This note serves to convey and communicate my distilled perspective of Tesla, Inc.

I will discuss my partnership with the company, its positioning relative to (alleged) competitors, and what I believe to be the most salient components of our Tesla thesis.

Because I believe Tesla is currently the coolest brand on earth bar none, I am excited to share these ideas with you.

To be very precise, Teslas currently drive themselves about as well as a teenager learning to drive. That said, FSD has improved over the years, and we believe it will continue to do so, and we believe it to be an accurate statement that “Teslas drive themselves,” though the product is certainly not perfect, hence the current title: “Full Self Driving Beta”

Spencer Platt

My Partnership With Tesla

I believe dissecting my 3.5 year partnership with Tesla, Inc. (NASDAQ:TSLA) would be a very worthwhile use of our time together today, in that my partnership sheds light on how I think about businesses within my business of owning businesses and, of course, Tesla specifically.

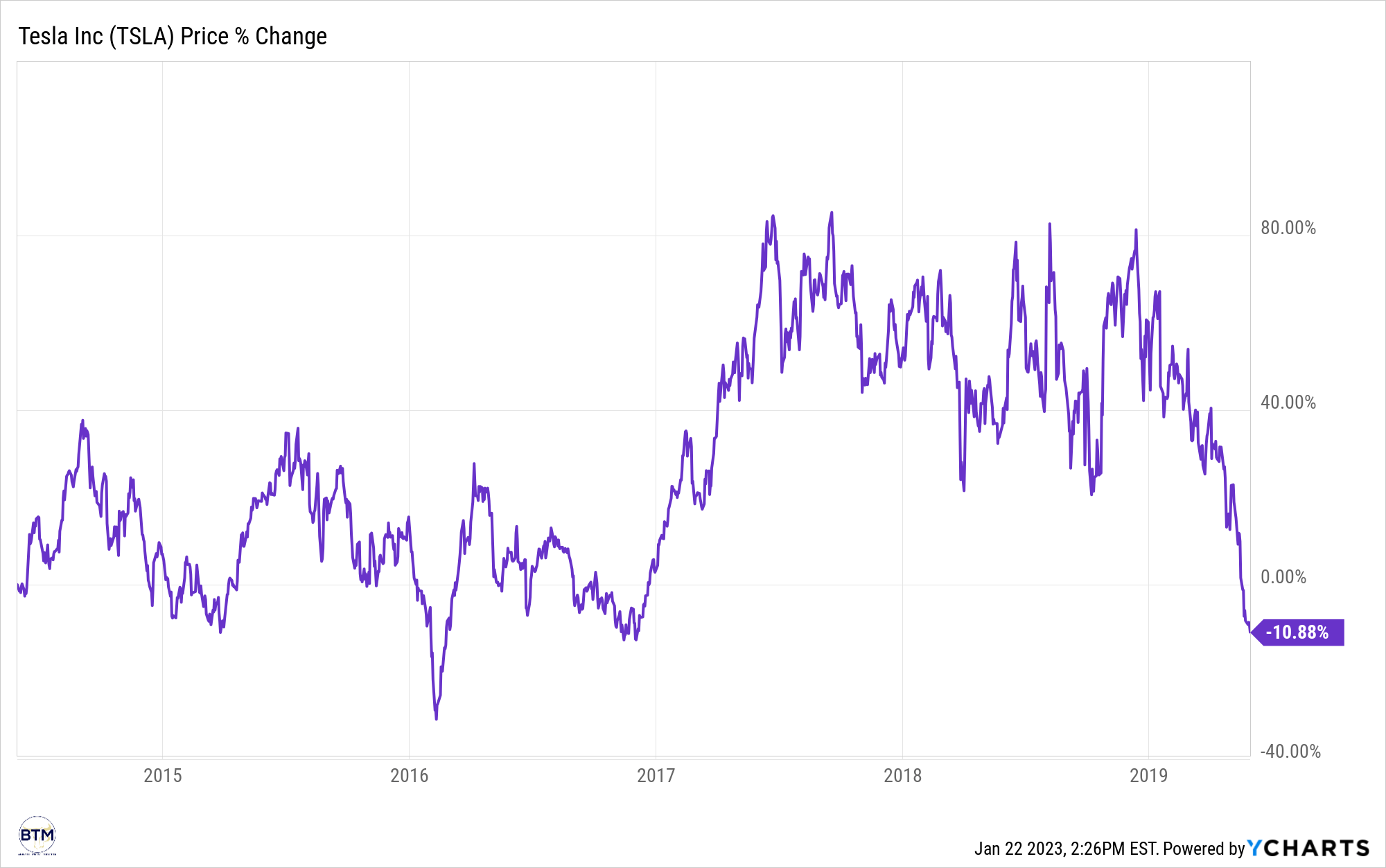

In the summer of 2019, Tesla’s share price was in free fall. The stock had stagnated for nearly a half decade; at the end of which, it entered into this free fall.

Total Return For Tesla Stock (June 1st, 2014 – June 1st, 2019)

YCharts

Of course, this free fall did not occur in a vacuum. The company had a large tranche of convertible notes at a ~$350/share strike price, and it had neither the stock price nor the cash to satisfy the obligations of these convertible notes; hence, the stock entered a free fall.

Famed for correctly identifying the Enron fraud, short seller Jim Chanos boisterously announced his short position in Tesla, sending the stock down even further.

Tesla is and remains one of our biggest and our best short positions… We are still bears.

At the time, true to my mindset today, I assessed Tesla’s financials completely independently to see what I myself could divine.

The thesis I devised was really quite simple at the time (it’s still simple but a bit more involved today): I determined that Tesla had begun producing free cash flow in the few quarters prior to the summer of 2019, and it had exceptional growth, and, to this end, I began accumulating shares of Tesla within my business of owning businesses. Notably, while Tesla generated free cash flow in late 2018 and early 2019, it still did not generate GAAP profits (net income).

We detailed this incredible period in Tesla’s history, as well as my investment in the company, in the following note from approximately early 2020:

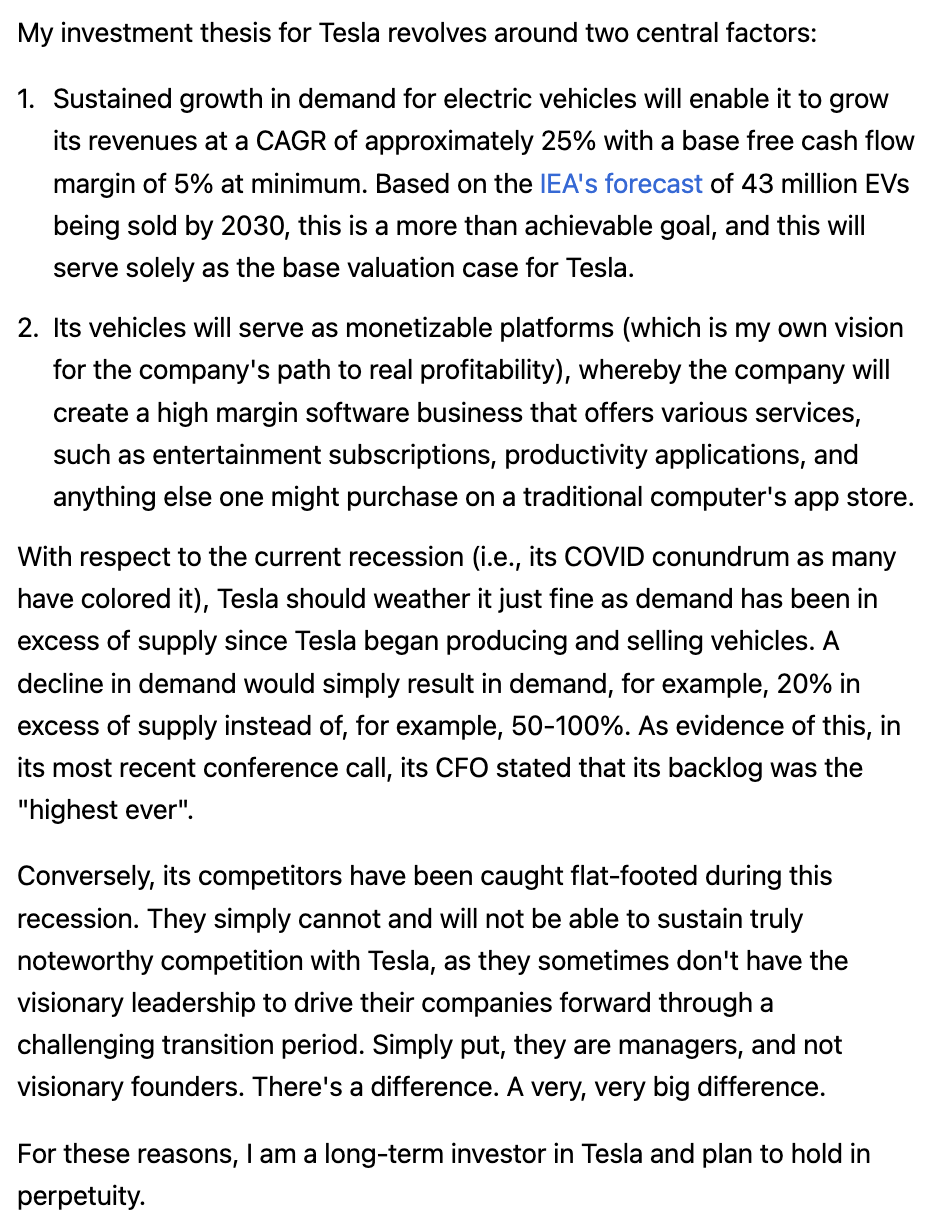

Within that note, we delineated our thesis for Tesla:

Beating The Market’s 2020 Tesla Investment Thesis

Author’s Creation

Of note, from our thesis for Tesla to our perception of competition, virtually nothing has changed as of today relative to what we asserted in our 2020 notes, and we will succinctly delineate as much in just a moment.

If anything, we’ve become even more emboldened now that TSLA stock trades at a valuation closer to where we purchased it in 2019 and again in May of 2020.

Assessing The Pillars Of Our Long-Term Tesla Thesis

Our thesis could be simplified into just three pillars as of today:

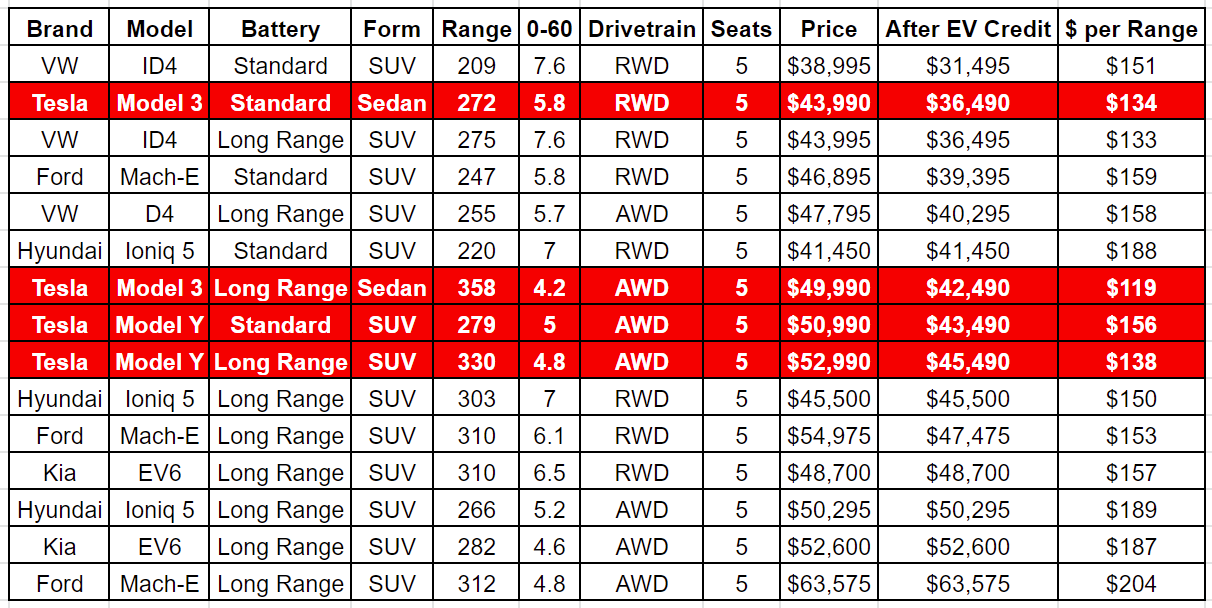

Tesla EVs (electric vehicles) still have no competition… mathematically speaking. Tesla’s competition still has not caught up to it in range/$, total range, Supercharger infrastructure, and acceleration, and this is no longer the game. The game is now FSD (full self-driving), and Tesla’s competition hasn’t even begun trying to catch up to Tesla here!

Tesla Energy could be as large, if not larger, than Tesla Legacy [EVs], though this is not being priced into the stock in any sense whatsoever. We identified the storage problem, which Tesla Energy addresses, in TGSGT VII, which we published in mid-2020.

Tesla is hands down the strongest it’s ever been from a variety of perspectives, e.g., total cash balance, the completeness of the FSD product, the ability to create Megapacks (formerly battery constrained), total number of products, etc.; notwithstanding this reality, Tesla now trades at one of its most depressed valuations in the history of the company. We contend that this represents “The Greatest Irony,” which, as we mentioned recently, could be rebranded as “The Greatest Opportunity.”

As we shared a moment ago, our 2020 Tesla investment thesis has solidly stood the test of time. We were too conservative in our estimation of margins in point one, but point two remains very much at the heart of our investment thesis for the company, and we believe more than ever that the U.S. government has created fertile ground for total annihilation of Tesla’s competition (though it believes it’s doing the opposite). We will discuss this further later today.

I articulated this “withstanding of time’s test” in the following manner earlier today in the Beating The Market chats:

Our Investment Thesis For TSLA in Early to Mid-2020

Author’s creation

Our Investment Thesis for TSLA in Early 2023

Author’s Creation

Let’s now walk through each of the above-mentioned three pillars.

Our First Pillar: The Tesla EV/FSD Thesis

For our first pillar, all that has changed, as of today, is that we now have more robust, tangible data with which we can more precisely articulate our thesis. There’s also now Tesla Energy, which could be larger than Tesla’s current entire $80B EV/FSD business.

For instance, we stated in our original thesis, “Its vehicles will serve as monetizable platforms…”

A completely valid response would have been at the time, “Great, show. me. the. money.”

And, at the time, we couldn’t fully do so, but, as of today, we could certainly oblige!

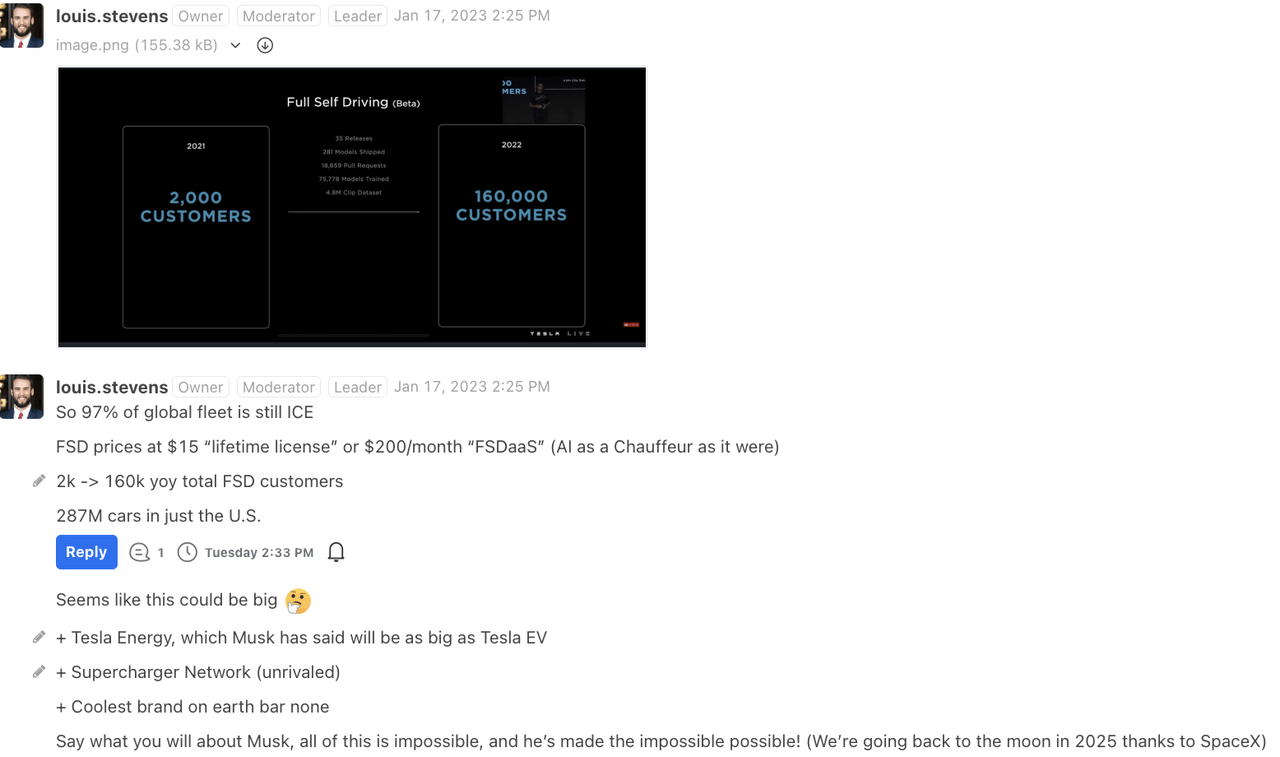

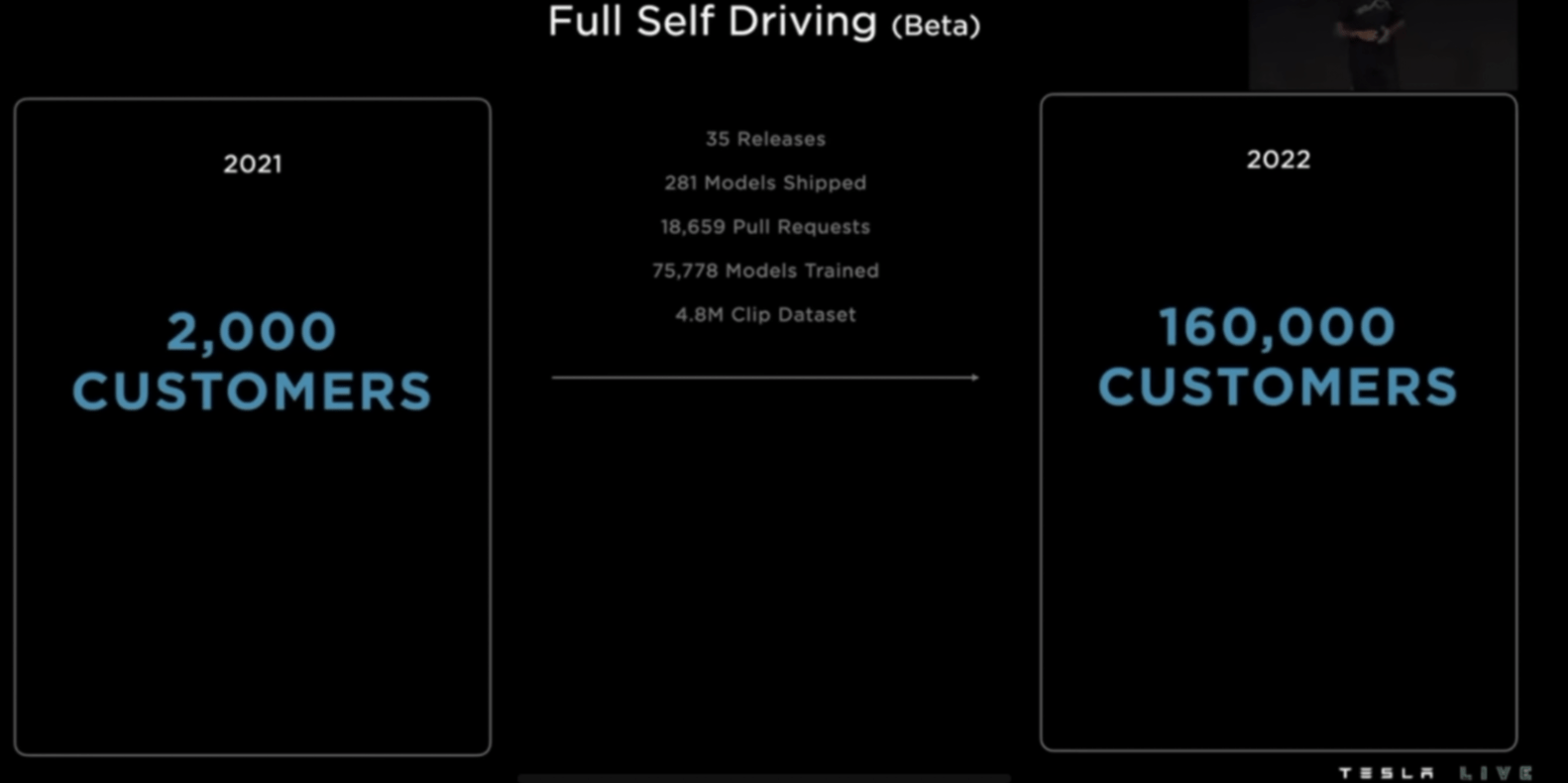

Total FSD Customers

Tesla FSD Day

As can be seen above, in 2020, FSD was extremely limited, but it has experienced meteoric, exponential growth, in line with our 2020 thesis, which we articulated a couple times earlier in this note.

This is fantastic, especially when we consider the cost of this product; however, Beating The Market believes we’ve barely even begun.

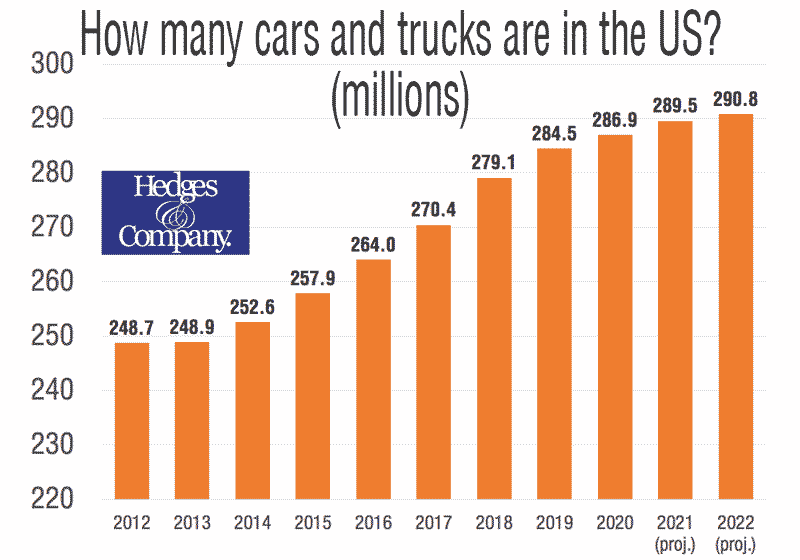

As the above screenshot asserted, 97% of earth’s vehicle fleet remains ICE (internal combustion engine). In the U.S. alone, there are 290M total cars on the road, and this number will continue to grow.

Total Cars On The Road In The U.S.

Hedges & Company

We could imagine a scenario where 290M total cars grows at about 1.25% annualized for the next 10 years.

This would imply that the U.S. would have 328M total vehicles on the road by 2033.

Let’s say Tesla captured just 20% of the total vehicles on U.S. roads by 2033, and let’s say 80% subscribed to FSD. Let’s further assume that FSD costs less by 2033 at just $100/month or $1,200/year (currently $200/month or $2,400/year).

This would create $65B in very high margin software revenue for Tesla, and this does not include international revenue.

And there’s also Tesla Premium Connectivity, which is $10/month, which will be massively aided by Starlink, in which we’ve invested via Shift4 Payments, Inc. (FOUR). You may learn more about this investment here.

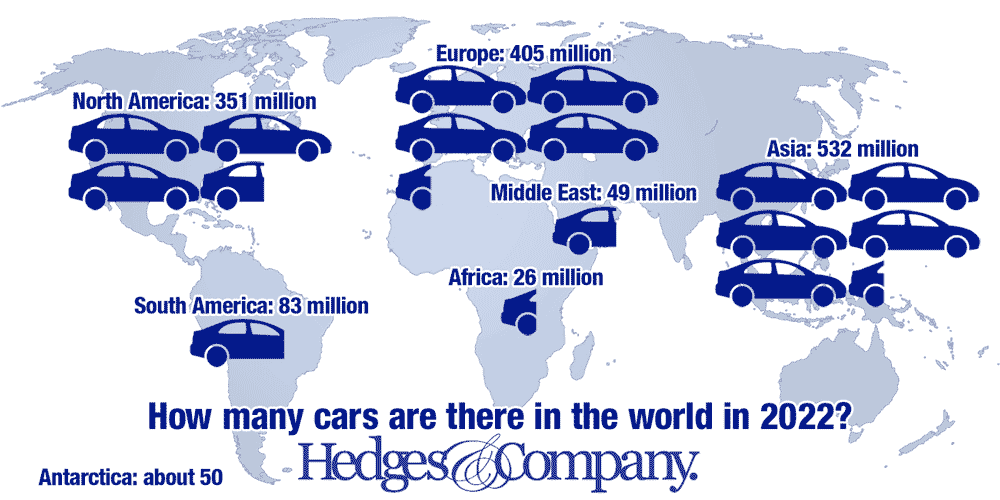

Total Cars On The Road In The World

Hodges & Company

Of course, Beating The Market, at least in the near term, is most interested in the U.S. market, as it represents the “Holy Grail” for Tesla.

But we could quite easily imagine scenarios where Tesla has 100M+ FSD subscribers globally at some point in the 2030s, and this would entail likewise huge revenue/free cash flow for the company.

Now, our FSD thesis alone could be the entirety of Beating The Market’s thesis for Tesla, but our thesis certainly does not stop there.

This does not include Tesla Energy.

This does not include Tesla’s unrivaled Supercharger Network and the optionality around that business.

This does not include Tesla being hands down the coolest brand on earth.

Tesla has single-handedly ushered in the sustainable energy revolution. This has been something all have either been too incompetent to accomplish or too fearful.

Musk and the team at Tesla have done it.

Earth’s fate has been forever changed by Tesla, and we should, as a global community, appreciate this reality for what it is (really effing cool).

Our Second Pillar: The Tesla Energy Thesis

Like our thesis for Tesla’s vehicles, our “sustainable energy” thesis has likewise largely stood the test of time. We delineated this thesis in a note that I will share with you in just a moment.

If you’d like to learn more about Tesla Energy, Beating The Market would invite you to watch the video contained in the Tweet below (we’ve shared videos from The Tesla Space often in the past).

If you’d like an even more in-depth exploration of the problem Tesla Energy solves, we’d invite you to read our work on the sustainable energy revolution, which I like to call, “I can breathe freely without having to inhale the exhaust of my neighbor’s car” revolution.

As I mentioned a moment ago, like our thesis for Tesla’s legacy business [EVs], our thesis for “the central problem in the sustainable energy revolution” has very, very much stood the test of time. In TGSGT VII, we shared,

An Excerpt From TGSGT VII

Author’s Creation

And, of course, Tesla’s Energy business principally solves the storage problem via its battery technology in conjunction with its software and AI acumen, which will invariably serve as essential components of the sustainable energy future, and we shared as much in TGSGT VII.

Musk Comments On Tesla Energy Business On Tesla’s Q3 2022 Earnings Call

Tesla Q1 2023 Earnings Call

Palantir Technologies Inc. (PLTR) did a fantastic job of illustrating the need for robust AI and software in a sustainable energy future in the following video:

As with Tesla FSD, while there’s scantly any data to share with you today for Tesla Energy, we’re fairly confident that we will see robust data shared in the next 36 months, as the recession opens up even greater battery capacity to fulfill demand for Tesla’s Energy storage product (the Megapack).

Some Final Thoughts: I Am Empathetic Towards Legacy Auto

As I shared in TGSGT VII,

Because I know the immense and profound pain of failure myself, I do not envy anybody in the auto sector right now.

This section is almost unnecessary at this point, as we genuinely believe that competition is truly, truly the least of Tesla’s concerns.

That said, it’s worth laying out why we believe this to be the case in a data-centric manner. Let’s begin:

Legacy auto companies fundamentally cannot win against Tesla as of today, and it makes no sense to buy any other EV other than a Tesla. Here’s why:

In America, “buying American” is a huge deal. Ford Motor Company (F) has done well in the U.S. car market for decades due to its “American brand.” Those days are over. Truly, it’s over for this universe of thought. This is why. So, if you’re looking to buy American, Tesla is the only option in the EV space, and the Cybertruck will be brilliant, and it will drive itself, and there will be nothing that competes with its value in Beating The Market’s opinion.

Can’t win in full autonomy [FSD]. “Ford said Wednesday (in 2022) that it had concluded that the large-scale profitable commercialization of self-driving cars was further out than expected.” Teslas already (mostly) drive themselves today, and you can have a Tesla drive you around for $200/month.

Can’t win in culture wars (Tesla utterly dominates social media. Elon Musk owns Twitter.)

Can’t win in balance sheet health. It’s not even close. Tesla has a massive cash hoard that dwarfs its long-term debt.

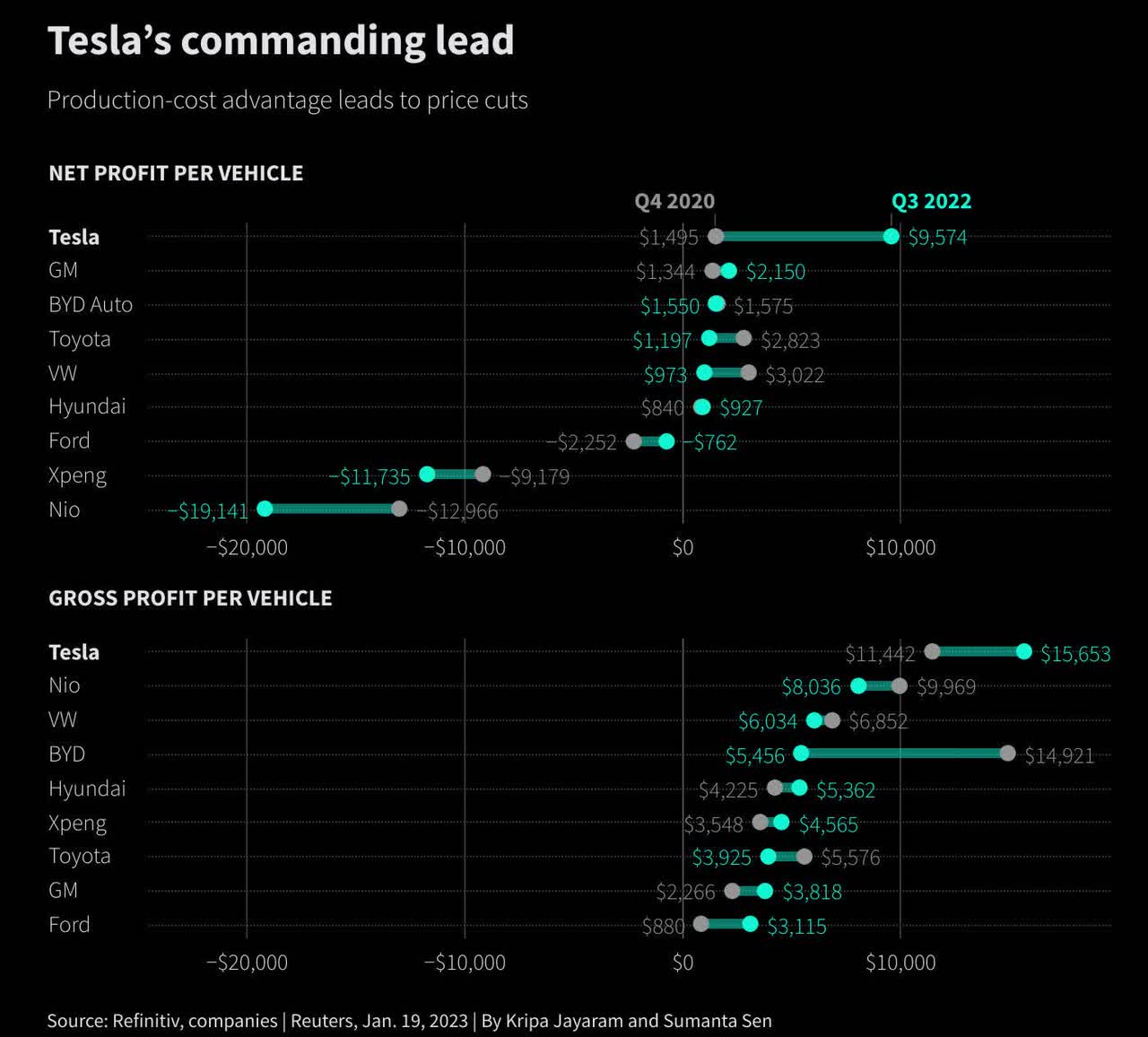

Can’t win in profitability:

Refinitiv

Can’t win in branding. The Nikola Tesla reference is simply brilliant. Learn more about Nikola Tesla here.

Were BTM not in such a profound losing season, I wouldn’t nearly have the empathy I have for legacy autos, but… I have a feeling that their losing season will be on par with what ours has been like! Unfortunately!

Can’t win in acceleration.

Twitter Influence Farzad Mesbahi

God Help Ford

As I reworked the Tesla investment thesis today, the phrase, “God help Ford,” organically came to my mind. I believe this phrase came to my mind for a few reasons (you likely already know them based on the previous section, but they bear repeating):

For any American buying an EV, it fundamentally makes 0 sense to buy a Ford.

Ford is not the most American. Tesla is the most America. Ford does not offer the best range/$. Tesla offers the best range/$. Ford’s brand is nowhere near as cool as Tesla’s brand. Ford did not step up to the plate and take the soul-crushing risk necessary to usher in the sustainable energy future. Tesla did. Tesla’s brand deserves to be incredibly cool. Ford does not offer FSD capabilities. Teslas, again, mostly drive themselves. Tesla’s acceleration (and therefore fun) is universally better than Ford’s.

Now, this is as of today. As of today, unless one faces a massive information asymmetry (as in they don’t know which product offers the best value), it simply makes 0 sense to buy a Ford EV product, much less any other EV products.

That said, of course, Ford, with enough time, could likely close a few of the above gaps. Notably, they’ve had about 15 years to close these gaps, and they still haven’t closed even the most basic ones.

And now game is no longer about acceleration. The game is no longer about range/$ or total range. The game is no longer about which car is the most American. To be sure, Tesla utterly dominates in all regards.

The game is now about FSD, and Teslas drive themselves far better than competitors, and there’s a fairly high chance Ford never fields an FSD product.

With all of this in mind, I do believe it’s worth acknowledging that, with enough time, Ford could likely close even the most ambitious gap.

But there’s likely not “enough time.”

Governments around the world, including the U.S. government, are now forcing these legacy auto companies to transition to and field in the marketplace highly, highly dubious EV products; EV products that make absolutely no sense to buy from every conceivable vantage point… mathematically speaking.

These EV products do not have custom-built Superchargers all over the world. They’re sort of stumbling out into the environment: an environment that is about to get soul-crushingly brutal as the Fed hikes rates into massive amounts of deflationary data and a generationally inverted yield curve.

While the U.S. government urges these legacy auto co.’s to transition, the U.S. government is simultaneously inducing a recession, as evidenced by our most recent deflationary data and the “generationally inverted yield curve.” The last time the yield curve was this inverted, the corresponding recession was fairly vicious (early 1980s).

In a perfectly symmetrical information environment, Ford would not sell a single EV; meanwhile, the U.S. government is inducing a recession, in which car sales will decline… the same sales that, logically, Ford should not have in the first place.

To this end, “God help Ford,” as the U.S. Fed works to induce a recession of fairly epic proportions.

I echoed these thoughts in a similar way recently:

So TSLA “missed delivery estimates.”

It “only” grew at 40%…

It grew at 40%! during the fastest repricing of credit in the history of America dating back to 1788.

Cost of credit (how people buy cars) went from effectively 0% to 5% in the span of months! Unprecedented!

Cost of credit as measured by prime rate and general behavior of U.S. treasuries

And they still grew deliveries at 40%?!

The market will trade TSLA down on its delivery “miss,” which I just contextualized, while wholesale disregarding the economic content/potential of Tesla Energy, its Supercharger Network, and FSD, which will lend to its Robotaxi ambitions

A recession will only serve Tesla.

I think the market is missing this. A recession would eliminate probably all of Tesla’s competitor

I mean think about what the U.S. government is doing right now: It bailed out auto in 08-09. Nothing much has changed. These companies will go bankrupt again due to their massive debt burdens

The government is forcing them to transition to EVs while inducing a recession that will almost invariably destroy the same companies they’ve propped up in the past

How utterly insane is this policy being executed by the U.S. gov’t?

It is virtually guaranteeing TSLA’s long term success in my mind. Force debt ladened ICE OEMs to build dubious EV products while simultaneously inducing a recession, the last one of which caused major auto manufacturer failures

If it weren’t my economic system/global economic system, it’d actually be kind of funny

Teslas barely make sense as cars.

They only make sense for the brand and promise of FSD.

In my opinion, nobody in their right minds would buy an EV from any other manufacturer other than TSLA simply because they’re not practical cars right now. They only appear to make sense within the context of “Elon’s science experiment gone global.”

The Greatest Irony

As I’ve thought about Tesla, Inc. over the last six months, my mind often applies The Greatest Irony framework to the company, and, indeed, Tesla could quite easily be the poster-child for The Greatest Irony, though, to be sure, the competition for this spot has been and remains absolutely fierce.

But, to be sure, Tesla’s price action is just preposterously ironic. In no uncertain terms, Tesla’s business is the strongest it’s ever been… From every conceivable perspective of which I’m aware: competitive positioning, FSD adoption, cash on balance sheet, debt load (now diminutive relative to where this note started), Tesla Energy, etc., Tesla is hands down the strongest version of itself in its corporate history.

Simultaneously, it now trades at one of its most depressed valuations in its corporate history!

I echoed these thoughts recently in remarking,

I find Tesla interesting insofar as it fits perfectly in The Greatest Irony series (a series I’ve been working on over the last 6-9 months to highlight the utterly exceptional opportunity that we’re now being offered).

Similar to Roku (ROKU) or Twilio (TWLO) or effectively all of our companies, Tesla was vastly weaker as a business in 2020 relative to where it finds itself today.

Tesla FSD Day

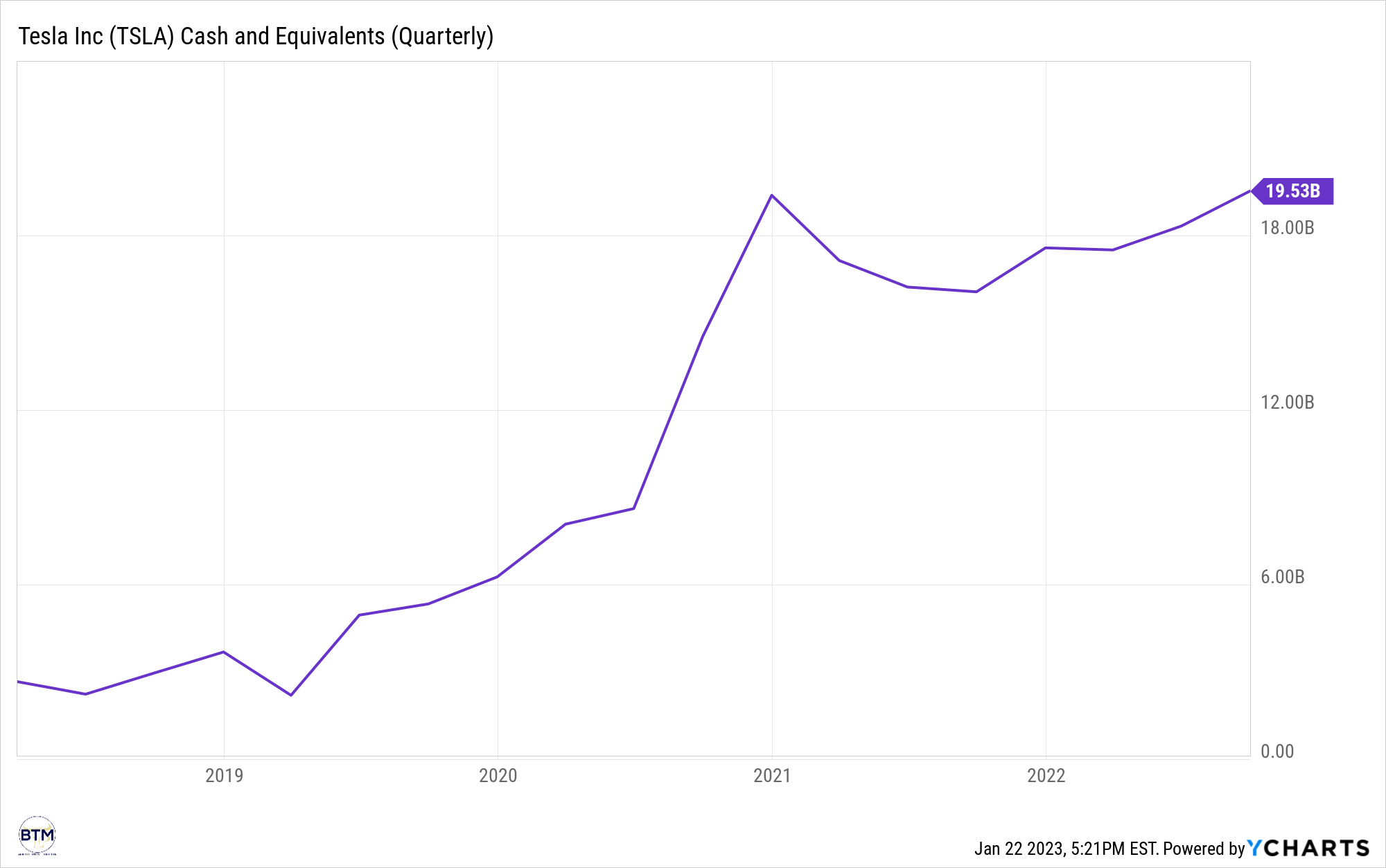

Tesla’s Growing Cash Hoard

YCharts

It had less cash. Tesla Energy was still years away. FSD needed a lot more work. Supercharger Network was smaller. From virtually every conceivable perspective, TSLA was materially weaker in 2020… When it traded at a vastly higher valuation.

Tesla Trades At Its Most Depressed Valuation Since 2019 From A Price To Gross Profit Perspective

As I’ve shared, it’s so curious to me that it’s almost as if the universe conspired to build these businesses to their greatest points of strength (more cash, more products, more data, more intelligence, bigger brand equity) to trade them to their lowest valuations in years or in these companies’ histories.

Tesla is hands down vastly less risky relative to where it was in 2020. It’s a vastly better business today from a variety of perspectives. Notwithstanding these realities, TSLA trades at a valuation that implies that it’s riskier than [at any point in the last three years].

If one studies the business for just a few weeks, one finds that TSLA is positively operating from its greatest position of strength… in the history of the company from what I’ve gathered!

I get the bubble. I get the recession and Fed hiking rates into deflation and a generationally inverted yield curve. Get all that. That will all fade away in the coming 12-24 months.

(will all likely fade away, but I vehemently believe it will be an afterthought and everyone will be worrying about xyz next)

Obligatory Statement Of Risks

If you are buying a business, you are assuming material risk.

Further, if you are buying a public stock such as that of Tesla, Inc., you should be okay with material volatility to accompany the aforementioned material risk.

If you do not want to assume material risk, then purchase U.S. Treasury bonds.

We are all grown-ups and can discern this reality.

That said, here are a few risks to consider:

Bad execution

Poor decision making from management

The fastest repricing of credit in the history of America and the associated follow-on impacts

We just witnessed the 2nd, 3rd, and 4th largest bank failures in U.S. history, and the Fed appears willing to further hike rates, but I cannot be sure.

There are many, many more risks to consider in addition to these, and I would encourage to study them.

As always, thank you for allowing me to serve you in building your business of owning businesses!

Onward to 10M FSD subscribers and beyond!

Analyst’s Disclosure:I/we have a beneficial long position in the shares of TSLA, TWLO, ROKU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.