Summary:

- The Home Depot has been a compounding darling with solid dividend growth and share price appreciation over the years.

- HD shares have recently underperformed the S&P 500, possibly due to weakening consumer spending.

- With consumers being more cautious with spending, home improvement projects may be taking a backseat, impacting HD’s performance.

M. Suhail

When it comes to the Power of Compounding, there are not many better examples of there than The Home Depot (NYSE:HD). HD has been a compounding darling for years, and what I mean by that is the fact that they have provided not only solid dividend growth over the years, but separate from the dividend, they have provided great share price appreciation.

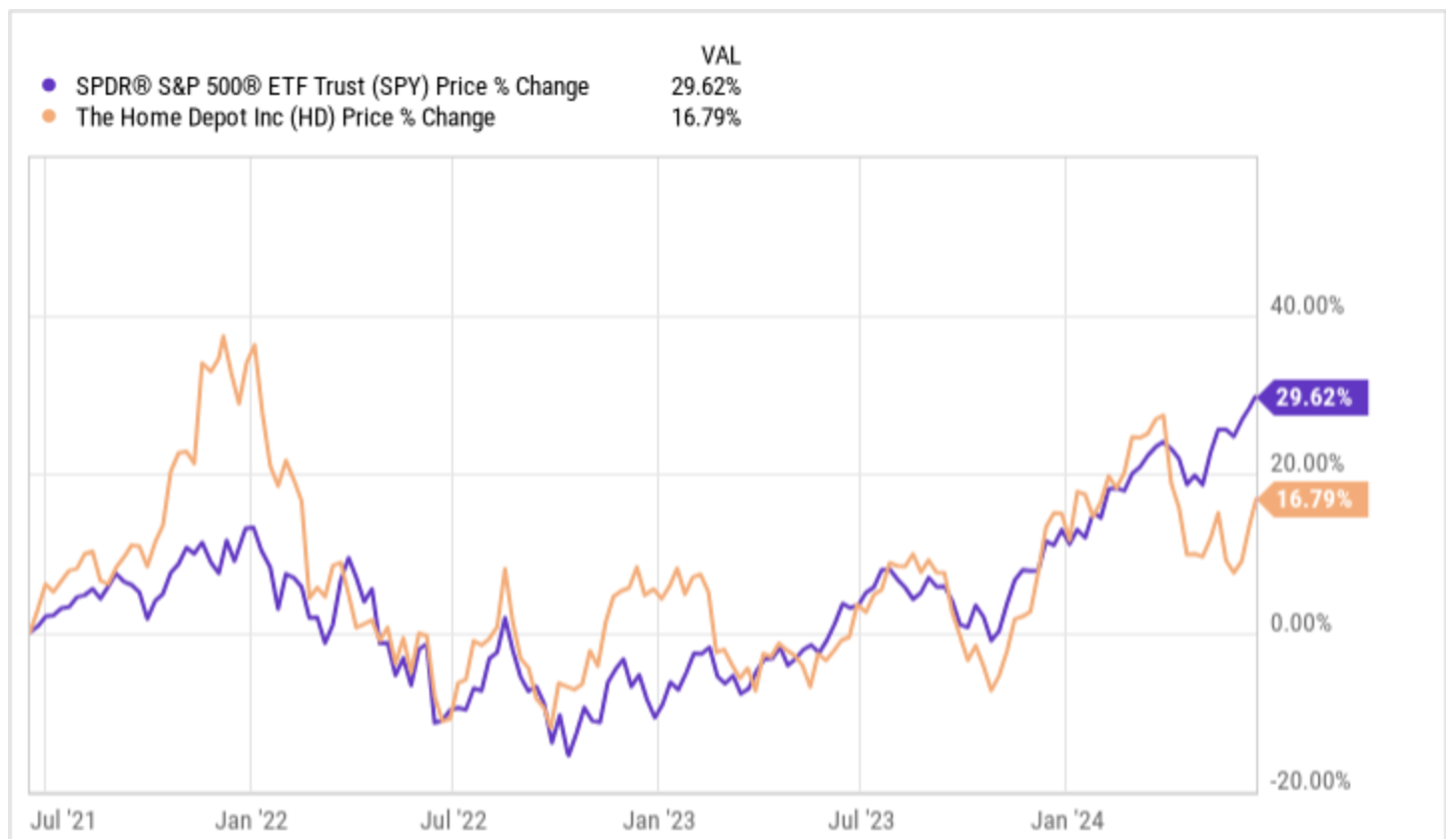

However, over the past few years, HD shares have well underperformed the S&P 500 (SPY) by a decent margin.

yCharts

Looking at the performance chart above, you can see that HD has actually outperformed the S&P 500 for much of that past three year period, but not until recently has the roles switched, which could indicate that shares of the home improvement giant may be trading at a discount, which is something we will look at more closely today.

HD In The Eye of a Weakening Consumer

It has been no secret that the US consumer has been weakening as inflation and higher interest rates have finally taken their toll. Enough is enough and the consumer dollar, especially the discretionary dollar is drying up.

We have seen a push back from consumers at companies such as Starbucks (SBUX) and McDonald’s (MCD), which have indicated consumers are being more picky, finally, with how they spend money after years of extremely high inflation.

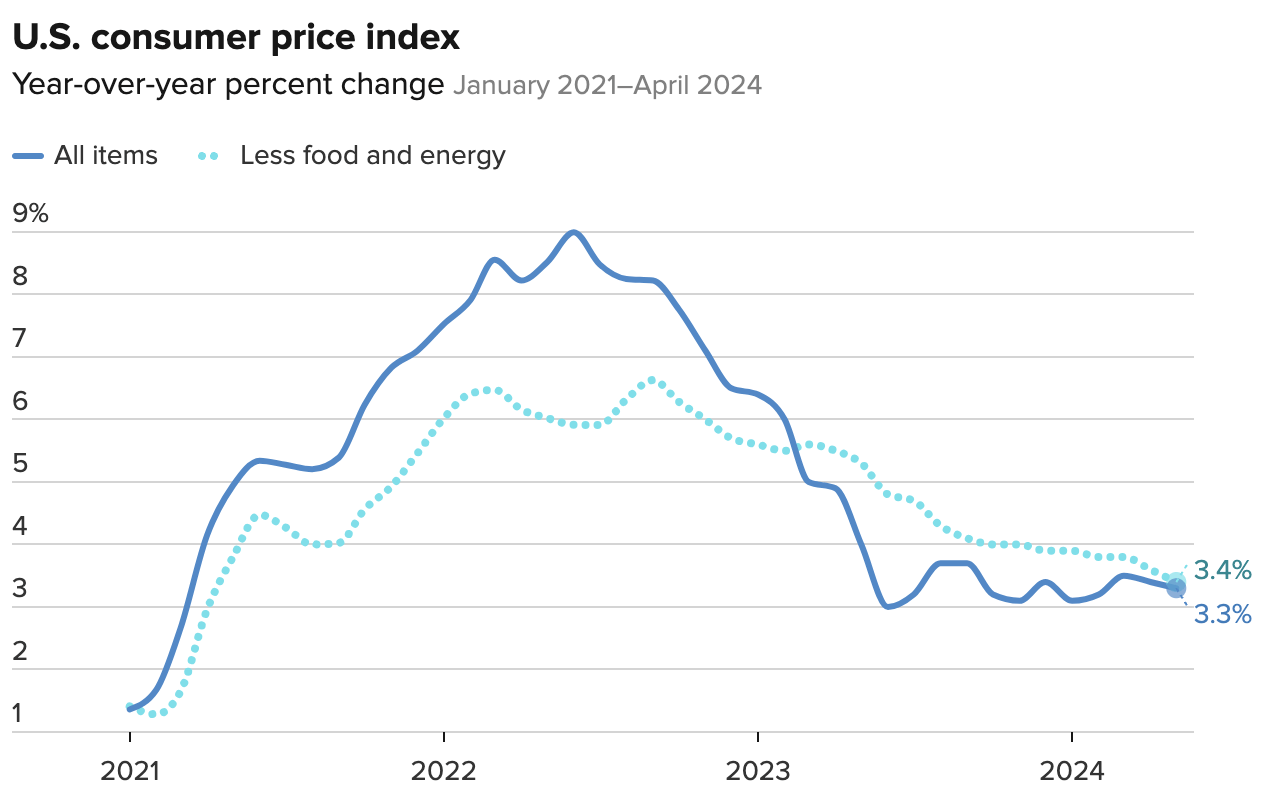

In the latest CPI report, although interest rates have remained high, inflation has remained sticky. The May 2024 CPI report showed an increase of 3.3% year over year and core-CPI, which excludes volatile food and energy prices, rose 3.4% over last year. The Federal Reserve has a goal of bringing these figures down closer to 2%, meaning they still have a lot of room for improvement.

cnbc.com

In terms of retail sales, the May report just came out showing retail sales increased 0.1%, which was below estimates looking for 0.2% growth year over year. When you exclude auto sales, retail sales actually declined.

Given all this, with US consumers clearly being more considerate with how they spend their money, home improvement projects have taken a backseat, especially after the boom we saw in 2020 and 2021 during the pandemic with many people working from home for a long period of time, something that has become normal today.

So given all this, is HD shares a BUY, SELL or HOLD?

Time to Buy Shares of HD?

When it comes to home improvement stores like HD and its closest competitor Lowe’s Companies (LOW), both of these companies rely heavily on the spring selling season as consumers tend to shore up the landscaping at their current homes or they may have just purchased a new home and want to add landscaping. Whatever it may be, the garden category is important during this time of the year.

However, when we breakdown the retail sales report for the month of May, the building materials and garden sector of the report showed a year over year decline of 4.3%, one of the weakest categories within the report.

Looking from another angle, U.S. homebuilder sentiment weakened in May for the first time in six months showing that higher interest rates are weighing on home sales.

The NAHB Housing Market Index fell unexpectedly to 45 in May, the lowest since January. The reading was below every single analyst estimate that was published.

Home Depot caters less to the DIY consumer and more to the Pro consumer, but a combination of a weaker US consumer and builders showing a lack of confidence does not bode well for this home improvement giant at the moment.

In the company’s latest earnings report, HD reported a decline of 2.8% in comparable store sales and a decline of 3.2% in US comp store sales. Revenues came in below analyst expectations at $36.4 billion, declining 2.4% year over year.

Management reaffirmed their guidance, which called for total sales growth of only 1% and comp sales decline of 1% for the full year, telling us management is not very optimistic on the US consumer either in 2024.

As such, there is not a lot to like from a macro standpoint when it comes to investing in shares of HD. However, as a long-term investor, if shares are priced extremely low, it could point to a great entry point for those willing to wait it out. Let’s take a closer look at some of those valuations now.

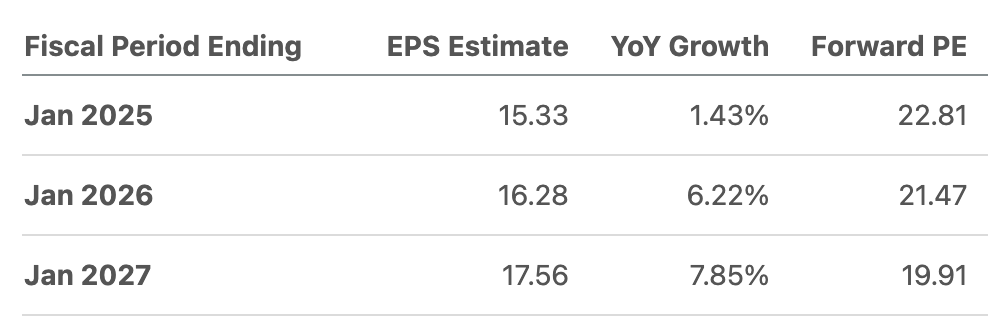

Analysts are not expecting much in terms of EPS growth this year, but the following two years EPS is expected to jump between 6-7% per year.

Seeking Alpha

Using this year’s guidance, shares currently trade at 22.8x and they trade at 21.5x next years earnings. For comparable purposes, shares have traded at an average P/E multiple of 22.7x over the past five years. Given that, there is not much of a discount at all when it comes to shares of HD.

From an Enterprise Value to EBITDA standpoint, shares trade at 16.1x, which is well above their 5-year average of 14.9x.

I love HD, but the valuation and the weak consumer does not have me all that excited at the moment.

A Dividend Compounder

As I mentioned at the start, HD has been a compounding darling and a portion of that has to do with not only the company paying a solid dividend, but it has been the company’s ability to increase the dividend at a solid clip.

Seeking Alpha

Shares of HD currently yield a dividend of 2.6% and they have a 5-year dividend growth rate of nearly 13%. The company has increased the dividend for 14 consecutive years and counting.

The Power of Compounding allows you to take this dividend income every year, and reinvest that to add more shares to your investment. With a company that consistently increases its dividend, not only do you now have more shares, but since they pay a higher payout each year, your dividend income will rise at a faster clip every year as well. It is a powerful process over the long run.

Investor Takeaway

The Home Depot is a fantastic company and extremely well run, but the current environment does not bode well for this home improvement juggernaut.

Although they continue to pay a growing dividend, valuation does not look all that cheap at all considering we are seeing a weakening consumer and a slowing economy. Discretionary spending is key for HD and that has soured in recent months.

As such, I am going to take a PASS on shares of HD right now, as their is no intrigue at the current valuation, and I will wait to see if I can enter at a much lower price.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

no marketing to add