Summary:

- NIO’s stock has lost over 50% of its value in the last three months, with deteriorating fundamentals and market share.

- NIO’s Q4 earnings missed EPS estimates, and its revenue growth lags significantly behind the overall Chinese EV market.

- NIO continues to burn cash and is expected to raise new funds, leading to increasing leverage and share count.

Andy Feng

Investment thesis

I made a big mistake last time when I upgraded my rating for NIO’s (NYSE:NIO) stock to bullish as the stock lost more than 50% of its value within the last three months. Last time I overestimated the strength of NIO’s Q4 deliveries data, which did not convert into financial success. In reality, the company’s fundamentals keep deteriorating as its market share is melting down. The company continues to burn cash, which means that the leverage and share count are poised to grow further. NIO appears to be significantly undervalued from the perspective of discounted cash flows, but considering the “rich” history of disappointing investors, even a significant upside potential does not outweigh the risks to me. Moreover, I have doubts about NIO’s business model sustainability. All in all, I downgrade NIO to “Strong Sell” again.

Recent developments

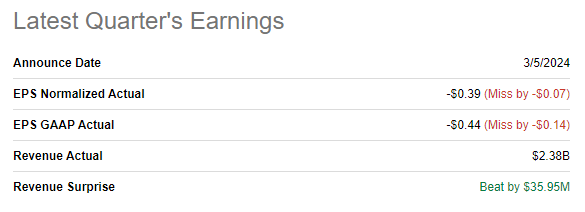

NIO released its latest quarterly earnings on March 5, when the company topped revenue consensus estimates, but the EPS surprise was negative. Revenue was almost flat in Q4 2023, and the adjusted EPS improved from -$0.52 to -$0.44. It was the tenth quarter in a row when NIO missed EPS estimates.

Seeking Alpha

For the full FY 2023, NIO delivered a 9.7% revenue growth. NIO’s revenue growth in 2023 looks ridiculous compared to the overall Chinese EV market, which expanded by 38% in 2023. NIO bulls might say that looking at the accounting revenue might not be fair enough, and it is better to look at physical volumes delivered. However, from this perspective NIO also lagged behind the countrywide EV market growth with a 30% increase in deliveries in 2023. Lagging behind the market is a significant warning sign to me, which means that NIO is losing its market share to competitors. For example, Li Auto (LI) expanded its deliveries by 182% in 2023. Even Tesla (TSLA) with its massive footprint and production volumes in China, demonstrated a 33% deliveries growth in Chinese market. NIO’s competitor in the luxury segment, Mercedes-Benz (OTCPK:MBGAF) has almost doubled its Chinese EV deliveries in 2023. Another German luxury automaker, BMW (OTCPK:BMWYY) demonstrated a 138% increase in EV deliveries in China. That said, NIO is rapidly losing its market share to competitors.

However, the start of 2024 was even more sour for NIO. In Q1 2024 NIO delivered 30,053 vehicles, about a thousand less than it did in Q1 2023. To add context, Li Auto delivered more than 80 thousand vehicles, demonstrating a 53% YoY growth. Even XPeng (XPEV), a company which I also consider fundamentally weak, demonstrated a 20% YoY deliveries growth in Q1 2024. Overall, the Chinese EV market grew by 14.7% YoY in Q1 2024. That said, NIO continues losing its market share at a notable pace.

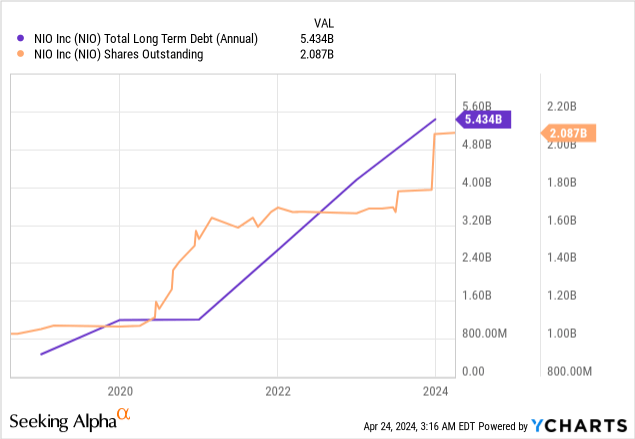

As the company continues burning cash, it has no options other than to raise new funds. That is the reason why the company’s total debt and the share count has skyrocketed in the last two years. Since consensus estimates do not expect the EPS to turn positive until 2027 it is highly likely that the warning trend of increasing leverage and share count to continue over the next several quarters.

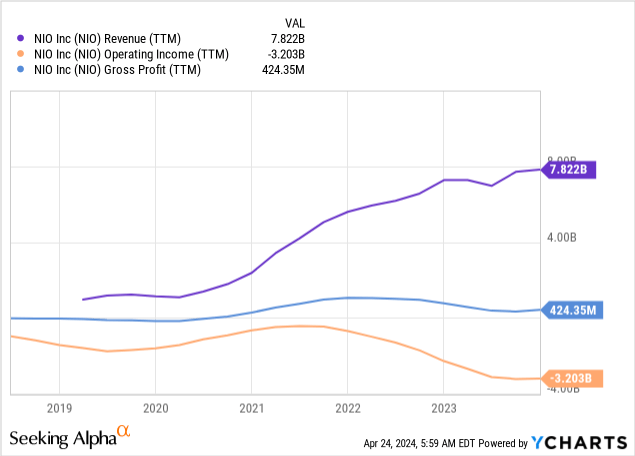

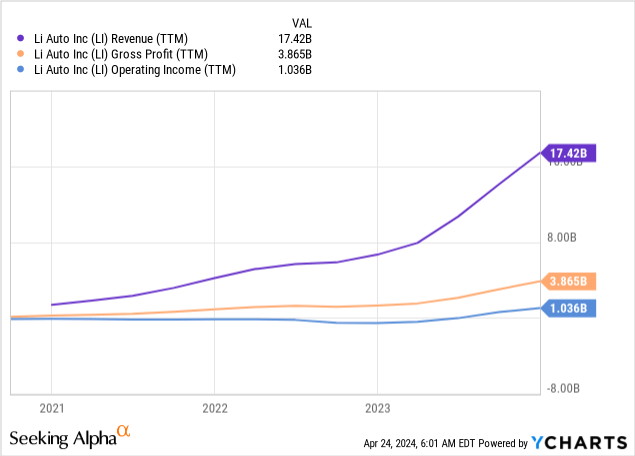

What is most crucial, I have doubts about the sustainability of NIO’s business model. As shown above, revenue demonstrated impressive growth since 2020, but the gross profit has been stagnating and the operating income even declined sharply. In a healthy and sound business model, profitability should follow the revenue growth. Otherwise, there is no point in driving revenue growth, especially considering that NIO still generates operating losses. Below you can see that the more revenue Li Auto generates, the more gross profit and operating income it generates. While the correlation is not perfect and profits lag behind revenue growth, all three metrics are moving in the same direction, indicating that Li’s business model is working.

Current industry trends also do not look favorable for NIO, as evidenced by Tesla’s Q1 earnings. The most technologically advanced [in my opinion] EV company in the world, with a strong track record of ramping up, delivered a mere 3.5% YoY revenue growth in Q1. Tesla also missed consensus revenue estimates by more than half a billion dollars. When an EV giant like Tesla struggles to drive revenue growth and misses consensus estimates, weaker players like NIO are highly likely to face even more severe challenges.

Overall, I see a myriad of reasons to be bearish about NIO. The company is still struggling to demonstrate the operating leverage, NIO’s market share is melting down, and the balance sheet is poised to suffer for many quarters ahead. Last but certainly not least, I have doubts about the sustainability of NIO’s business model. The more vehicles it sells, the further its operating loss expands, suggesting that under the current model, additional topline growth may lead to further deterioration in shareholder value.

Valuation update

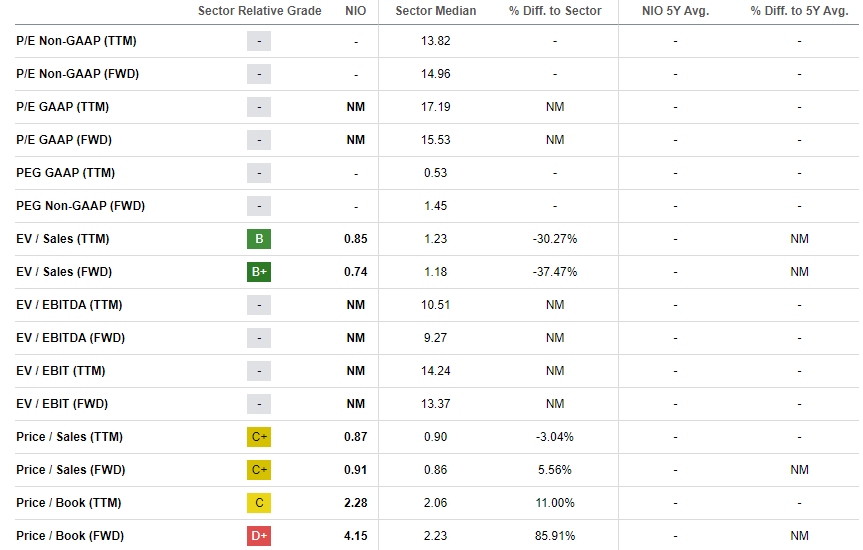

NIO declined by 51% over the last twelve months and its YTD dynamic has been almost the same with a 55% decline since January 1, 2024. NIO’s valuation ratios now look moderate with price-to-sales ratios moving below one. Since NIO is still deeply unprofitable, most of the ratios are not applicable.

Seeking Alpha

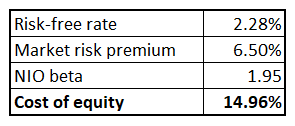

Now let me proceed with the discounted cash flow [DCF] simulation. I consider a 15% WACC to be fair considering political and geopolitical risks inherent to all Chinese stocks together with company-specific several fundamental weaknesses, which I have highlighted in the section above. My WACC assumption is also backed by the CAPM approach. NIO’s market beta is 1.95, according to Yahoo Finance. China’s 10-year governmental bonds yield is currently at 2.28%, which I use as a risk-free rate. A 6.5% equity risk premium for Chinese stocks is my personal judgment, which is approximately in line with the levels recommended by Aswath Damodaran [5.63% equity risk premium + 1.03% country risk premium]. The CAPM formula gives me 14.96%, but I round it up to 15%.

Author’s calculations

Due to the fierce competition, which is poised to intensify further, I expect NIO to underperform compared to the overall Chinese EV market and project a 10% revenue growth. Consensus EPS estimates project the bottom line to become positive not earlier than FY 2027. Therefore, I project that NIO will deliver a 1% FCF margin in FY 2027 and will proceed further with a one percentage point yearly expansion, which correlates with the revenue growth projection.

Author’s calculations

According to my DCF valuation, the stock is around 41% undervalued. However, I consider such a deep discount to be fair given all the fundamental weaknesses the company demonstrates. A 41% upside potential is insufficient to me because all the risks I have highlighted in “Recent developments” suggest that there are risks that NIO might potentially be out of business within the next couple of years, if the company does not find its path toward profitability. Should this occur, investors could potentially lose up to 100% of their investment in NIO, which does not appear to offer a fair risk-to-reward relationship.

Risks to my bearish thesis

NIO is still backed by an investment vehicle controlled by the government of oil-rich Abu Dhabi. The company received another $2.2 billion in late 2023, which indicates firm confidence of NIO’s major investor in the business’s prospects. With such a support from a wealthy investor, NIO might eventually come up with a new jaw-dropping technology or a new best-selling model. Even if NIO continues stagnating, every new piece of information regarding a new tranche from the Abu Dhabi fund might lead to share price spikes.

NIO’s stock does not exist in vacuum and its movements also depend on the sentiment around the whole EV industry, or even the health of biggest names like Tesla and BYD (OTCPK:BYDDF). The company’s fundamentals might not improve, but a potential rally in Tesla’s stock might be beneficial for the NIO’s share price. The same with other news which do not directly improve NIO’s fundamentals, like the accelerated growth in the Chinese economy or improved geopolitical situation between China and the U.S., which will highly likely lead to a rally in all most popular Chinese stocks.

The largest EV maker in the world, BYD, is not currently presented in the luxury segment. I believe there is a possibility that BYD might wish to expand its reach to high-end consumers, potentially making NIO a target for acquisition. Should this happen, NIO’s shares might be bought out by BYD at a premium. Even if this potential deal never materializes, the stock could surge on rumors of such a possibility, which would work against my thesis.

Bottom line

To conclude, NIO is a “Strong Sell”. The Chinese EV market is steadily maturing, and growth rates are poised to cool down. At the same time, the competition is intensifying, and NIO does not look like a powerful enough player to compete in this red ocean. The attractive valuation should not mislead potential investors as the company’s strategic positioning is weak, and its business model appears to be unsustainable.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.