Summary:

- Tesla, Inc. shares have dropped 20% in a month, but are still 12 times higher than pre-pandemic levels.

- Tesla is primarily an automotive company, with automotive sales comprising 80% of total revenue.

- Despite growth in the EV market, Tesla’s valuation is highly overpriced, and future earnings estimates are overly optimistic.

onurdongel

Introduction

Tesla, Inc. (NASDAQ:TSLA) shares have had a volatile month. The automaker’s one-month loss extended to 20% following Monday’s big selloff. Despite the drop, Tesla shares are twelve times higher than where they were before the pandemic. A couple of weeks ago, Tesla reported its second quarter earnings, where EPS missed expectations for the fourth consecutive quarter.

It’s been more than six years since I last talked about Tesla, and in that case, it was focused on their debt. With the recent market volatility and a selloff in shares, I wanted to examine Tesla again to see if there was a buying opportunity. Unfortunately, I found the shares as highly overvalued.

Tesla Is Primarily an Automotive Company

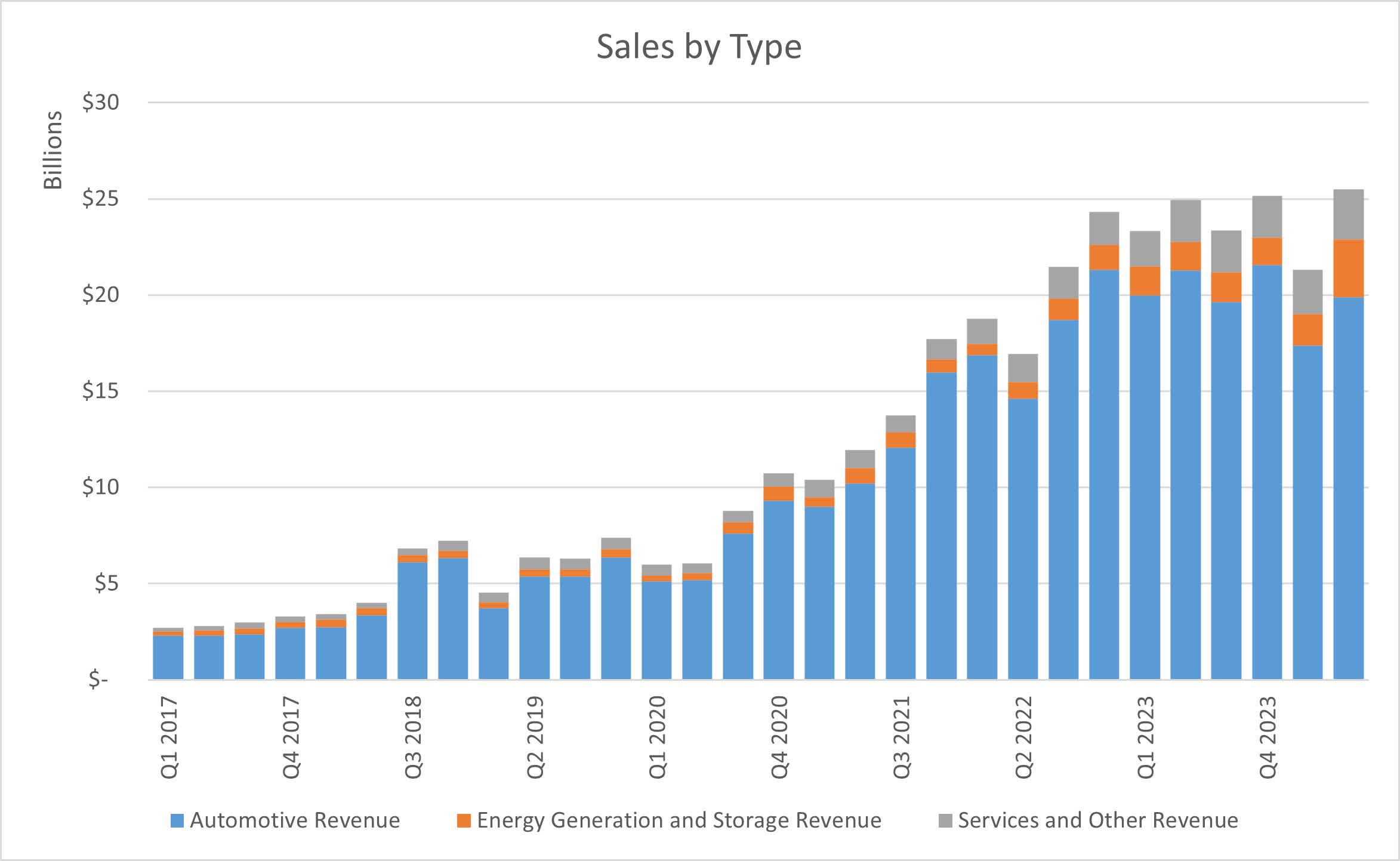

From the start of the pandemic until 2023, Tesla has had a remarkable growth run, with quarterly sales growing from just over $5 billion to $25 billion. An overwhelming majority of the company’s sales over the past seven years have come from automotive products. While investors saw a sizable jump in energy generation and storage revenue in the second quarter, it is important to note that automotive sales still comprise 80% of the company’s total revenue. Many see Tesla as a tech company with many growth opportunities, but the fact of the matter is that most of their infrastructure and plans (robotaxi, Roadster, Cybertruck, semi) center around the automotive sector.

Company Earnings

The Auto Industry is Struggling

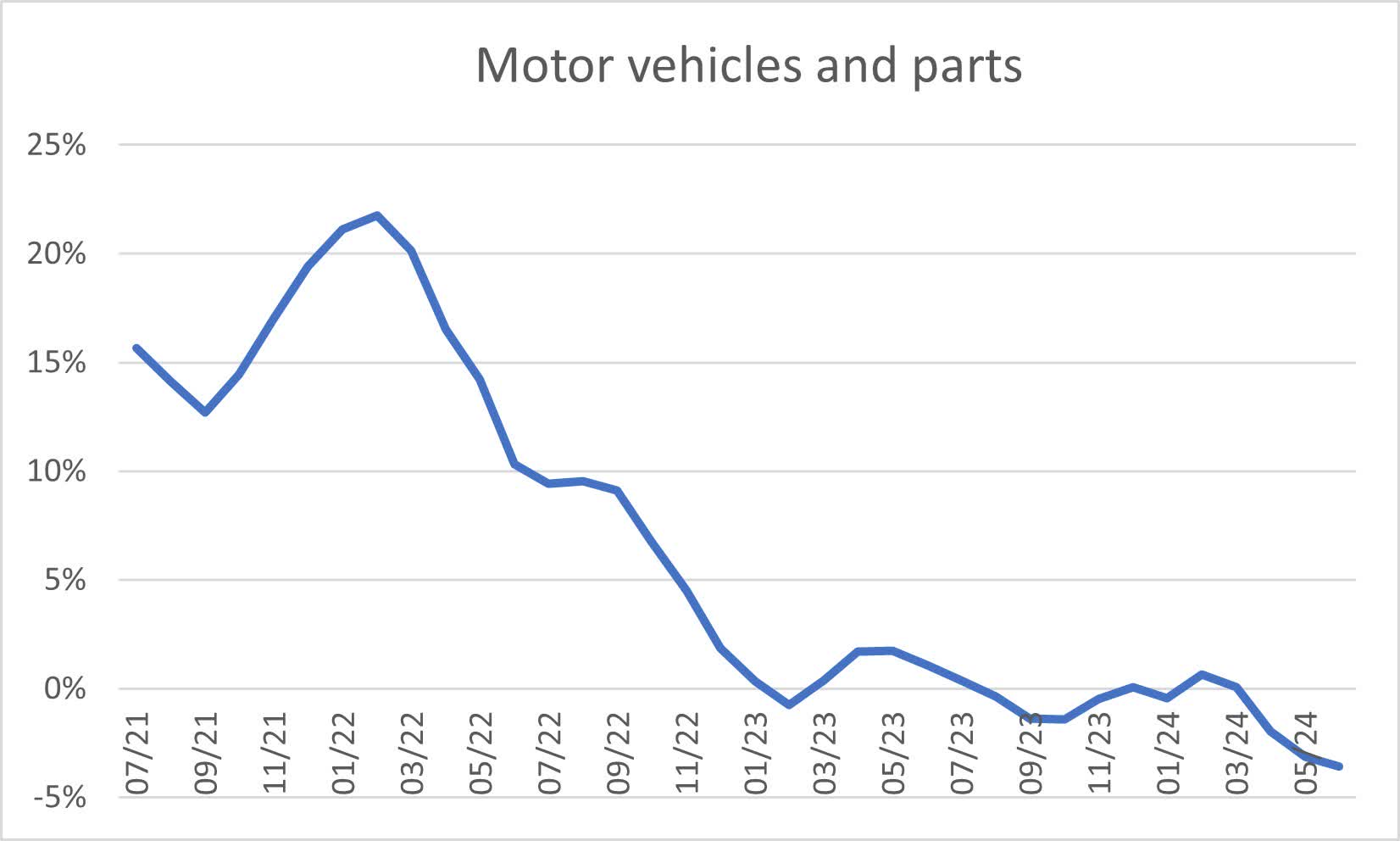

Regarding sales, Tesla has now experienced several quarters of headwinds where sales have been largely flat, dating back almost two years. A couple of reasons for this lie within the auto market itself. After a robust period of inflation within the sector (and durable goods overall) in 2021 and 2022, the auto sector has experienced two consecutive years of deflationary pressure, with recent readings nearing 5% declines year over year. Deflationary pressures within a sector increase competition and can often lead to declines in sales dollars, even if sales volumes are up.

Bureau of Labor Statistics

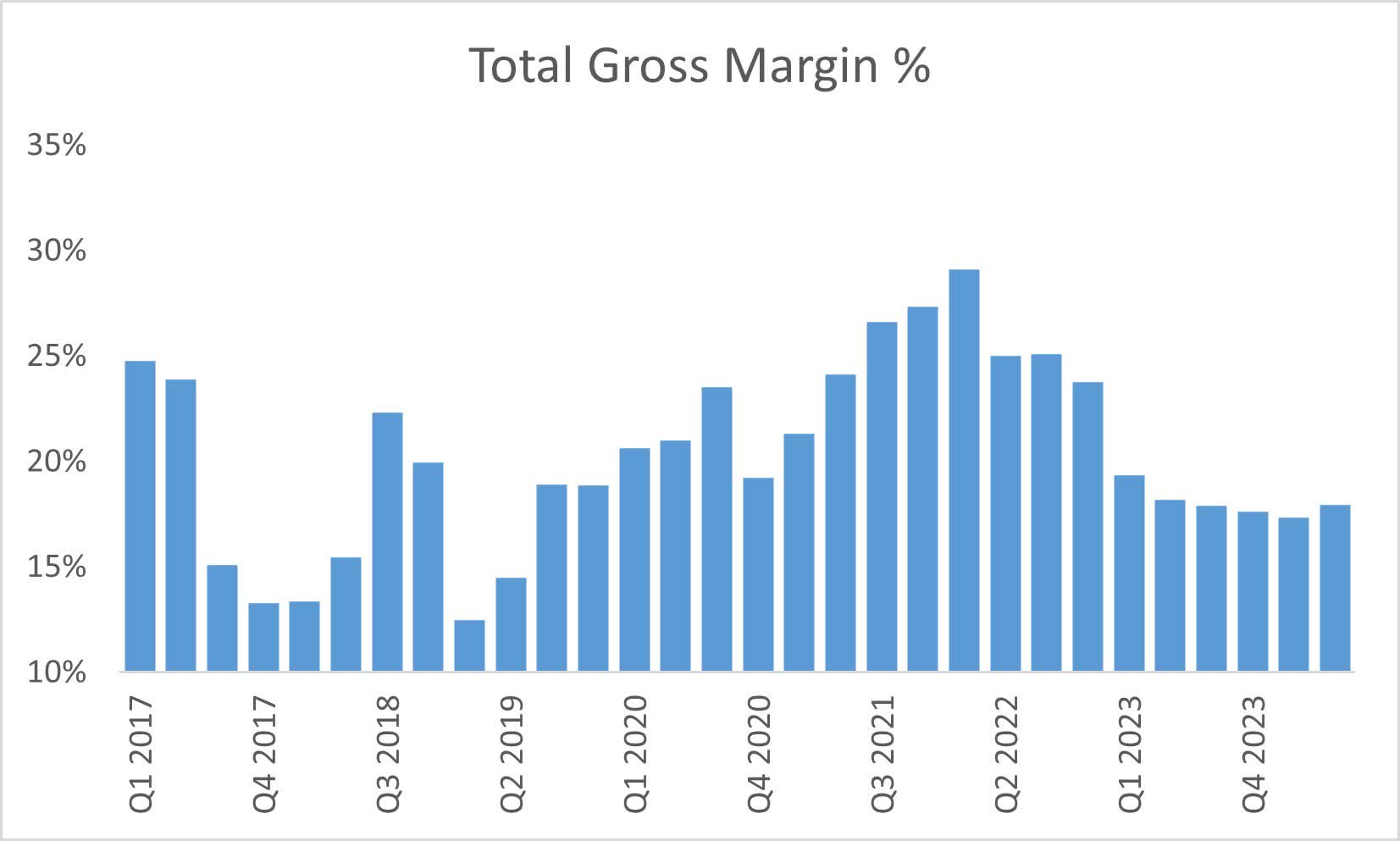

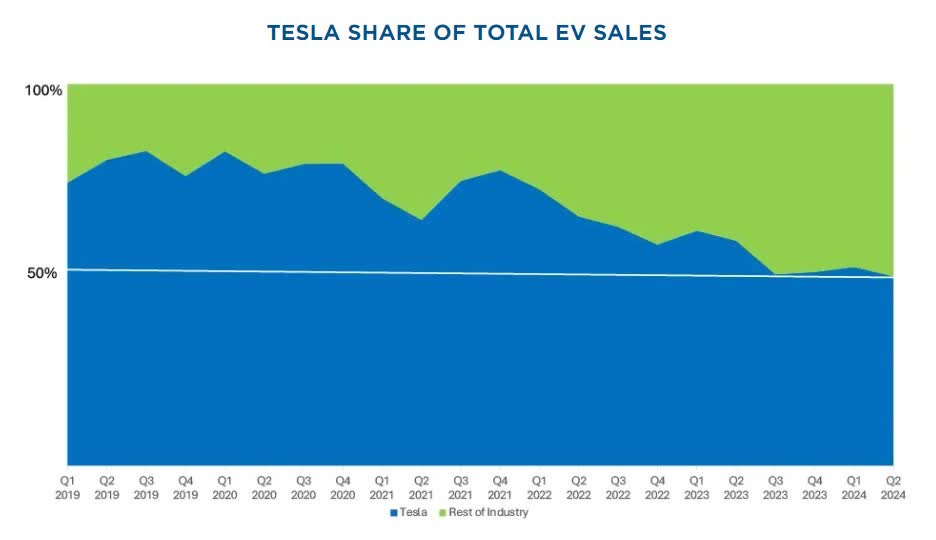

The deflationary pressures of the auto industry are not only hitting Tesla from the sales side, but the margin side as well. With production costs remaining elevated, the company has seen a notable drop in its gross margins from the high twenties down to the mid-teens. Drops like these require companies to manufacture and sell more products just to meet previous quarters’ profitability. While Tesla’s gross profit bounced back in the second quarter, it is still more than $1 billion off from the highs reached in 2021 and 2022. A combination of deflationary and competitive pressures has caused Tesla’s share of the EV market to decline, although it is still at 50%.

Company Earnings Company Earnings Cox Automotive

Two Angles to Quantifying the Hype

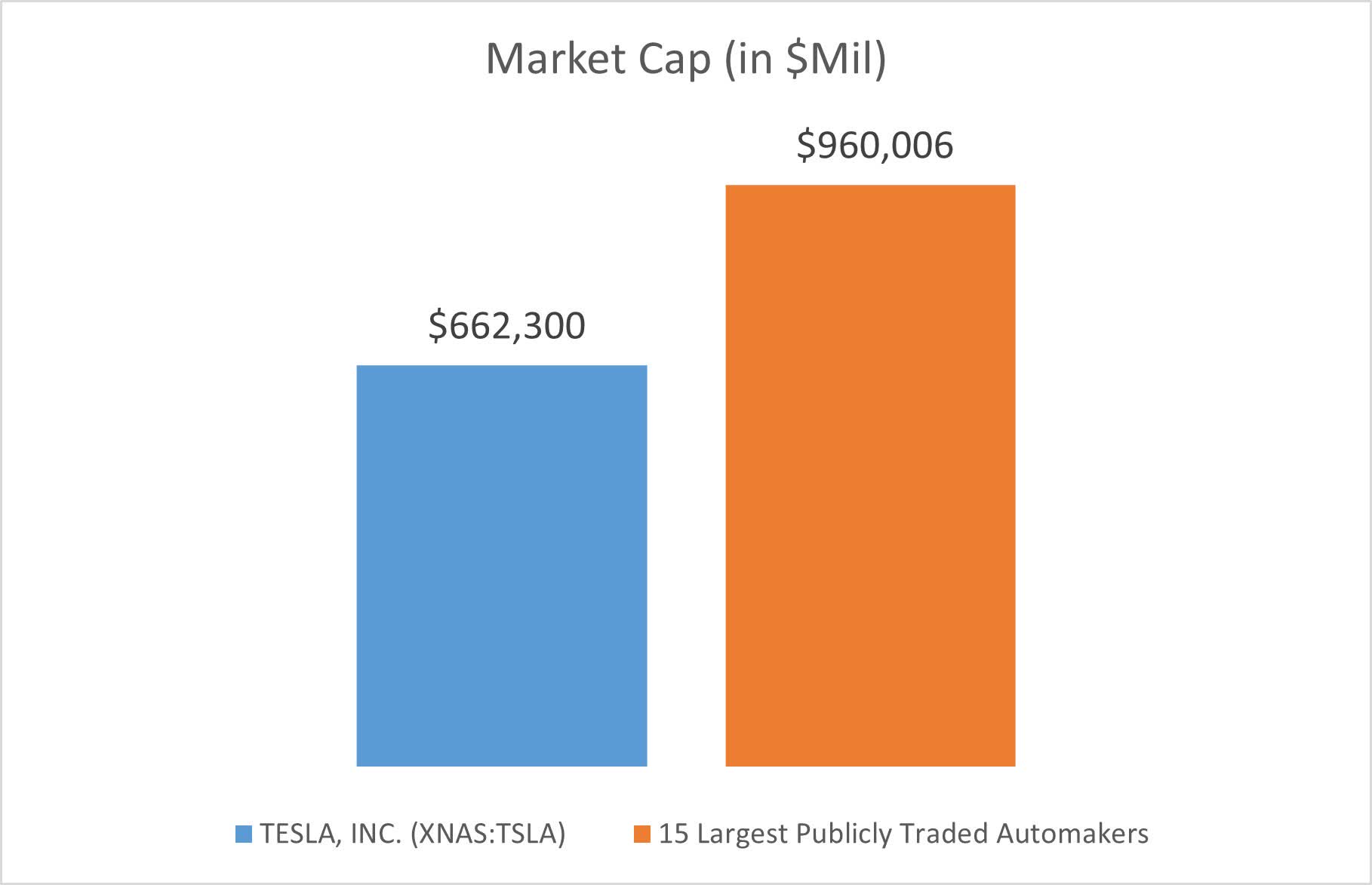

When examining the valuation of Tesla, I took a couple of different approaches. First, I examined the automotive industry without Tesla, where fifteen of the largest global automobile manufacturers comprise just under $1 trillion in total market capitalization. Tesla’s market cap is $662 billion, or two-thirds of the fifteen next largest publicly traded automakers combined.

Data from Seeking Alpha Entered Into Spreadsheet

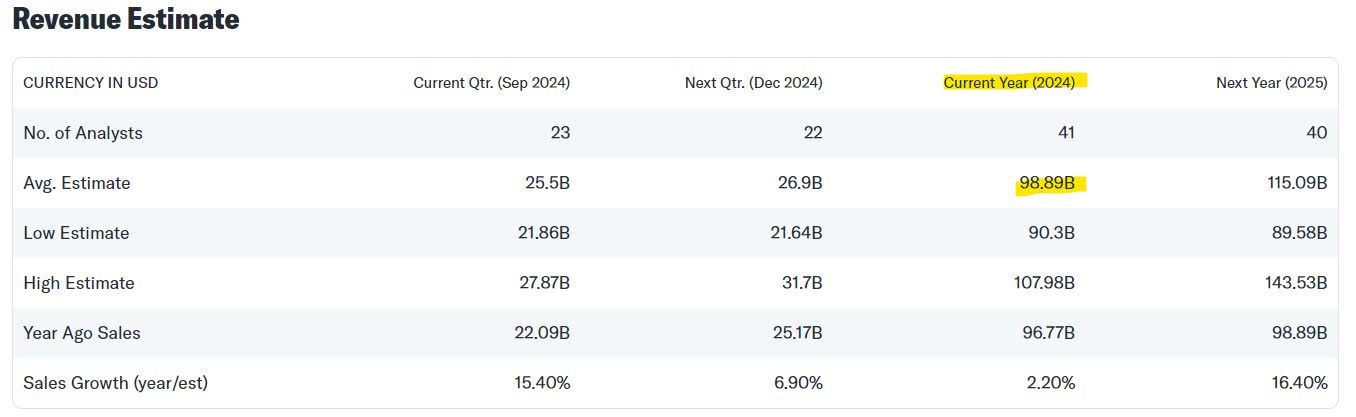

The other area I looked at was forward earnings estimates and how they sized up over time. As of earlier this week, Tesla’s 2024 earnings per share were forecasted to be $2.34 with analysts estimating just under $100 billion in revenue. Back in February 2023, analyst estimates for 2024 earnings per share were $5.56 and revenue estimates were nearly $134 billion. In 18 months, earnings per share expectations declined by nearly 60% with revenue estimates down 25%.

Yahoo Finance Yahoo Finance Yahoo Finance via Wayback Machine

There’s Still Hope

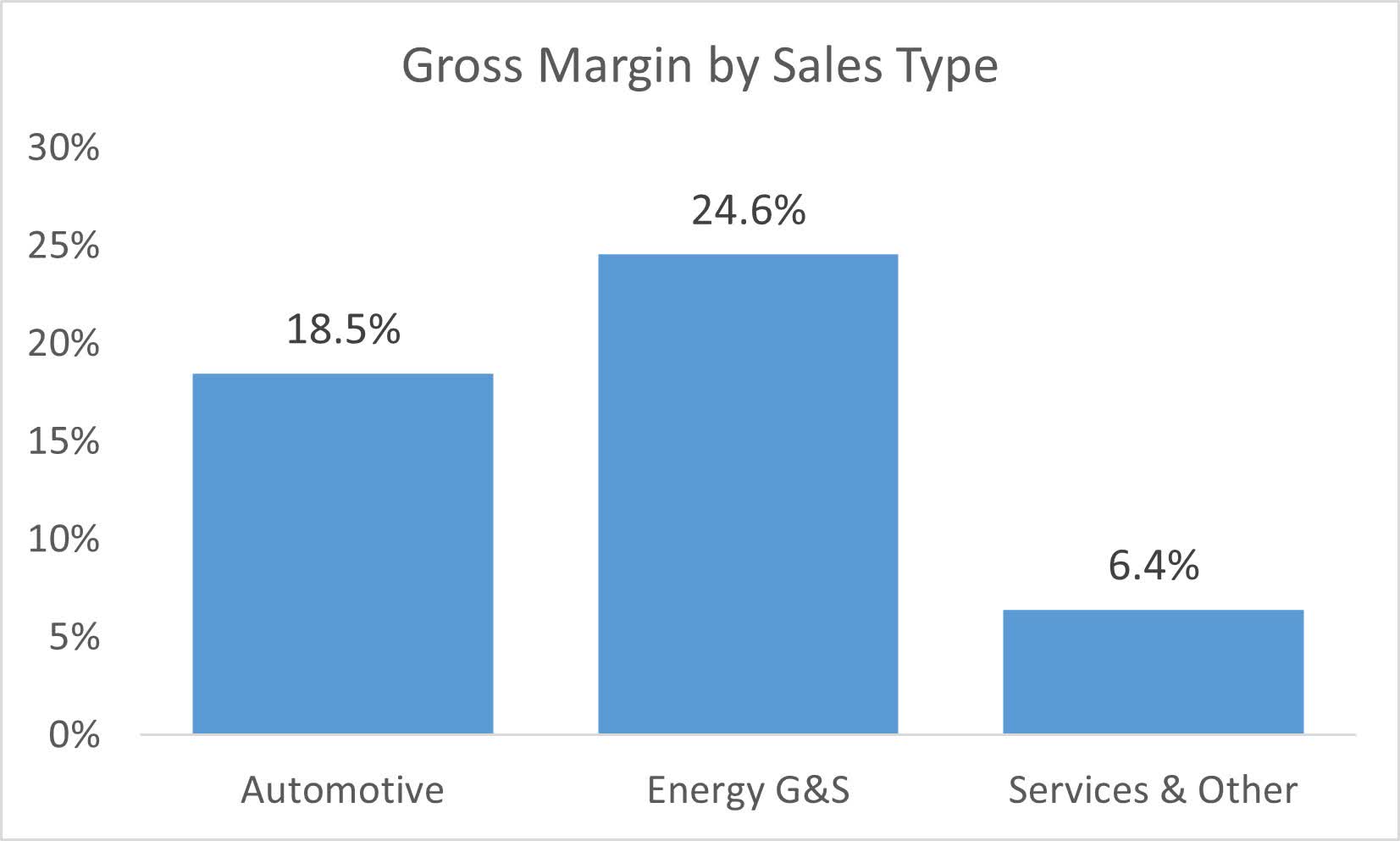

Not everything looks negative for Tesla. Despite some of the bad press that EVs and hybrid vehicles have been getting in the news, the EV market continues to grow. Year-over-year growth in electric vehicle sales continues to exceed 10%, and electric vehicles are taking a share in the overall automotive market. In addition to the automotive market, Tesla is starting to see results in energy generation and storage sales. This product line currently carries a higher gross margin than the automotive line and could become a source of profit growth for the company.

Company Earnings

Risks to Tesla

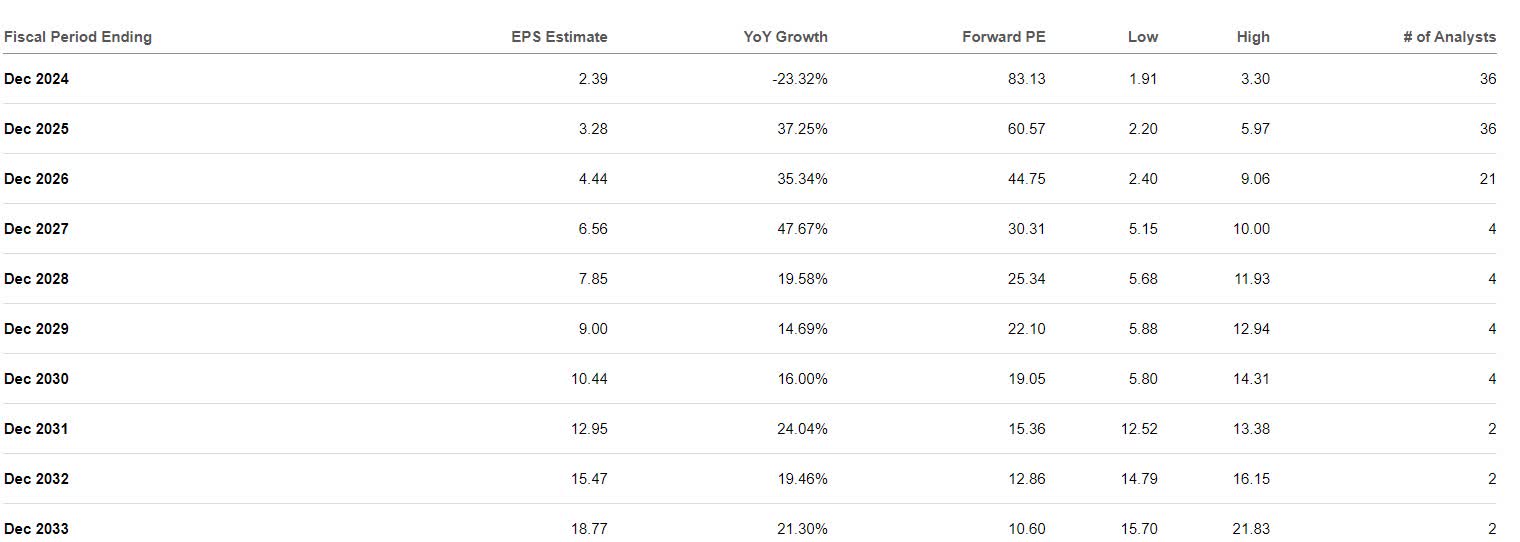

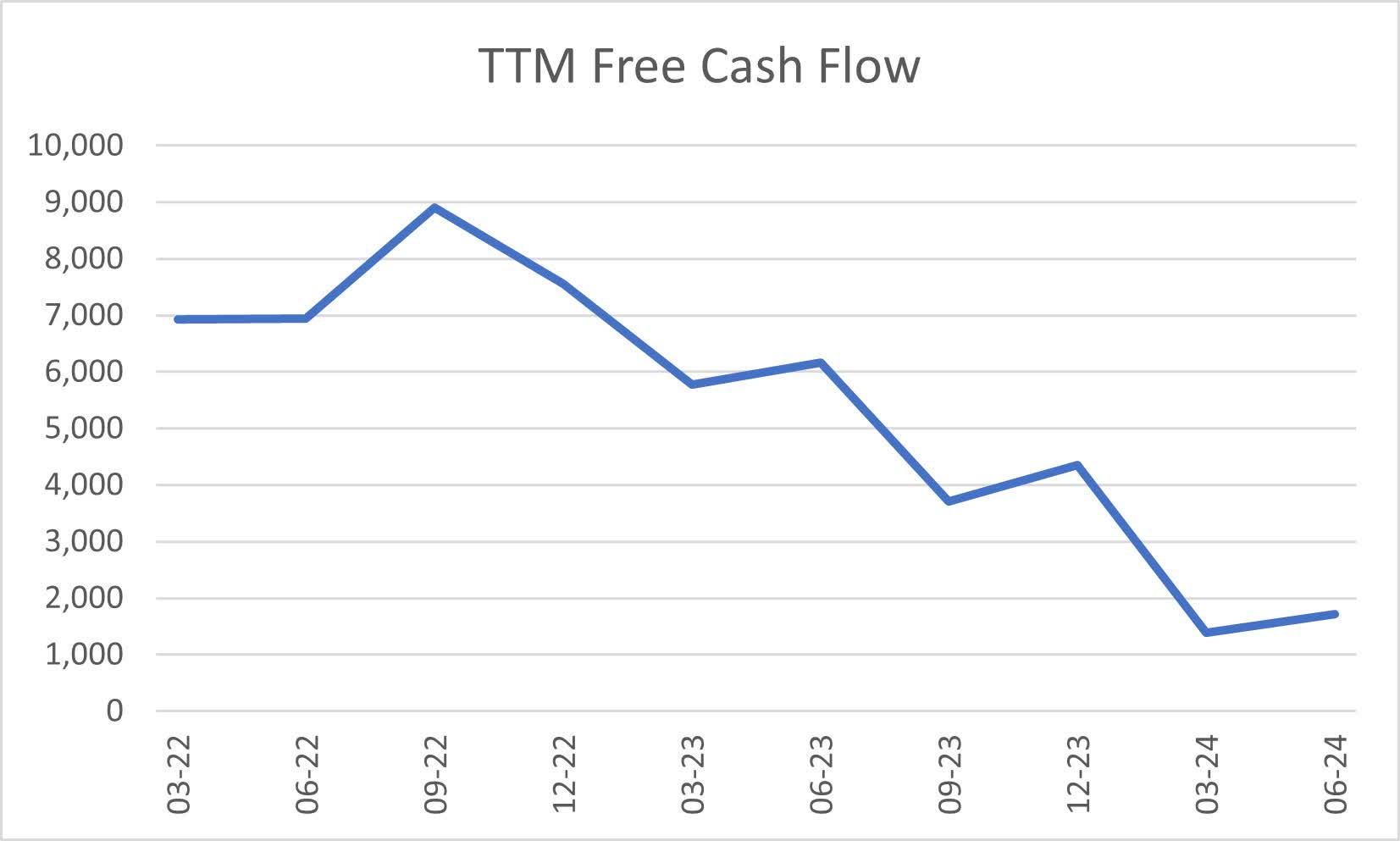

Despite some progress in diversifying sales and trying to improve gross margins, there’s still far too much optimism to justify an entry in Tesla shares at these levels. Just like in early 2023, analysts are pushing rosy earnings estimates for Tesla over the next ten years. Even if Tesla succeeds in more than tripling its 2024 earnings by 2029, the stock is still trading at 22 times those levels. These estimates become even more irrational as Tesla’s trailing twelve-month free cash flow has gone from $9 billion to under $2 billion in less than two years.

Seeking Alpha TIKR

In addition to optimistically euphoric earnings estimates, investors need to be mindful that Tesla is still primarily an automotive company whose success is tied to the success of the automotive market and the American consumer. Should the economy weaken, unemployment rise, and consumption drop, there’s no doubt that EV demand will take a hit. While the short position may seem like a “no-brainer,” I am opting to not take a position as Tesla appears to be the ultimate meme trade and is subject to future volatility that could hurt buyers or short sellers. A better strategy for investors here would be a bear put spread on options.

Conclusion

Tesla is a profitable company with a good balance sheet, but its valuation is way ahead of its time. Risk factors like a recession, which could reduce consumer spending and automotive demand, are too great to ignore when examining a stock trading at such a high earnings multiple. With volatility expected in the stock market related to the economic outlook, investors should expect volatility in Tesla shares to be greater than the market.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.