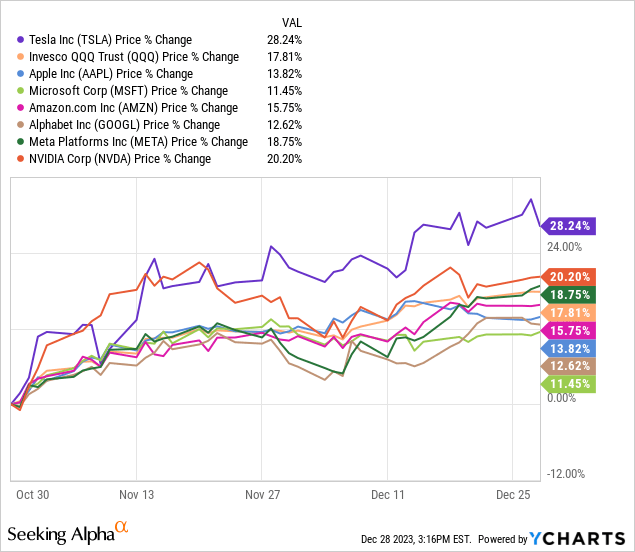

Tesla, Inc. stock has outperformed its big tech peers since late October 2023 due to its interest rate-sensitive business; however, Tesla is still playing catch up.

Technically, Tesla is finely poised, with the stock primed for a big breakout or breakdown out of a triangle pattern formed on its chart.

Plunging yields (easing financial conditions) could alleviate Tesla’s demand and margin pressures in 2024; however, the stock is richly priced at ~65x forward P/E.

In my view, Tesla’s valuation leaves little upside and no margin of safety. Read on to learn more.

Xiaolu Chu

Introduction: Tesla Is Still Trailing Its Big Tech Peers, Can It Catch Up In 2024?

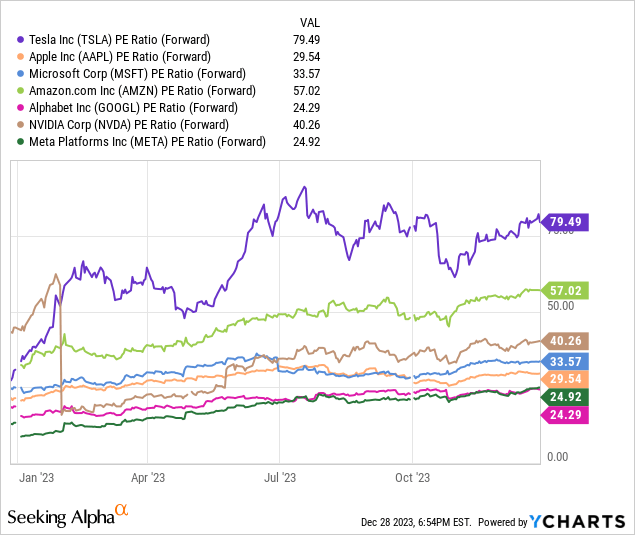

Amid a sharp decline in interest rates, Tesla, Inc. (NASDAQ:TSLA) stock has handsomely outperformed its big tech peers since 30th October 2023 as you can observe on the chart below. In my view, the interest rate-sensitive nature of Tesla’s business is the primary factor behind this outperformance from TSLA.

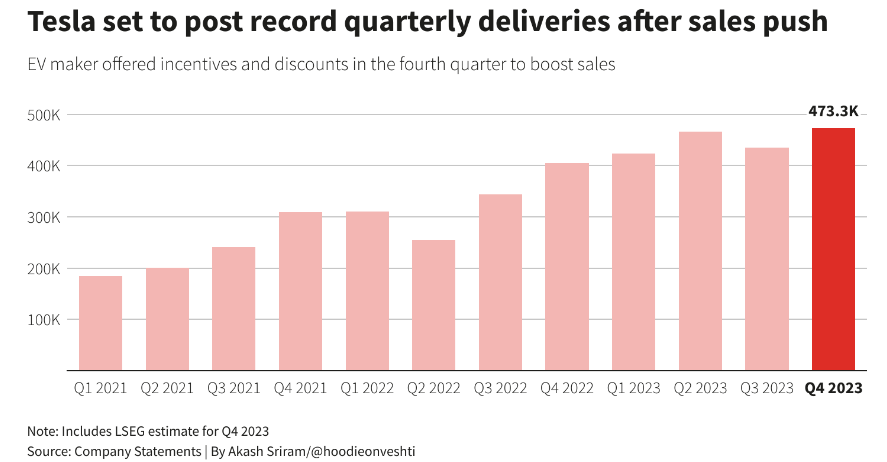

As we head into the new year, investors are surely looking forward to Tesla’s delivery numbers, which are due next week. According to a Piper Sandler analyst (emphasis added):

Overweight-rated TSLA will be announcing Q4 deliveries early next week (probably on January 2nd). We are currently expecting the company to deliver 507k vehicles in the quarter, implying a full-year total of 1.83M units. After considering the latest intra-quarter data, we think our estimate appears doable (though admittedly, our forecast is perhaps on the high end of a believable range).

Even if our estimate proves optimistic, we still think Q4 will set a record, with the annualized production rate exceeding 2M vehicles per year. We expect margins will also rise vs. Q3, given stable pricing and better fixed cost leverage. We will re-assess our margin forecast once Q4 delivery results have been released.

While these estimates from Piper Sandler seem overly optimistic, consensus delivery estimates of 473.4K (gathered by LSEG via a poll of 14 analysts) suggest a fresh record for Tesla deliveries in Q4 2023.

Reuters

With long-duration treasury yields easing up by ~140 bps, the cost of borrowing has come down significantly. And, in our view, this easing of financial conditions should alleviate some of Tesla’s demand and margin pressures. Heading into 2024, the demand outlook for Tesla is seemingly much better now than where it was just a few months ago, with the bond market pricing in seven rate cuts (hopefully due to falling inflation and not an impending economic downturn). If the consensus view of a soft landing in the economy holds true, then Tesla is likely to have another stellar year as a business in 2024.

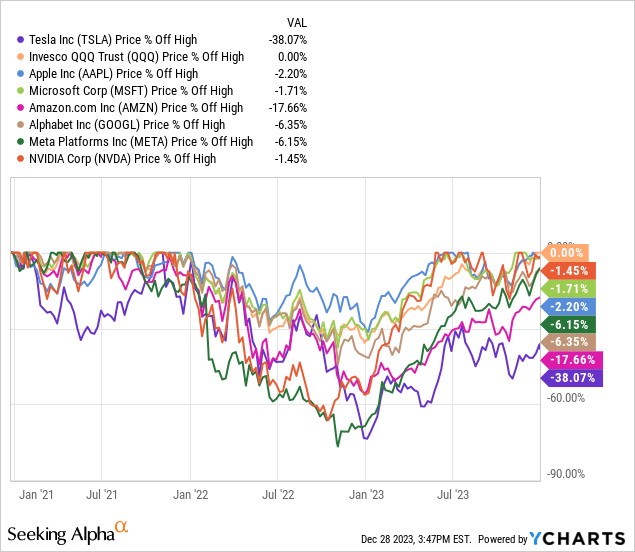

Now, plunging yields have sent tech stocks (QQQ) soaring to new all-time highs, with most of Tesla’s big tech peers hitting or very close to hitting new all-time nominal highs. However, Tesla is still sitting -38% off of its November 2021 highs, which means TSLA stock is trailing its big tech peers by a mile [despite being up +134% YTD].

Tesla’s Tryst With Technicals

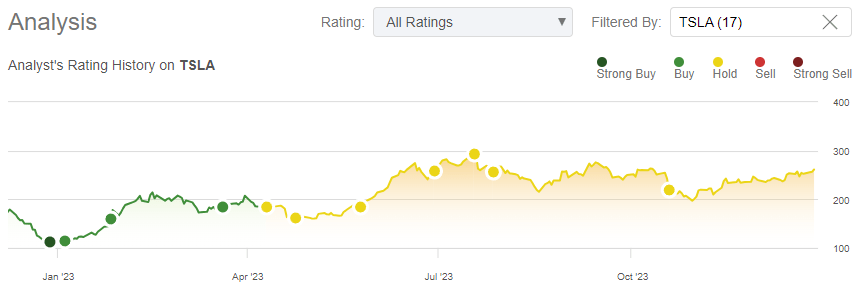

After rating Tesla an asymmetric buy in the low $100s in late 2022, I turned neutral on TSLA stock in April 2023 at ~$200 due to concerns about Tesla’s recession playbook [sacrificing margins to prop up volumes] and significant shift in the risk/reward dynamic due to a wild run-up in the stock.

Author’s rating on TSLA (Seeking Alpha)

In one of my recent articles – “Tesla: Q3 2023 Review, Musk And Co. Are Stuck In A Vicious Cycle” – I shared a cautiously bearish stance for TSLA with the stock trading at ~$270 at the time (emphasis in original):

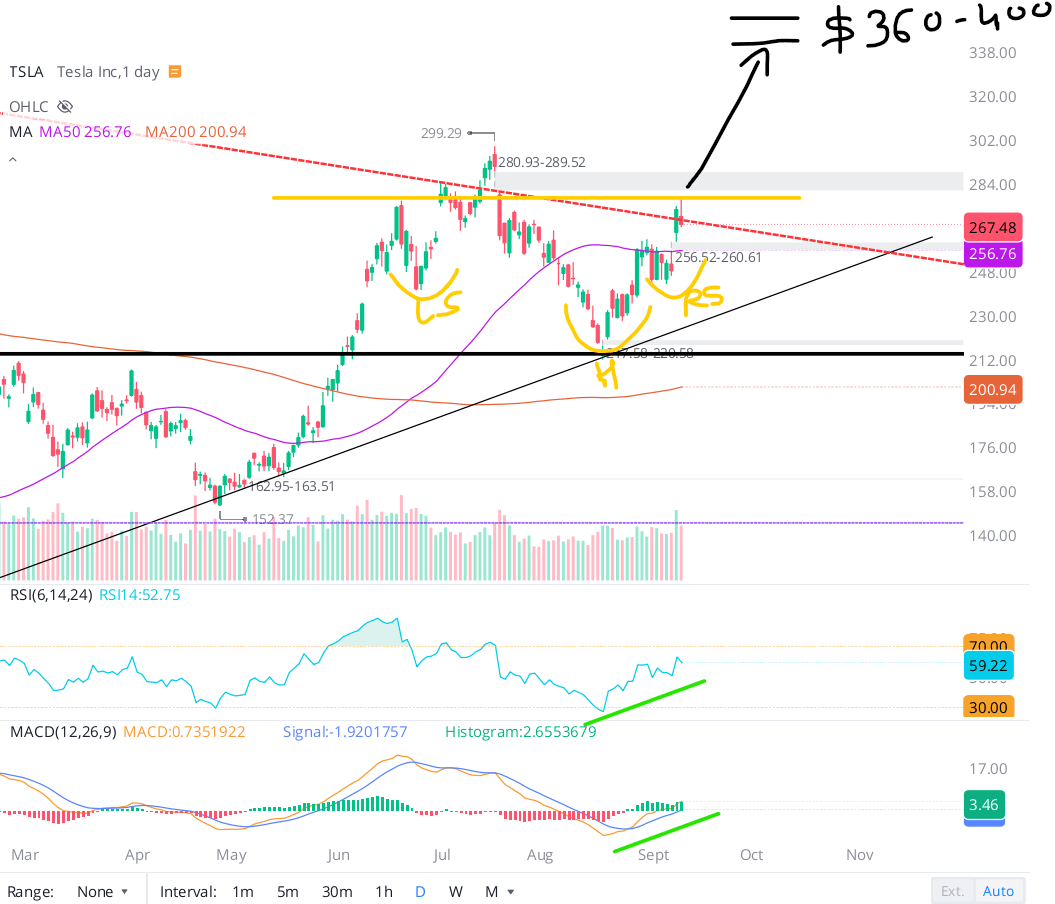

The bull-bear debate around Tesla being a technology or an auto company continues to rage on, with TSLA’s price action getting tighter and tighter in a triangle formation marked in the chart below –

Tesla stock chart 9/12/2023 (Webull Desktop)

Here are the two potential paths I see for Tesla:

1) An upside breakout above the $280-300 resistance zone could confirm the bullish “Inverse Head & Shoulders” pattern marked on the chart below:

Webull Desktop

The price objective of this bullish “Inverse H&S” pattern is ~$360, and if TSLA can retain bullish momentum, it can easily extend to new all-time highs above ~$400. In my view, a rise in daily RSI and MACD indicators since mid-August supports an upside breakout. TSLA stock is not overbought, and with 50-DMA well above 200-DMA, technical momentum is still looking strong here.

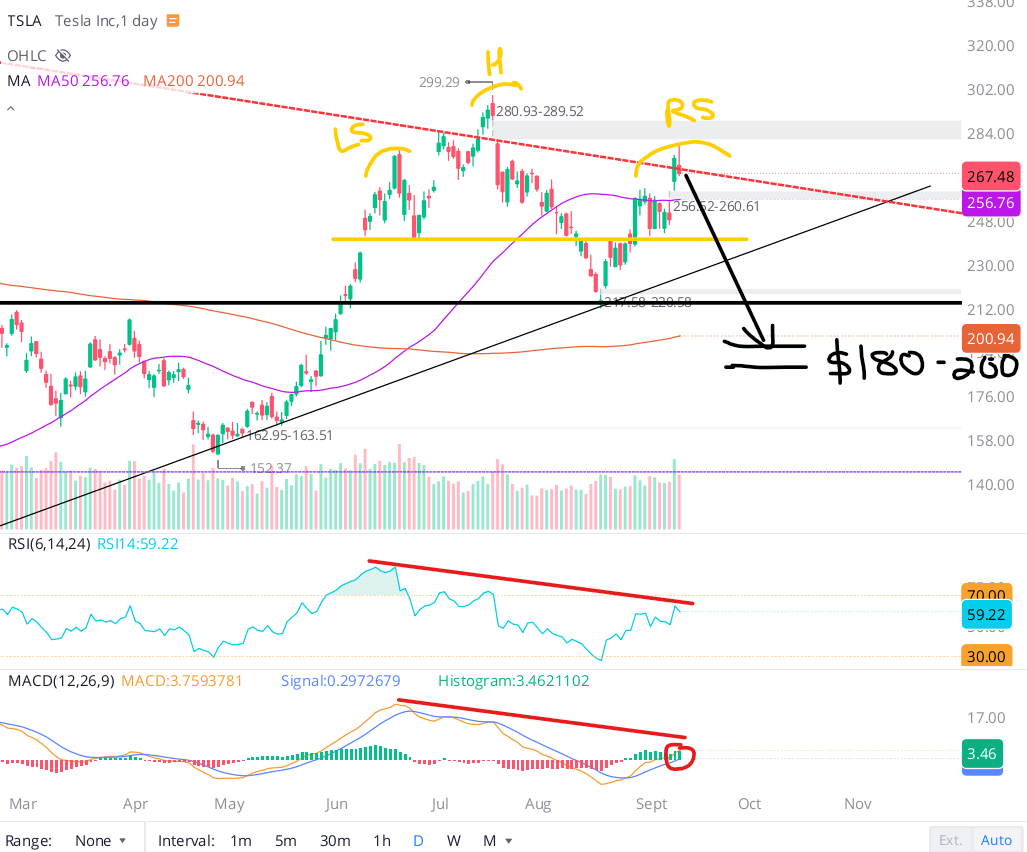

2) Conversely, a rejection at current levels or the $280-300 resistance zone could easily send Tesla shares tumbling back down to the $240 (neckline) level. And a breakdown of this level would confirm the bearish “Head & Shoulders” pattern marked on the chart below:

Webull Desktop

The price target of this bearish “H&S” pattern is ~$180, which coincidentally happens to be my fair value for Tesla. Negative divergence on daily RSI and MACD indicators since June supports a downside breakdown. As of today, both of these patterns are still in play, and Tesla stock could move ~$100 in either direction (up or down) when it breaks out of the massive triangle formed on its chart.

From a technical perspective, TSLA stock is still stuck in no man’s land in the $215 to $280 range, with risk/reward being finely poised at current levels. Given the triangle formation, Tesla stock could break out to the upside or break down to the downside in the near future. Either outcome is possible, but we can be sure that it’ll be a big move!

As of now, I would avoid taking any new near-to-medium-term position in Tesla shares. However, if I had to take a position, it would be on the short side with a tight stop-loss. So, this hypothetical position would be “Short Tesla at $270 (downside target: $180-200, reward: $70-100), with a stop-loss at $305 (risk: $35)”.

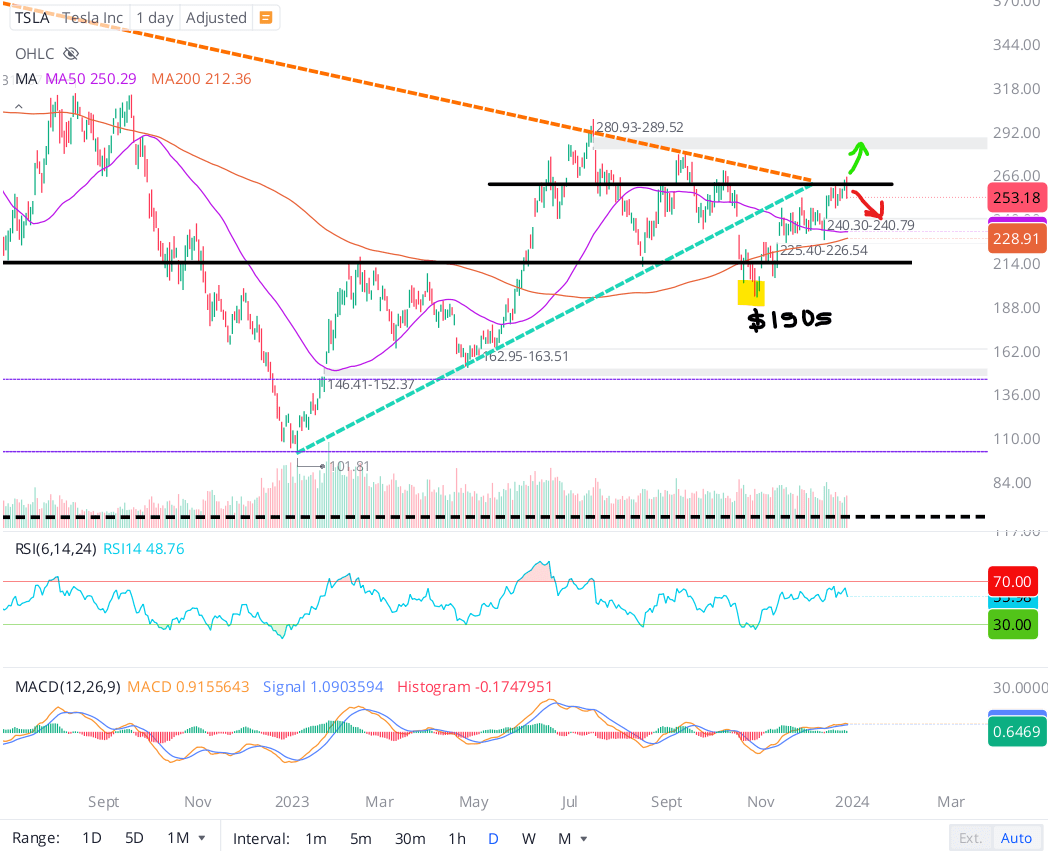

By late October, Tesla had dropped to the $190s, right into our target box of $180-200. While we did not get an opportunity to add to our existing long position at ~$180 (our fair value estimate for Tesla), the H&S pattern worked out to a tee in this instance.

Webull Desktop

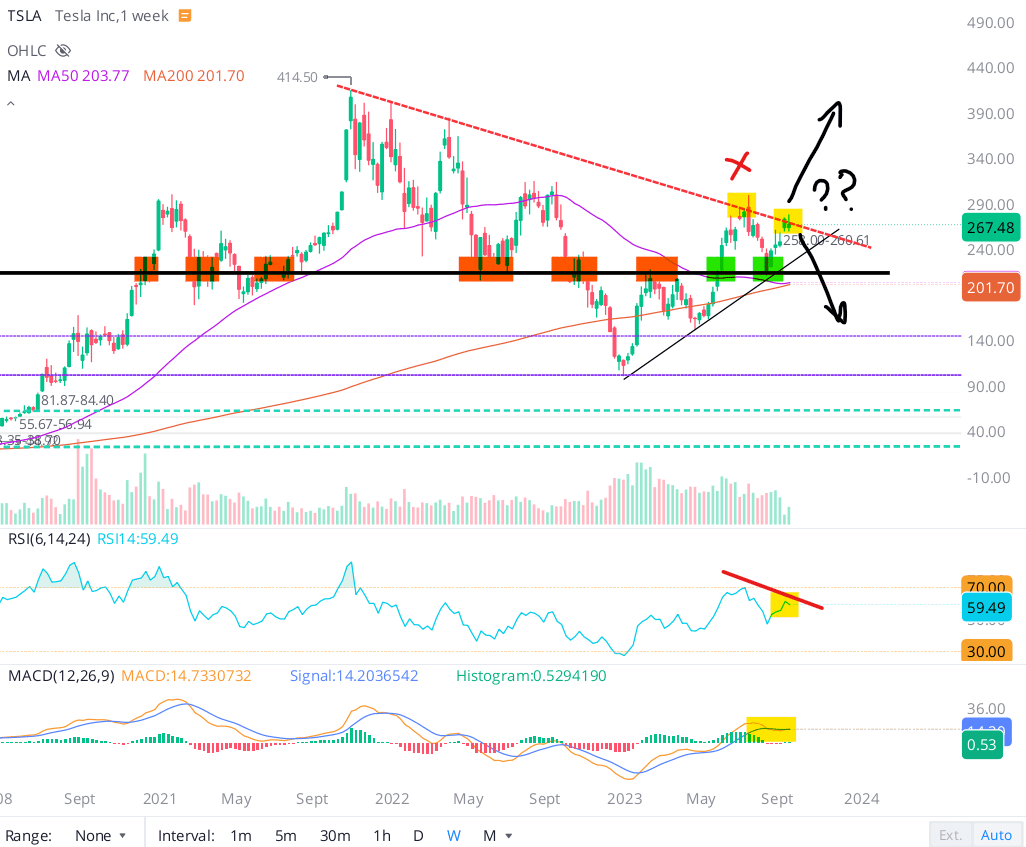

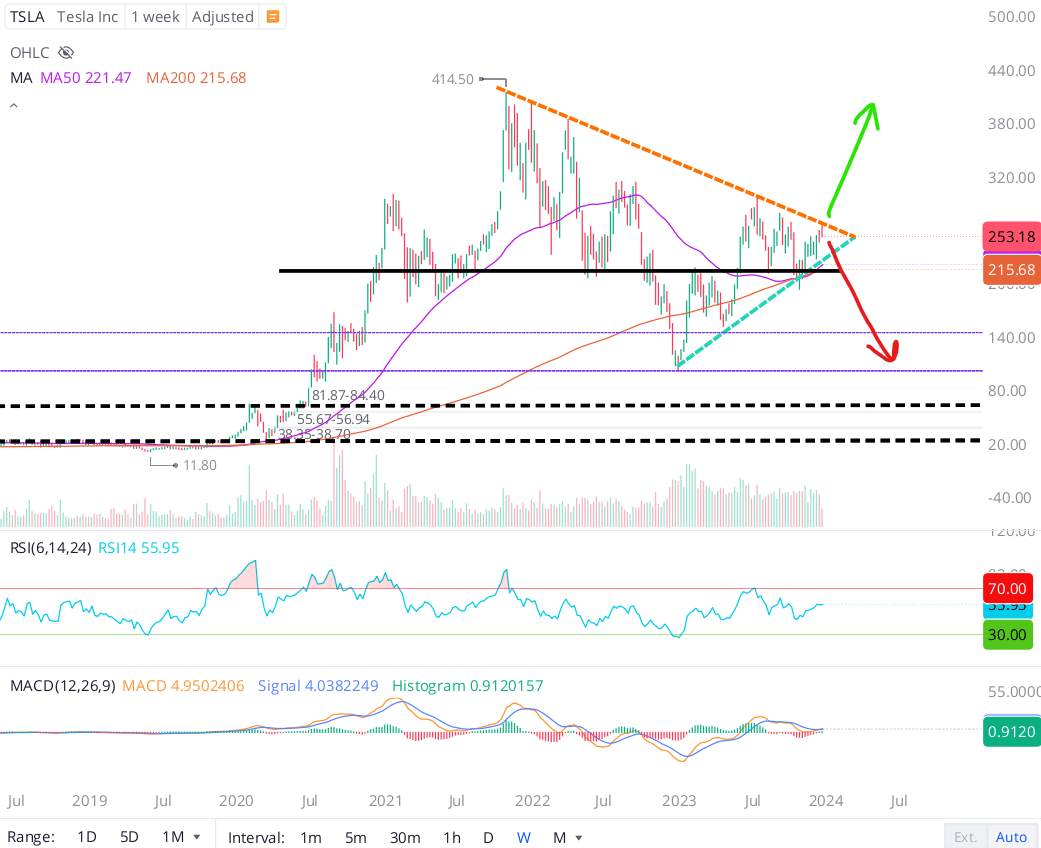

Now, on the back of a significant bounce off of those October 2023 lows, Tesla’s stock is testing a key resistance level in the form of the central line of the symmetrical triangle it broke down from a couple of months ago. Unlike QQQ and most of its big tech peers, Tesla is not overbought [daily RSI < 70].

Upon re-drawing the lines with recent local tops and local bottoms on the weekly chart, I think we can make the case that Tesla is still trading within a symmetrical triangle pattern. Since triangles can break in either direction, Tesla looks primed for a big breakout or breakdown.

Webull Desktop

As I see it, a break above $265-270 could send Tesla to $300 in quick order, and potentially to the $360-400+ range [new all-time highs] over the next 6-12 months. On the flip side, if Tesla suffers yet another rejection here, a breakdown below the $215-230 range could send TSLA stock into a tailspin that culminates in the low-to-mid $100s.

Concluding Thoughts: Is Tesla Stock A Buy, Sell, or Hold?

Back in September, my cautiously bearish stance for Tesla was based on the following rationale:

Tesla’s sales growth is decelerating and margins are contracting amid a tough macroeconomic environment. With interest rates likely to remain higher for longer, and auto loan delinquencies on the rise, I expect auto prices to come under further pressure in the foreseeable future. While Tesla is leading the auto industry’s price-cutting exercise, such rapid margin deterioration is never ideal.

Given Musk’s recessionary playbook (prioritizing sales over profits), Tesla is essentially a binary bet on FSD achieving full autonomy (which may or may not happen).

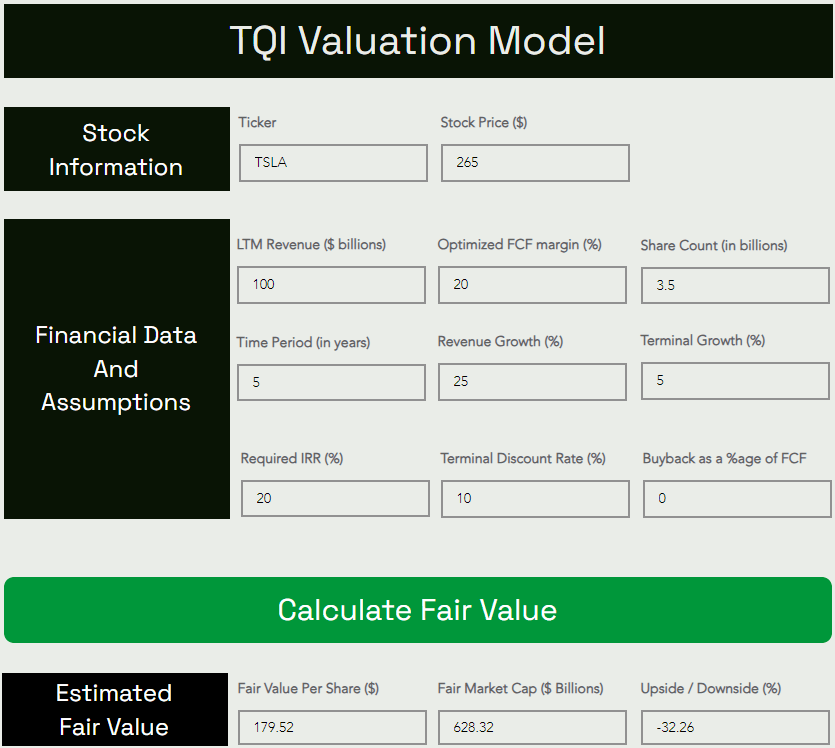

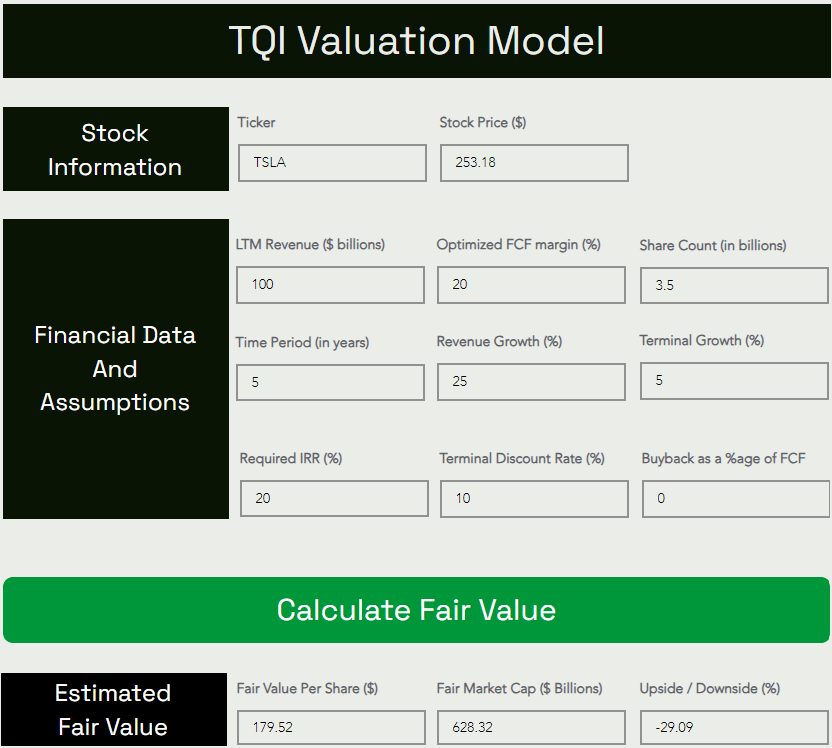

At >70x forward P/E, Tesla carries a demanding valuation. According to TQI’s Valuation Model, Tesla remains overvalued:

TQI Valuation Model (TQIG.org)

As per my model, Tesla’s intrinsic value is ~$180 per share. With the stock trading at ~$270 per share, it is currently overvalued by ~30-35%. Now, I am happy to pay a premium for a high-quality company like Tesla; however, the risk/reward isn’t attractive enough to justify an investment here.

TQI Valuation Model (TQIG.org)

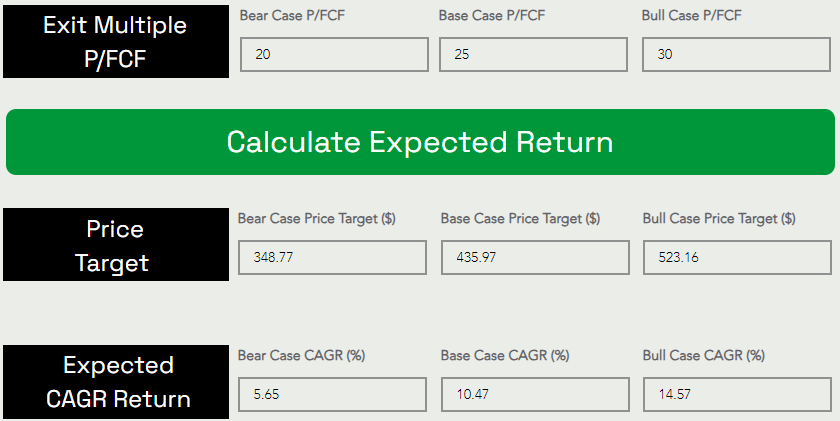

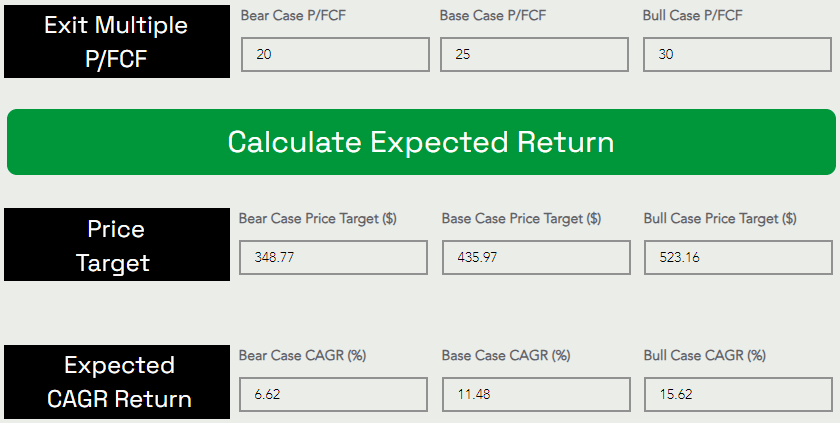

Assuming a base case P/FCF exit multiple of 25x, I see Tesla hitting $436 per share by 2027. As can be seen below, Tesla is projected to deliver CAGR returns of ~10.5% for the next five years, which falls well short of my investment hurdle rate (min. required IRR) of 15%.

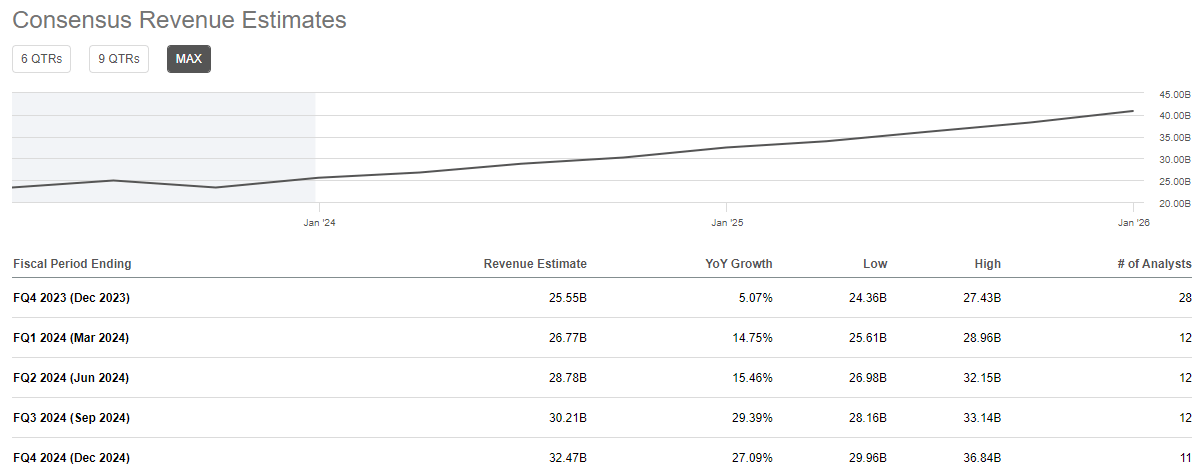

According to consensus street estimates, Tesla’s revenue growth rates are set to trough in Q4 2023, with a strong re-acceleration forecasted for 2024. Given the rapid drop in long-duration treasury yields (easing of financial conditions), I believe Tesla could outperform expectations next year if the economy avoids a hard landing.

Seeking Alpha

While Tesla’s price cuts have slowed in recent weeks, Musk’s recessionary playbook (prioritizing sales over profits) is still very much in play. Hence, I am not sure where auto margins will land in upcoming quarters. Tesla’s energy business is firing on all cylinders, and there’s a good reason to be optimistic about refreshed 3 & Y models, the Cybertruck, and a possible announcement of a $25K next-gen model with new plants coming up in Mexico and potentially India [if reports are to be believed].

That said, Tesla (trading at ~80x forward P/E [YCharts estimate], ~65x [my 2024 EPS estimate of $4]) commands a significant valuation premium compared to its big tech peers.

In our view, Tesla is currently valued as an AI and robotics company (being given a lot of credit for futuristic projects like FSD, Dojo, and Optimus robot), and such a demanding valuation leaves little to no margin of safety [especially due to high uncertainty around the outcomes of these ambitious projects].

According to our TQI Valuation Model, Tesla is currently overvalued by ~40%:

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

Now, I am generally fine with the idea of paying a premium for a high-quality growth business like Tesla; however, the risk/reward isn’t attractive enough to justify an investment in TSLA at current levels.

From a technical perspective, a big breakout or breakdown is in the cards for Tesla in the first half of 2024. As I see it, a soft or no landing in the economy can support another wild run-up in Tesla stock. However, Tesla’s valuation is already very rich, and it is hard to foresee any kind of expansion there. Furthermore, I expect an economic slowdown in 2024, which means the operating environment for Tesla could remain rough and worsen in upcoming quarters. Therefore, it is too hard to bet on a bullish breakout in Tesla.

That said, easing financial conditions could help alleviate Tesla’s demand and profitability concerns in 2024. Given the potential asymmetric upside of Tesla’s ambitious projects, investors may decide to look beyond an economic recession [if were to end up in one]. Therefore, my cautiously bearish stance on Tesla has moderated to a neutral stance.

As you may know, I hold a long position in Tesla [accumulated in late 2022: “Tesla Stock: An Asymmetric Buying Opportunity Arises Out Of Insider Selling, Demand Concerns, And A Scary Recession Playbook”]. And as of now, my plan of action for Tesla hasn’t changed:

If we see a quick move to the $360-400+ range, I will book partial profits on my long position.

Conversely, if we drop down to $180, I will restart accumulation and add to my long position.

Key Takeaway: I rate Tesla stock a “Avoid/Neutral/Hold” in the mid-$200s.

Thank you for reading, and happy investing! If you have any questions, thoughts, and/or concerns, please feel free to share them in the comments section below.

Analyst’s Disclosure:I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

How To Invest In This Environment?

In order to navigate this tricky economic period, we are pursuing “Bold, Active Investing with Proactive Risk Management” at our investing group – “The Quantamental Investor“. With a laser focus on valuations, profitability, and balance sheet strength, we are buying the winners of tomorrow! Furthermore, we are utilizing index-based options to guard against significant broad-market declines. Join us today to prepare for whatever the market may throw at you in 2024!