Summary:

- During uncertain times like ours, we should invest in wonderful businesses at fair prices (rather than in fair businesses at wonderful prices).

- In the case of UnitedHealth, recent price corrections have created an excellent entry point to buy a wonderful business at some discounts.

- These price corrections are an overreaction to EPS headwinds, which are temporary only in my view.

jetcityimage

UNH Stock Is Loved By Wall Street

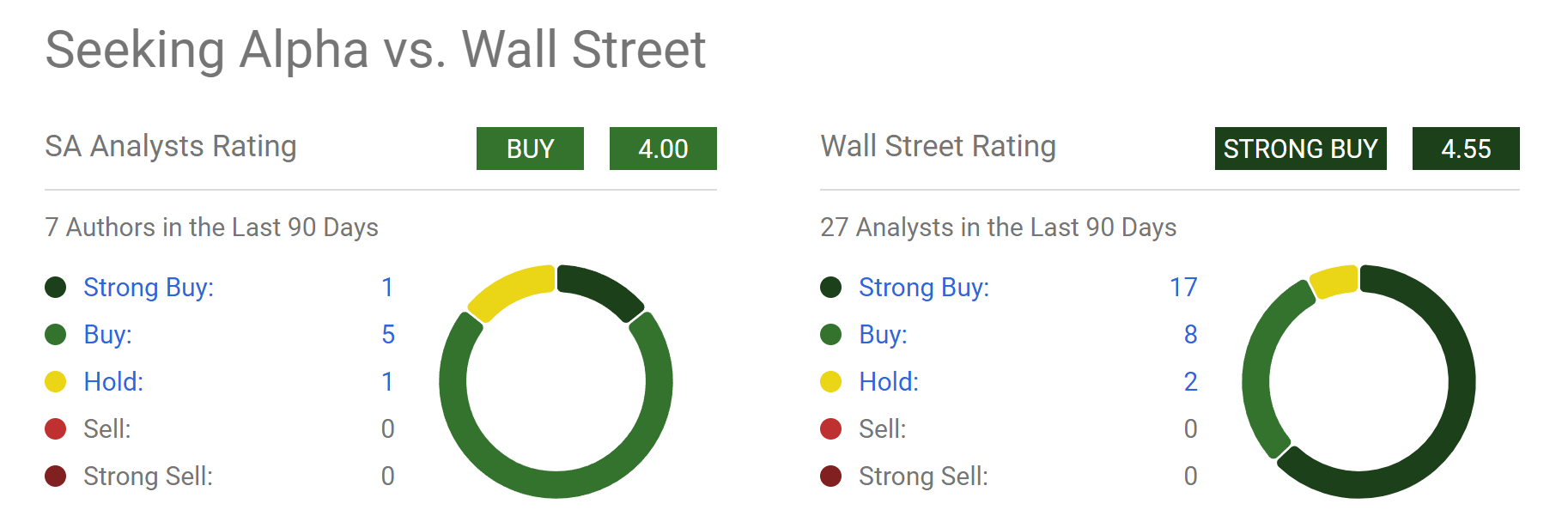

As contrarian investors, we often bet against Wall Street. However, in the case of UnitedHealth Group (NYSE:UNH) (NEOE:UNH:CA), we find ourselves in agreement with Wall Street ratings. As you can see from the chart below, the current sentiment on UNH stock is very strong from Wall Street analysts. To wit, Wall Street rates the stock as a STRONG BUY with a score of 4.55. Out of the 27 analysts writing in the last 90 days, 17 recommend Strong Buy and 8 recommend Buy. Only 2 recommend Hold and none recommend Sell or Strong Sell. The ratings from Seeking Alpha analysts are slightly less enthusiastic, but still represent a BUY.

Looking into the reasoning behind the above ratings, two things stand out. The first factor behind the bullish sentiment is the healthy outlook for the stock and the earning power in the long term. The second factor is that the recent price corrections have brought the valuation to a more reasonable level.

In the remainder of this article, I will present my independent assessment of both issues, and you will see my results support both factors.

Seeking Alpha

UNH Stock: EPS Headwinds Are Temporary

The recent price corrections were caused by some very valid concerns. But my view is that these headwinds are likely to be temporary only. A key concern at the top of my list is the Medicaid eligibility redetermination process. For this, I think the increase in its enrollment numbers, especially among commercial and senior patients, can more than offset the negative impacts due to this process. A second key concern on my list is the surge in insurance usage. To me, this is largely predictable, as we are gradually coming out of the pandemic. Indeed, by the end of 2023, UNH witnessed a medical cost ratio of 83.2% on average, up from 82.0% in the previous year. Moreover, that figure reached as high as 85.0% in the December period. However, I see such a surge as a one-time event (again, due to the aftermath of the pandemic).

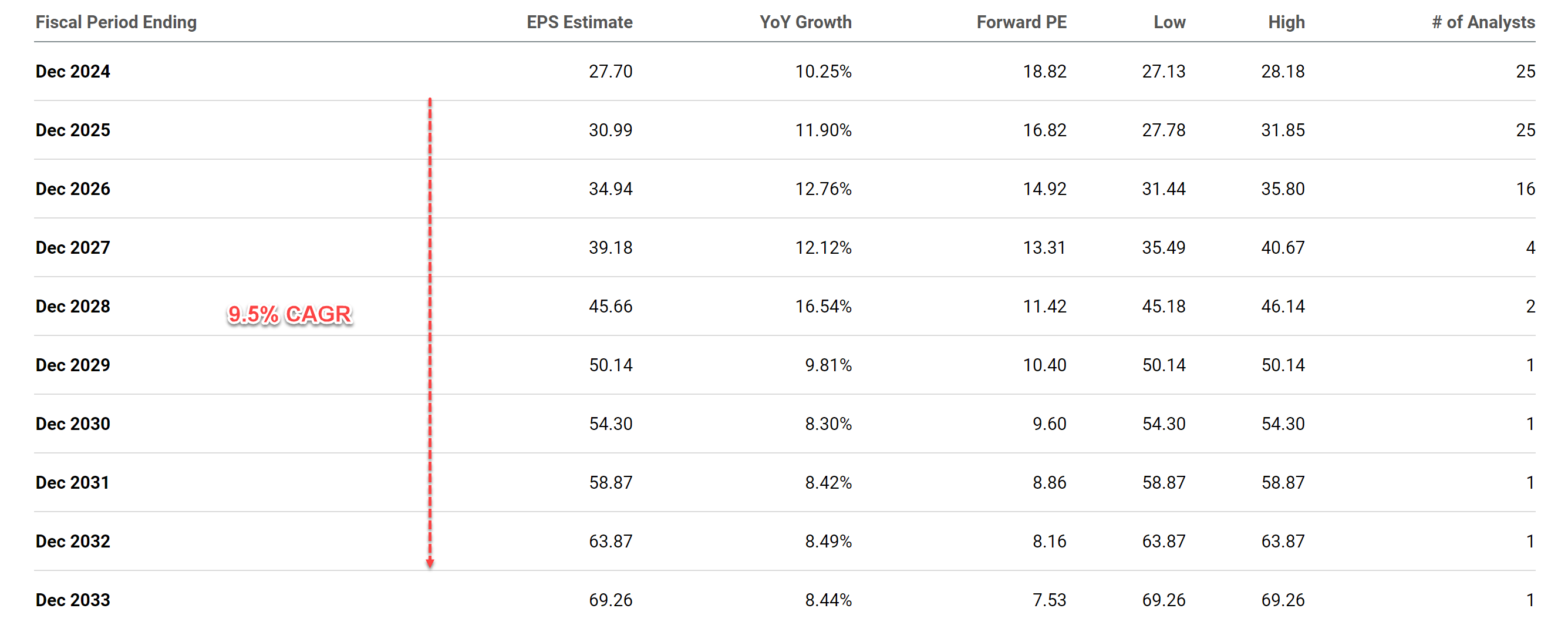

Looking ahead, the consensus EPS estimates point to a robust growth curve, as shown in the chart below. Analysts expect its EPS to grow steadily over the next decade at a CAGR of 9.5%. Given UNH’s scale and differentiation business model, I consider such projected growth to be very reasonable. The top two key differentiators in my mind are its vertical integration and data-driven approach. The vertical integration allows UNH to potentially manage costs more effectively and capture a larger share of the healthcare dollar. UNH has consistently invested in technology and data analytics, aiming to improve care coordination and optimize health outcomes for its members. This focus on data-driven insights positions UNH very well in the evolving healthcare landscape, in my view.

Seeking Alpha

UNH Stock: Valuation In Focus

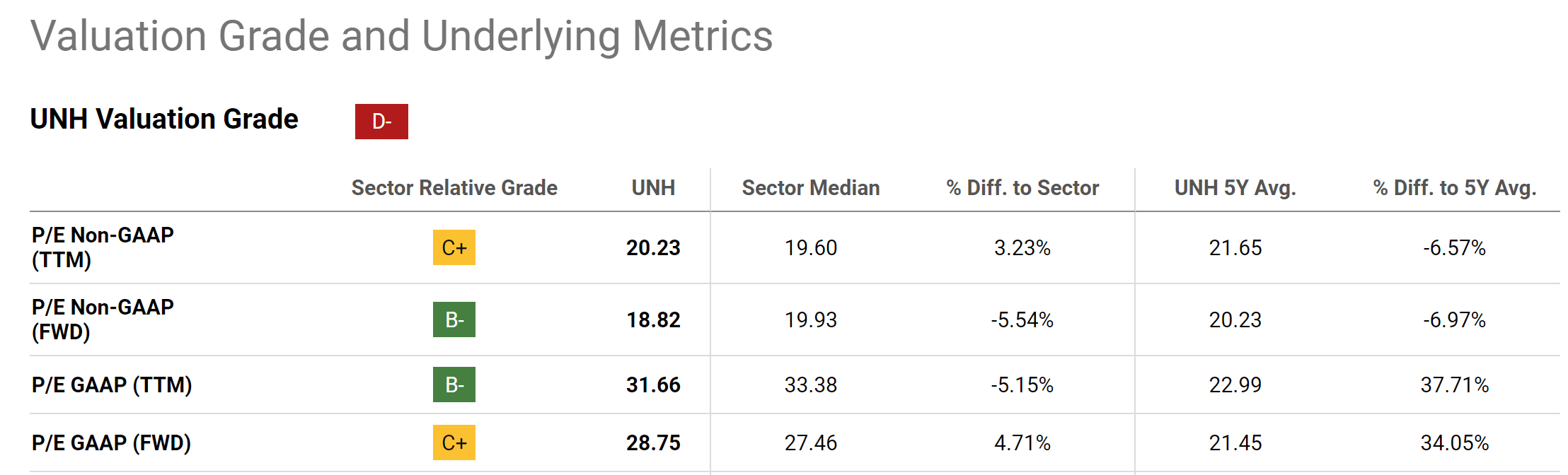

On to the second factor: valuation. Given its leading position and the above competitive edge, UNH has demanded a valuation premium over the sector most of the time in the past. However, due to the recent price corrections, the stock is not trading at a slight discount from the sector as seen in the chart below. In terms of FWD P/E on a non-GAAP basis, it trades at 18.8x, about 6% lower than the sector median of 19.9x. It is also about 7% lower than its 5-year average P/E of 20.2x.

Seeking Alpha

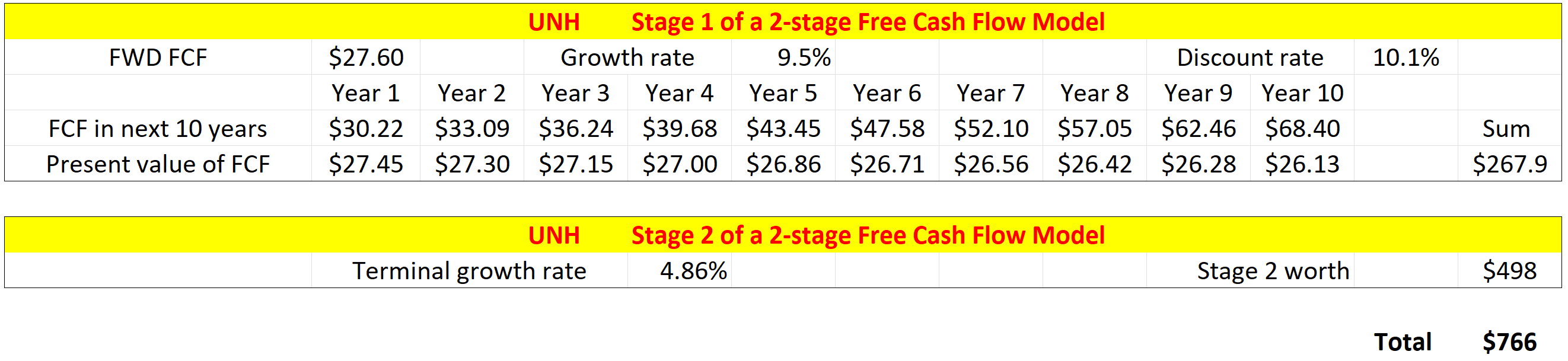

The discount is more substantial when compared to its fair price estimated from a two-stage discounted FCF model (free cash flow). The model is similar to the Discount Dividend Model (“DDM”) that was used in my earlier article on Microsoft (MSFT). And the only change I’ve made was to replace the dividends with FCF, as UNH only pays out a minor portion of its earnings as dividends (less than 30% on average). I will just summarize the key features of the model, so I can move back on to UNH:

There are a total of 3 key parameters in the 2-stage discounted FCF model: the discount rate, the growth rate in stage 1, and the terminal growth rate. For the discount rate, I relied on the so-called WACC, the weighted average cost of the capital model. The discount rate for UNH is about 10.1% on average in recent years following this model.

For the growth rate in the 1st stage, I will just use the 9.5% implied from market consensus based on the discussion above. For the terminal growth rates, I will estimate it based on the return on capital employed and reinvestment rate. The method is detailed in my other articles. I will just quote the end results for UNH here:

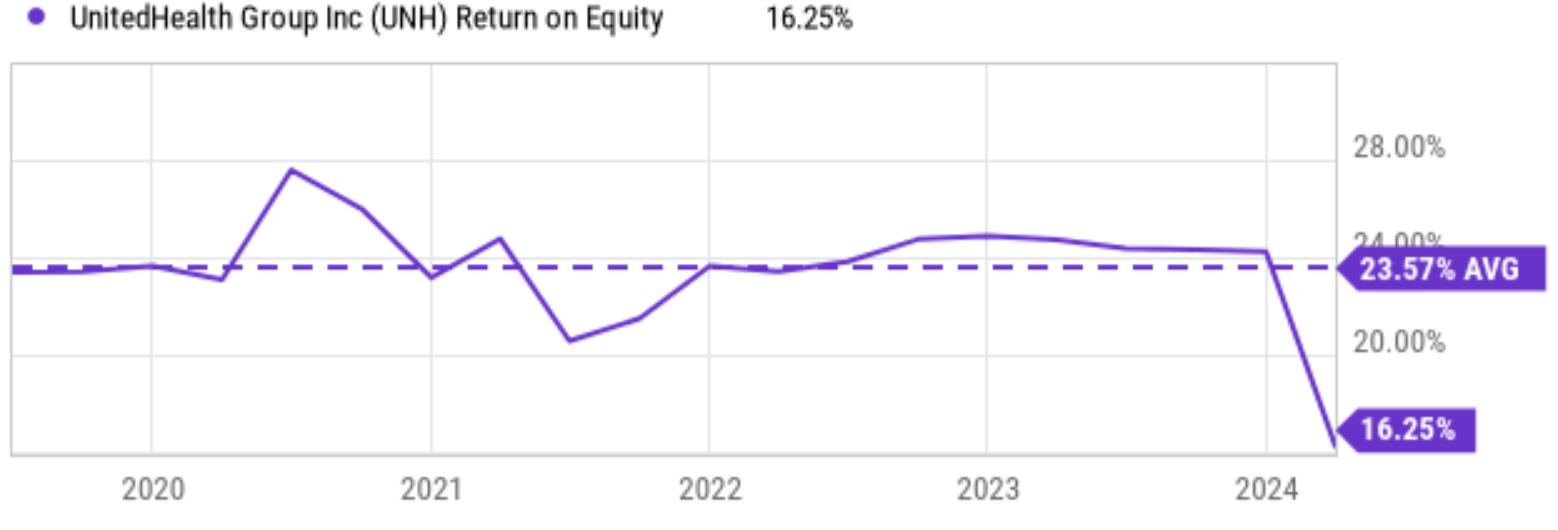

The method involves the return on capital employed (“ROCE”) and the reinvestment rate (“RR”). For a capital-light business like UNH (with negligible inventory and a minimal requirement on property, plants, and equipment), the ROE (return on equity) serves as an excellent approximation for ROCE. As seen in the chart below, UNH’s ROE has been around 23.57% on average in recent years. Assuming an RR of 10% in the long term, UNH’s perpetual growth rate would be ~2.36% (23.57% ROCE x 10% RR = 2.36%). Note this number is the real growth rate without inflation. To obtain a notional growth rate, one would need to add an inflation escalator. Assuming an average inflation of 2.5% would bring the terminal growth rate to 4.86%.

Seeking Alpha

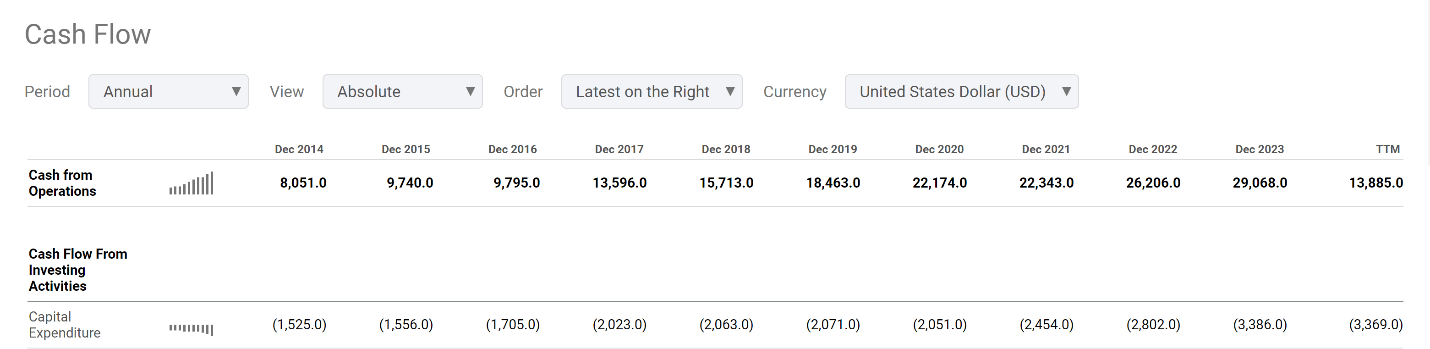

Finally, to estimate its FCF per share, I relied on its cash flow statement for 2023 as seen in the next table below. The FCF turned out to be $27.6 per share that year, with $29B of cash from operations and $3.4B of capital expenditures. With all these parameters, the last table summarizes the results from the 2-stage discounted FCF calculations. As you can see, the fair price of UNH turns out to be around $766. Compared to its current price of $581 as of this writing, there is a sizable margin of safety under current conditions.

Seeking Alpha

Author

Other Risks And Final Thoughts

In terms of downside risks, similar to other health insurance companies, UNH faces industry-wide risks like rising healthcare costs and potential changes in government regulations. The Medicaid eligibility redetermination process serves as a good example of this risk. There are also other potential regulatory changes that could negatively impact UNH. For example, changes in Medicare/Medicaid reimbursement rates could have a substantial impact on UNH. The government sets reimbursement rates for services provided to patients under Medicare and Medicaid. If these rates are reduced, it could decrease UNH’s revenue for these programs. Another potential risk involves regulations on prescription drug pricing. Recent efforts to address rising prescription drug costs could limit UNH’s ability to negotiate favorable prices with drug companies, potentially impacting its profit margins. Additionally, both UNH and its peers grapple with intense competition within the health insurance market. Additionally, the success of UNH’s data-driven approach could be disrupted by the recent rise of AI. The future in this space could be complicated by more intense competition (e.g., by the widespread of AI applications) and/or more stringent regulations to protect sensitive patient information.

All told, I agree with Wall Street that UNH represents a compelling BUY opportunity under current conditions. My overall feeling is that the positives far outweigh the negatives. It offers a well-rounded combination of growth potential, attractive valuation, and a stable business moat in a sector supported by secular tailwinds as our population ages. Finally, its superb balance sheet strength adds a further layer of safety.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Join Envision Early Retirement to navigate such a turbulent market.

- Receive our best ideas, actionable and unambiguous, across multiple assets.

- Access our real-money portfolios, trade alerts, and transparent performance reporting.

- Use our proprietary allocation strategies to isolate and control risks.

We have helped our members beat the S&P 500 with LOWER drawdowns despite the extreme volatilities in both the equity AND bond market.

Join for a 100% Risk-Free trial and see if our proven method can help you too. You do not need to pay for the costly lessons from the market itself.