Summary:

- Chinese steel sector should rely on exports to recover from residential construction crash.

- Seaborne iron ore prices may remain above $100 for an extended period.

- Vale’s valuation is discounted compared to Australian peers, suggesting potential for a 25% share price increase.

zssp/iStock via Getty Images

Summary

Vale (NYSE:VALE) has been range bound for the better part of 3 years driven by investor skepticism surrounding the future of China steel demand and the residential construction crises despite consistently high IO (iron ore) prices. I believe that IO prices can stay above US$100 as Chinese steel capacity maintains near peak on increasing exports. At some point Vale should close some of the valuation gap vs Australian peers, which points to 25% share price upside potential with a 7% dividend yield.

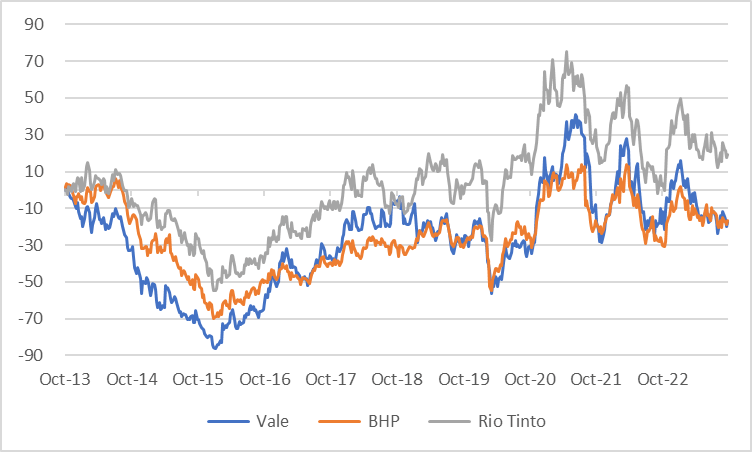

Vale Relative Share Performance vs Peers (Created by author with data from Capital IQ)

Investment Thesis

Vale is one of the largest seaborne IO miners with the bulk of sales going to China. As such the price setters are Chinese steel companies and their demand for IO has been thought to be greatly dependent on residential construction, which many investors are aware is in a structural decline after decades of overbuilding. The resiliency of IO prices has not translated into a higher share price for Vale, but rather a decline in valuation. The market simply does not price in current IO levels into the future.

The key question for Vale: What is supporting IO prices and can this be maintained.

There are 4 reasons to forecast higher for longer IO prices

- China steel demand can continue near capacity via exports.

- Chinese iron ore capacity and quality is restricted.

- Seaborne IO should continue to represent the bulk of demand input.

- The top 4 IO miners are not planning significant expansion.

This means that the seaborn IO miners have entered maturity with a few resounding caveats, there main client depends on them, there are scant substitutes for exported iron ore and the Chinese steel sector can take share from other steel makers via pricing. In essence the iron ore miners are in symbiotic existence with the Chinese steel sector.

Thus, the key to Vale fundamentals is the health and peculiarity of the Chinese steel sector. As with the case for many Chinese companies, the creation of shareholder value may not be a priority. Employ and produce is more relevant. As long as the steel companies can run production at near breakeven (with plenty of govt subsidies) they will make steel products for China and export the rest. The exports prices can and have been highly competitive, perhaps predatory or dumping but that’s the operating model.

Vale and the Australian IO miners see peak China steel production in sight and should limit capacity expansion or perhaps begin to reduce. This is similar to what many oil companies are doing, rationalizing capex, attempting to balance supply with demand and maintaining reasonable prices that permit very healthy FCF and dividend payouts i.e. capital discipline.

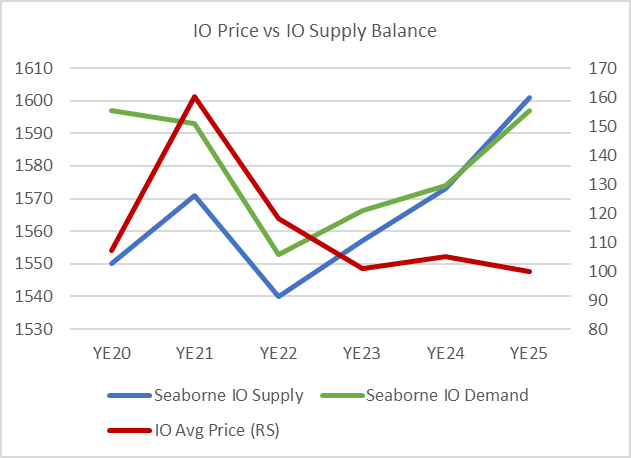

Iron Ore Price vs Supply and Demand (Created by author with data Vale)

The Iron Ore Balance

China is 50% of global steel capacity (1bn tons) and it consumes most of the seaborn IO, about 85%. Thus, as real estate construction demand fell and continues to decline (massive over building) China steel companies will export and displace share in any market without high import barriers.

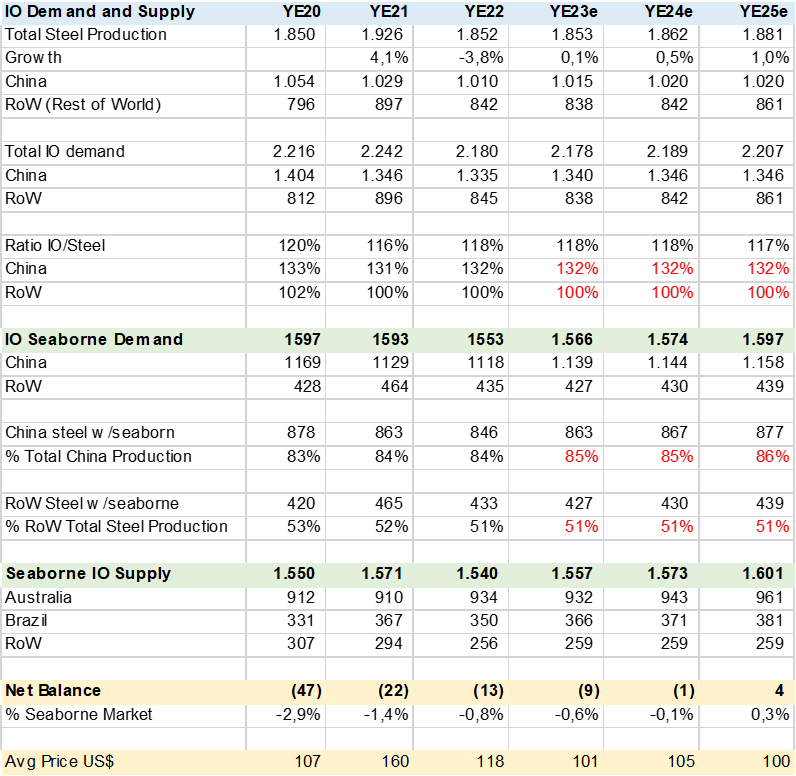

Below are my estimates of the seaborne IO balance between supply and demand. There are many drivers and moving parts. Fundamental to seaborne IO demand is that Chinese steel output remains near peak or near capacity while its primary suppliers do not add significant capacity. Note that I assume global steel demand grows at half a percent in 2024 and 1% in 2025, any move higher means greater IO imbalance.

Steel and Iron Ore Supply and Demand (Created by author with data from GS, Vale, Rio Tinto and BHP)

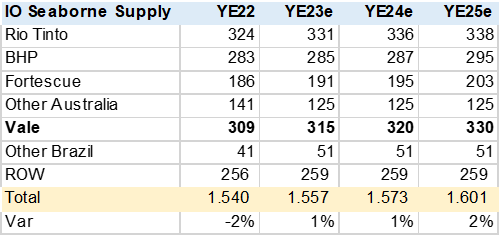

IO Capacity Estimates (Created by Author with data from Vale, Rio Tinto and BHP)

What Has Happened In The Chinese Steel Sector?

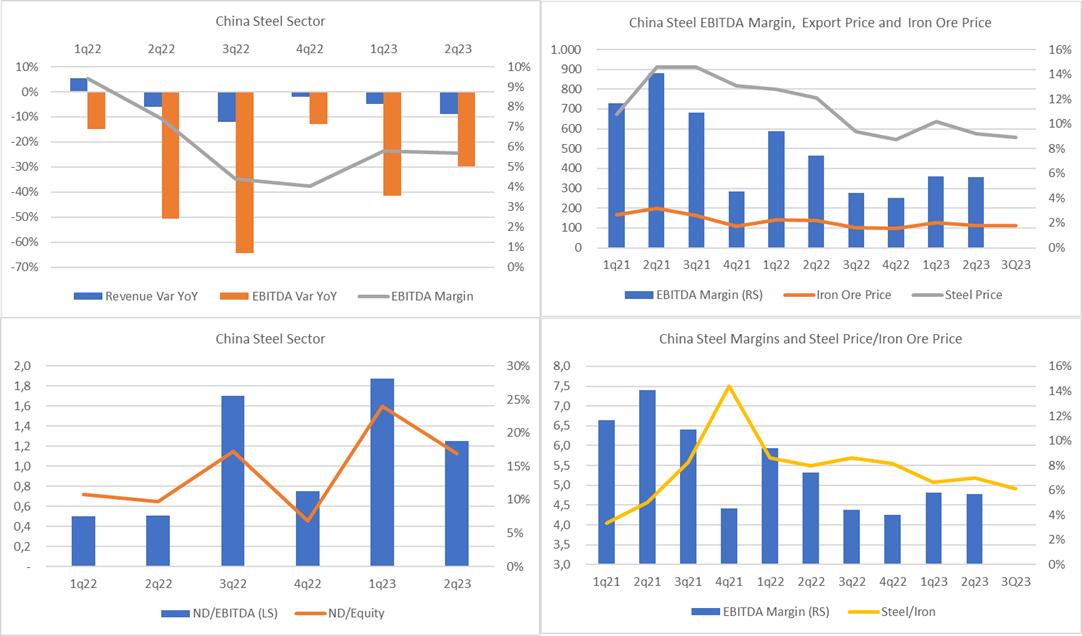

The Chinese Steel sector is large and divers, I found data and consensus estimates for 9 companies. One of the largest is Baoshan with 50m ton capacity (5% of total).

Contrary to headlines, the sample group, seems to be weathering the real estate construction sector decline well. Revenue and EBITDA has fallen up to 1Q23 and now turned positive in 2Q23. Steel prices seem to have stabilized at above US$500mt with the ratio to iron ore prices at 5x (4x is thought to be healthy). Balance sheets seem to be in good shape with leverage under control.

Chinese Steel Financial Data (Created by author with data from Capital IQ)

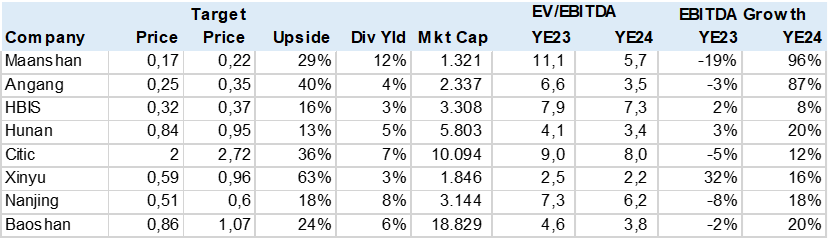

The market, as judged by consensus estimates, seems to have a favorable outlook for the sector with over 20% upside and a significant EBITDA rebound in YE24. The demand side dynamics for iron ore looks robust or at least better than in YE22 and YE23.

Chinese Steel Consensus Data (Created by author with data from Capital IQ)

Peer Comps Iron Ore Miners

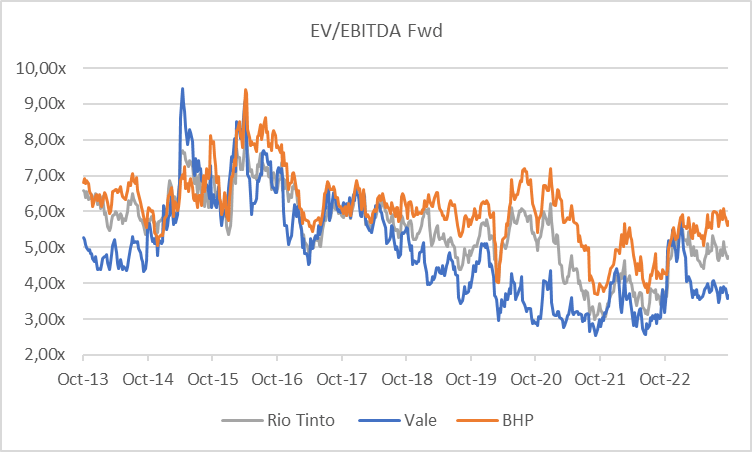

Vale compares well on fundamentals vs. its peer group of IO miners such as BHP (BHP) and Rio Tinto (RIO). We see similar growth and margin profile but at a lower valuation due primarily to lower business risk on product diversification and country risk i.e. Australia vs Brazil.

IO Mining Stock Comps (Created by author with data from Capital IQ) Vale and Peers Forward EV/EBITDA (Created by author with data from Capital IQ)

Valuation

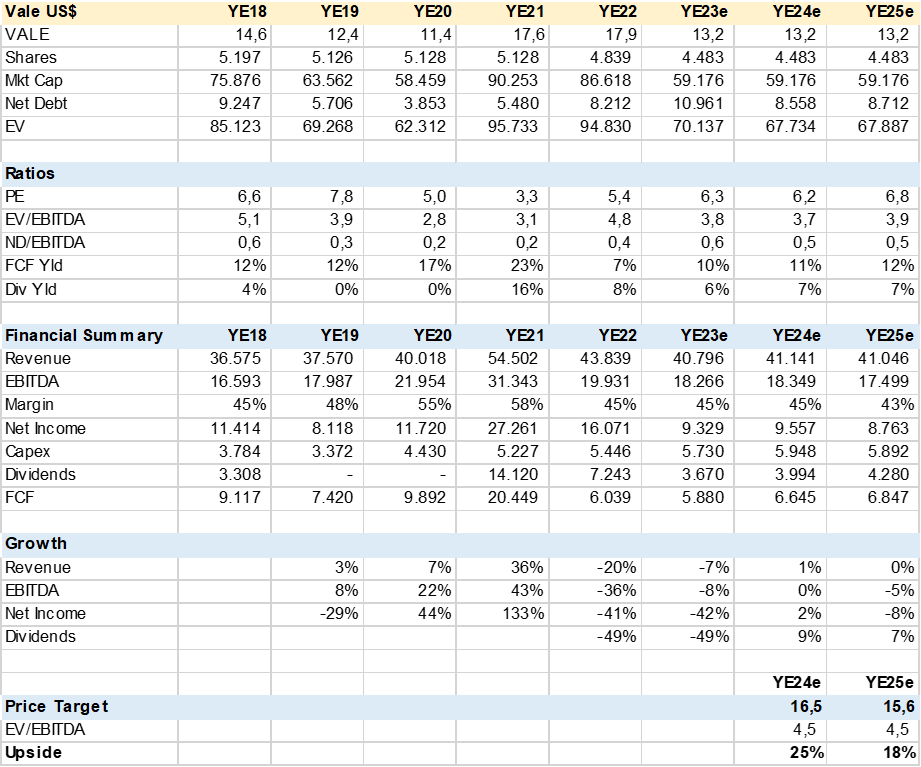

The stock is cheap vs peers and relative to FCF generation and dividend payout trading at 3.7x EV/EBITDA and 6.2x PE on YE24 consensus estimates. The US$16.5 price target is based on a 4.2x EV/EBITDA target multiple, below peers such as Rio Tinto and BHP, which have a slightly lower risk profile as Australian companies.

Vale Consensus Estimates and Valuation (Created by author with data from Capital IQ)

Conclusion

Vale is a BUY on positive IO price dynamics supported by Chinese steel exports which drives significant free cash flow and dividends/share buy backs. The stocks valuation is discounted vs peers which further supports a possible re-rate and 25% upside potential.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.