Summary:

- Tesla, Inc. stock has gone on a rampaging run as it took out a new high this week.

- TSLA’s enthusiasm is predicated on a more permissive federal regulatory regime for self-driving vehicles as Trump returns to office.

- Tesla still needs to overcome several critical hurdles before it can even scale its robotaxi business, indicating significant execution risks.

- Investors have thrown caution to the wind as TSLA’s forward-adjusted PEG ratio surpassed 19.

- I argue that while TSLA’s upward momentum seems incredibly strong, its surging run could end sooner rather than later.

Xiaolu Chu

Tesla, Inc. (NASDAQ:TSLA) investors have had a lot to celebrate lately, as the stock of the Elon Musk-led company surged to a new high this week. As a result, it has outperformed the S&P 500 (SPX, SPY) significantly since Tesla’s Q3 earnings release on October 23, 2024. TSLA’s spectacular rise to the top has coincided with the victory of President-elect Donald Trump in the recent presidential election in early November. In addition, Elon Musk has secured a key (albeit informal) role as one of the co-chiefs of Trump’s Department of Government Efficiency, demonstrating his increasing influence within Trump’s inner circle. Hence, the market has raised its optimism about Tesla’s ability to secure a less onerous regulatory environment from 2025 as the EV leader seeks to build and scale its autonomous driving ambitions.

In my previous Tesla article, I highlighted why TSLA’s Q3 earnings release suggests the worst is likely over. However, the stock’s meteoric rise since then has likely stunned even bullish forecasters, even as Wall Street’s average price targets on TSLA have struggled to keep up. However, the market seems to have thrown caution to the wind, as TSLA’s forward adjusted EPS multiple shot above 161x. Arguably, the market has attempted to price Tesla’s long-term potential in its robotaxi business which Ark Invest estimates to account for “nearly 90% of Tesla’s enterprise value and earnings” by 2029. Trump has likely helped set the recent rally going for Tesla, as he highlighted that he would prioritize the setting up of a federal-level framework for the development of self-driving vehicles, led by the DoT. Bullish Tesla analysts have added fuel to the fire, assessing that it could pave the way to accelerate Tesla’s full-scale deployment of its robotaxi network.

Notwithstanding the market’s incredible optimism built on the recent developments, I urge investors to exercise extreme caution. In Tesla’s core automotive business, it still faces significant pressure to deliver 515K vehicles in Q4 to avoid falling into a YoY decline in deliveries for the full year.

While the company has made notable progress in China, the competitive environment has heightened recently, as BYD Company Limited (OTCPK:BYDDF) has upped the ante against its Chinese EV peers. Therefore, Tesla faces significant challenges in its biggest overseas market, which could scupper a more robust delivery growth outlook for 2025. The EV penetration rate in the US market remains far below that of China. However, it’s increasingly likely that the $7.5K EV credit could be scrapped after Trump returns to the White House. Hence, it is expected to hamper the growth rate of the overall EV market from 2025.

However, the market’s optimism suggests investors are confident that Tesla could fare more favorably than its legacy and pure-play EV peers. I believe that optimism isn’t entirely misplaced, given its market-leading scale and profitability. Hence, Tesla remains well-placed to outcompete its US rivals based on its massive capacity. As its rivals struggle with their unprofitable EV businesses, the elimination of the EV credits is expected to impede their transition, potentially handing back the market advantage to Tesla. Hence, the outlook for Tesla in 2025 is assessed to be mixed at best, given the intensely competitive environment in China, worsened by BYD’s competitive clout.

Moreover, Tesla’s ability to secure expedited federal approval for its robotaxi business remains highly uncertain. Even if it does so, Alphabet Inc.’s (GOOGL), (GOOG) Waymo seems to have pulled ahead, as Waymo has scaled up its robotaxi offerings to more US states. Moreover, Tesla could face hurdles in obtaining the necessary state permits even as it seeks to offer L3 services in Texas and California in 2025. I believe the market has raised optimism about Tesla’s potential success as General Motors Company (GM) has exited the robotaxi market, assessing that it’s no longer a core business for GM to focus on. Therefore, Tesla and Waymo are expected to be the leading players in a potentially highly lucrative robotaxi market if they can scale it effectively. Despite that, execution risks are incredibly high, as the business model is unproven. Is it really worth paying that much for TSLA’s potential in autonomous driving based on Trump’s declaration to prioritize a federal self-driving framework?

TSLA Quant Grades (Seeking Alpha)

There’s little doubt that TSLA’s forward-adjusted PEG ratio of 19.7 is extremely optimistic. Hence, investors have baked highly optimistic scenarios over the coming years, as Tesla expects to lift its core automotive sales from 2025. In addition, the market seems to have assessed the increased viability of Tesla’s autonomous driving ambitions, attributed to Musk’s potentially stronger influence in Trump’s inner circle. Hence, TSLA’s momentum has surged to “A+” from “D” over the past six months. In addition, analysts have also upgraded their estimates on Tesla, assessing more robust execution through 2025.

Notwithstanding its industry-leading scale and profitability, the optimism in TSLA has reached “stratospheric” levels. Hence, less-than-perfect execution on Tesla’s automotive business recovery prospects in 2025 and regulatory and technological hiccups on its autonomous driving ambitions could delay its deployment further. The market seems to have overstated Tesla’s ability to scale its robotaxi segment quickly, which could offer significant benefits to its operating income. However, I urge investors to consider that such significant benefits could accrue only through the end of the decade, underscoring the immense execution risks for Tesla to reach that level.

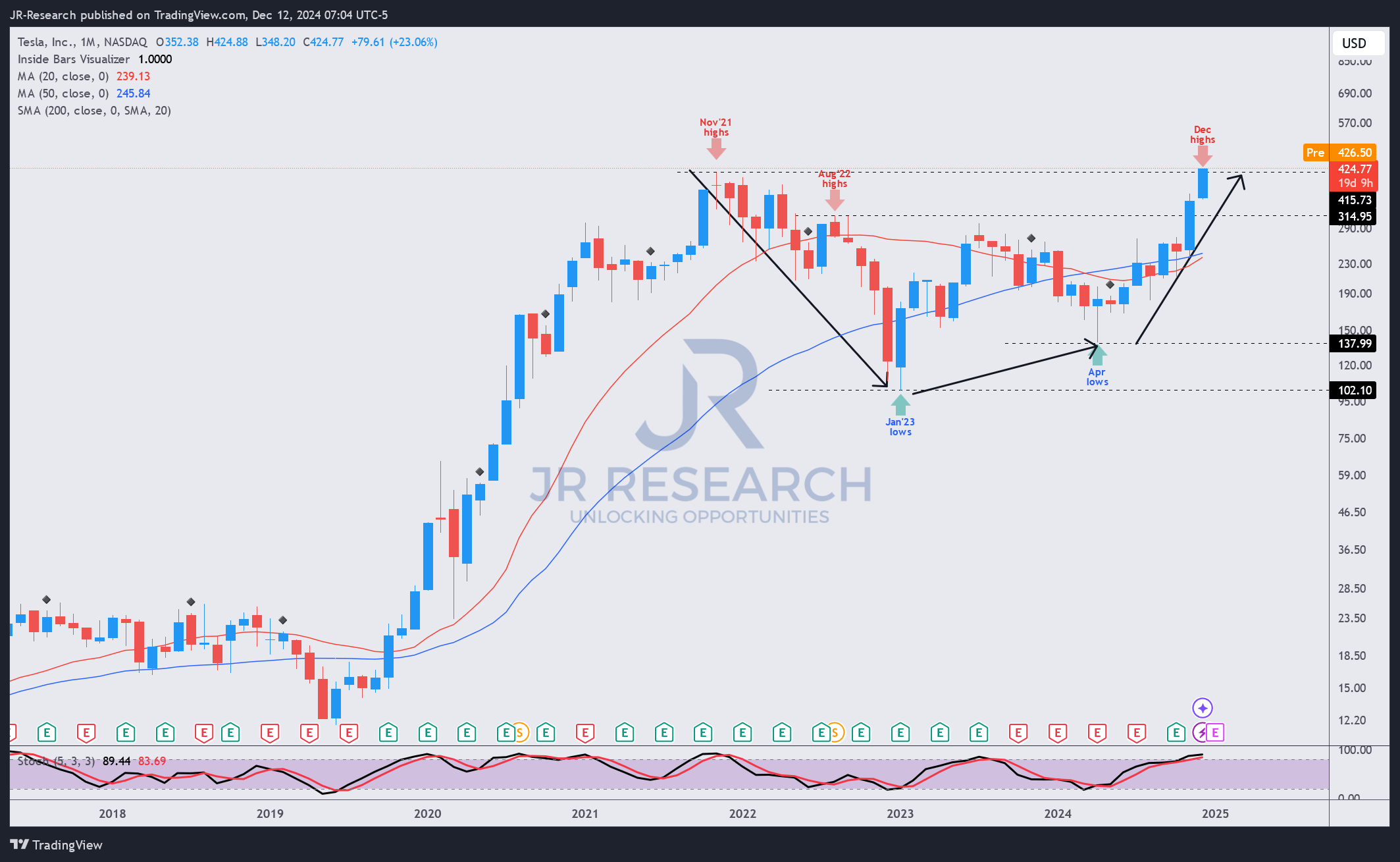

TSLA price chart (weekly, medium-term) (TradingView)

TSLA buyers have regained control of its long-term, bullish narrative, as seen in its price chart above. Its April 2024 bottom has been defended stoutly, over and above its January 2023 lows. In other words, sellers are nowhere to be seen, as TSLA’s short interest ratio remains below 3%. However, it’s also critical for investors to note that the last time TSLA’s forward EPS multiple surged above 150x was in November 2021, before it peaked.

Hence, investors who are considering buying into TSLA’s breakout thesis need to assess whether they are confident about its ability to reignite its growth momentum over the coming years. Its “C-” growth grade hasn’t changed over the past six months, suggesting the recent surge is likely attributed to a valuation re-rating based on the successful deployment of its robotaxi business through the decade. However, GM’s experience suggests it’s coupled with significant execution risks on a business that was considered core just a few years back. Therefore, it seems premature for the market to go on a rampaging run and lift TSLA’s earnings multiples to such high levels.

As a result, I assess that the risk/reward on TSLA stock is increasingly skewed toward the downside. I urge investors to consider taking profits if they have managed to partake in its recent surging run.

Rating: Downgrade to Sell.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Consider this article as supplementing your required research. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing, unless otherwise specified.

I Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

A Unique Price Action-based Growth Investing Service

- We believe price action is a leading indicator.

- We called the TSLA top in late 2021.

- We then picked TSLA’s bottom in December 2022.

- We updated members that the NASDAQ had long-term bearish price action signals in November 2021.

- We told members that the S&P 500 likely bottomed in October 2022.

- Members navigated the turning points of the market confidently in our service.

- Members tuned out the noise in the financial media and focused on what really matters: Price Action.

Sign up now for a Risk-Free 14-Day free trial!