europe (tariffs imposed by the EU on imports of Chinese-made autos will not fully stem the flow of competitors), weak charging infrastructure (in the US and other non-key regions for Tesla).

It is worth noting that it is not just Tesla that is struggling and losing ground to local manufacturers in China. The reasons are: price competition, growing Chinese consumer confidence in domestic brands and demand for electric vehicles, and a tightening regulatory framework on emissions.

One of the ways to win customers is to get approval and introduce FSD in Chinese cars, which is expected to happen within 2024. Today, the competition among Chinese automakers for consumers is largely built around the gadgetization of the car and ADAS. Thus, in the case of the introduction of FSD Tesla in the Chinese market, this will not only be the reason for increasing the average check of a sold car, but also a way to attract customers.

Cybertruck production has more than tripled sequentially, from 2.8k sales in Q1 2024 to 8.8k sales in Q2 2024. The production ramp-up has been faster than we expected, and we have therefore revised our forecast upwards for Cybertruck deliveries from 24k to 34k for 2024 and from 44k (+85% YoY) to 66k (+95% YoY) for 2025.

As for new Tesla models, on a conference call with analysts, Ilon Musk noted that an affordable EV model will be released in 1H 2025, and reiterated previously announced plans for Semi production by the end of 2025. There is no news on the Roadster model.

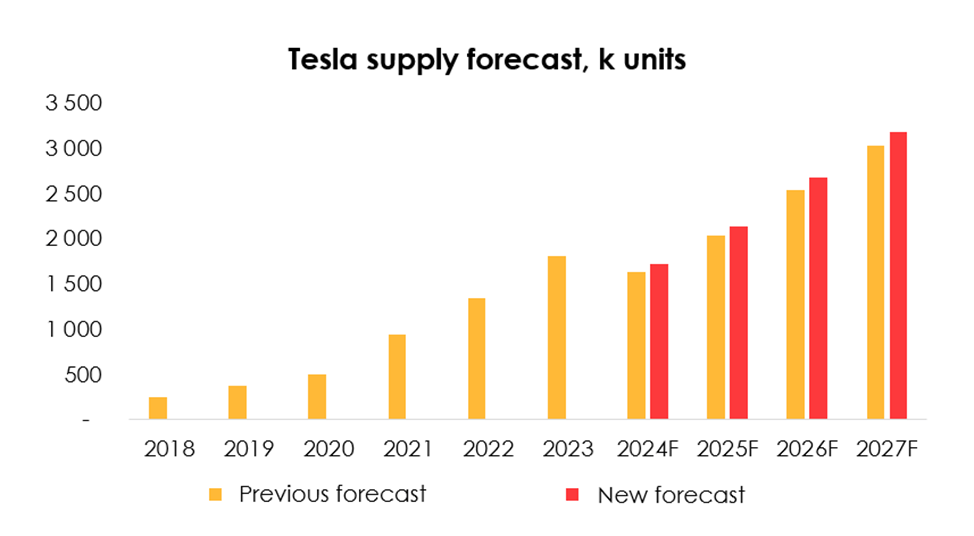

We have therefore revised upwards our forecast for aggregate Tesla deliveries from 1.63 million units (-10% YoY) to 1.71 million units (-5% YoY) for 2024 and from 2.03 million units (+24% YoY) to 2.14 million units (+25% YoY) for 2025 due to:

- higher actual deliveries in Q2 2024;

- increase in the forecast for Cybertruck deliveries in the U.S.;

- increase in the forecast for electric vehicle deliveries in non-key regions where the company operates due to strong results for Q2 2024.

Company data, Invest Heroes calculations

Autonomy: Full Self-Drive and Optimus

Tesla continues to invest in developing its own autonomous driving system, which at the same time allows it to develop the “intelligence” of its Optimus humanoid robots.

Full Self Drive

Measures such as lowering the purchase and monthly subscription prices of FSD, demonstrating the capabilities of the driver assistance system before buying a car, and activating a free period of FSD use, introduced in Q1 2024, are having a positive impact on the number of FSD users. According to the company’s CEO, most people who tried the driver assistance system for free continue to use it on a payment basis.

The robotaxi presentation, previously scheduled for August 8, 2024, has been postponed to October 10, 2024, due to the necessity of improvements.

We maintain our expectations for FSD revenue and expect that with current inputs it will not contribute significantly to Tesla’s automotive revenue over the valuation horizon. As for robotaxi, due to the lack of official announcements, we have not yet budgeted its revenue into the financial model and at least wait for an announcement on October 10, 2024.

Optimus

On the Q2 2024 results conference call, Ilon Musk said that he expects to start mass production of Optimus robots in early 2025 and that this will enable the introduction of thousands of humanoid robots in Tesla’s manufacturing facilities by the end of 2025 and open access to orders from external customers starting in 2026. Currently, two Optimus robots assist in workflows at Tesla’s manufacturing facilities.

Given Tesla’s historical tendency to be overly optimistic about announced new products (especially those related to autonomy), as well as the high degree of uncertainty, at this point we consider Optimus a venture capital bet and do not include it in our forecast.

Tesla’s revenue

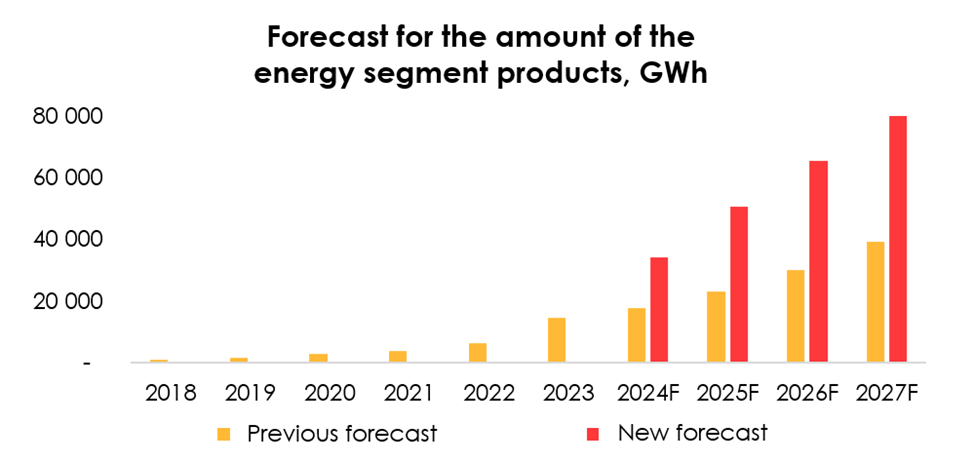

Tesla reported 9.4 GWh (+157% YoY and +132% QoQ) of energy segment product installations in 2Q 2024, which was above our expectations. Management has repeatedly said that Tesla’s energy segment will grow at a high rate (higher than the auto sales segment), but such strong non-linear growth in 2Q 2024 exceeded market expectations.

Tesla says that although they are already prepared for additional demand, they are in the process of expanding production capacity in the U.S. for the future, as well as building a Megapack factory in China.

We have revised upwards our forecast for the energy segment’s installed product volume from 18 GWh. (+22% YoY) to 34 GWh. (+132% YoY) for 2024 and from 23 GWh. (+30% YoY) to 51 GWh. (+48% YoY) for 2025, which will lead to revenue growth in this segment.

Company data, Invest Heroes calculations

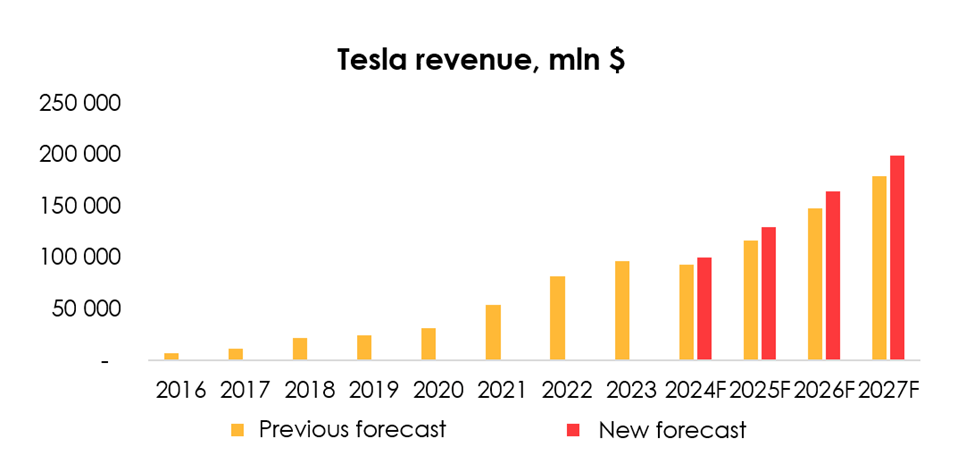

We have revised upwards Tesla’s revenue forecast from $92.6 bn (-4% YoY) to $100.2 bn (+4% YoY) for 2024 and from $116.6 bn (+26% YoY) to $129.1 bn (+29% YoY) for 2025 due to the following:

- increase in Tesla’s 2024-2025 aggregate supply forecasts;

- upward revision of the forecast for energy segment revenue from $7.2 bn (+20% YoY) to $11.3 bn (+87% YoY) for 2024 and from $9.4 bn (+30% YoY) to $16.2 bn (+44% YoY) for 2025).

Company data, Invest Heroes calculations

Tesla’s financial results

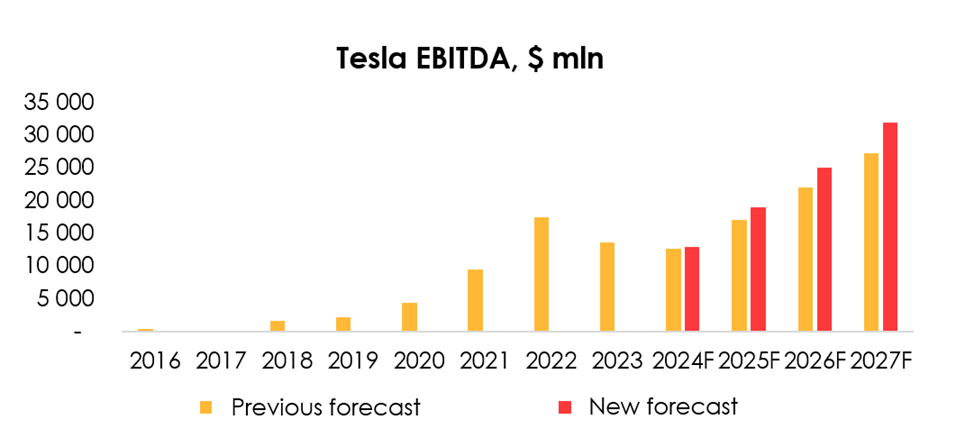

We have revised upwards Tesla’s EBITDA guidance from $12.6 bn (-7% YoY) to $12.9 bn (-5% YoY) for 2024 and from $17 bn (+35% YoY) to $18.9 bn (+46% YoY) for 2025:

- upward revision of revenue forecast in 2024-2025 (positive effect);

- downward revision of the company’s gross margin guidance from 18.5% to 17.8% for 2024 and from 19.8% to 18.8% for 2025 (negative impact).

Tesla’s gross margin outlook was revised downwards due to the continued high costs of ramping up Cyber truck production, as well as the expected negative impact of raw material tariffs.

Company data, Invest Heroes calculations

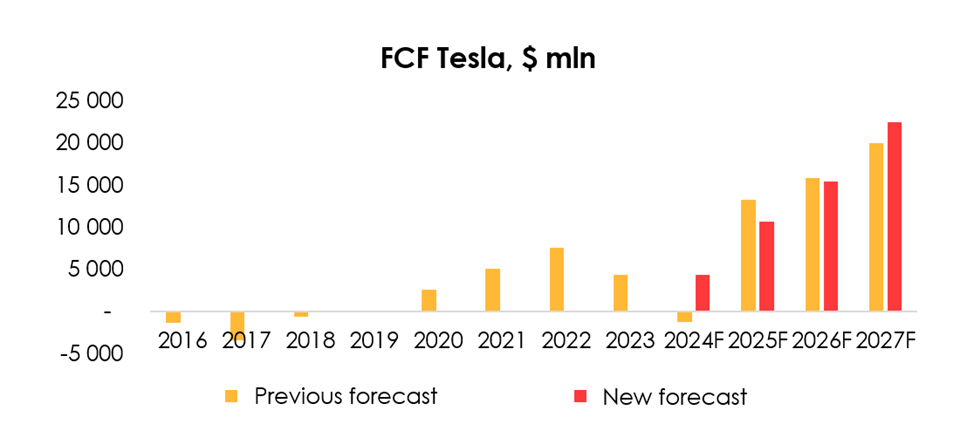

The cash flow forecast was revised upwards from ($1.3) bn to $4.4 bn (-0% YoY) for 2024 and downgraded from $13.2 bn to $10.7 bn (+146% YoY) for 2025 due to:

- upward revision of the company’s 2024-2025 operating profit forecast;

- adjusting the inventory forecast with a view to their reduction in Q3-Q4 2024 and subsequent setting consistent inventory turnover ratio.

Company data, Invest Heroes calculations

Valuation

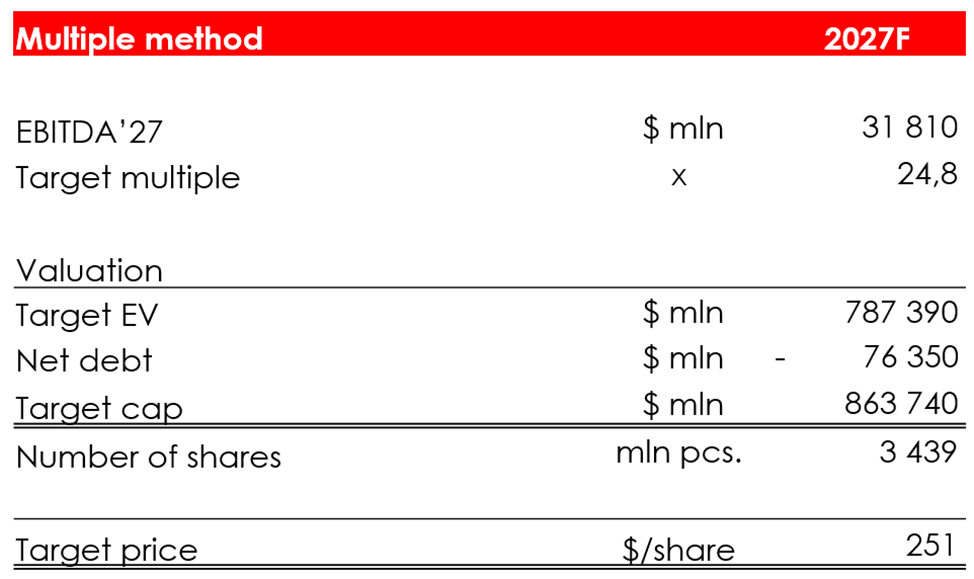

We have revised upwards our target price from $153 to $185 due to:

- increase in EBITDA guidance for 2024-2027, which also resulted in an increase in the EV/EBITDA multiple from 23.8x to 24.8x;

- the shift of the FTM valuation period by 1 quarter, which means future financial results have gotten closer.

Stock status – SELL.

The valuation at $185 was obtained by discounting using the multiple method at 13% p.a. The discount rate of 13% is the average growth of the S&P 500 Index over the past 20 years. In other words, when we value a company based on its long-term results, it is important to us that the company’s growth exceeds the average growth of the index.

Invest Heroes

Upside risks

Upside risks to our valuation include:

- An improved macroeconomic environment, which would be positive for new vehicle purchases (e.g., lower interest rates);

- Faster improvements in charging infrastructure (especially in the U.S., as this is a key region for Tesla);

- Significant new customer acquisition in China due to the prospect of FSD approval and entry into the Chinese market within 2024;

- Government incentives for consumers to purchase BEVs could lead to increased sales of Tesla electric vehicles;

- Larger revenue impact from FSD;

- Earlier or greater impact from unannounced AI-enabled products such as Optimus and Robotaxi.

Conclusion

As a result, despite the price target increase, we do not consider Tesla stock a compelling buy and have a SELL rating. To manage your positions, we recommend following Tesla’s earnings releases, EV market updates.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.