Summary:

- Visa’s impenetrable moat and position in an industry experiencing secular tailwinds make it compelling for a GARP-style investment.

- Visa returns virtually all free cash flow to shareholders, with the current shareholder yield of about 4% poised to drive strong low mid-teens EPS growth for years to come.

- Visa’s revenues are inflation protected and exposed to many areas of the economy, not just consumer spending, allowing investors to participate in global economic growth and the transition from cash.

- Regulatory risks have resulted in fines in the past, but the moat around Visa’s payment network has remained intact against a host of threats, demonstrating resilience.

- Visa’s exposure to cyclical discretionary spending affords it strong growth when times are good, but it generated enough operating income in the last year to pay off almost all of its long term debt, showcasing a rock-solid balance sheet that can weather recessionary environments with strength.

FinkAvenue

Visa (NYSE:V) is one of the most recognizable brands worldwide. With a market cap of over $600 Billion, the company is one of the largest in the world, comprising about 1% of the S&P 500. It has an unusual corporate history dating back to the 1950s, which has led to its ascension as the largest payment processing company outside of China. The company’s egregiously lucrative business model has made it one of the most hated corporate entities in the world, despite its place as a provider of critical payment security infrastructure. Today, I want to dive into the company and summarize why investors might find it compelling as a long-term investment. From its oligopolistic market dominance and impressive financial metrics to its robust economic moat and consistent shareholder returns, Visa offers a unique combination of growth and stability. In this analysis, we’ll explore Visa’s corporate history, financial performance, valuation, dividend policies, risks, and market position to uncover what makes it a standout player in the global financial landscape-and why it might deserve a place in your portfolio.

Investment Thesis

Visa’s investment thesis is built on two primary drivers. First, it benefits directly from global GDP growth by capturing a small percentage of every transaction processed through its network. This makes Visa a play on steadily increasing global spending. Second, Visa stands to gain from the secular shift toward a cashless society as businesses and consumers increasingly adopt digital payment systems. The company’s business model is highly scalable, taking a toll-like fee on every transaction processed through its VisaNet network. This model not only ensures indiscriminate growth across non-sector-specific spending, but also provides strong inflation protection, as Visa’s revenue grows proportionally with rising prices and across goods and services.

As the largest payment network globally, VisaNet has created a moat for the company that is virtually impenetrable. This moat is further strengthened by Visa’s ability to continually expand its network through new card issuances and increasing transaction volumes, while occasionally bolting on value-add services that allow them to monetize the network infrastructure they have further. While the company is rarely at a value price and certainly isn’t now, I think it is a fairly low-risk investment that has potential to provide steady shareholder returns for many years across economic cycles.

Company Overview and History

Founded in 1958 by Bank of America (BAC) Visa began as the BankAmericard credit card program, marking the first general-purpose credit card issued by a conventional bank. Initially created to facilitate consumer credit, the program was a success and eventually evolved into VisaNet, the world’s largest payment processing network. In 1976, the program was rebranded as Visa and transformed into a cooperative owned by issuing banks. My suspicion is that BOA knew that forming into a cooperative would ultimately mitigate regulatory concerns and scrutiny of the network from government entities; however, I am just speculating there. I welcome my readers to provide their thoughts on this.

The first BankAmericard was launched in 1958 in Fresno, CA (bankerandtradesman.com)

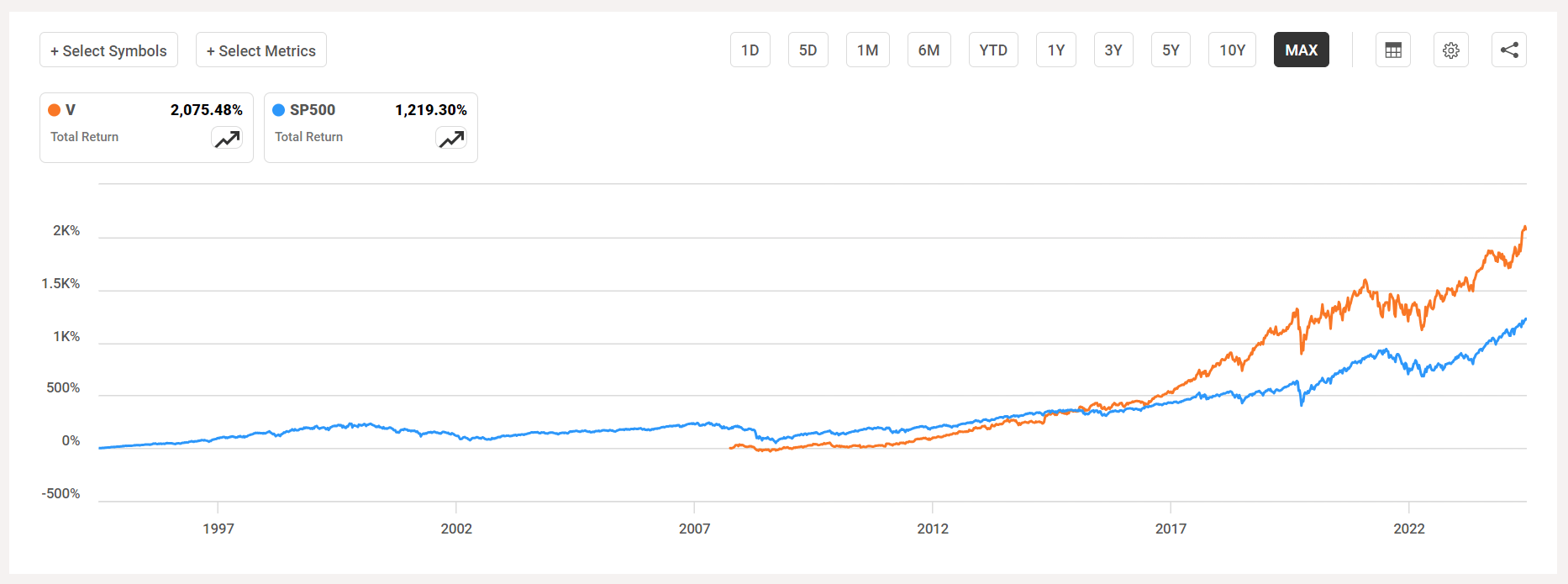

In 2008, Visa became a publicly traded company through what was then the largest IPO in U.S. history, raising $17.9 billion. This transition allowed Visa to operate independently and for the coop banks to monetize their stakes while insulating them somewhat from scrutiny. I believe that the network achieved such size and scale that it made sense to restructure the entity, allowing it to stand on its own to drive more value for stakeholders but also to shield the cooperative banks from regulatory risk. Since its IPO, Visa has significantly outperformed the S&P 500, achieving a > 1800% price return and solidifying its position as a key provider of global financial infrastructure. In fact, if an investor had stayed out of the market from 1994 until the 2008 IPO and allocated 100% of their portfolio to Visa, they would have still outperformed the 30 years total return of the S&P 500.

Visa has outperformed the S&P 500 over 30 years, despite only trading since 2008 (Seeking Alpha)

Financial Analysis

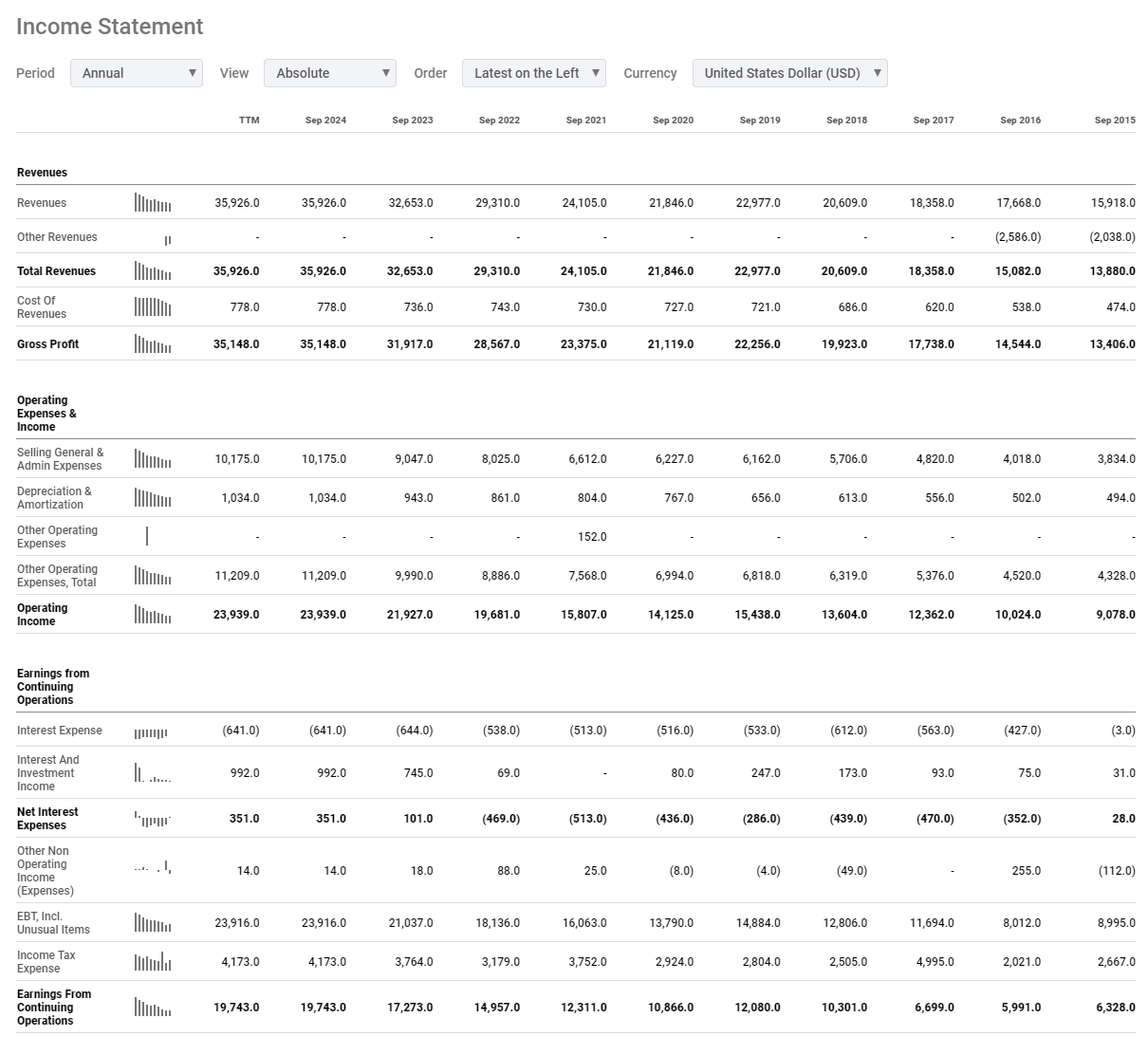

A quick scan of the income statement highlights the efficiency of the business model, and frankly is just a great-looking income statement. Over the past decade, Visa’s revenue has nearly tripled, growing from $16 billion in 2015 to $36 billion in the TTM. The best takeaway here is that while revenues have almost tripled, cost of revenues have less than doubled, implying stronger gross margins over the timeframe. This is direct evidence of the scalable business model in action.

Visa has seen consistent and strong growth over the last 10 years, with profits accelerating faster than revenues (Seeking Alpha)

Operating income has followed a similarly robust trajectory, increasing from $9 billion to $24 billion over the same period. Net income growth has been growing quicker than gross profits, rising from $6.3 billion to nearly $20 billion. The main observation here for me is more of what has been said already, that the company need not pour so much into SG&A to drive business growth, and that it is riding the long-term secular growth wave that it is in pole position to benefit from.

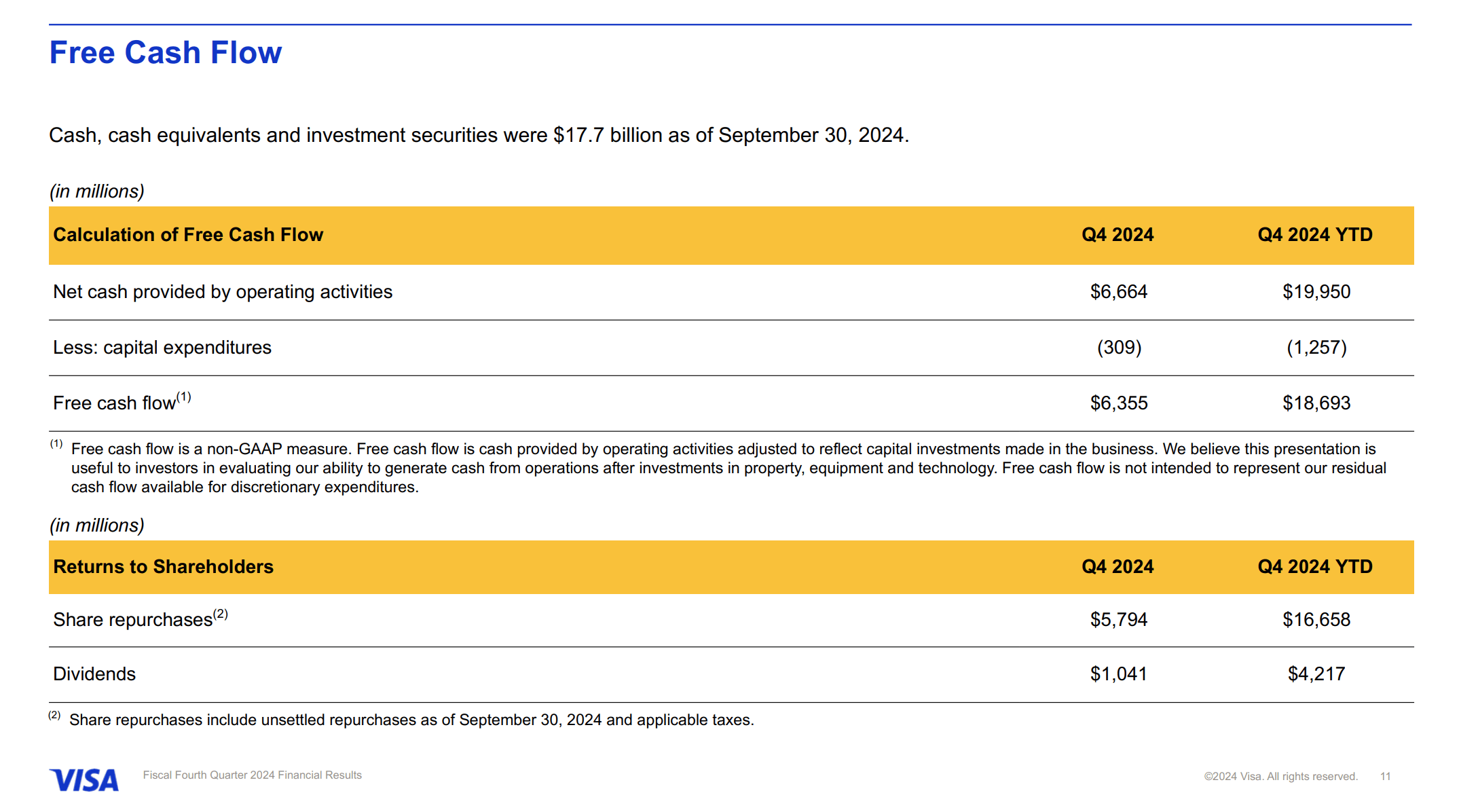

Prospective investors in Visa need to understand that the company returns basically all of its free cash flow to shareholders, and that the strong organic growth it sees is complemented by an aggressive share buyback strategy. In the most recent quarterly results, Visa repurchased $5.8 billion worth of shares and distributed $1.04 billion in dividends vs $6.355 billion of free cash flow. The company returning more than 100% of its free cash flow to shareholders signals a vote of confidence in the strong financial position and its confidence in the sustainability of its operations.

The company returned more than 100% of its FCF to shareholder in the recent quarter (Visa Q4 2024 earnings report)

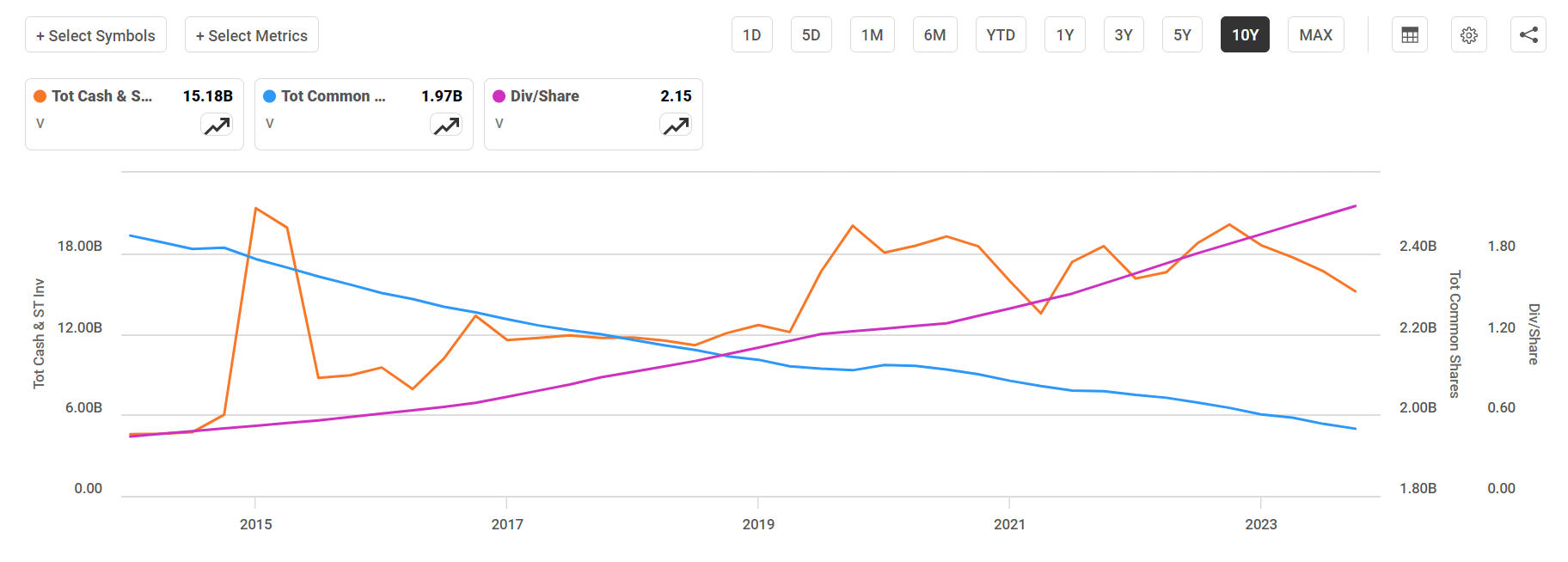

Over the past decade, Visa has retired approximately 25% of its outstanding shares. And boasts a shareholder yield of roughly 4%. I’ve read lots of well-written articles here that have highlighted the low payout ratio that Visa has, which I do find somewhat misleading despite being technically correct. The fact of the matter is that when buybacks are included, the payout ratio of this company is virtually 100%, sometimes exceeding 100% in a quarter. While this isn’t a bad thing for shareholders, it does bring up something to consider for investors: that it doesn’t appear to be very easy for the company to make acquisitions due to 1) high regulatory scrutiny and 2) low levels of EPS accretion from investments vs. just buying back their shares, even when overpriced. I’m sure many dividend investors would be cautious about purchasing a company with a 100% payout ratio, but don’t bat an eye when looking at this company, despite those buybacks being so accretive to EPS growth. Just food for thought. This aggressively buyback strategy does create enormous value for shareholders, but it is worth noting that the stock has benefited tremendously from financially engineered EPS growth, in addition to its strong organic growth profile.

The company has aggressively bought back shares, allowing it to post high-teens % dividend growth for several years while still growing its cash position (Seeking Alpha)

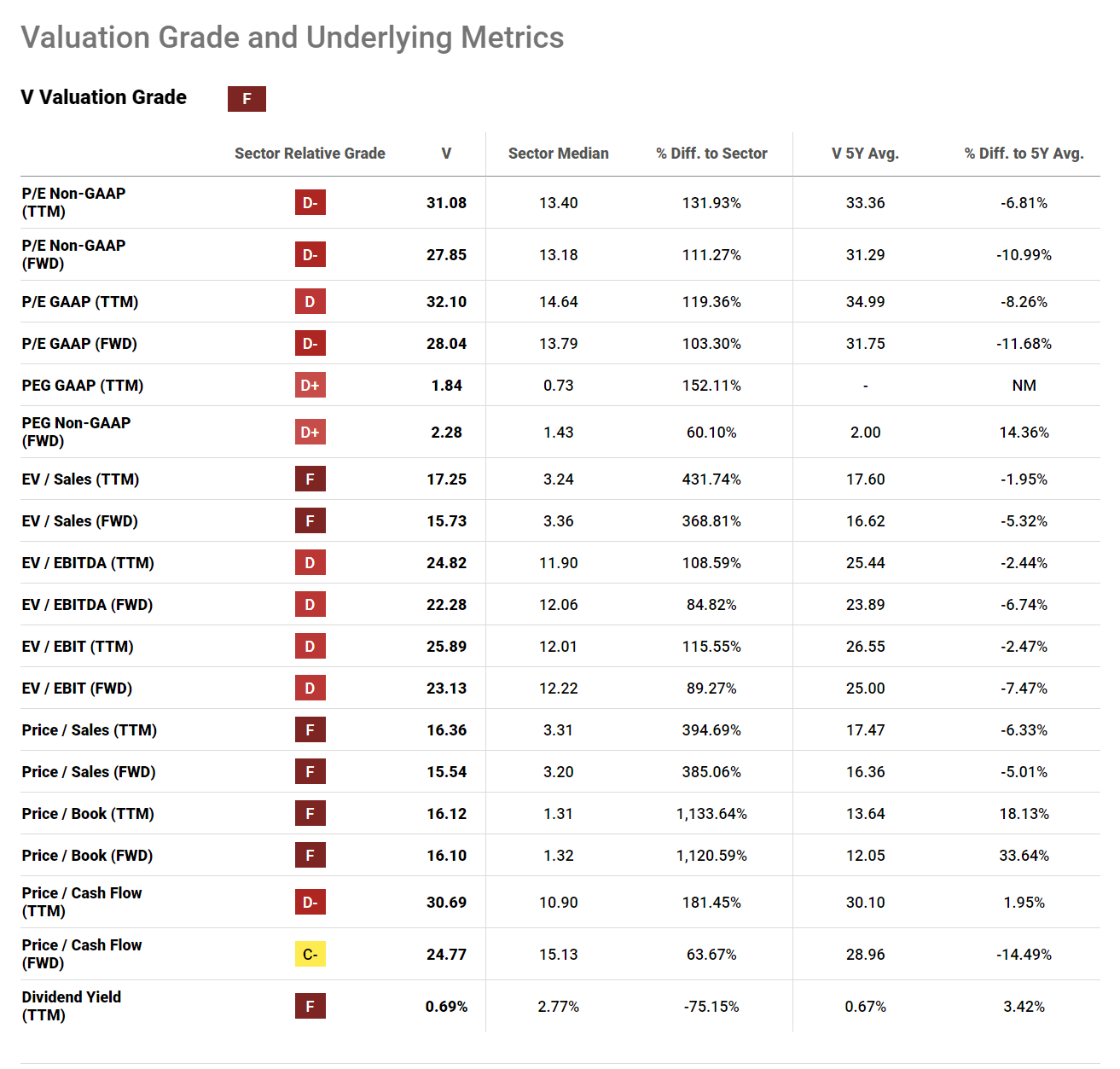

The Valuation is Not Cheap, But it Appears Fair

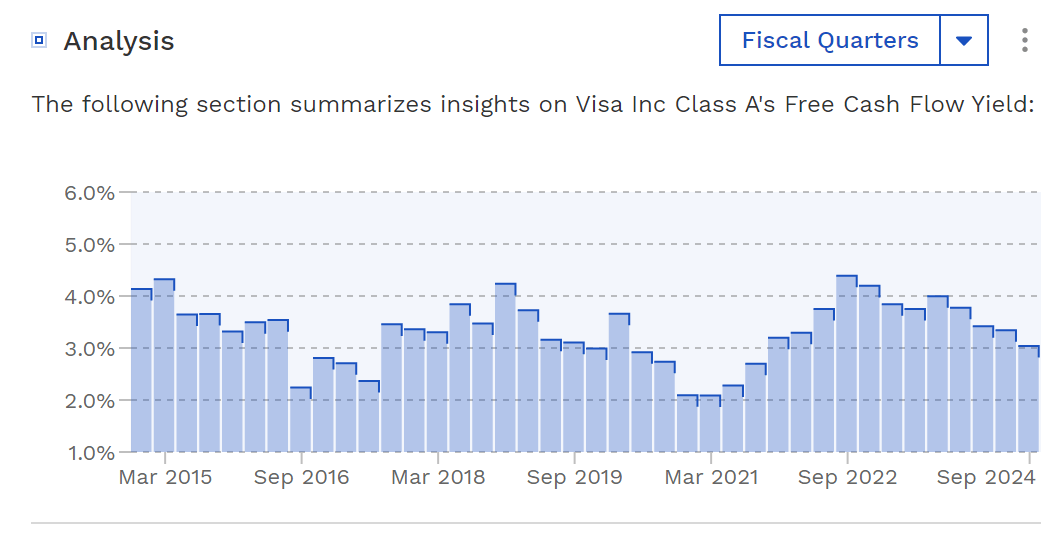

Visa’s valuation reflects the strength and stability of its business model but also indicates that investors pay a strong premium for this quality. The company currently trades at a PE ratio of around 30 and price/sales and price/book ratios of ~15 each, respectively. Visa’s asset-light model means its valuation is far disconnected from any tangible assets that it owns. It’s important for investors to recognize that an investment in Visa is not really backed by lots of cash, or assets like real estate, factories/machines, or other physical infrastructure. This isn’t really a value-style investment that allows investors to scoop up shares for a price lower than what the company has invested in. Furthermore, a business with growth rates like Visa that trades roughly 15x sales and book value is objectively expensive, if not egregiously so. However, I don’t think that these metrics are worth focusing on too heavily given the toll-booth nature of the business model. Since Visa is a FCF machine and returns all of it to shareholders in most quarters, the Free Cash Flow Yield is the best metric for judging Visa’s valuation, in my opinion. Analysis of the FCF yield vs. the last 10 years shows that the current yield is at a fair level, indicating a fair price.

Visa’s price/sales and price/book seem absurd for a company of its size, but make sense when considering the asset-light nature of the business (Seeking Alpha) Visa’s free cash flow yield looks fair compared to the prior 10 years (finbox.com)

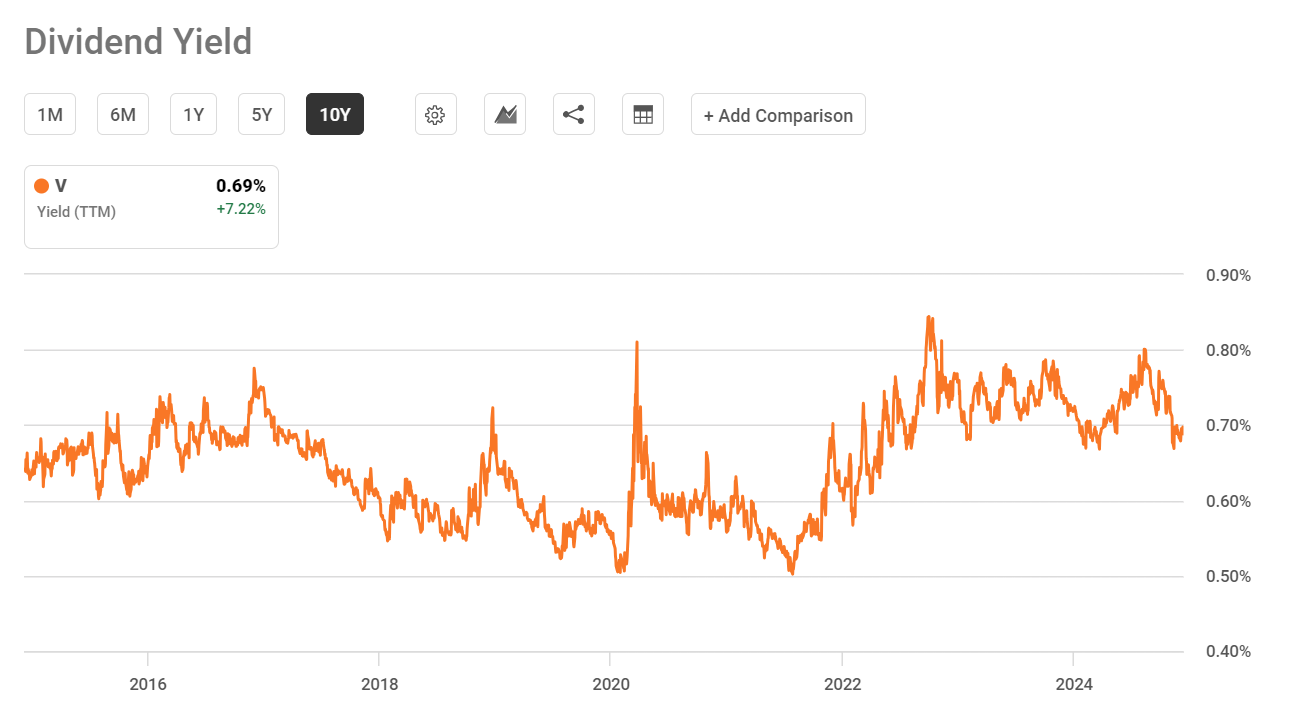

Dividend Metrics

Visa’s dividend metrics are another attractive feature for long-term investors. The company’s forward dividend yield is currently 0.76%, which, while modest, is on the higher end of the last ten years. Over the last decade, Visa’s dividend has grown at an impressive compound annual growth rate of 17%, with recent increases in the low double digits. If purchased at the IPO, Visa’s yield on cost would now be approximately 14% after 16 years, which is pretty good. It is easy to see why this stock has broad appeal to investors who prioritize dividend growth. While I do expect dividend growth to moderate over time, I find no reason to believe that it won’t be above average for many years to come.

The dividend yield looks fair compared to the last 10 years of data (Seeking Alpha)

Risks

The company is frequently scrutinized by regulators and currently faces antitrust action from the U.S. Department of Justice. In September 2024, the DOJ filed a lawsuit alleging that Visa unlawfully maintains a monopoly in the debit card market, potentially leading to increased regulatory oversight and financial penalties. In the past, this type of action has resulted in the company paying a large fine, but hasn’t really been a threat to its economic moat. As long as the moat is not threatened, any regulatory action is just noise to me.

In regions such as China and India, alternative payment networks have been developed to compete with Visa and limit its market share. Prominent examples include China’s UnionPay and India’s RuPay, with RuPay gaining significant traction due to government support and initiatives promoting domestic payment systems. While these networks do mitigate some of the market share growth story for Visa, they don’t pose much risk to interfering with volume and transaction growth in current markets.

The strong margin profile of the business is definitely a strength but does imply risk as well. Visa’s strong gross margins could theoretically be threatened if competitors undercut these margins. However, given the high barriers to entry and Visa’s tiny per-transaction fees, this risk appears minimal at present.

There have been many innovations in payment processing over the years, but Visa and Mastercard (MA) have found ways to integrate into them. For example, Apple Pay does not remove the card networks as intermediaries, it simply removes the need for a physical card to be swiped. Furthermore, the Apple Pay ecosystem uses both Mastercard for the Apple Card and Visa for Apple Cash.

While regulatory actions have caused volatility in the price as of late, I don’t really believe that regulatory risks threaten the moat of Visa. Rather, they stand to siphon off some of the cash it generates in the form of large fines over time. Luckily, the company sets aside money to deal with these issues.

Sentiment has Seemed to Weigh on the Stock

Another thing to address is that the company has underperformed the S&P 500 over the last 5 years. It’s tough to say exactly why, of course, but I think the rise of cryptocurrency has weighed on Visa’s stock performance unjustifiably. While cryptocurrency is often touted as an alternative payment network, its use case as a currency is limited in my opinion. I don’t believe that cryptocurrency networks have much appeal as mediums of exchange. Bitcoin and Ethereum’s low inflation rates vs. the M2 money supply do imply that they have more appeal as stores of value than as currencies, and until capital gains treatment of cryptocurrency is changed, this will especially be the case. Visa’s economic moat remains intact, but the growing competition in payment systems will likely require ongoing innovation and investment.

Speaking of sentiment, I also believe that the “vibescession” we have been in for a few years has weighed on the stock given its exposure to macroeconomic downside. Many investors have been fearful of a market drawdown or recession for the last few years despite robust economic indicators, which does lend credence to the thesis that the stock might actually have underperformed unjustly.

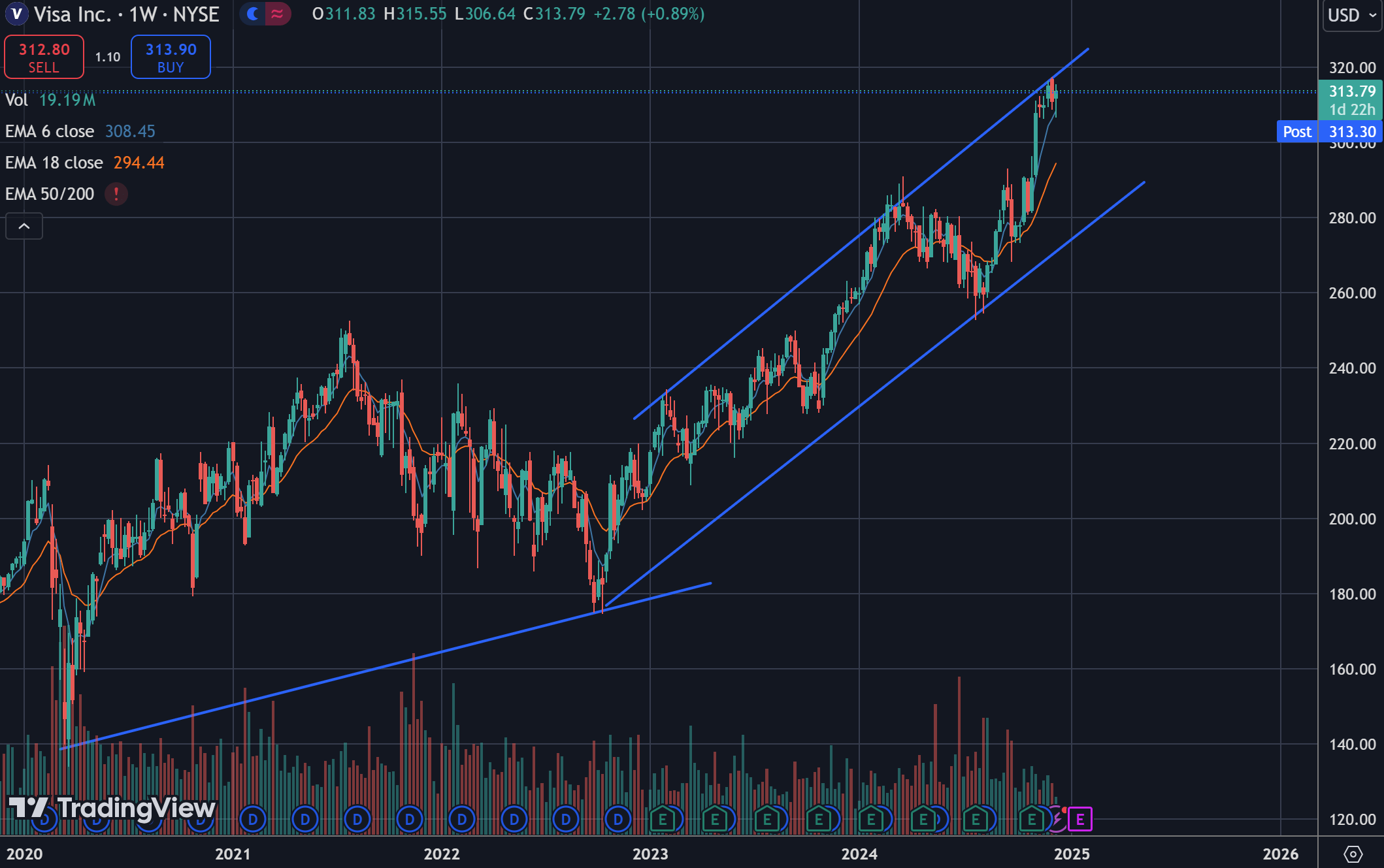

Technical Analysis

Visa’s stock has exhibited a clear uptrend since late 2022, moving largely in line with the broader market. The most notable takeaway from the chart is that the stock is basically at all-time highs but hasn’t really broken out above its long-term uptrend with strong volume, indicating that a short-term pullback might be in the cards soon. While I don’t believe that current levels represent a strong entry point, long-term investors could find value in adding to their positions during pullbacks or periods of consolidation. Every time I have bought shares of Visa, I haven’t been too concerned with the current price action, as I believe it will perform well for years into the future.

Technically speaking, it does appear that the price might move lower in the very immediate term. However, the stock is in a clear uptrend (TradingView)

Grade: Buy

Visa earns a buy rating for its strong business model, consistent growth, and dominant market position. While the valuation is high, it reflects its ability to generate strong shareholder returns. However, based on a currently average valuation and technical analysis that doesn’t look very bullish one way or the other, it is not a strong buy at current levels. Investors might want to consider accumulating shares gradually, especially during pullbacks, to build exposure to this high-quality business.

I believe Visa is worth consideration as a core holding for investors seeking consistent performance, growth, and exposure to the continued transition to cashless payments. Also, it does a good job at insulating financial performance from inflation. It is a stock that has historically rewarded patience and aligns well with a long-term, diversified portfolio strategy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of V, MA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.