Summary:

- Lucid Group, Inc. Air Sapphire Edition offers impressive performance but is priced at $250,000, while Tesla’s Model S Plaid offers similar performance at around half the price.

- Lucid has struggled with low production and delivery figures, resulting in significant financial losses.

- Lucid faces challenges in a competitive market, with Tesla’s ability to lower prices and capture market share posing a threat.

- Despite the Saudi Arabian PIF’s backing, it’s best to stay clear of Lucid shares.

Khosrork

Disclosure: While I was bullish on Lucid Group, Inc. (NASDAQ:LCID) in the past, holding the stock is increasingly risky now. I like electric vehicle (“EV”) companies with significant potential, but Lucid’s position has weakened considerably over the last twelve months. Moreover, the challenging economic environment compounds the issues. Lucid company is burning through billions of dollars, with no end to the losses in sight. At some point, it’s best to face reality. I got caught up in the Lucid hype and kept hoping Lucid could get its house in order. That’s looking less likely every day.

Lucid makes quite a vehicle. The Lucid Air can go from zero to sixty in under two seconds, has an estimated range of more than 500 miles, and boasts a mid-numbing max power of more than 1,200 horsepower. Unfortunately, you’ll have to dish out around $250,000 for this kind of performance in a Lucid Air Sapphire Edition vehicle. A significant problem for Lucid is that Tesla, Inc.’s (TSLA) Model S Plaid offers similar performance, starting at less than half the Sapphire’s price tag, just $108,490.

Another significant issue for Lucid is that it produces and sells far fewer vehicles than expected. Furthermore, Lucid burns money hand over fist. The company posted a staggering $1.54 billion GAAP net loss for the first half of this year. Lucid produced just 4,487 in H1 2023, and Q2 showed a second sequential decline in production and delivery figures. Additionally, while production was nearly 4,500, Lucid delivered only 2,810 vehicles in the first half. This dynamic equates to a staggering $550,000 loss per delivered vehicle. Oy Vey.

Things are not going well for Lucid. It initially anticipated 20,000 units in 2022 but produced just 7,180 cars, delivering only 4,369 vehicles. Meanwhile, competing luxury automakers like Mercedes (OTCPK:MBGAF) and BMW (OTCPK:BMWYY) are selling more than 10,000 annual 100% electric vehicles. Moreover, Tesla delivered around 30,000 Model S/X vehicles in the first half of 2023.

Lucid has fallen far behind its much more experienced and profitable competitors and may not recover. We remain in a challenging economic environment. Interest rates are sky-high, making financing more difficult. Consumers hesitate to dish out $100-300K for an EV. Moreover, Tesla can lower price tags to increase demand, taking market share from struggling startups like Lucid. Lucid faces perpetual challenges and will likely continue burning cash, leading to more significant dilution and a much lower stock price in the coming years.

High Hopes – Dying For Lucid

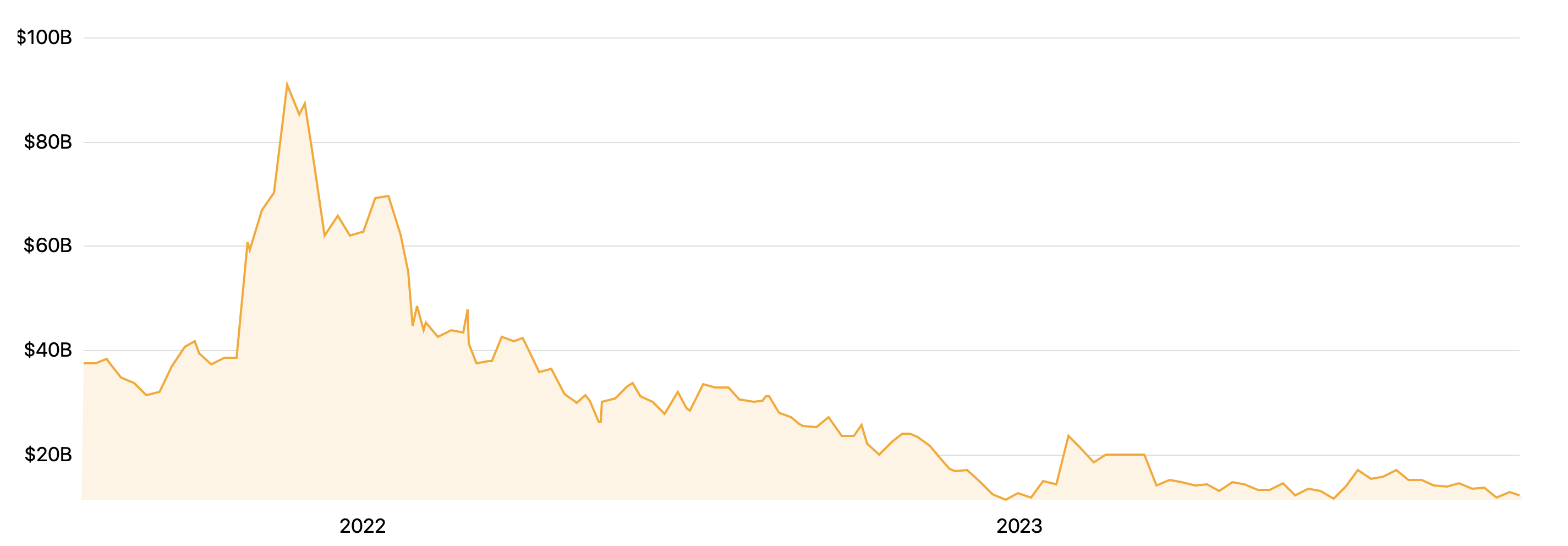

Lucid market cap (Companiesmarketcap.com)

Lucid’s market cap surged following its SPAC mega-merger in July 2021. It’s challenging to comprehend, but Lucid was valued at about $90 billion on pure hype alone. The company had a merger, $27 million in revenues in 2021, and had demonstrated no ability to mass-produce vehicles at all. Please don’t laugh. I bought into the hype, owning Lucid shares on and off in recent years. However, things have become more apparent with the economic slowdown, the Saudi connection, and the recent dilution. Lucid may remain a niche automaker, but it’s not the next Tesla, and it’s not a stock that I want to own.

Lucid’s Short Interest Tells A Story

Roughly 24% of Lucid’s float is sold short. In total, Lucid has about 2.3 billion shares outstanding, approximately a $12 billion market cap, and about 10% of its market cap, $1.2 billion is sold short. This dynamic illustrates that a substantial amount of “smart money” is continuing to bet against the struggling EV maker.

So, who owns Lucid? Well, most of the company, about 60.5%, is owned by Saudi Arabia’s “Public Investment Fund” (“PIF”). Look, let’s not beat around the bush here. While the PIF is one of the most significant sovereign wealth funds globally, it is controlled by the Saudi royal family. Thus, one man controls the PIF, Crown Prince Mohammed bin Salman. Saudi Arabia is an authoritarian state and one of the most significant global oil exporters. It’s doubtful that the kingdom is interested in EVs taking over the world. Thus, Lucid may remain a niche automaker.

Lucid is addicted to cash-burn. Lucid was favored to succeed in 2021 partly due to its solid $6.2 billion cash position. Within one year, Lucid managed to burn through much of this cash, requiring a raise of $1.5 billion, diluting existing shareholders by 8.4%. The PIF led this capital raise, and there is a high probability of more dilution rounds as Lucid continues burning through cash.

Poor Demand And Production Concerns

Poor demand suggests that Lucid could remain a small, niche EV maker. In mid-2022, Lucid said it had 37,000 reservations for its vehicles. In the November 2022 quarter, instead of increasing reservations, they fell to 34,000. More recently, Lucid’s reservations fell to just 28,000 cars. There is a significant problem here. Instead of rising demand, we see declining demand for the new automaker as its brand fails to catch on.

Also, demand is just one of many issues as production needs to work on getting off the ground. Lucid completed its Arizona factory construction in 2020, intending to ramp up annual production to 400,000 cars. Nonetheless, in 2022, Lucid had a production target of 20,000 vehicles but managed to build just 7,180 cars. In 2023, Wall St. analysts expected the production of 27,000 vehicles. However, Lucid shocked analysts with a 10,000-14,000 production estimate, later stating that it expected “over 10,000” car output in 2023.

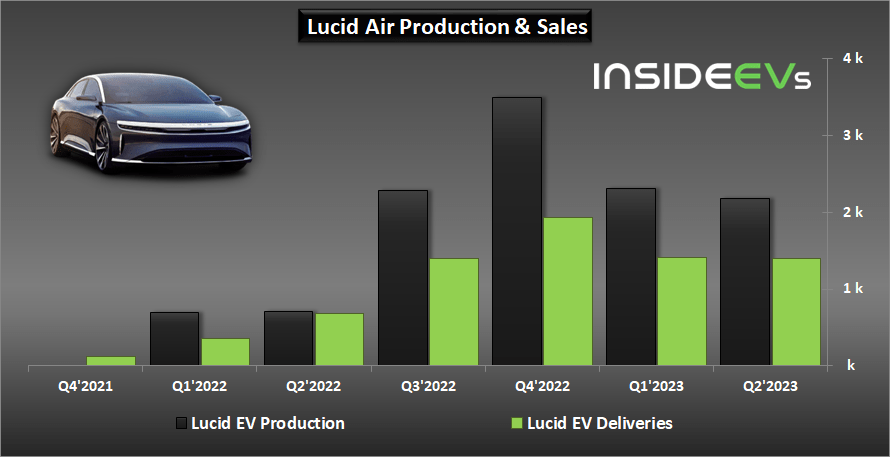

Production Vs. Deliveries Divergence

Production/deliveries (InsideEVs.com )

If things were “okay” at Lucid, the company would at least be selling close to its production capacity. Unfortunately, Lucid is producing far more cars than it can sell. Lucid produced 4,487 vehicles in H1 2023 but sold only 2,810 cars. That’s a sales-to-production ratio of only 62%. Where are the other 38% of Lucid cars going? Are they sitting in a warehouse somewhere waiting to be sold? What happened to the 37,000, 34,000, 28,000 reservations?

This dynamic is profoundly troubling and implies softer-than-anticipated demand, supply chain problems, and other issues. Have you considered buying a Lucid vehicle? Me neither, because I have yet to determine where I would go to service mine. Lucid has a van that can service your vehicle. Is this a cost-effective solution for the company?

Lucid Is No Tesla

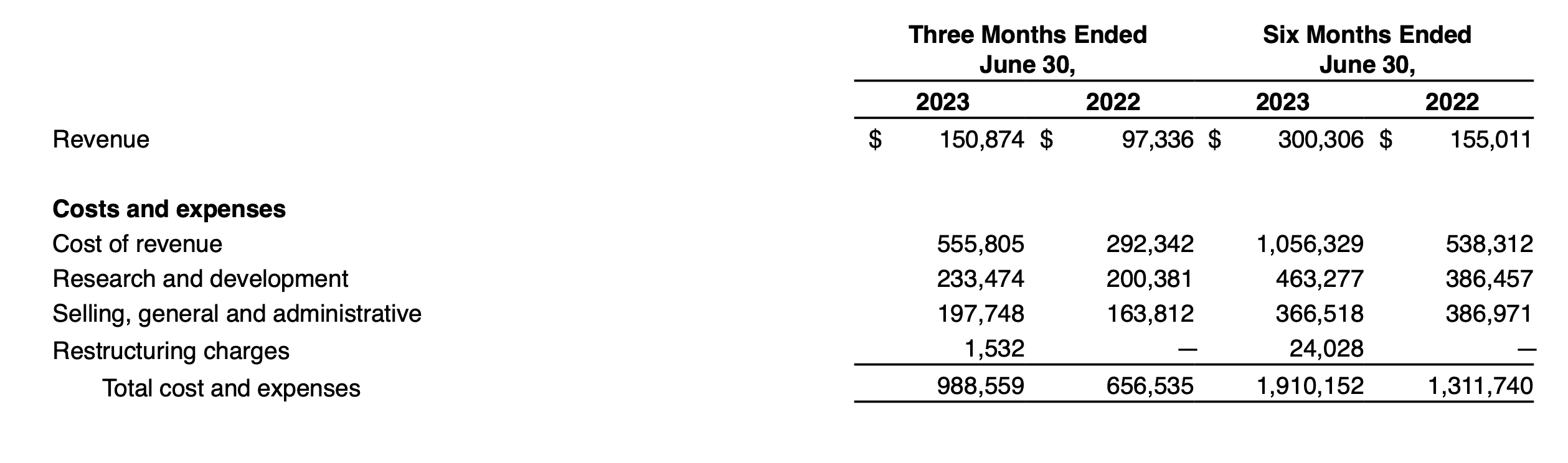

Statement of operations (ir.lucidmotors.com)

I owned Tesla’s stock, and I have covered Tesla for many years. Even in the darkest days of the Model 3 ramp-up, Tesla’s gross margin was around 14%. Last quarter, Lucid’s gross margin was about -270%. Its total cost and expenses were nearly a billion dollars last quarter while only providing around $151 million in revenues. Lucid’s losses are monumental and ludicrous, and a valid question arises. How long can this last?

In the first half of 2023, total costs and expenses hit nearly two billion dollars on only $300 million in revenue, equating to an operating loss of around $1.6 billion for H1. At this pace, Lucid will burn through its remaining cash position relatively quickly and may require another capital raise before the end of the year.

The Bottom Line

In Lucid’s case, building an excellent vehicle is much easier than mass-producing it efficiently. Moreover, there are demand, supply chain, and other issues. We remain in a tight monetary environment, and the economic slowdown process may take longer to pass. Tesla produces excellent EVs, selling them cheaper than Lucid, offering servicing, supercharging, and other infrastructure that Lucid cannot compete with. Moreover, Tesla has pricing power, enabling it to capture market share from Lucid by lowering prices in challenging times.

Meanwhile, holes continue materializing in Lucid’s story, and the company remains in an exceptionally cheapening place. Lucid is losing money hand over fist, delivering a staggering net loss of more than $1.5 billion in the first half of this year. Worse, the company has a meager 2,810 car deliveries to show for its enormous loss. Lucid is losing a staggering $550K per car sold, burning through cash at light speed.

I’m avoiding Lucid Group, Inc. stock, as another capital raise is approaching. Regardless of PIF backing, Lucid must improve operations soon, or bankruptcy could hit the struggling start-up in the coming years.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Are You Getting The Returns You Want?

- Invest alongside the Financial Prophet’s All-Weather Portfolio (2022 17% return), and achieve optimal results in any market.

- The Daily Prophet Report provides crucial information before the opening bell rings each morning.

- Implement my Covered Call Dividend Plan and earn 50% on some of your investments.

All-Weather Portfolio vs. The S&P 500

Don’t Wait! Unlock Your Financial Prophet!

Take advantage of the 2-week free trial and receive this limited-time 20% discount with your subscription. Sign up now and start beating the market for less than $1 a day!