Summary:

- Alphabet/Google’s revenue and stock performance suffered last year, but the company has implemented cost cuts and seen a revival in advertising revenue.

- Google Search remains dominant despite concerns about competition from ChatGPT.

- Google’s growth is supported by strong performance in Google Cloud, YouTube, and its moonshot projects like Waymo.

igoriss

This article was coproduced with Chuck Walston.

Last year, investors in Alphabet Inc. (NASDAQ:GOOG) (GOOGL) aka Google took a beating. There were a variety of reasons the stock tanked. Alphabet’s revenue had slowed compared to past years. In the last quarter of 2022, Alphabet’s sales were only up 1% year-over-year, and operating profit margin fell to 24%.

With predictions of a recession on the horizon, pundits noted that advertising, the company’s primary revenue source, would slow considerably. Add to that competition the likes of Amazon (AMZN) brings to the digital advertising space.

Next came concerns regarding ChatGPT. Many thought its integration with Microsoft’s Bing would deliver a mortal blow to Google Search.

But there is more to the story.

Alphabet instituted cost cuts, including laying off 12,000 employees. Fears of a recession are receding, and with that comes a revival in advertising revenue, and the company’s growth has accelerated over the last two quarters.

Bears can point to ChatGPT as the coming downfall of GOOG, but AI has been an integral part of GOOG’s search engine and other product lines for some time. Alphabet became an AI oriented firm seven years ago.

Add to that a variety of initiatives that could boost growth, and the bear/bull argument becomes more complicated.

The 2023 Turnaround

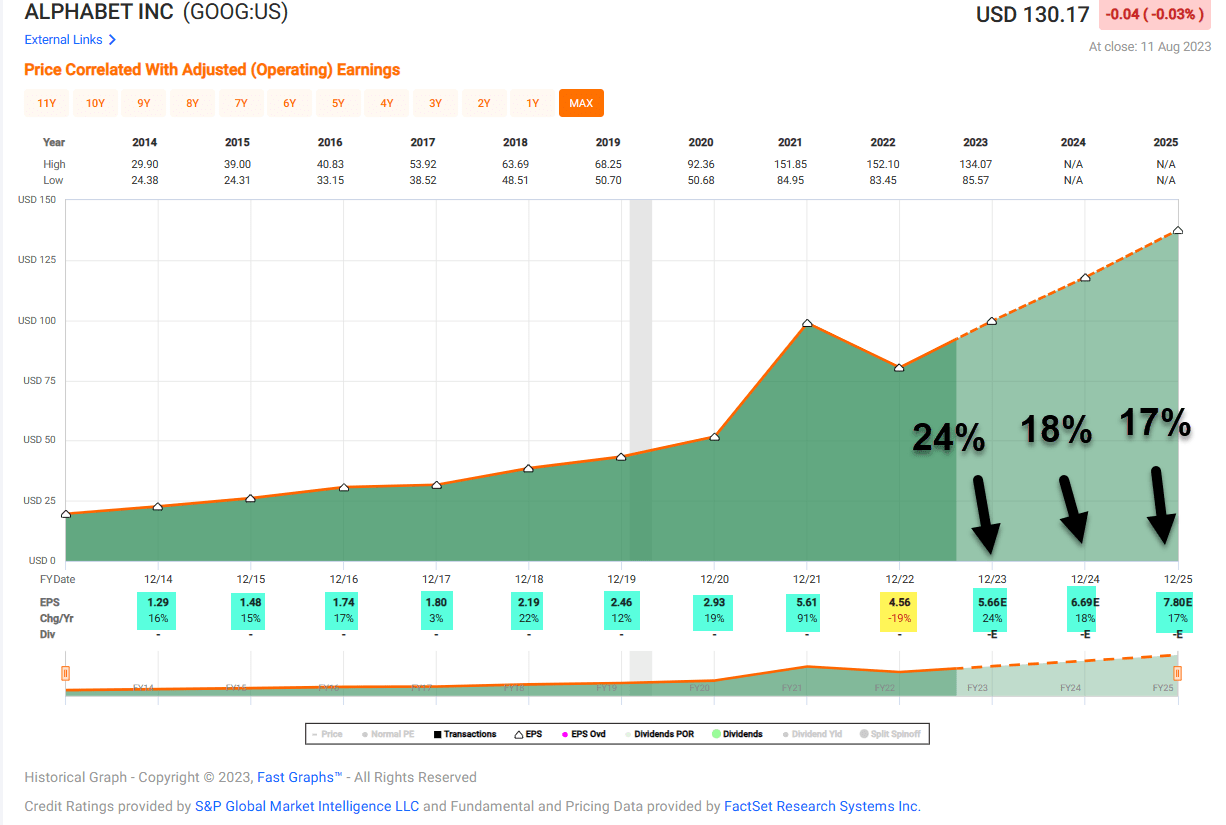

After hitting a low of roughly $83 a share in November, GOOG stock has been on the rise. Now trading at a hair below $130, Alphabet is within striking range of the levels reached in 2021 and early 2022.

Late last month the company reported Q2 23 results. Revenues were up 7% to $74.6 billion, beating analysts’ estimates by $1.84 billion. EPS of $1.44 also beat consensus by $0.10, and free cash flow (“FCF”) jumped more than 12% to $21.8 billion.

Google Services revenues of $66.3 billion were up 5%.

Google search, which constitutes 78% of Alphabet’s overall revenue, also increased 5% year over year. Holding a near monopoly, Google Search has a 93% share of the world’s market. Alphabet’s online search business appears to be unfazed by the likes of ChatGPT.

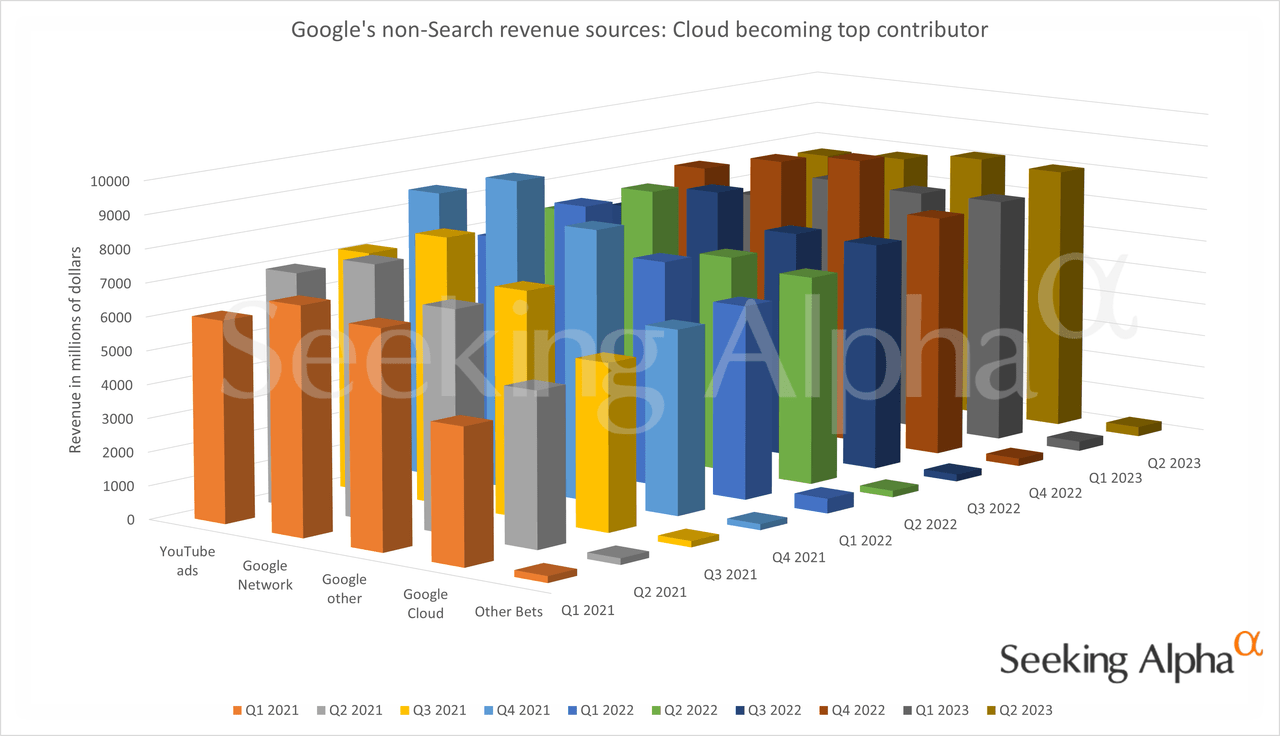

A strong positive was found in the company’s Google Cloud Platform (“GCP”) results. GCP has been losing money for years. In 2022 alone, that segment recorded an operating profit loss of $590 million.

However, Cloud revenues have roughly doubled to nearly $40 billion over the last two years. In Q2, Cloud generated $8 billion in revenue, a 28% increase, along with an operating profit of $395 million.

Seeking Alpha

YouTube reported a revenue decline in Q1, but YouTube’s revenue increased 4% to $7.7 billion in Q2. YouTube’s trailing 12-month sales now stand at $40 billion with YouTube TV and YouTube Premium gaining traction.

YouTube Shorts are now viewed by over 2 billion a month, up from 1.5 billion a year ago.

Perhaps most importantly from an investor’s point of view, Alphabet generates massive free cash flows. Last quarter, FCF totaled $22 billion, up 73% from Q2 of 2022.

Ten ABCs Of Alphabet

As the dominant force in digital advertising, GOOG stands to benefit greatly from the growth in that market.

PRECEDENCE RESEARCH projects a CAGR of 9.22% for the global digital ad spending market size from 2022 to 2030.

Other areas of growth lie in YouTube Shorts, which are now watched by over 2 billion users every month.

Last September, YouTube passed Netflix (NFLX) to become the streaming leader in the U.S. YouTube is now viewed by over 150 million people on connected TV screens in the U.S. and growth among international users is gaining momentum.

Alphabet strengthened YouTube’s offerings with the recent purchase of the rights to the NFL’s Sunday Ticket games. Sign-ups for NFL Sunday Ticket began in April, and YouTube will broadcast their first football season this fall. This will likely lead to greater growth in YouTube TV.

Turning to Cloud, Fortune Business Insights forecasts a CAGR for the global cloud computing market of 19.9% through 2029.

Here is where Alphabet may hold a distinct advantage over rivals in terms of future growth. The following excerpt (emphasis added) from the Q2 earnings call indicates that the boom in AI, rather than hurting Alphabet, could work in the firm’s favor.

More than 70% of gen AI unicorns are Google Cloud customers, including Cohere, Jasper, Typeface and many more. We provide the widest choice of AI supercomputer options with Google TPUs and advanced NVIDIA GPUs, and recently launched new A3 AI supercomputers powered by NVIDIA’s H100. This enables customers like AppLovin to achieve nearly 2 times better price performance than industry alternatives.

Our new generative AI offerings are expanding our total addressable market and winning new customers. We are seeing strong demand for the more than 80 models, including third-party and popular open source in our Vertex, Search and Conversational AI platforms with a number of customers growing more than 15x from April to June.

Among them, Priceline is improving trip planning capabilities. Carrefour is creating full marketing campaigns in a matter of minutes. And Capgemini is building hundreds of use cases to streamline time-consuming business processes.

Our new anti-money laundering AI helps banks like HSBC identify financial crime risk. And our new AI-powered Target and Lead identification suite is being applied at Cerevel to help enable drug discovery.

Our generative AI capabilities also give us an opportunity to win new customers and upsell into our installed base of 9 million paying Google Workspace customers.

As stated, with 70% of AI startups currently Google Cloud customers, it is reasonable to believe that some of those companies will provide a significant boost in cloud revenue.

I also believe that Alphabet’s Other Bets segment holds a great deal of promise. Waymo, Wing, AI research company DeepMind, smart home products from Google Nest, and Verily life sciences, represent moonshot projects that could eventually drive growth.

Just today it was announced that California regulators approved Waymo to expand the company’s operations. Waymo can now transport paying customers throughout the city, 24 hours a day, without a human safety driver. Waymo was also approved to operate vehicles in inclement weather and at speeds of up to 65 miles per hour.

It should be noted that Waymo has partnerships with Daimler AG (OTCPK:DTRUY) (OTCPK:DTGHF), Jaguar Land Rover, Volvo (OTCPK:VOLAF), Nissan-Renault, and Stellantis (STLA).

Morgan Stanley estimates Waymo’s potential valuation at $105 billion, while analyst Eric Sheridan of UBS forecasts $114 billion for Waymo’s taxi service revenue in 2030.

A report by McKinsey and Company projects revenue for autonomous cars could reach $300 billion to $400 billion by 2035, and Alphabet is at the forefront of this technology.

FAST Graphs

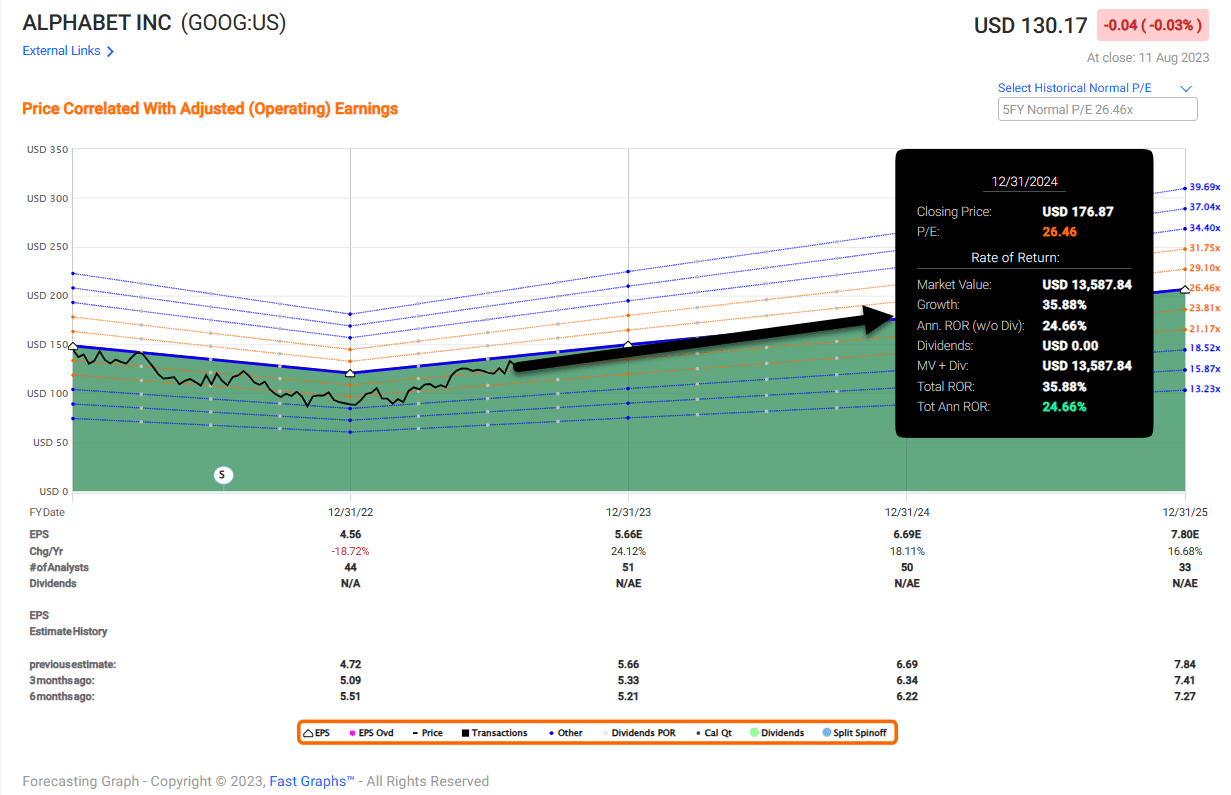

Debt And Valuation

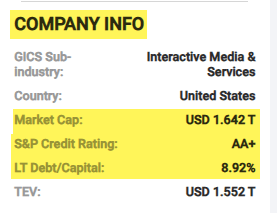

As of the end of Q2, Alphabet held $118 billion in cash and cash equivalents, and had $14 billion in long-term debt.

GOOG trades for $130.05 a share. The average 12-month price target of the 12 analysts that follow the stock is $132. The price target of the 3 analysts that rated the stock following the last earnings release is $150.

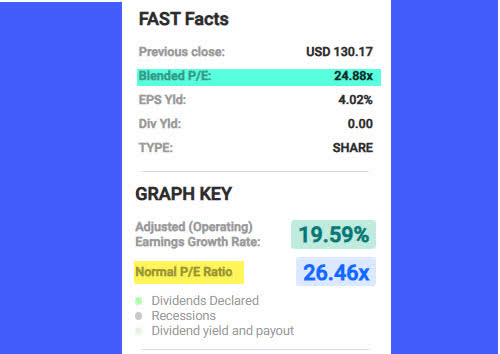

Alphabet’s forward P/E is 23.25x, well below the stock’s 5-year average P/E of 26.51x. The 5-year PEG of 1.46x is on par with the average PEG ratio for the stock over the last 5 years of 1.50x.

FAST Graphs

Is Alphabet A Buy, Sell, Or Hold?

After a few quarters of tepid returns, Alphabet has bounced back rather smartly. I see Cloud becoming profitable as a strong positive, and I view concerns regarding the potential for AI to hurt Google as misplaced. In fact, I believe Alphabet’s own AI platforms will serve the company well.

I will also opine that Google’s moonshots hold a great deal of potential, particularly Waymo.

FAST Graphs

Furthermore, even if my confidence in the company is misplaced, with $118 billion in cash and cash equivalents and $14 billion in long-term debt, coupled with that amounts to 21% of revenue, Alphabet can weather a few miscues.

I will concede that if we endure a recession, ad revenues will falter.

However, analysts forecast for nearly 17% EPS growth next year on sales growth of about 11%, and GOOG is trading for a reasonable valuation.

I rate the stock as a Buy, and I believe it is a solid investment for those holding the shares over the long haul.

FAST Graphs

I have a small position in GOOG.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Sign Up For A FREE 2-Week Trial

Join iREIT on Alpha today to get the most in-depth research that includes REITs, mREIT, Preferreds, BDCs, MLPs, ETFs, Builders, Asset Managers, and we added Prop Tech SPACs to the lineup.

We recently added an all-new Ratings Tracker called iREIT Buy Zone to help members screen for value. Nothing to lose with our FREE 2-week trial.

And this offer includes a 2-Week FREE TRIAL plus my FREE book.