Summary:

- NFLX profits hit $1.6 billion (up 20% from a year earlier) and the platform added 9 million new subscribers.

- Netflix has invested heavily in diversification, in the form of international content. The company is shifting spending away from Hollywood and increasing investment in local-language productions.

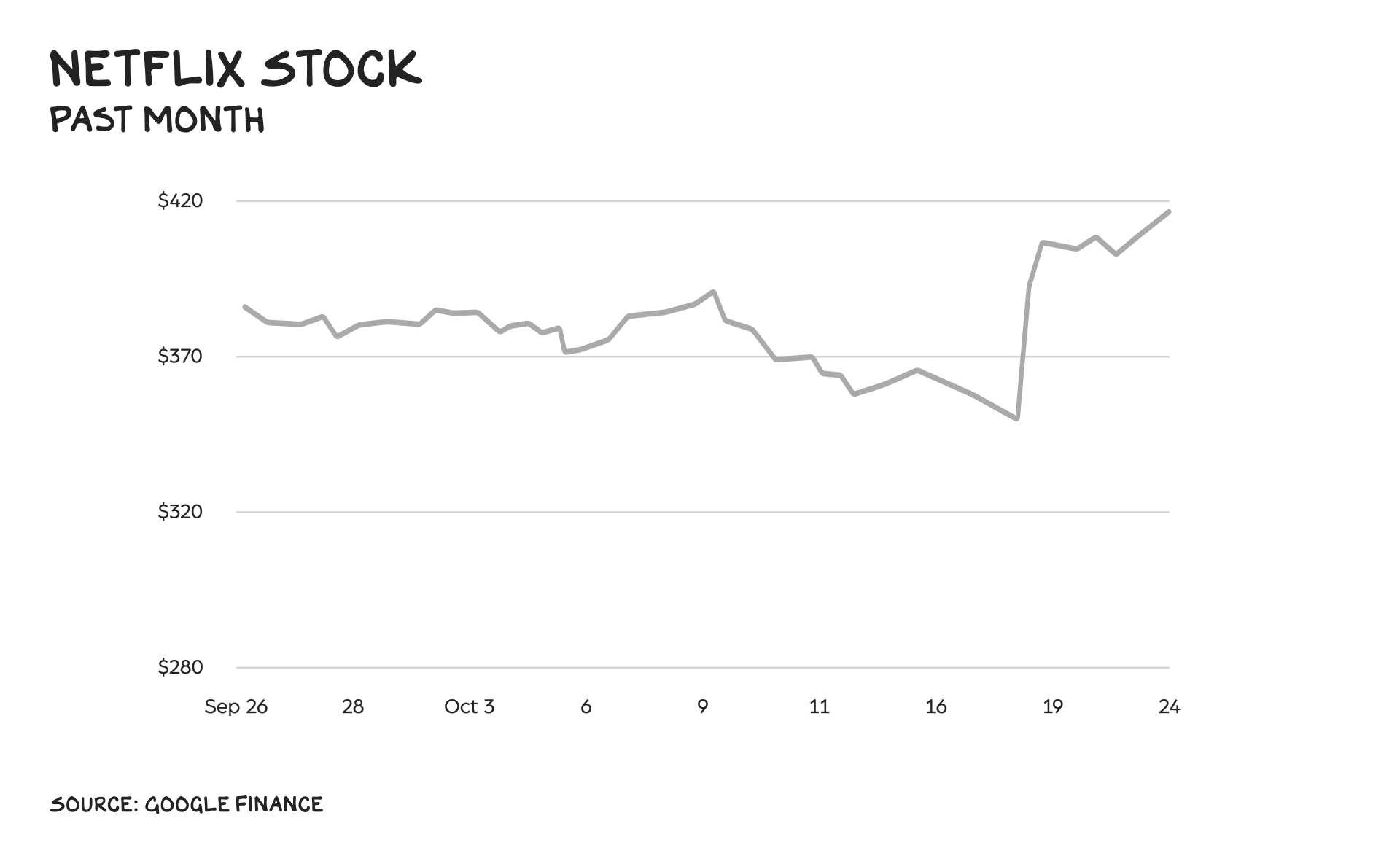

- Netflix’s decision to increase subscription prices this quarter reflects the strength of the platform. It has reached utility status.

Mario Tama

Despite receiving scant coverage, the biggest business stories last week were Netflix (NASDAQ:NFLX) and Meta’s (META) quarterly earnings. The numbers were striking: NFLX profits hit $1.6 billion (up 20% from a year earlier) and the platform added 9 million new subscribers.

Meanwhile, the company is raising prices. Over at Meta, revenue increased 24% and costs declined 7%, resulting in a doubling in profits. For this post though, I’ll focus on Netflix.

Rewind

A year ago, Netflix was losing 1 million subscribers per quarter and had shed 75% of its market cap. It was the worst performing stock in the S&P 500. Fast-forward one circumnavigation of the Sun, and Wall Street is “gushing” over its “beautiful” results while the rest of the industry flounders.

However, rebounds are not new for Netflix. Since it delivered DVDs in envelopes, the company has defied the odds. Think about it: a DVD-by-mail company turned internet platform turned Hollywood giant that would eventually join the same power acronym as Apple (AAPL), Amazon (AMZN), and Google (GOOG) (GOOGL).

We’ve discussed entertainment’s woes at length this year, but Netflix has replaced Disney (DIS), Discovery (WBD), and Paramount (PARA) on the content Iron Throne and boasts a market cap equal to all three combined.

Told You So

Five months ago, I predicted the writers’ strike would do more to help Netflix than harm it. My thesis: The strike would “force” a universal reduction in spending, while actually increasing the relative value of Netflix to consumers.

The streamer was able to cut costs without materially affecting the user experience, as it already had a content library as deep as the Mariana Trench. Also, it helps to not be cable, because unlike news, late night, and sitcoms, Ozark and Bridgerton aren’t perishable.

In addition to a 20% profit bump, the company is expected to generate $6.5 billion in free cash flow this year. That’s up from $1.6 billion in 2022. Meanwhile, revenue is also up, but only slightly (8%).

Which means the multibillion-dollar windfall is a direct consequence of lower costs – that is, not having to spend $20 million per episode on The Witcher. Analysts are even cautioning against too much optimism, as the “resolution of the writers’ strike will bring higher costs” and thus depress profits.

Put another way, investors don’t want the strikes to end. Would we be surprised if we found out the folks running the WGA/SAG-Aftra were covert assets working for the streaming giant? NETspionage if you will (couldn’t resist).

Anyway, Netflix’s strength in the face of the work stoppage was both a function of the strikers’ lack of long-term strategy and Netflix’s abundance of it. Over the past two decades, the company has employed several simple but important business strategies that have endured. Let’s review them.

Diversify

I asked ProfG.AI to explain the value of diversification. Its answer: “Diversification is the kevlar that protects you from fatal financial injuries. It’s a defensive strategy that limits your downside, even if it limits your upside.” I’d hate to hang with this guy, but he isn’t wrong.

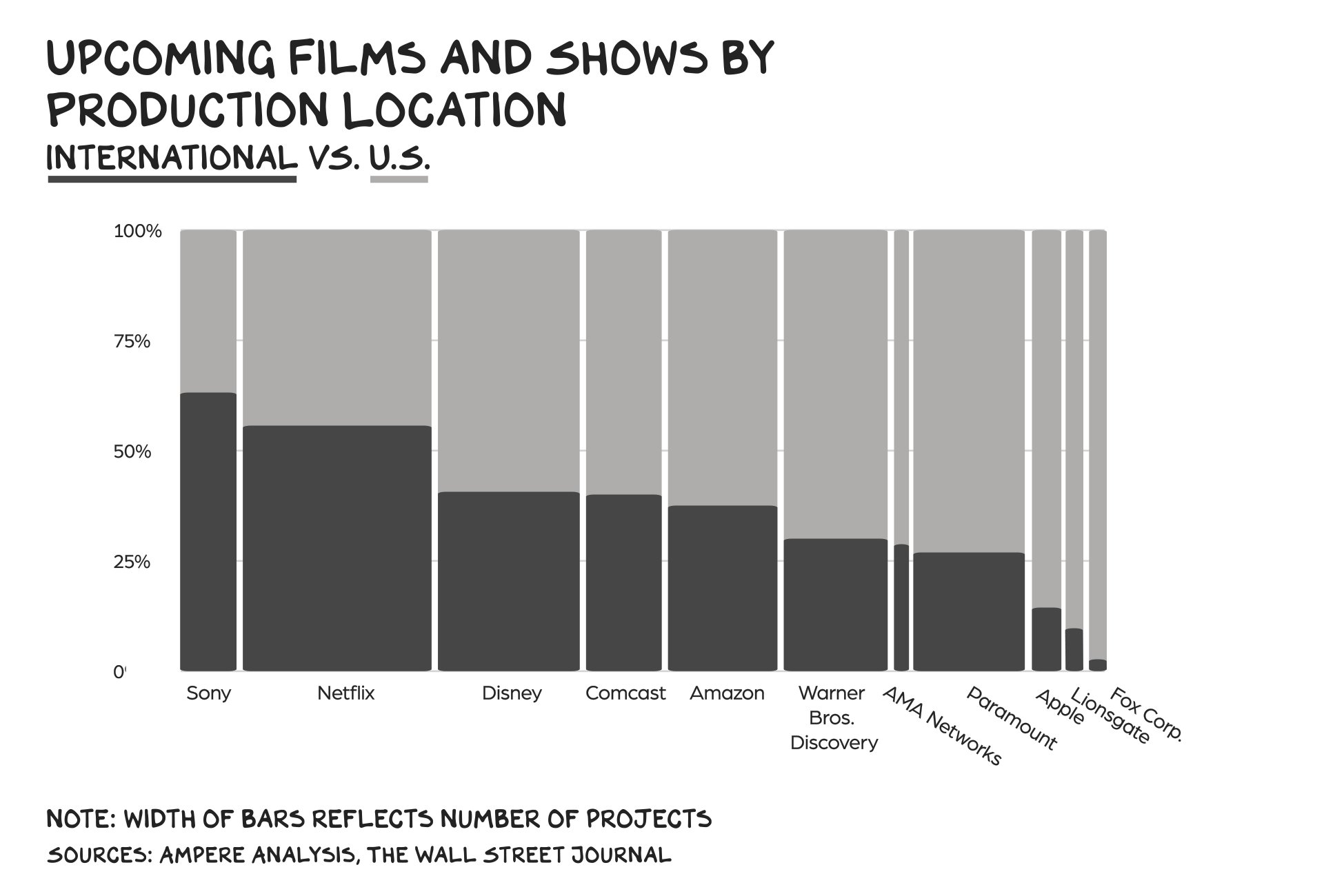

Netflix has invested heavily in diversification, in the form of international content. The company is shifting spending away from Hollywood and increasing investment in local-language productions.

In the past two years, spending in Asia has increased to $2 billion and European investment has doubled. More than half of Netflix’s scripted titles are being produced abroad.

Compare that to Warner Bros. Discovery (a third) and Paramount (a quarter). The effect has been protection against supply chain interruptions (i.e. content shortages), because while American actors and writers went on strike and TV series orders declined 25%, the foreign production gears kept grinding.

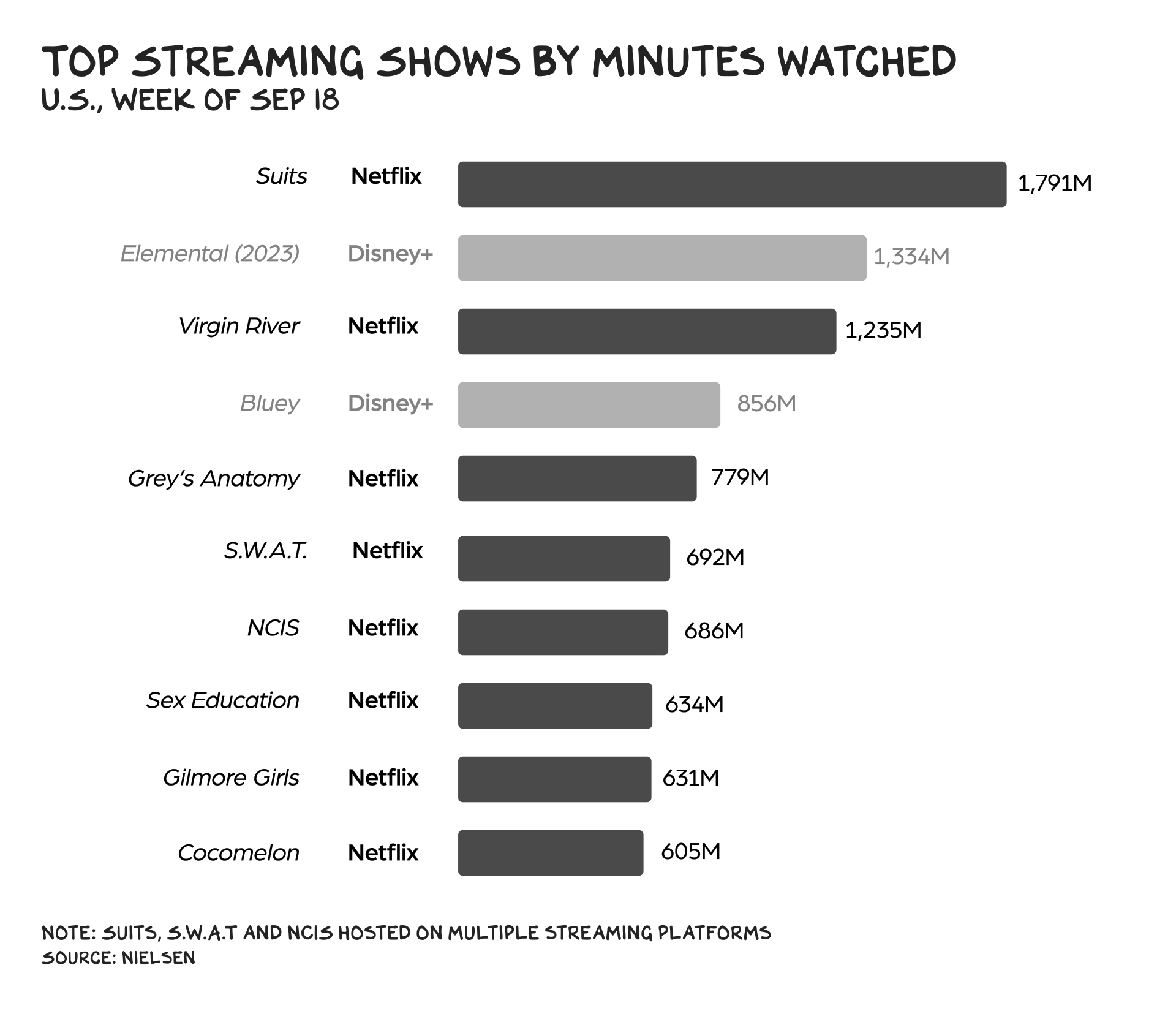

In addition, Netflix has diversified its library with a mix of original and licensed content. One of its more creative moves this year was approaching NBCUniversal to buy the rights to Suits.

After debuting on Netflix this summer, the 2011 legal drama performed better than any original Netflix show this year. Scratch that – better than any show, period.

Suits was the most streamed show across all platforms for three straight months this year, hitting the record for most-ever weeks at No. 1. This is the Netflix Effect in action: Take a solid series, reheat it, and make it the most consumed content on the planet.

Adapt or Die

The species that survive aren’t the strongest or fastest but the most adaptable. As we’ve discussed before, the most valuable companies in the world all have one thing in common: They build a thick layer of innovation on top of investments made by the premier VC in history, the U.S. government.

Apple used Darpa’s GPS to build the iPhone. Facebook (META) built an app on top of a government-funded hosting service called the Internet. And Netflix, like Amazon, leveraged the nation’s largest content distribution platform – the U.S. postal system – to send DVDs by mail.

Mailing DVDs sounds dense now, but it was a great business. The company launched in 1997, went public in 2002, and reached a billion dollars in revenue in 2006 by addressing a pain point: that IED in your kitchen drawer, the VHS of Turner & Hooch you forgot to return.

The company’s leadership could have settled and backed away from the massive investment required to pivot to streaming. But CEO Reed Hastings recognized another multibillion-dollar investment in broadband would soon render DVDs obsolete. “Don’t be afraid to change the model,” Hastings said, and in 2007, Netflix introduced streaming to the world.

Streaming was not the company’s only bold pivot. In 2011, despite its reputation as a “platform,” Netflix decided to foray into original content. At the time, it seemed absurd.

The company was going up against Universal (CMCSA), Paramount, Warner Bros., Disney, and Sony (SONY) – Hollywood titans known in the industry as the Big Five.

Still, Netflix dove in headfirst, spending $2 billion on content in Year One. One of its first original series, House of Cards, went on to earn 33 Emmy and 8 Golden Globe nominations.

Opportunities vs. Problems

Peter Drucker said invest in your opportunities, not your problems. Few have done this better than Netflix. For a long time, the company’s obstacle was plain to see: It was burning hundreds of millions in cash every year.

But Netflix knew brute force was its strength. Specifically, it recognized the market viewed it as a tech company, so it did what other media companies couldn’t: Massively invest, lose money, and grow.

In 2015, Netflix registered negative $840 million in free cash flow. By 2017, that number was negative $2 billion; two years later, negative $3 billion. Fearless spending was its differentiator.

Capital as a weapon, if you will – specifically, cheap capital. Original content spending at Netflix grew faster than at any other streaming service, and by 2021, the company was investing $18 billion on content per annum, with free cash flow still in the red.

Meanwhile, the legacy media players were beholden to a different investor base that wouldn’t tolerate the losses needed to go toe-to-toe with the streaming platform.

Netflix is now firmly profitable in all aspects of the business. It is the only entertainment company with a profitable DTC streaming business, and the legacy players are playing catch up.

Name Your Price

Netflix’s decision to increase subscription prices this quarter reflects the strength of the platform. It has reached utility status.

There are 140 million households across the U.S. and Canada, and 77 million Netflix accounts. Consumers no longer consider the cost benefit of a subscription. The question isn’t if you subscribe to Netflix, but rather, what other platforms you decide to accessorize it with.

The premium plan is now $22.99 per month, up 15%. Meanwhile, the standard ad tier remains $6.99. Netflix has correctly adjusted for the most fundamental economic trend in America, income inequality.

It has adopted a means-based pricing strategy that retains low-income users while squeezing more from upper-income households. Plus, research has found that introducing lower-quality products actually increases sales of your higher-margin premium products. I was skeptical of Netflix advertising at first, but it may ultimately drive more users to the premium product.

Threats

I’m tempted to say the only thing that can stand in the way of Netflix is Netflix. But that’s not true – it’s TikTok and YouTube.

We’ve discussed TikTok’s ascent before. The Chinese juggernaut is stealing eyeballs (especially young ones) from the streamers and generating $25 billion in quarterly revenue in the process. BTW, that number is up 34% from last year.

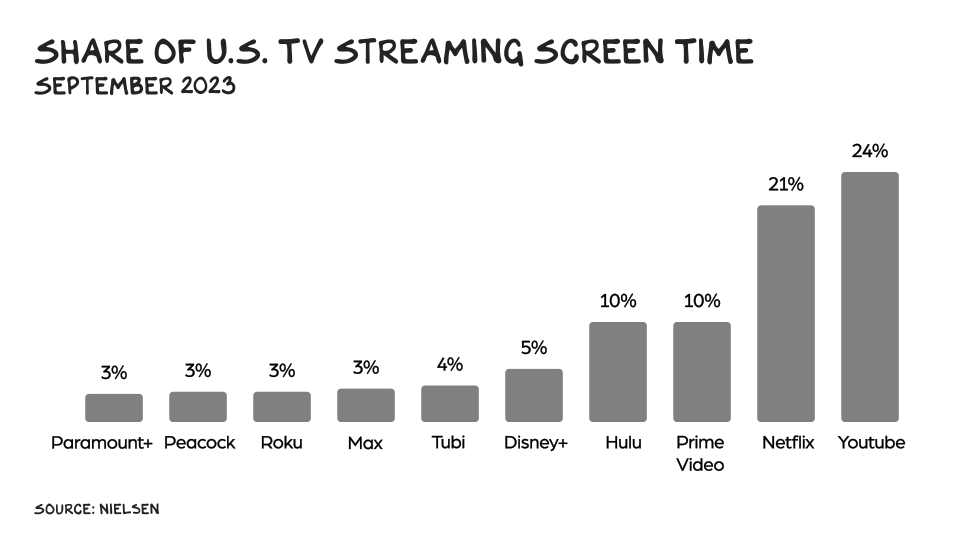

Less discussed, however, is the threat of YouTube. Netflix gave it a casual mention in its shareholder letter, but the implication was so relaxed as to be tense.

“Our share of TV screen time in the U.S.,” the letter read, “is greater than any streamer other than YouTube.” This was meant as a not-so-humble brag. It isn’t.

YouTube is the most popular TV streaming service, and that doesn’t account for the minutes it gets on laptops and mobile phones. I assume (hope) management recognizes this is a problem.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.