Summary:

- Walmart and Target are both strong dividend payers in the retail sector, but their investment appeal differs considerably in today’s market.

- Walmart’s high valuation reflects its safe-haven status but limits near-term upside potential.

- Target’s lower valuation and higher dividend yield appeal to value-oriented investors, though its reliance on discretionary categories adds volatility.

- Walmart offers consistency for conservative investors, while Target’s current share price is attractive for those with a higher risk tolerance.

John Rensten/DigitalVision via Getty Images

Investors value Walmart (NYSE:WMT) and Target (NYSE:TGT), the first and third-largest companies in the Merchandise and Retail industry, for their size and relative stability. However, with high valuations and an uncertain consumer environment, it’s worth considering whether either stock offers much upside potential at current levels.

This analysis examines their business models and growth prospects to assess which might be the preferred investment opportunity—or if both warrant a cautious approach at this time. I conclude that Walmart is a Hold at current valuations, while Target is a Buy for potential long-term investors seeking a combination of income and growth who have tolerance for volatility.

Walmart vs. Target: Business Models

Walmart’s revenue is anchored in its extensive scale and its dominance in essential categories like groceries, attracting a broad base of budget-conscious consumers. Operating over 10,000 stores globally, the company has built a reputation as a low-cost retailer for decades, with its core revenue coming from in-store retail sales of essential goods. Walmart e-commerce platforms, including Walmart Marketplace and Walmart+, now contribute an increasingly meaningful portion of revenue. At around 8.7% collectively, e-commerce represents a fast-growing area for the company, though in-store retail still accounts for the vast majority of revenue. This essential-goods focus allows Walmart to perform reliably in various economic environments.

Target’s business model is more concentrated, with a U.S.-only presence and a product mix tailored toward middle- and upper-middle-income consumers. Key differentiators include private-label lines like Good & Gather in grocery and Cat & Jack in children’s apparel, as well as exclusive partnerships, such as Hearth & Hand with Magnolia. These offerings help Target cultivate brand loyalty by providing higher-quality, unique items that may appeal to shoppers seeking distinctive or trend-forward products. However, unlike Walmart, Target’s revenue mix is weighted more toward discretionary categories, such as apparel and home goods, making its performance more sensitive to economic conditions.

Growth Prospects and Strategic Focus

Walmart’s growth strategy is heavily focused on expanding its digital footprint, which has become a significant driver of growth. Investments in automation, such as robotics in fulfillment centers and AI-driven inventory management, aim to reduce costs and reinforce its logistical advantages. At the same time, third-party sales on Walmart Marketplace and its Walmart+ subscription service are helping to diversify its revenue base. With e-commerce now approaching 10% of the company’s total revenue, these digital sales represent a significant growth area and driver of potential long-term share appreciation.

Target’s growth strategy includes an integrated omnichannel approach with same-day fulfillment options like curbside pickup, similar to Walmart’s. Digital integration remains a central focus for Target, but it faces intense competition from both Walmart and Amazon in this area. The company’s emphasis on exclusive brands and private-label products helps foster customer loyalty and reinforces its unique position in the retail market. However, Target’s reliance on discretionary categories and U.S.-only market presence could constrain growth if economic conditions weaken, potentially leaving it more vulnerable than its larger, more diversified peer.

Walmart vs. Target: Performance

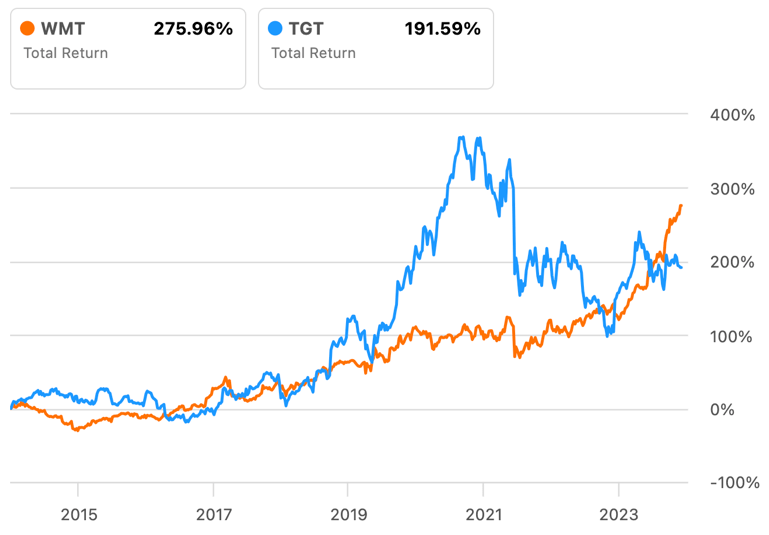

The thrust of this analysis is well-captured in the chart below, which compares the ten-year total return for Walmart and Target:

Total Return: 2014-2024 (Seeking Alpha)

Walmart’s annualized return of around 27.5% has come mostly through steady, consistent gains with some steepening over the past year. Target’s returns have been more volatile, with its share price climbing from around $94 during the COVID lows to over $260 just sixteen months later. The impact of the pandemic on Walmart’s stock performance is almost unnoticeable. The two-year period from November 2021–November 2023 was exceptionally challenging for Target, reflecting its struggles with inflation, inventory management, and shifts in consumer spending away from home goods to experiential activities. But a key takeaway is that up to May 2024, the two companies had essentially identical total returns over the preceding decade. Walmart has pulled ahead over the past six months as Target’s share price continues along a more volatile path.

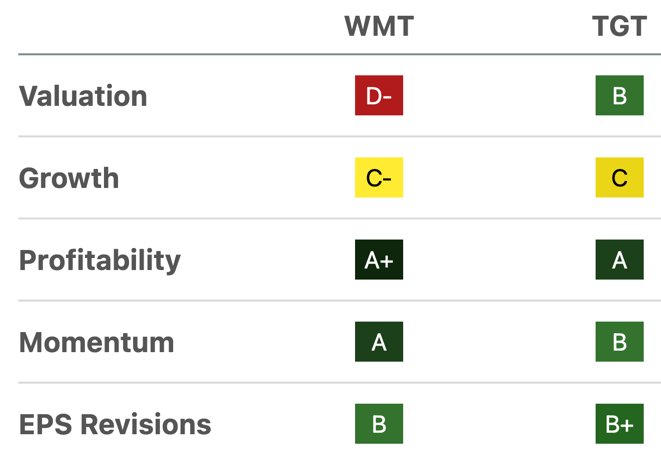

That said, Seeking Alpha’s Quant system currently has Target as a Strong Buy and Walmart as a Hold, with Target holding the edge in three of the five factors—most notably, in valuation:

Seeking Alpha

Walmart vs. Target: Valuation

Walmart’s valuation, trading at a P/E of around 33x, reflects market optimism about its stability and growing e-commerce potential. While the digital expansions support this premium valuation, it may limit near-term upside for new investors, as much of Walmart’s growth potential may already be priced in. On a price-to-free cash flow basis, Walmart’s valuation exceeds 50x, with substantial capital expenditures directed toward digital and logistics initiatives. These investments position Walmart for long-term competitiveness but limit free cash flow available to shareholders in the near term. Although Walmart is expanding into higher-margin segments like advertising, healthcare, and third-party sales, these areas are still a relatively small part of total revenue, meaning its safe-haven status might come with limited shorter-term growth potential.

|

WMT |

TGT |

|

|

P/E TTM |

44.2 |

15.4 |

|

P/S TTM |

1.12 |

0.79 |

|

EV/EBITDA TTM |

18.2 |

9.2 |

|

P/Cash Flow |

20.1 |

8.1 |

Target’s valuation is more appealing on a relative basis, trading at a forward P/E of ca. 15x. This lower multiple is attractive, but as noted, its reliance on discretionary sales introduces volatility. If the economy contracts, demand for non-essential items could weaken, potentially offsetting the valuation advantage. Recent insider selling, including by Target’s CEO, has raised questions about management’s confidence in the company’s near-term performance.

Walmart vs. Target: Shareholder Returns

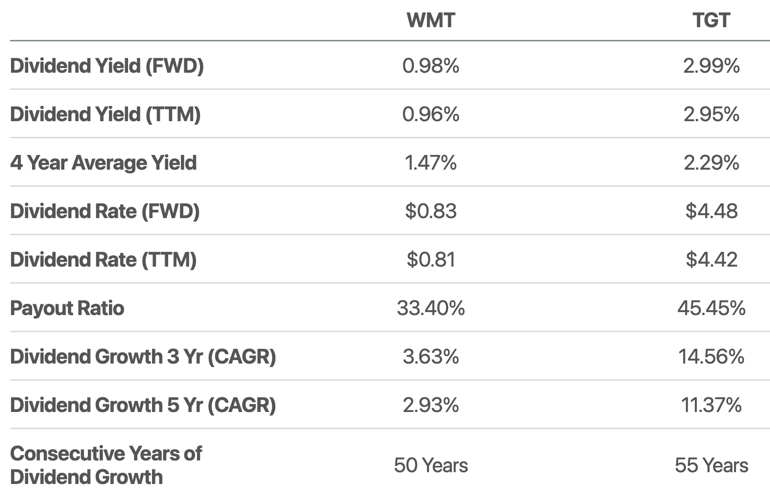

Walmart’s forward dividend yield of around 1% puts it in the category of a stable, low-risk investment rather than a strong income generator. Given the company’s substantial capital expenditure in digital transformation and logistics, free cash flow has been constrained, potentially capping dividend increases in the near term. Although Walmart’s dividend has grown without pause for over a half century, the low yield combined with a high valuation reduces its appeal for some investors.

Seeking Alpha

Target’s forward dividend yield of around 3% is a more attractive option for income-seeking investors. The company has maintained a moderate payout ratio—higher than Walmart’s but still allowing plenty of room for future increases, assuming earnings remain stable. But again, if economic conditions worsen and consumer spending on non-essential items declines, dividend growth would likely be constrained. Like Walmart, Target has capital demands for inventory and pricing adjustments, but its focus on discretionary categories may amplify the impact on its ability to maintain consistent dividend growth in challenging economic conditions.

Final Verdict: Stability vs. Value

Walmart’s expansive business model and market positioning provide stability in uncertain times, yet its high valuation may constrain near-term upside. As a safe-haven investment, Walmart does offer consistency, but new investors may find limited appeal in a stock that is already trading at historically high multiples. The company’s advancements in e-commerce, logistics, and digital expansion support long-term growth for investors with a multi-year outlook.

Target’s lower valuation and higher dividend yield make it a more appealing option for value-oriented and income-focused investors, particularly those comfortable owning more economically sensitive companies. However, Target’s exposure to discretionary categories and recent insider selling may give some investors pause; the stock may be more suitable for those with a higher tolerance for volatility.

In sum, Walmart’s stability makes it a sensible choice for conservative investors, though initiating a new position at the current price is unappealing. Target’s valuation and yield provide greater potential rewards for those willing to ride out a more challenging near-term environment, and the current share price may present a reasonable entry point to begin dollar-cost averaging.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.