Summary:

- Lumen Technologies’ debt restructuring deal closes, providing the company with a five-year runway to turn around operations.

- The company’s first quarter financial results show a decline in revenue and adjusted EBITDA, but 2024 guidance offers optimism for future growth.

- LUMN has improved liquidity and is working towards reinventing itself, but investors should be cautious of the risks involved.

DKosig

Last week, Lumen Technologies (NYSE:LUMN) announced its first quarter earnings. The telecom company is attempting a turnaround by transforming its business. I’ve been holding the company’s 2039 maturing bonds, which are currently trading at 31 cents on the dollar and yielding 26% to maturity, along with a small equity position. After covering fourth quarter earnings and reviewing the company’s first quarter earnings report, I believe the company is making progress in what will be a critical year.

FINRA

The Lumen Debt Restructuring Deal Closes

In late March, Lumen closed on a debt restructuring deal with some of its creditors. The deal moved a significant debt wall coming due in 2027 to 2029 and 2030. As a result, the company has a five-year runway to turn around operations. Over the next three years, the amount of debt due is under $1 billion before it begins to ramp higher towards 2029. Because the deal closed in late March, it’s too early to see how the changes have affected earnings.

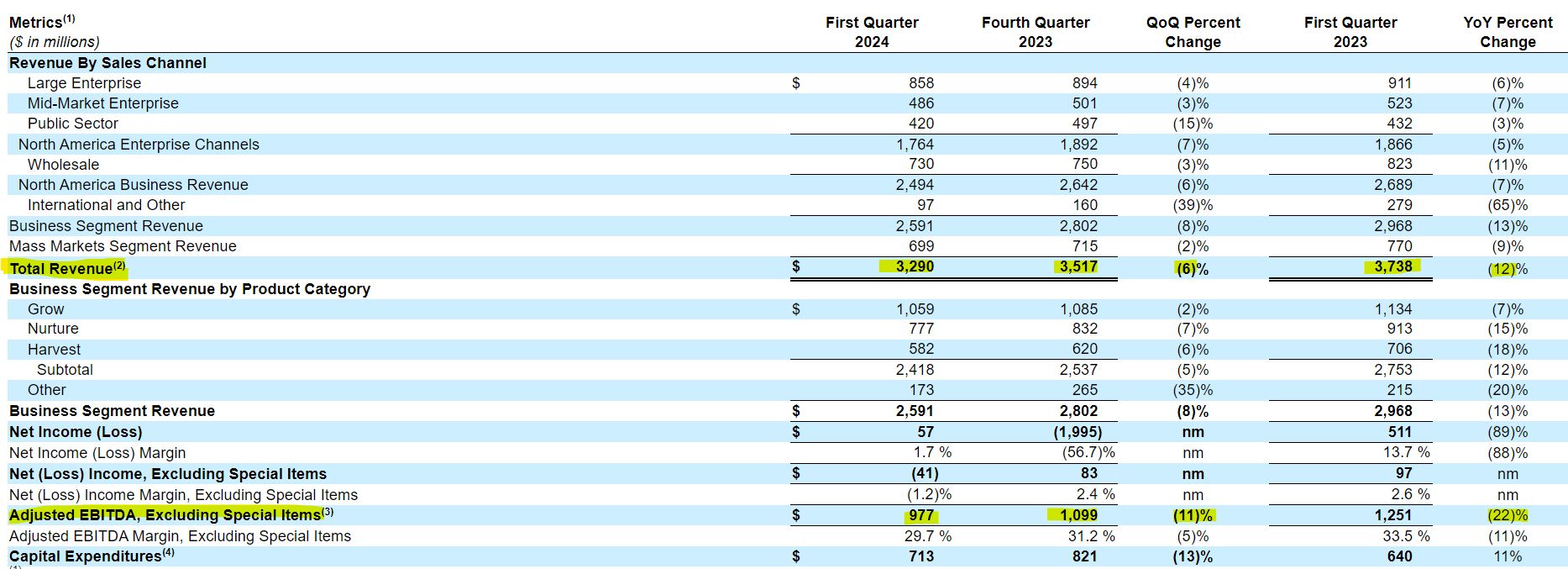

Earnings Presentation SEC 10-Q

Lumen’s First Quarter Financial Results

Lumen Technologies’ operating results show that the company is continuing to shrink. Revenue declined across each of the company’s segments, with overall revenue down 6% from the fourth quarter and 12% from the first quarter of 2023. Management explained in the earnings call that some of this decline had to do with anxiety surrounding the debt deal. Adjusted EBITDA saw a large decline to $977 million, which was 22% lower than a year ago. While the drop in revenue may be alarming to investors, it’s important to note that the company highlighted 2024 as a low point in revenue when it announced its turnaround plans last June.

Earnings Presentation Turnaround Presentation/Earnings Updates

Lumen Technologies’ balance sheet shed light on the company’s capital structure after the debt deal was reached. The company currently has $1.6 billion in cash. Lumen also paid down its long-term debt by $1.2 billion in the first quarter. Equity investors have reason to be optimistic as shareholder equity increased by nearly $100 million to over $500 million.

SEC 10-Q

Lumen Technologies’ cash flow statement shines some light as to why the company was able to pay down some long-term debt in the first quarter. Lumen increased operating cash flow to $1.1 billion and free cash flow to nearly $400 million in the first quarter. Unfortunately, the cash flow jump was due to a one-off tax refund of $700 million, which is included in net changes in current assets and liabilities. The cash infusion, combined with cash on hand, allowed Lumen to pay down its debt.

SEC 10-Q

Lumen Technologies’ Liquidity and Its importance

While the debt restructuring plan has been heavily debated, the company has benefitted from expanded access to cash should it be needed. When combining cash and borrowing capacity on its revolving line of credit, Lumen had more than $2.3 billion in liquidity at the end of the first quarter. Should Lumen’s turnaround plans go better than expected, the company can use some of this liquidity to accelerate its capital investment plan.

SEC 10-Q

Lumen’s 2024 Guidance Offers Some Optimism

While revenue and earnings continue to decline, Lumen did reiterate its 2024 financial guidance, which showed adjusted EBITDA accelerating and finishing above $4 billion, along with free cash flow of $100 to $300 million. The midpoint of 2024’s free cash flow guidance is $100 million higher than the guidance released from the initial turnaround plan. These numbers give me hope that investors may start to see growth in the next couple of quarters.

Earnings Presentation Turnaround Plan/Earnings Updates

Risks

Due to the high-yield nature of Lumen Technologies’ debt, and its highly leveraged balance sheet, there are obvious risks. The success of this investment is dependent upon a turnaround plan that has yet to see any growth. Now that the company’s creditors have a secured position, I’m unsure how long they will be patient if the overall trends remain down into 2025. Investors need to be mindful of these uncertainties and cautiously examine future quarters earnings, free cash flow, and continue to monitor guidance updates from management.

Conclusion

Lumen Technologies continues to be an interesting story of a legacy telecom company working to reinvent itself. Revenues and EBITDA continue to slide, but management warned us that we would not see a sustained turnaround until next year. The debt wall has been delayed to 2029, but the impact of a new debt structure won’t be seen until future quarters. I continue to hold onto a small position of Lumen shares as well as the 2039 notes in the hopes of capitalizing on this turnaround story.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of LUMN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I own Lumen debt maturing in 2039.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.