Summary:

- Brazilian miner Vale is a great investment for the iron ore price uptick. Even though its price declined over the past year, in recent months, it has already started climbing.

- Despite this, its market multiples are still far more attractive compared to other big iron ore producers. With improved revenues and earnings expected in 2024, further price upside is likely.

- Even considering currency and macro risks, Vale looks like a good buy for this year.

Opla

The past year has been relatively weak for miners, with a 5.6% increase in the S&P 500 Metal and Mining Select Industry index compared to a 22.1% increase in the S&P 500 (SP500) index over this time.

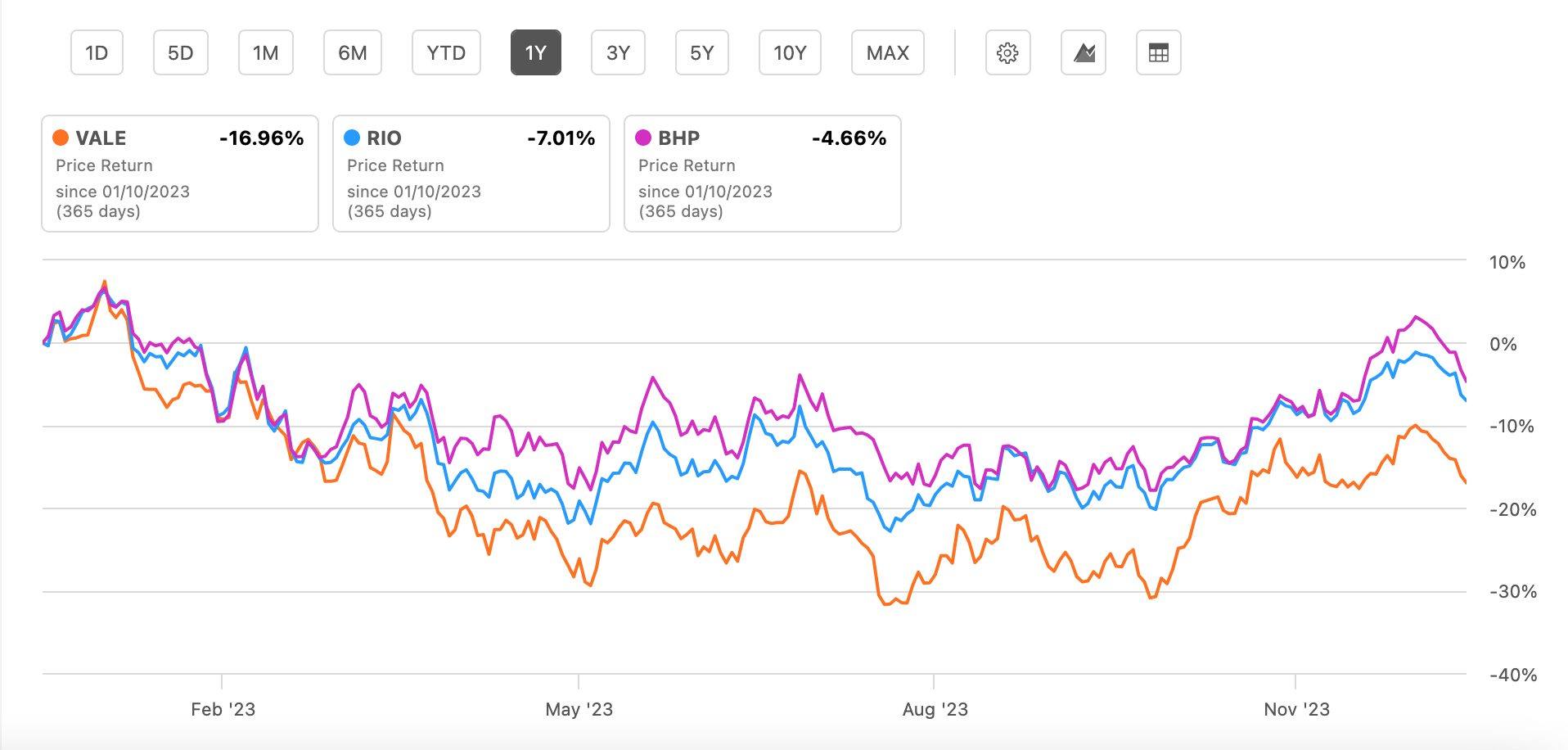

But it has been even iron ore miners. The three biggest ones, the Brazilian Vale (NYSE:VALE), Rio Tinto (RIO) and BHP (BHP) have all seen a share price pullback over this time (see chart below). Vale has had it the worst with a price decline that’s more than double that for RIO, the second worst of the three.

Here I take a look at whether the next year looks as bad for Vale or if there’s scope for an uptick now.

Price Returns, Iron Ore Producers (Source: Seeking Alpha)

Supportive iron ore prices

As it happens, the recovery is already underway. The yearly stock price trends obfuscate the fact that over the past six months, Vale has risen by almost 13%. In fact, it has seen a slightly bigger price rise than both Rio Tinto and BHP during this time. This is no surprise considering that almost the entire adjusted EBITDA and over 80% of the net operating revenues for the company come from iron.

Underpinning the renewed optimism in iron ore producers is China’s support to the economy, which is the world’s biggest consumer of the commodity. The news sent iron ore prices rallying, which are now up by 39% since the lows seen last May.

Iron Ore Price (Source: Trading Economics)

Improved iron ore prices along with better sales volumes have already reflected positively on Vale’s third quarter (Q3 2023) results. Its net operating revenues grew by 9.8% year-on-year (YoY) and the adjusted EBITDA increased by 12%. This is in stark contrast with an 18.6% revenue decline in 2022 and a 37% contraction in adjusted EBITDA in the full year 2022.

Small revenue rise seen in 2024

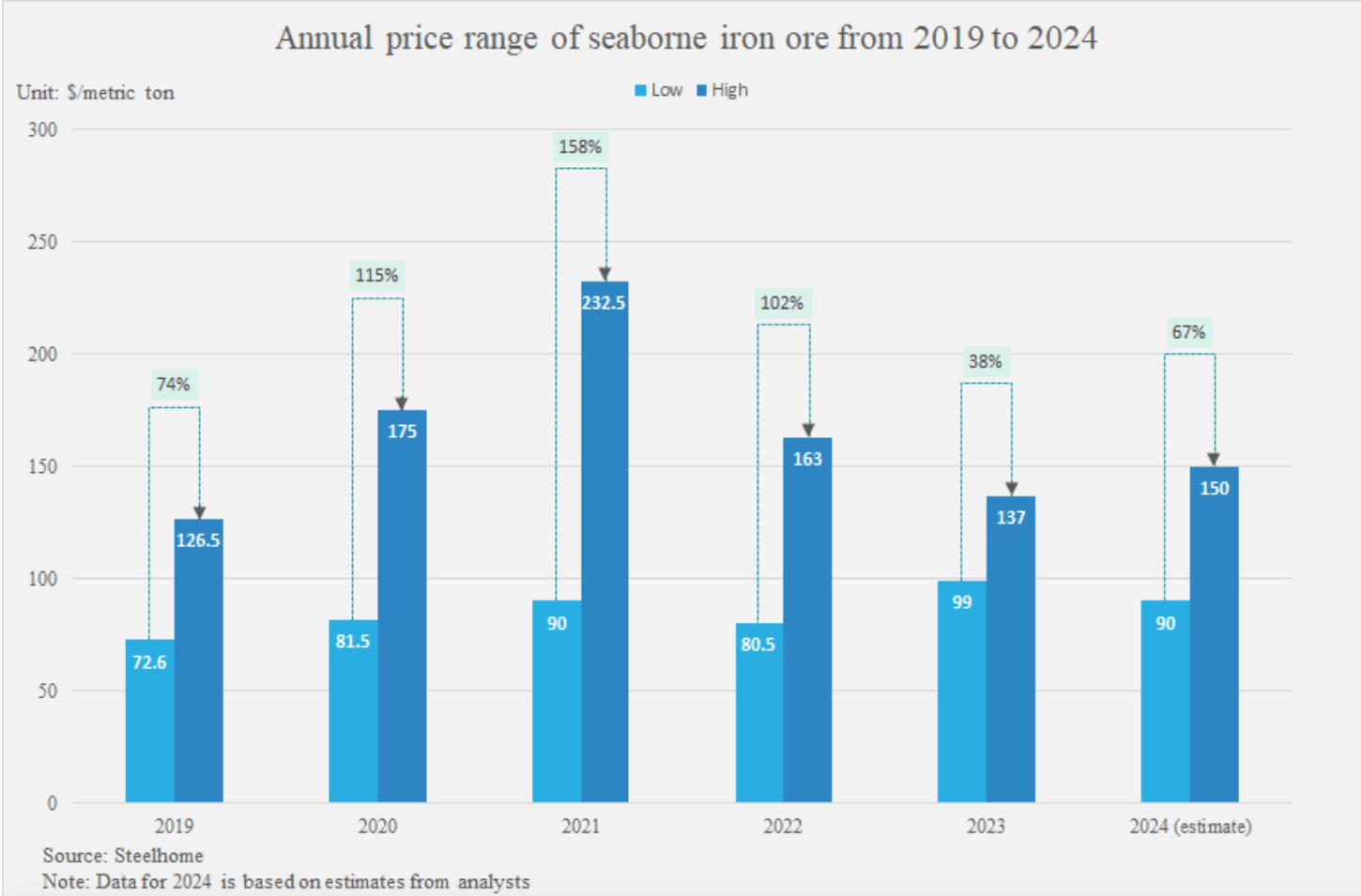

Revenues can continue to improve in 2024 as iron ore prices are stable to increasing during the year. According to China’s data and consulting provider Steelhome, the average price of seaborne iron ore is expected to be slightly higher at USD 120/metric ton [mt] in 2024 compared to USD 118/mt in 2023.

Source: Steelhome

Further, Vale’s iron ore production is expected to be similar to that in 2023. The company has a production target of 310-320 mt for 2024, compared to the estimate of 315 mt of production for 2023. In line with this, analysts expect a 1.4% increase in the company’s revenues for the next year.

Earnings jump expected

But the earnings per share [EPS] are expected to rise much faster by 14%. At first glance, this sounds too optimistic. Even as the iron ore price rise in Q3 2023 resulted in improved revenues, the net earnings attributable to shareholders fell by 36.3%, making it the seventh consecutive quarter of shrinking earnings for Vale.

However, the picture becomes clearer when we consider two facts. In Q3 2023, the company’s adjusted EBITDA figures were already up as earlier noted. This indicates that the net attributable income declined for factors other than the revenue-cost dynamic. The answer is found in foreign exchange losses.

In Q3 2022, Vale had seen currency gains of USD 1.8 billion as opposed to a USD 102 million loss on the same account. If it had instead posted the same foreign exchange gains, the income would, instead have risen by 6.3%. With improved pricing conditions through 2024, we can then reasonably expect earnings gains.

Risks to the outlook

But the risk of another year of currency losses can’t be ignored either. While a small revenue uptick is forecast, it’s not enough to counter these losses if they occur.

Moreover, there’s the slowdown risk to consider. Even though China is expected to see continued healthy growth in 2024, other big economies like the US and euro area are seen slowing down. If the slowdown is bigger than is now forecast, it can dent both Vale’s revenues and earnings.

Attractive market multiples

Even taking the risks into account though, Vale’s market multiples look rather attractive. Not only are they lower than that for the materials sector, but they are also better than those for other iron ore producers.

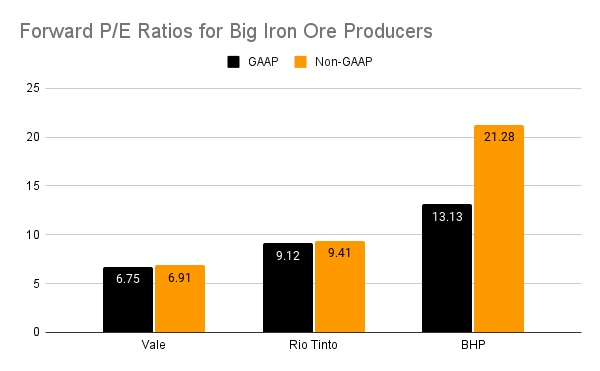

The forward non-GAAP price-to-earnings (P/E) for Vale is at just 6.9x compared to 16.35x for the materials sector, while the forward GAAP P/E is at 6.75x compared to 16.8x for the sector.

If this isn’t convincing enough, the same trend is reflected in its comparison with the other big iron ore producers, Rio Tinto and BHP (see chart below). If Vale’s forward P/E were to rise to the average of the non-GAAP forward P/E for both its peers, its share price could double.

Source: Seeking Alpha

Now, these forward ratios are for 2023, results for which will be out soon. To get a better perspective on what 2024 could hold for Vale, I also looked at the forward P/Es for this year. The same trend shows up. While Vale is at 6.1x, Rio Tinto and BHP are at 8.6x and 23x respectively. This further confirms the potential for a price rise this year.

The company’s current share buyback programme for 3.5% of its shares outstanding can also improve the price. Besides this, its 7.9% dividend yield significantly adds to the returns on an investment in the stock.

What next?

With the commodity cycle coming out of a weak place now, there’s a good chance that Vale can be an outperformer in the stock markets in 2024. The stock’s uptick has already started, as seen in the price rise over the past six months.

Despite this, its market multiples are still low compared to other iron ore producers, indicating much further upside ahead, further backed by its share buyback and dividends. Additionally, its improving financials should add to investor confidence in the stock. There are still currency and macro risks to the stock, but on the whole, there’s more going for Vale than not. I’m going with a Buy rating.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in VALE over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

—