Summary:

- Thermo Fisher’s stock is now a “buy” due to signs of recovery, including positive sales growth and stabilized margins, despite recent bearish trends.

- The company’s post-pandemic challenges are easing, with optimistic executive comments and improved guidance for 2024, indicating a potential return to organic growth.

- Potential deregulation under Trump’s administration could benefit Thermo Fisher by increasing demand for its equipment and consumables in a more competitive pharmaceutical market.

- Valuation based on free cash flow conversion suggests a fair value of $526, making Thermo Fisher a conservative, low-risk investment with expected returns of 9-10%.

alvarez

Introduction

I have already written two articles about Thermo Fisher (NYSE:TMO), one of my favorite companies in the healthcare sector. I recommend you take a look at them if you want to fully understand my perspective on the company. In the first article, I explained my thesis and why I believe it is a superior business model within the industry. In the second article, I discussed how we were likely at the bottom of the cycle and how the company was positioning itself to return to growth in the upcoming quarters and years, in my opinion.

Currently, the stock has entered a bearish phase, especially since Donald Trump won the election a month and a half ago. I believe the market is misunderstanding the impact the new president will have on the industry, and I want to use this article to explain why. I will also review the last few quarters and the comments made by the executives in recent earnings calls. Finally, I will update my valuation model and explain why I am upgrading the rating of Thermo Fisher’s stock to a buy, after keeping it at hold for over a year and a half.

Seeking Alpha

The cycle is turning around

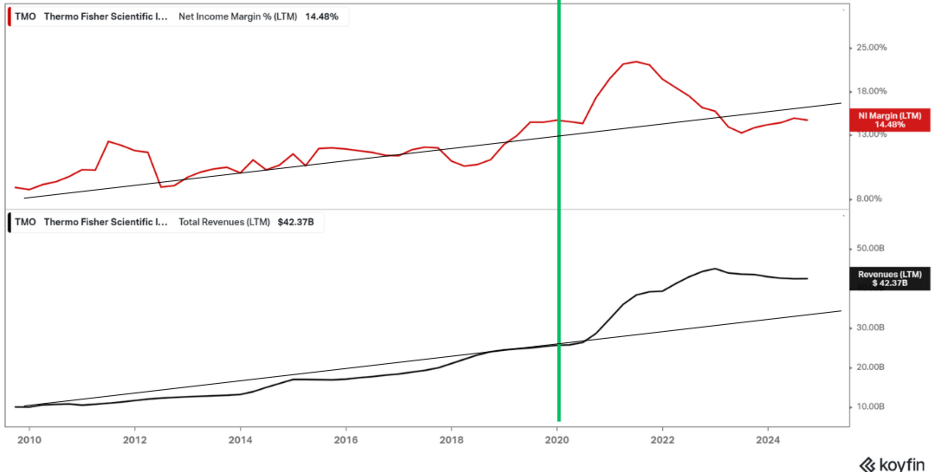

As we already discussed in previous articles, Thermo Fisher and other companies in the healthcare sector, such as Danaher (NYSE:DHR) and Eurofins, found themselves navigating the post-COVID aftermath. During the pandemic, spending on diagnostics and vaccine research skyrocketed, and one of the main beneficiaries was Thermo Fisher, as its catalog of products and services aligned perfectly with market demands at that time. Revenues and profit margins surged well above the trend established over the previous decade, and, consequently, the stock price soared as well. However, the issue was that the market extrapolated this growth into the future, leading to inflated expectations. Once the pandemic subsided, much of that extraordinary spending disappeared, and both sales and margins contracted back to pre-pandemic trends.

Koyfin

However, I believe we already have enough signals to affirm with a certain degree of confidence that the bottom of the cycle is behind us and it is slowly starting to turn around.

-

Last quarter was the first in nearly two years of positive sales growth for Thermo Fisher. A modest 0.25%, but nonetheless, it marks a return to growth.

-

Thermo Fisher’s guidance for the full year forecasts sales growth of between 0-1%. Again, it’s almost negligible growth, but it seems to confirm that the cycle has bottomed out.

-

The company’s margins already appear to have stabilized, with three consecutive quarters of recovery.

-

The results from Danaher, its main competitor, are following a similar trend, although they remain slightly more delayed compared to Thermo Fisher.

-

The executives’ comments are beginning to sound more optimistic regarding the coming quarters and years.

This last point seems particularly relevant to me because I noticed the most optimistic remarks of the past year and a half during the third-quarter earnings call. Some of the comments I found most interesting are as follows:

Mark Casper, the CEO, mentioned that 2025 will be the last year in which the headwinds from the pandemic will have a negative impact, and that in 2025, this impact will be much smaller than this year. With these remarks, we can infer that organic growth may return next year, thanks to the near disappearance of these headwinds.

“In 2025, what I would say is that it’s the final year of the runoff of the pandemic-related activity and while that’ll still be a headwind to growth, it’s going to be less than it was in 2024.”

This ties in with comments about the improvement in end markets throughout this year and the expectation of returning to organic growth as early as next quarter.

“The end markets are modestly improving throughout the year. We’re excited that in the fourth quarter, we’re going to return to growth organically.”

They are even starting to show greater optimism regarding China, although I prefer to remain cautious and not count on significant growth in this region for now.

“I came away from the visit, seeing firsthand how well-positioned we are to capitalize on the market opportunities when the economy picks up in China.”

Finally, they also express confidence in their organic growth and acquisition strategy, which is allowing them to gain market share.

“Our growth strategy is driving share gain. Our PPI Business System enables outstanding execution. We have a disciplined capital deployment strategy that generates returns. Our acquisitions are performing well. And we’re going to be well-positioned to deliver differentiated performance once again in 2025.”

In conclusion, I think we should take these words with caution and wait to confirm this change in trend, but I believe there are already enough signals to be optimistic about recovery in the coming quarters.

Q3 Earnings

If we take a look at the latest earnings presentation, we can see how these recovery signals we mentioned translate into numbers. Sales growth was 1%, with 0% coming from organic growth, 1% from acquisitions, and, as noted earlier, COVID-19-related sales had a 0% impact this quarter. As we discussed, the impact of pandemic-related sales has almost completely vanished, and next year it will be nonexistent. Therefore, everything will depend on the organic and inorganic growth of the business itself.

Author’s calculations

If we break it down by segments, we see that most show almost no growth, except for Life Sciences Solutions, which continues to face more significant challenges:

-

Life Sciences Solutions: Declined by 6.4% compared to last year, representing 22.3% of sales.

-

Analytical Instruments: Grew by 1% year-over-year, accounting for 16.8% of total sales.

-

Specialty Diagnostics: Increased by 1.5% compared to the same quarter last year, making up 10.7% of sales.

-

Laboratory Products and Biopharma Services: Declined by 0.6%, representing 54.7% of sales.

The company’s optimization efforts have paid off, as evidenced by the third consecutive quarter of improved margins. Operating income reached $1.84 billion, with an operating margin of 17.3% (vs. 17.6% in 2023), driven primarily by improved gross margin and restructuring carried out in previous quarters.

Thanks to the improved conditions in the sector and the operational efficiencies implemented, the company has slightly raised its guidance for 2024:

-

Revenue: $42.4 to $43.3 billion

-

EPS: $21.35 to $22.07, a slight increase from the previous range of $21.29 to $22.07.

The Republican Victory Benefits Thermo Fisher

An interesting point to discuss is the recent decline in Thermo Fisher’s stock price, as well as that of other companies in the sector, following Donald Trump’s victory. Some investors fear that the deregulation proposed by the new administration could negatively impact Thermo Fisher’s business. From my perspective, not only do I believe this won’t be the case, but it might actually benefit the company.

Seeking Alpha

A broad deregulation could make patents obsolete and encourage greater competition among pharmaceutical companies for the development and commercialization of medicines. Let’s consider an extreme example—not something I think will actually happen, but it will help illustrate my point. Imagine Donald Trump cancels Novo Nordisk’s patent for Ozempic. This would obviously be terrible for Novo Nordisk, but it would be very beneficial for other pharmaceutical companies, which would now be able to market their own versions of the medication and compete in a market that was previously closed to them.

As I often point out, Thermo Fisher sells the “picks and shovels” of the pharmaceutical sector. When all these pharmaceutical companies start developing and researching their versions of Ozempic to bring them to market, they’ll need to purchase the necessary equipment and consumables to do so, directly benefiting Thermo Fisher.

Massive deregulation would eliminate efficiencies and economies of scale across the sector, leading to an increase in duplicated spending on machinery and consumables. Therefore, in my opinion, if this deregulation were to occur, Thermo Fisher and similar companies like Danaher could actually emerge as major beneficiaries, even though the market doesn’t currently perceive it that way.

As mentioned, the Ozempic example is simply meant to illustrate my perspective—by no means am I suggesting this specific scenario will happen. However, even a softening of certain regulations could result in similar effects on a smaller scale, potentially benefiting Thermo Fisher. In my view, the market is wrong to penalize Thermo Fisher for the Republican victory and fails to fully grasp the impact it could have on the healthcare sector.

Valuation and Conclusions

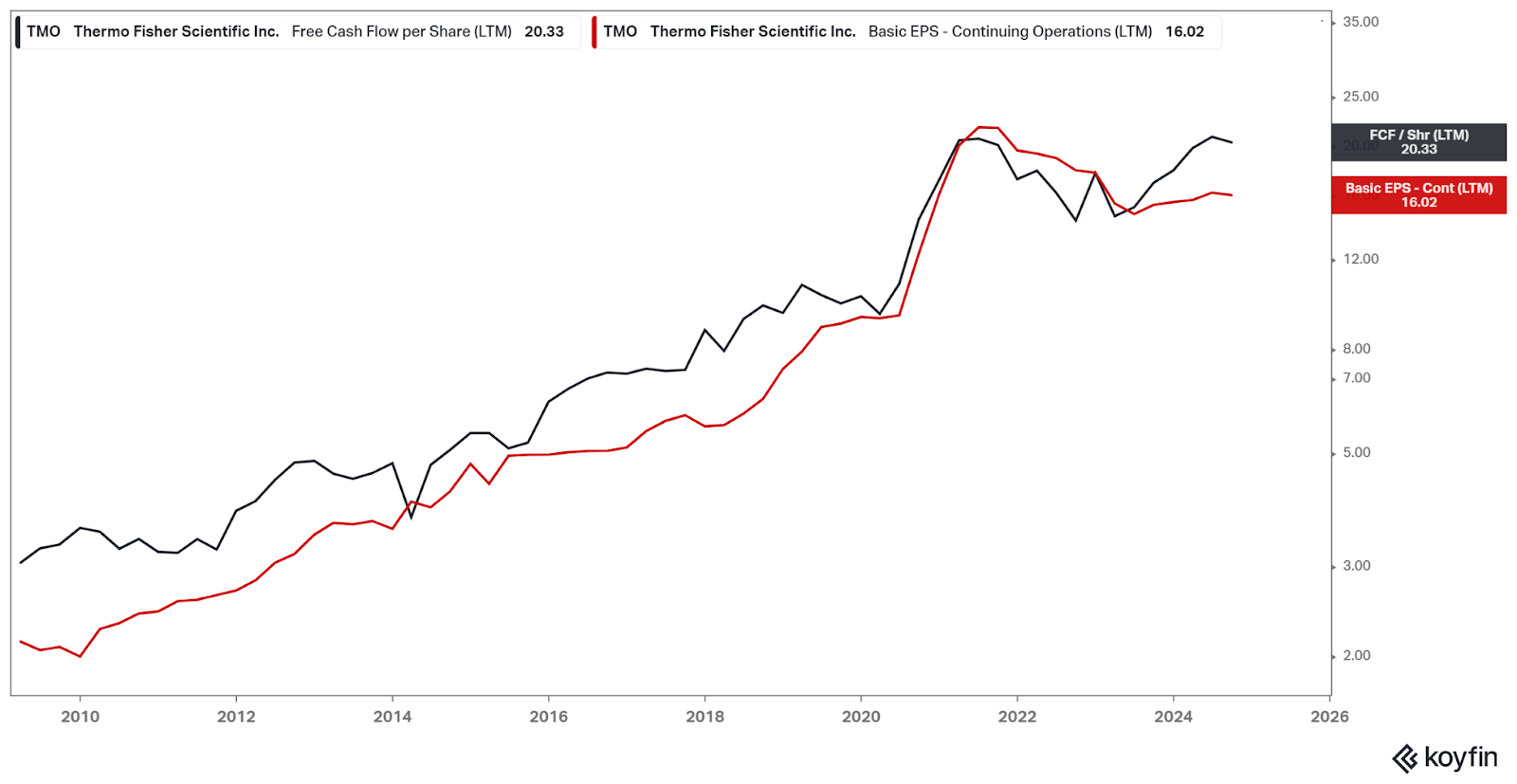

My valuation model hasn’t changed significantly because the company’s operational performance is in line with what I had expected in my previous articles. However, I’ve made an important change in how I value the company. In my earlier articles, I used EPS to determine the intrinsic value of the company. However, using this metric overlooks one of Thermo Fisher’s greatest strengths: its ability to convert earnings into cash flow.

Over the years, Thermo Fisher has consistently converted more than 100% of its net income into free cash flow, which is a remarkable quality. For this reason, I believe that FCF per share offers a better valuation metric than earnings per share. It more accurately reflects the company’s ability to generate cash, which ultimately drives value for investors.

Koyfin

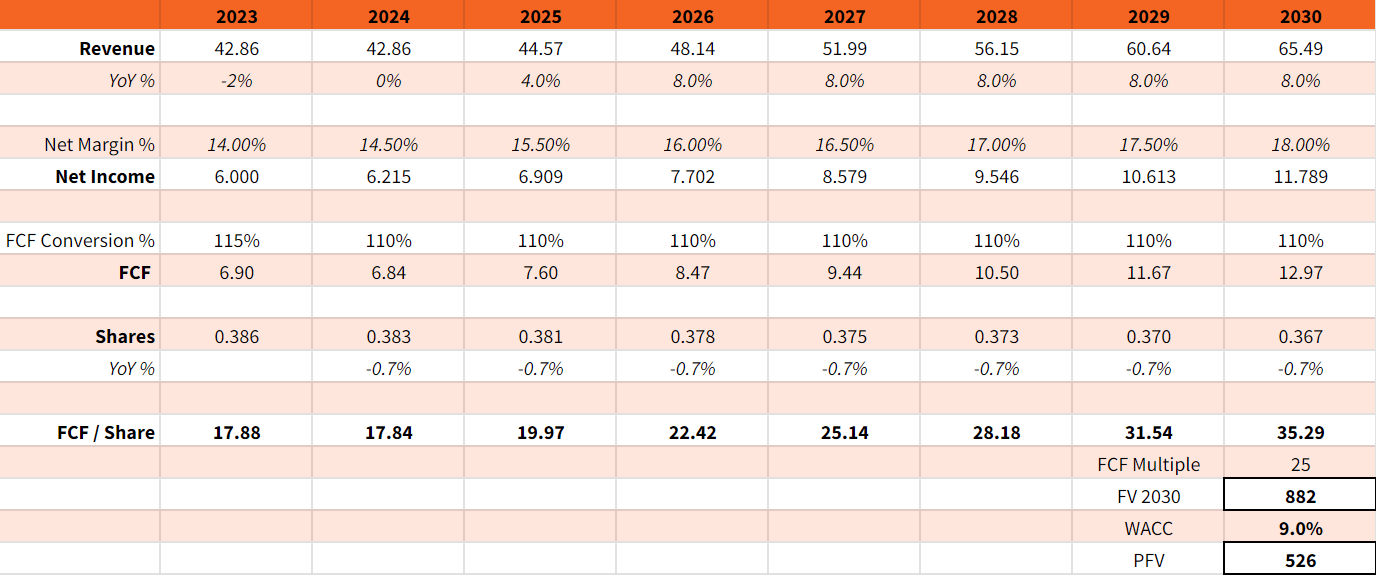

So, with this adjustment, here’s my base-case scenario for Thermo Fisher in the coming years:

-

Moderate sales growth of 4% for next year, followed by 8% long-term growth. Let’s remember that the company’s goal is to achieve 7-9% growth, so we are settling on the midpoint, which, I think, is reasonable to achieve.

-

Gradual margin expansion in line with the projections presented by the company during its Investor Day.

-

Free cash flow conversion of 110%.

-

Annual share buybacks of 0.7%, consistent with what they’ve been doing in recent years.

-

Exit multiple of 25x FCF. In my opinion, this is fair, given the superiority of Thermo Fisher’s business model and its terminal growth potential.

Based on this scenario, we arrive at a fair value of $882 for 2030, which, discounted at 9%, gives us a present fair value of $526. It’s worth noting that we haven’t accounted for net debt or the small dividend the company pays, but in this case, these don’t have a significant impact on the final valuation. Therefore, to achieve a 9% annual return, we should buy shares in the range of $520-535.

Author’s calculations

In summary, I don’t think this company will make you a millionaire, but if you’re looking for a conservative option with limited risk within the healthcare sector, I believe Thermo Fisher is a very good choice. As we’ve seen, we can conservatively expect returns of 9-10% from this company. However, if you’re aiming for slightly higher profitability, I’d recommend being patient and trying to buy it below $500.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.