Summary:

- Micron Technology, Inc. stock has performed well despite its cyclical nature and unpredictable short-term earnings.

- Investors should focus on a 2-5 year time frame and ignore short-term earnings predictions.

- The current decline in Micron’s stock price could potentially take several more years to recover from, especially if a recession occurs.

Eoneren

Introduction

There are three words professional sell-side stock analysts almost never say. Those words are “I don’t know.” The inability to utter or write those words stems from the fact that analysts are hired with the express purpose of pretending like they know, or, at least that it’s possible to know what the earnings of a business and the stock price will be 12 months or less into the future. It’s really the message that “it’s possible to know” that is being transmitted to individual investors which can be especially dangerous for their returns. An investor who finds a way to perpetually remain humble with regard to their predictions and expectations is usually the investor who wins over the long term, not the one who makes bold assertions about the short-term price of a stock.

This was the theme behind my last Micron Technology, Inc. (NASDAQ:MU) article back in June, titled “Micron Stock: Q3 Earnings Should Be Ignored By Investors.” In that article, I shared my relatively long history of writing about and investing in Micron stock and how I had managed to be one of the few analysts/investors who have performed well with it over the past 5 years. Today’s article will be shorter and more to the point, but I strongly suggest reading the June article if you would like more details about my process because they are all covered in detail there.

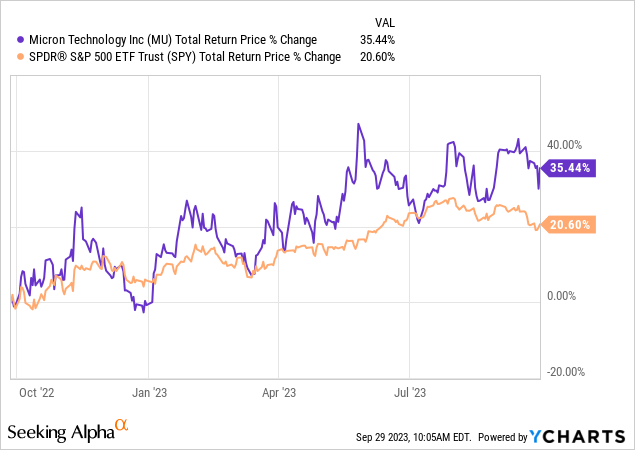

After performing well with Micron stock from late 2018 through the end of 2019, I purchased Micron again last year and wrote about it in my article “6 Lessons For Micron, AMD, And Nvidia Investors” on 9/27/22. Since that time, here is how Micron has performed.

Even after the recent post-earnings price decline, Micron is still handily outperforming the S&P 500 (SPY) and has produced good absolute returns as well. I am currently still holding my position.

Basic Understanding of Micron’s Cyclicality

These are the core principles I think investors need to understand about Micron’s business and Micron’s stock price.

- Micron’s earnings are deeply cyclical.

- Even though EPS is cyclical, it also has secular growth.

- Because earnings are deeply cyclical they are unpredictable over the short term.

- Because Micron has secular growth, EPS is somewhat predictable over the medium term.

- Put these facts together and investors should focus on a 2-5 year time frame and ignore short-term earnings and stock price predictions.

- Because the time frame for a recovery in earnings might be long, investors need to buy when the stock price is well off its highs and be prepared to wait a few years for a recovery.

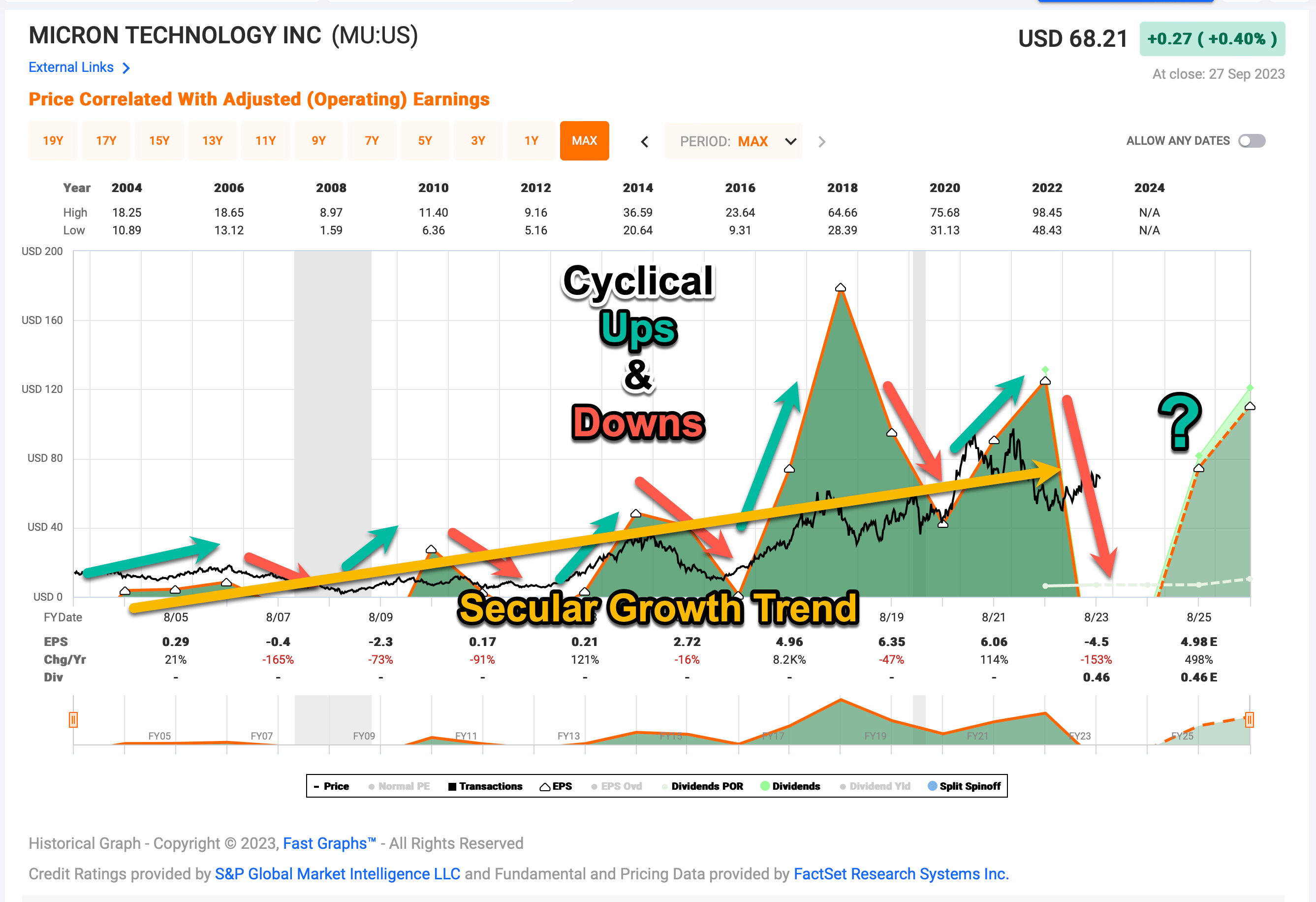

FAST Graphs

In the chart above, I have attempted to highlight the historical pattern I shared in the bullet points. We can clearly see the deep earnings cyclicality as well as the longer secular uptrend over time. The current downcycle is particularly bad because of the COVID boom in electronics goods which is now in its “Bust” phase. What is not factored in, yet, is a potential U.S. recession. If that occurs (and I think it probably will), then Micron’s very quick 1 to 2-year recoveries we’ve gotten used to over the past decade might take 3 to 5 years instead. Here is how they have played out in the past.

| ~Year | ~Time Until Bottom | ~Duration | ~Depth |

| 1984 | 1 year | 9 years | -89% |

| 1986* | 6 months | 18 months | -79% |

| 1988 | 6 months | 1 year | -42% |

| 1989 | 18 months | 4 years | -71% |

| 1995 | 1 year | 4.5 years | -80% |

| 2000 | 2.5 years | 18 years+ | -92% |

| 2004* | 1 year | 2 years | -47% |

| 2006 | 1.5 years | 7 years | -90% |

| 2014 | 1 year | 3 years | -73% |

| 2018 | 6 months | 2 years | -53% |

| 2022 | ? | 1.75 years+ | -50%? |

We are almost 2 years into the current decline from the peak stock price. If the U.S. avoids a recession, it’s possible the worst is over, especially if the longer-term secular growth catches up sooner rather than later. This is why I went ahead and took a position in Micron stock last year around this time when the stock was -50% off its highs. There was always a chance the worst historical outcome would be avoided, and I could still get pretty good returns even if it took several years for the stock price to recover its old highs.

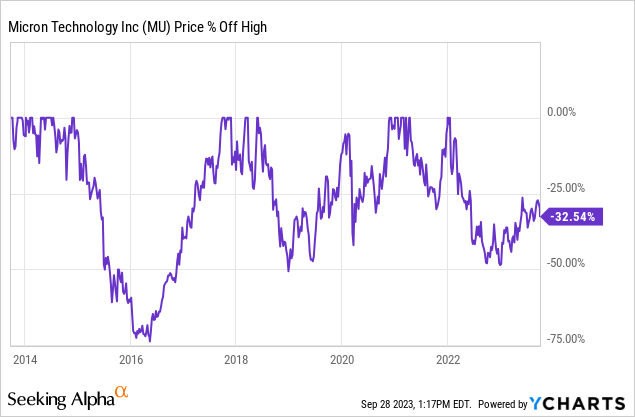

But if we still have a recession to go through, then we probably need to use the 2006 downcycle as a guide for the future and expect it could take up to 5 more years to recover. Additionally, in the recession scenario, the stock price might fall as far as -65% to -75% off its highs, which is significantly deeper than where it trades today. I would likely add to my current position if it does so. Here is where the stock price stands off its highs now.

This drawdown chart only goes back 10 years, so this is not ancient history. Micron has had a nice bounce off the bottom so far, but I would not be a buyer with new money at today’s price because there is much farther this stock could drop. I generally try to avoid buying stocks if there is a reasonable chance the price could fall -50% or more after I buy it. So, even though there is about a +50% upside from here if Micron goes on to recover its old highs, if it takes 5 years to do so, that will only produce an +8.45% CAGR. This is about average in terms of the long-term stock market returns, so Micron is likely fairly valued at today’s price, but I aim for better-than-average returns, so I prefer to buy stocks when they are cheaper than average with a margin of safety.

Everyone loves to write about Micron because both the earnings and the stock price fluctuate a lot and are very unpredictable over the short term, so this creates a lot of space for disagreement and debate over the near-term future. It also creates an interesting situation where everyone who doesn’t buy at the top and sell at the bottom gets to be “right” if they just hold on to their opinion long enough. The difficulty is being the investor that is mostly right before a big downcycle and takes profits, and then also being mostly right somewhere near the bottom of the downcycle, buys, and then hangs on long enough for a recovery.

Eventually, both earnings and the stock price will recover. Inventory will be worked through, and the market will need more memory. What we have to accept is there is a wide range in terms of the timing of when that recovery might happen and basically nobody knows what the timing will be, not even the people running Micron. But, it’s safe to say from this point in time the earnings recovery will probably be 1 to 5 years from now, and at that point, Micron stock will recover its old earnings peak and the stock price will rise accordingly. Knowing this, all investors really need to think about is whether they can commit to that 5-year holding period, and what sort of return is acceptable to them. I aim for high returns, so I usually don’t buy a deep cyclical stock like Micron unless I can get a 100% return in 5 years or less. Usually, it takes less time, but it might not this time with the triple whammy of stimulus bust, U.S./China trade tensions, and the possibility of a recession.

Conclusion

I remain long on Micron Technology, Inc. stock as I wait for a full recovery, but for new money, I wouldn’t buy Micron unless it was under $50 per share because the risk of a deeper drawdown remains. For investors who are already long Micron as I am, we can pretty much ignore the stock for at least another year unless it loses another -50% from here, at which point we should consider doubling our position. I maintain that it’s mostly useless trying to predict earnings quarter by quarter when nobody really knows what is going to happen over the short term.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of MU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

If you have found my strategies interesting, useful, or profitable, consider supporting my continued research by joining the Cyclical Investor’s Club. It’s only $30/month, and it’s where I share my latest research and exclusive small-and-midcap ideas. Two-week trials are free.