Summary:

- Tilray stock has fallen 37.9% in 2023, despite being up 8.9% in 2023 in early September.

- The company’s Q1 results were reported in October, along with the filing of the 10-Q.

- Tilray is still overvalued compared to its peers, despite the significant decline in its stock price.

Torsten Asmus/iStock via Getty Images

I warned that Tilray Brands (NASDAQ:TLRY) was potentially very overpriced in mid-September, and the stock has fallen substantially since then. The stock was up 8.9% year-to-date at the time I warned, and it is now down 37.9% in 2023. In this follow-up, I discuss its Q1, which was reported in October, review the outlook in the analyst estimates, assess the charts and look at the valuation.

Tilray’s Q1

On October 4th, the company issued news about its Q1 ending in August and filed the 10-Q. Analysts, according to Sentieo, had been expecting revenue of $174 million and adjusted EBITDA of $11 million. The company reported revenue of $176.9 million, up 15%. Adjusted EBITDA was $11.4 million, down 16% from a year earlier. The operating loss was $34.4 million, which was larger than a year ago. The company used $15.8 million to fund its operations.

Looking at the revenue by segment, net cannabis revenue grew 20% to $70.3 million, which was 40% of overall revenue. The gross margin of 28.2% fell from 50.7%. Medical cannabis in Canada fell 6% to $6.1 million. International cannabis expanded 37% to $14.3 million. Wholesale sales exploded over 12X to $5.3 million. The largest part of cannabis for the company, net adult-use sales, fell 3% to $44.6 million. This decline was related to the acquisition of HEXO.

Looking at the three components of the majority of the revenue, pharmaceutical distribution sales grew 14% to $69.2 million, which was 39% of overall revenue. Wellness revenue (hemp food) fell slightly to $13.3 million, 8% of overall revenue. Beverage alcohol revenue grew 17% to $24.2 million, which was 14% of overall sales.

The balance sheet improved during Q1. Net debt fell from $131 million to $88 million. Tangible equity increased from $333 million to $402 million. During the quarter, the company issued 66.6 million shares, mainly related to the HEXO acquisition.

The balance sheet changed after the end of the quarter. The company spent $85 million of its cash, $20 million of which was borrowed, to write a check to Anheuser-Busch (BUD) in exchange for a portfolio of craft beer and beverage brands. This acquisition may weigh on tangible book value. It also repurchased $20 million of its convertible debt by issuing 7 million shares and then the rest of that issue by paying $107 million in cash in early October.

The Outlook Shows Lower Margins

The analysts were expecting FY24 revenue ahead of the Q1 report to be $729 million and FY25 revenue to be $800 million. Now, they expect FY24 revenue to grow 30% to $816 million and FY25 to grow 13% to $924 million. These higher numbers reflect the recent acquisitions. The analysts were expecting adjusted EBITDA to be $70 million in FY24 and then $94 million in FY25. Now, they forecast $69 million for FY24 and $105 million in FY25. At the consensus, the adjusted EBITDA margin for FY24 is now 8.4%, down from an estimated 9.6% before and also down from the 9.8% experienced in FY23. EPS are projected to be negative in both FY24 (-$0.23) and in FY25 (-$0.13).

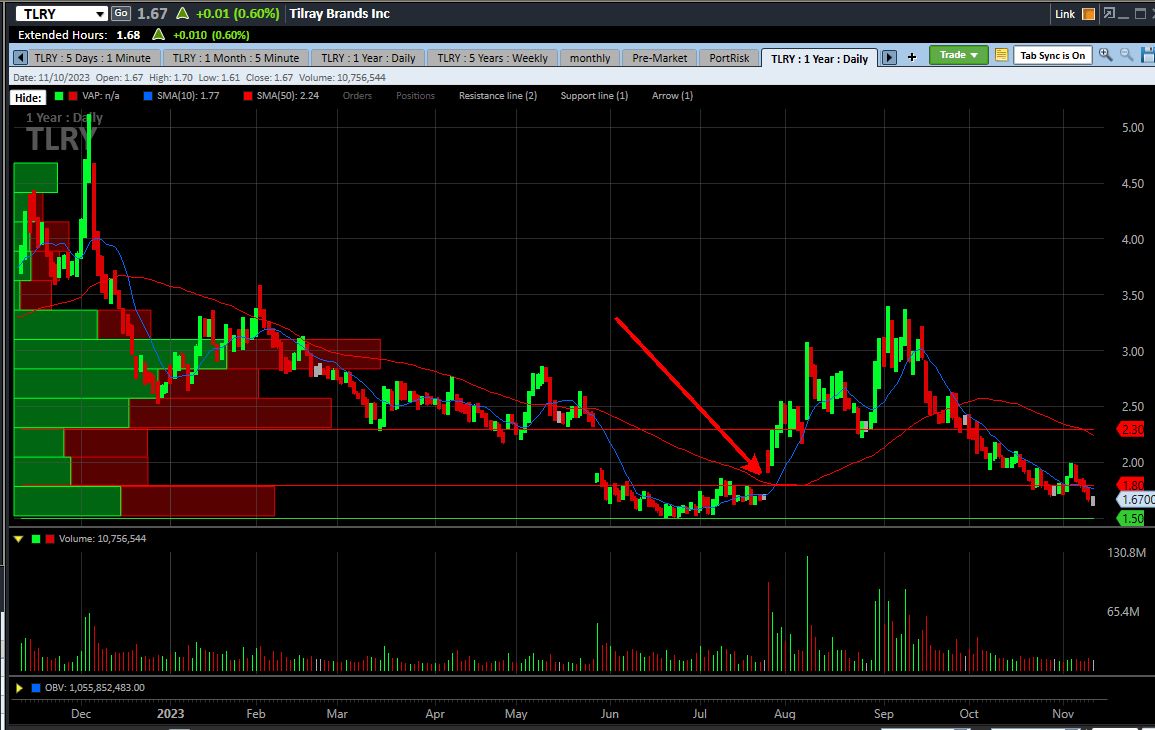

The Chart

Over the past year, Tilray traded briefly above $5, but it is close now to the all-time low set during the summer at $1.50 and filled the gap left behind in July:

Charles Schwab

The stock has support about 10% lower at the all-time low of $1.50, and I see potential resistance at $1.80 and $2.30. If $1.50 breaks, investors will fear potential delisting ahead, as NASDAQ requires the stocks to trade above $1.00. Of course, the company could address this by doing a reverse-split, but this move has pressured many cannabis stocks.

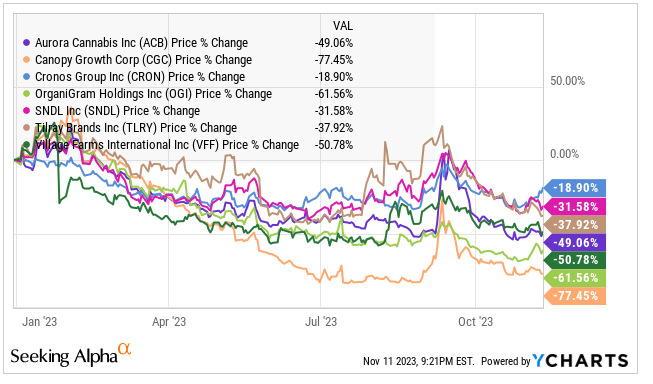

Comparing the move in 2023, Tilray has fallen less than most peers:

YCharts

The Valuation

In that article in September, I had a price target below where TLRY was trading at the time. My projection of $0.94 was based on an enterprise value to projected adjusted EBITDA for FY25 of 10X. This price was also 1.5X tangible book value, a premium to where some debt-free companies like Cronos Group (CRON) and Organigram (OGI) are trading currently.

Updating the target for the higher estimated adjusted EBITDA and the better net debt now yields a target at the same ratio of enterprise value at 10X the projected adjusted EBITDA would yield $1.28. This would boost the price to tangible book value to 2.4X, which is excessively high compared to peers and to many ancillary companies.

I said two months ago that the 10X multiple may be too aggressive, and I continue to believe that is the case. I am lowering the multiple to 8X, which yields a price target for TLRY of $1.00. This would be 1.9X TBV, still very high relative to peers.

Conclusion

While Tilray has declined significantly, it is still overvalued relative to peers. Investors can find other Canadian LPs that have better balance sheets that trade with lower valuations, and they can also find ancillary names that look more attractive.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

420 Investor launched in 2013, just ahead of Colorado legalizing for adult-use. We have moved the service to Seeking Alpha. Historically, we have provided great coverage of the sector with model portfolios, videos and written material to help investors learn about cannabis stocks, and we are excited to be doing it here!