Summary:

- Tesla remains a market leader in EVs, with new factories boosting production capacity and operational advantages, priming shares for a breakout.

- Tesla’s diversified business model includes insurance, charging systems, autonomous driving software, solar panels, and energy storage, offering significant growth potential.

- Tesla’s strong balance sheet, the potential for share repurchase, and innovative projects like AI and humanoid robots suggest a fair value of $307.50 per share.

- Risks include competitive pressure from traditional and Chinese automakers, potential loss of subsidies, and the possibility of secondary offerings to fund development plans.

Roman Tiraspolsky

Tesla, Inc. (NASDAQ:TSLA) remains the domestic market leader in electric vehicles (“EVs”) and appears likely to sustain this title for the foreseeable future. Tesla also appears capable of performing well in most international markets. The company opened two factories in 2022, allowing the company to further increase its production capacity and operational advantages versus the majority of its competitors. Tesla’s capacity is underappreciated, and shares appear primed to break out of a recent downtrend that lasted most of this summer. If shares can get through the $220s, I believe they are primed to gap up and break-out to considerably higher levels.

Fundamentals

Tesla’s current business model includes not only selling electric vehicles EVs, but also auto-related costs incurred by its customers, such as insurance, charging systems, and autonomous driving software. Tesla’s charging systems also extend to solar panels and energy storage batteries. The company’s competitiveness in solar power generation and battery storage is both a competitive advantage within EVs, and also a large market in its own right, which has the potential for considerable growth in the coming years.

Tesla’s operational advantages versus domestic EV makers appear to be continuing, with no domestic manufacturer yet capable of producing a competitive threat at scale and for a profit. Meanwhile, Tesla has reduced its unit production costs, and appears capable of further reductions in the future. Tesla has previously used some reduced costs of production as opportunities to reduce the price of its vehicles, and such moves are likely to occur again over the coming years. Such price cuts will make it exceedingly difficult for its competitors to gain traction in the EV marketplace without sustaining significant losses on its units sold.

Tesla also has the potential to benefit from its position in full self-driving (“FSD”) software, where it appears to be among the leading global and domestic developers. Tesla already sells its existing FSD as a monthly subscription, and as the technology improves, it is probable that Tesla’s subscription revenue will substantially increase. It also seems of growing likelihood that some competing auto manufacturers will license Tesla’s FSD technology. This may look very much like how several have adopted Tesla’s Superchargers.

I also would not be surprised if some competing auto manufacturers end up buying batteries from Tesla. Some have attempted to develop and manufacture their own EV batteries, and the progress has been slow and costly. Meanwhile, Tesla seems to have less operational difficulty in ramping up production of its products.

It appears Tesla’s revenue will only rise in the low single digits in 2024. However, I believe that the company’s recent development of two factories (Austin, Texas and Berlin, Germany) that have now had time to ramp production capacity and address initial issues will allow it to significantly increase production in 2025 and 2026. As a result, I expect Tesla’s revenue to again accelerate next year, growing by double digits and potentially as much as 20% in each of the next two years.

Precise revenue growth will be dependent upon not only production capacity, but whether Tesla reduces its pricing, as well as whether it can release a new model. These factors will also be meaningful in the continuing success of Tesla’s Cybertruck. However, given the reservation count of over two million units that the model received, it should continue to be a meaningful supplier of revenue over the coming years.

I anticipate Tesla will realize adjusted EPS of about $2.40 in 2024 and $3.50 or greater in 2025. Tesla also has a balance sheet commensurate with a mega-cap tech company, boasting ample cash of over $30 billion, and nearly no debt. If Tesla is capable of increasing its cash position while completing the potential development of another factory in Mexico (or scrapping the plan), the company may then institute a share repurchase plan.

I believe Tesla is close to being fairly valued for its auto production business, where I expect the fair value of is $3.50 in minimum expected 2025 EPS should trade at a forward P/E of about 65, resulting in $227.50. Nonetheless, I do not believe this price reflects the multiple moonshots that remain under the Tesla umbrella. These include AI computing competency and the development of humanoid robots for market. Tesla’s position in FSD may also bring forth the development of a highly competitive ride-hailing application.

Similarly, Tesla’s battery technology may become a product for competing auto manufacturers, and the company’s charging systems could influence meaningful changes within the electric utility marketplace. These numerous potentially valuable products appear to be worth at least another $80 per share, which, if added to the $227.50 valuation of the automotive business, results in a fair value of $307.50.

Technical Analysis

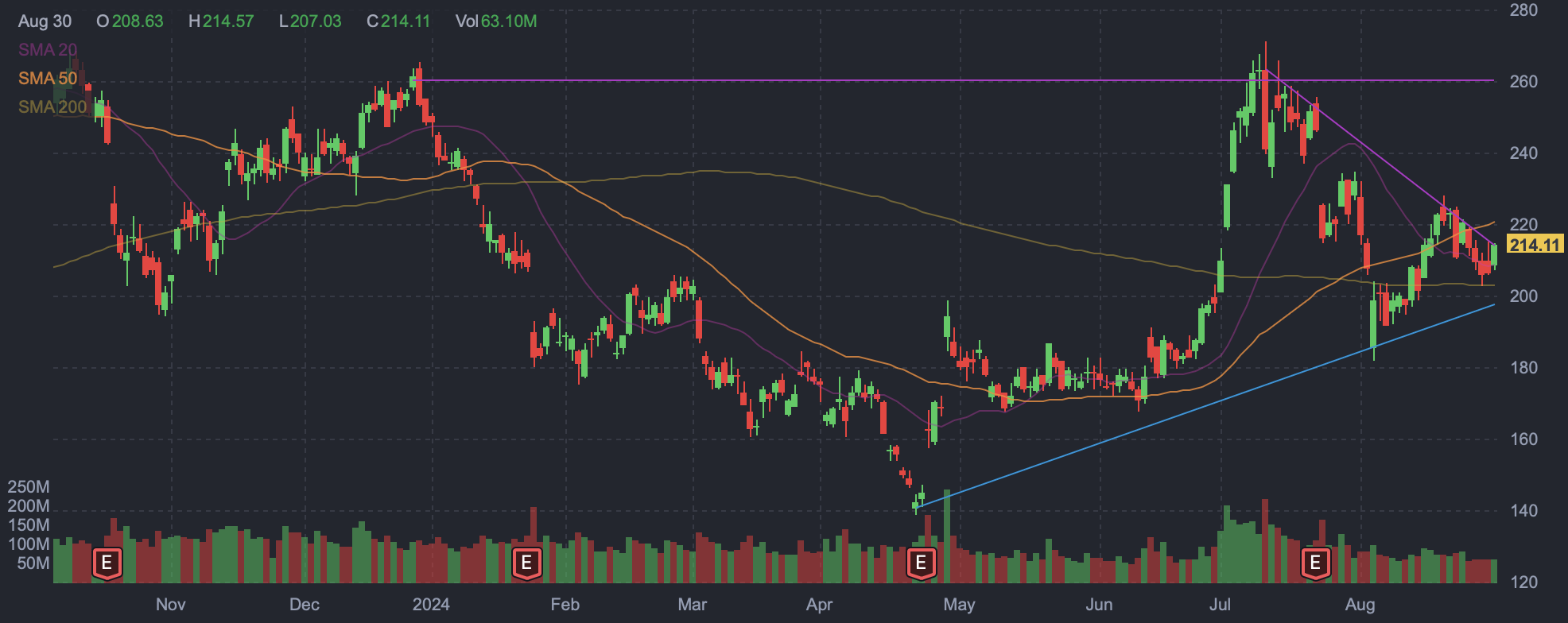

Tesla shares also now appear to be approaching an inflection point where shares have a strong likelihood to break higher. If shares can make it through the $220s. I believe they have the potential to make a quick move to the mid $200s and possibly resistance at around $260.

Tesla daily candlestick chart (Finviz.com)

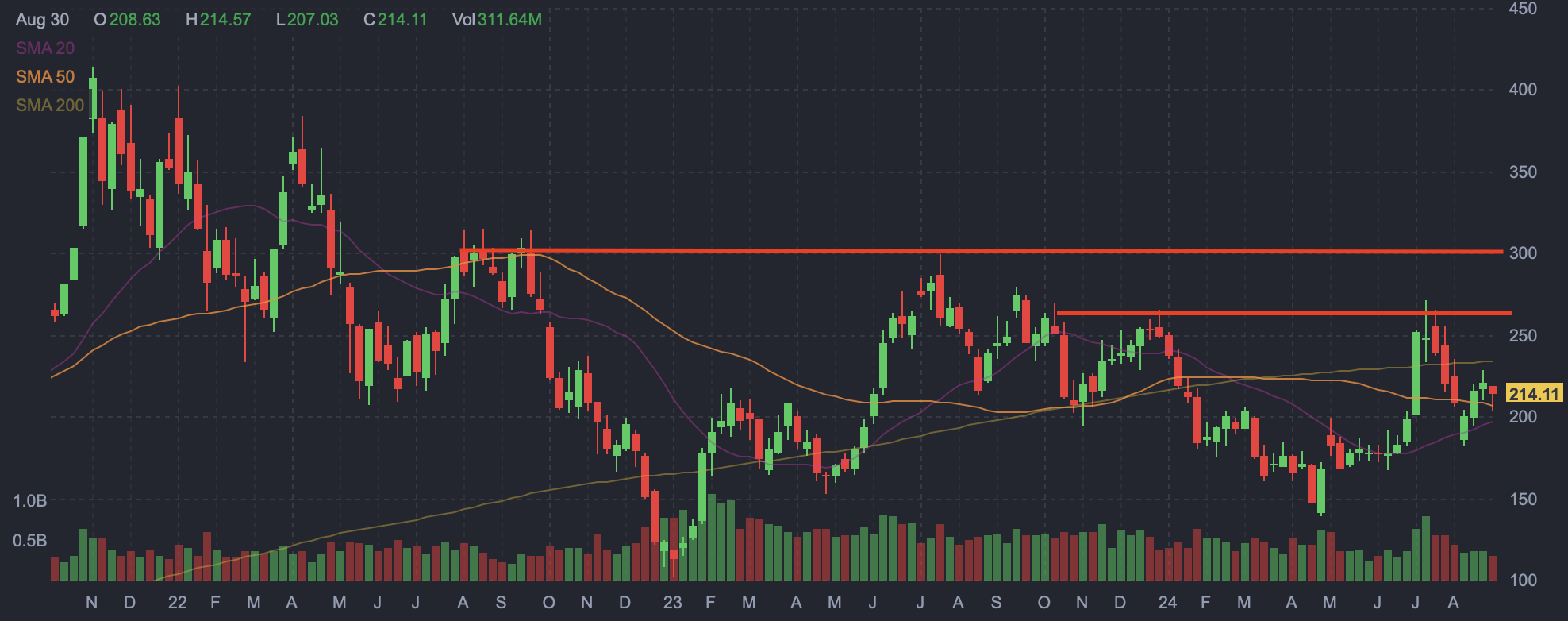

Further, shares may be able to push considerably higher. If Tesla were to appreciate to a resistance at around $260, that would appear to complete a cup and handle on the chart that has been forming since the start of 2024. If shares can break above $260 on a strong near-term move, Tesla may actually break even higher and test further resistance, which appears to be at about $300.

Tesla weekly candlestick chart (Finviz.com with red lines by Zvi Bar)

This level is also roughly in line with the $307.50 price where I believe Tesla should be valued based upon its probable auto sales plus the potential for the multiple other projects it has in house.

Risks

Risks to Tesla include possible competitive pressure from traditional automakers and new entrants, including Chinese manufacturers. Competitors are making substantial investments in developing EVs, and this competition could take market share and/or force pricing pressure that could reduce margins and result in lower-than-expected EPS. Historically, Tesla has been able to compete with domestic manufacturers by cutting prices, but this may not be possible versus Chinese manufacturers.

Tesla may also face pricing competition in the form of lost subsidies, which may be dependent upon where batteries are made. Tesla’s Model 3 contains a Chinese battery that should disqualify it from eligibility for U.S. subsidies.

The company has been an opportunistic issuer of secondaries to raise capital. While it has not recently issued a secondary offering, the company may opt to do so to fund its development plans. The probability of a secondary increases along with share price appreciation.

Conclusion

Tesla shares have had a difficult 2024 so far, but appear to be gaining traction and possibly ready to gap up higher. If TSLA shares can break out of the considerable downtrend they have been stuck within since the start of the summer, shares seem likely to test their 2024 highs at around $260. Further, if they can break through that level, shares appear capable of gapping up to $300 in short order. Such a move would not be out of the ordinary for Tesla, which has always been prone to rapid repricing following a change in momentum.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in TSLA over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.