Summary:

- Verizon Communications Inc. Q2 earnings were solid, with revenue slightly below expectations but strong wireless growth and cost controls leading to outperformance in operating income and adjusted EBITDA.

- Despite concerns about debt, Verizon’s free cash flow remains strong, with a well-covered dividend and plans for debt reduction in the future.

- Investors should consider Verizon for income, as the company is on track for significant free cash flow and growth in various financial metrics, with better days ahead.

Paper Boat Creative

We reiterate our Buy rating on Verizon Communications Inc. (NYSE:VZ) shares today following the just-reported Q2 earnings. While we have had a buy rating on the stock since the low $30s, the stock has stalled out hitting the $40s. In our opinion, Q2 earnings were solid, and today’s mini selloff creates a buying opportunity once again in the $30s. Let us discuss.

Verizon Q2 results in context

Markets have started an interesting rotation of late. As a telecom with a strong dividend yield, Verizon stock is likely to hold up in this environment. While Verizon stock rallied hard last year and into 2024, the mostly sideways action recently is not all that bad if you are buying for income.

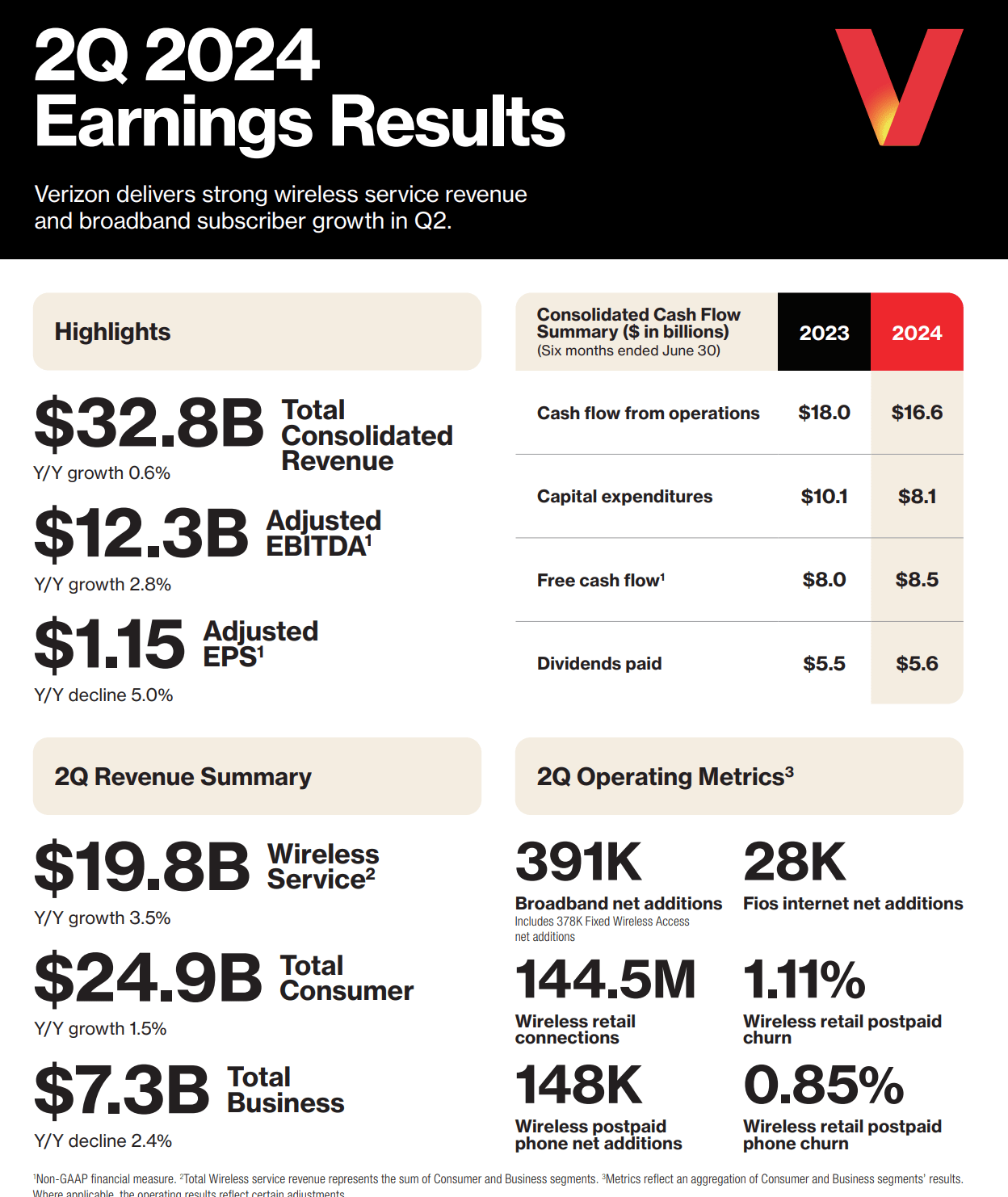

That said, Verizon’s revenues were below expectations. While we thought Verizon may once again have difficulty with margins and earnings from being very promotional to attract customers, the earnings power was once again strong considering a revenue figure that missed expectations by $240 million. Revenue came in at $32.8 billion and rose 0.8% from last year. See the Q2 infographic below:

Verizon Q2 Infographic

The metrics of most importance are largely summarized above for Q2. Wireless growth was strong, while business suffered once again.

Verizon’s Q2 2024 earnings revenue drivers

As we saw, revenues rose 0.6% but were below expectations. For Q3, we were looking for $33.0-$33.2 billion for the top line, so the Q2 revenue results were also below our projections. We were slightly more bullish than consensus. Our expectations were missed by $300 million. What about customer additions? We were looking for retail postpaid net additions of 100,000+ and wireless postpaid phone gross additions to increase in low-single digits year-over-year. Furthermore, We were looking for phone churn below 1.0% for retail postpaid customers. For broadband, we were looking for net additions of 400,000 and were projecting 25,000+ Fios Internet net additions.

In wireless, we saw 3.5% revenue growth from last year to $19.8 billion. Retail postpaid phone net additions were 148,000, and retail postpaid net additions were 340,000, both above our expectations. Retail postpaid phone churn was just 0.85% while postpaid customer churn was 1.11%. Over in broadband, there were net additions of 391,000. Once again here in Q1 2024, we saw continued robust demand for fixed wireless and Fios products, though this missed our expectations slightly. There were 378,000 fixed wireless net additions.

This is the second quarter in a row of sub-400,000 broadband net additions. We do not see this as bearish, the growth remains strong and there are well over 3 million subscribers. There were 28,000 Fios Internet net additions, also surpassing our expectations of 25,000. Overall, it was a good but mixed quarter, especially when you consider business lines continue to decline

Verizon Q2 2024 earnings outperformance

For Q2, we had once again been expecting ongoing cost controls to continue to help earnings power. Remember back in Q1, we also learned Verizon is turning to AI. The AI is being employed to improve the efficiency of the overall business and to boost customer service. Q2 2024 operating expenses were $24.98 billion while we were targeting operating expenses of $25.0-$25.2 billion, so this was slightly better than expected, and was down from last year’s operating expenses of $25.37 billion. We were targeting an operating income of $7.6-$7.8 billion. Verizon reported $7.8 billion in operating income, and this was up 8.3% from last year’s $7.22 billion.

For adjusted EBITDA, we are targeting $12.0-$12.2 billion. On a per-share basis, assuming our projections capture the results with relative precision, we saw EPS of $1.15-$1.18 for Q2. Analysts were looking for $1.15, the low end of our target range. Well, despite the top-line miss, with well-controlled operating expenses, the company reported $1.15 in EPS, meeting consensus expectations. Adjusted EBITDA was $12.3 billion, also surpassing our expectations slightly.

Verizon’s free cash flow

Assuming cash flow from activities of $8.8 billion-$9.4 billion, capex and other expenditures of $4-$4.5 billion, we were targeting free cash flow of $2.7 billion to as high as $4.8 billion. Well, cash flow from operations was $9.5 billion, and Capex was $4.1 billion. Keep in mind that Verizon pays more each year to the dividend. Dividends paid were about $2.8 billion in Q2. Free cash flow was $5.8 billion, at the higher end of our free cash flow expectation. As such, the free cash flow payout ratio was about 48%.

For the year, we are anticipating a payout ratio of less than 75%. We are on a good path to that figure thus far, as $5.6 billion in dividends have been paid out of the $8.5 billion in free cash flow, or a 66% payout ratio.

Update on the debt

Verizon will always carry a debt load. Why? Because there will be constant new refinancing or issuing of debt to fund new constructions, research, spectrum auctions, to build out AI, grow the business etc. That said, leverage must be reduced because the debt is using up a ton of cash flows. The debt burden is large, make no mistake. Interest expense will continue to climb on new debt at higher rates in this climate. So, the company is trying to chip away at the debt. The net debt dipped slightly to $122.0 billion, down $4 billion from the start of the year, and the net debt-to-adjusted EBITDA ratio ticked down from 2.6X in the sequential quarter to 2.5x this quarter.

Final thoughts: a buy for income

For the many income seekers, the dividend is well-covered. Verizon is certainly on track for about $19 billion in free cash flow this year. Changes to this outlook could hit the stock, but right now, while there were mixed results for customer and business growth, the key here is that free cash flow is growing and debt is being chipped down. Taking this quarter’s results into consideration, we still expect to see growth of 2-3.5% in total wireless service revenue, total revenue growth of flat to up 2%, adjusted EBITDA growth of 1-3%, and adjusted EPS of $4.50-$4.70. Management did actually guide to this exact earnings range as well, versus $4.57 consensus. Today’s dip back into the $30s is a buying opportunity.

Have something to share?

Do you think the company’s future is looking shaky? Can they overcome their debt burden? Are you a long-term investor, holding on to the stock for dividends? Do you trade options for this company’s stock? What’s your strategy for maximizing gains? Know of any other dividend-paying stocks that are strong contenders? Anything else to add to the discussion?

Analyst’s Disclosure: I/we have a beneficial long position in the shares of VZ either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Pay yourself dividends with outsized returns

Get more with our playbook to advance your savings and retirement timeline by embracing a blended trading and investing approach at our one-stop shop. Start winning TODAY.

Our prices go up soon, but if you act now through this column, you can lock in $65 off our annual price.

We invite you to try us out, with a money back guarantee if you are not satisfied within your first 30 days. There’s also a light version of BAD BEAT, on sale for 55 cents a day with great benefits too. Come take the next step!