Summary:

- Canadian cannabis and beverage firm Tilray beat top and bottom street estimates for its fiscal Q4 period.

- The company has made strong progress on reducing its large debt pile.

- While progress is being made, shareholders are facing significant dilution over time.

Shutter2U

After the bell on Monday, we received fiscal fourth quarter results from Tilray (NASDAQ:TLRY). The Canadian cannabis and beverage firm was one of the leading bubble names back in 2018, but shares have lost almost all of their value since. Over the past couple of quarters, the company has worked to shore up its balance sheet a bit, but it has come at a major cost to shareholders. Monday’s report showed some solid improvements, but not enough yet to warrant a buy recommendation.

Previous struggles to get going:

Tilray’s run to $300 put shares at several hundred times their expected yearly revenue back in the day, and the stock has lost more than 99% since. I’ve long worried about the company racking up large losses and cash burn, along with its inability to meet longer-term revenue growth targets. With management using a lot of stock for acquisitions and debt repayments, along with multiple capital raises, the outstanding share count has risen steadily quarter after quarter.

When I last looked at the name in May, Tilray had announced an equity distribution agreement to raise up to $250 million. This was one of the items I needed to see before I could even consider an upgrade to a buy rating, as the balance sheet definitely needed to improve. Since that time, going into Monday’s report, shares had lost about 5.7%, while the S&P 500 had gained about 3.1%.

Fiscal Q4 results:

For the fiscal period ending in May, Tilray reported revenues of just under $230 million, representing about 25% year-over-year growth, and beating street estimates by more than $2.5 million. The growth leader again was the beverage-alcohol segment, up 137%, thanks to new product innovation and contributions from the acquired craft beverages. Cannabis revenue was up 12%, mostly thanks to two acquisitions, while wellness sales were up 6%, and distribution revenue was down by the high single digits. Once we lap the anniversary of the craft beer completion later this year, the revenue growth percentages will fall off quite a bit.

Overall, Tilray continues to make solid progress on its cost structure. While beverage margins were down slightly, gross margin dollars soared thanks to that large revenue increase. Cannabis margins were down significantly due to the completion of the HEXO advisory services agreement in Q1 fiscal 2024, while distribution margins rose. Overall, adjusted net income for the period was more than $35 million, compared to a nearly $12 million loss a year earlier. The adjusted profit of 4 cents per share handily beat street estimates by a nickel per share.

Balance sheet progress continues:

Tilray reported over $30 million of adjusted free cash flow in Q4. That number did drop about 37% from the year ago period, but at least we’re past some of the large cash burn quarters. The fourth quarter number meant the second straight year of adjusted free cash flow, although the end result of nearly $6.6 million was down significantly from the prior year’s $19.1 million.

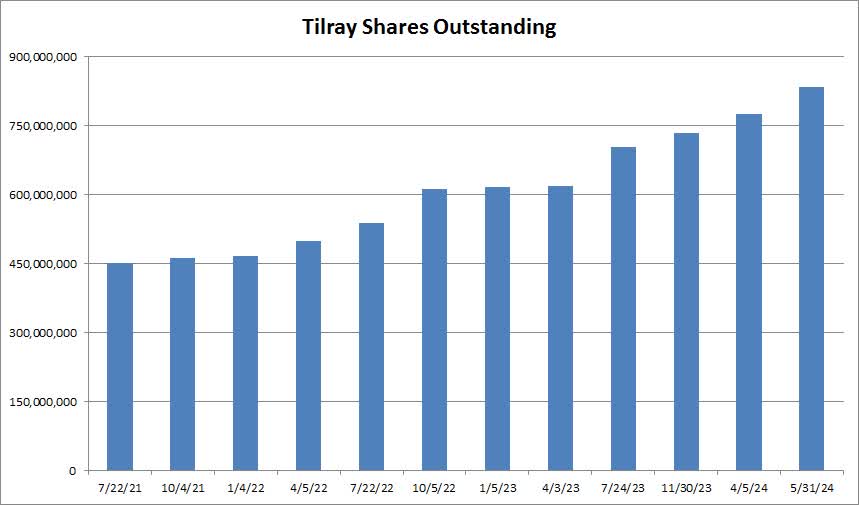

The company has worked to reduce its large debt pile significantly in recent quarters. Total debt came down by more than $80 million alone in the Q4 period, while the net debt balance improved significantly from over $177 million to $61 million sequentially. However, that major progress has come at a large cost to shareholders, however, as dilution continues to pile up over time as seen in the chart below.

Tilray Shares Outstanding (Company Filings)

To get the balance sheet to a net cash positive position, the company will either have to raise more money through its share offering program, or make additional deals with bondholders to convert those debts to shares. It is possible that we’ll see a net cash positive position during this May 2025 fiscal year, but that could take the share count over 900 million when you include other expenses already paid via stock.

Looking at the valuation:

On a valuation front, Tilray went into Monday’s report trading for about 1.75 times its expected sales for the May 2025 fiscal year. That’s a sizable discount to the valuation that peer Canopy Growth (CGC) went for at 2.7 times its March 2025 expected revenue. Tilray is projected to see more near term revenue growth, although Tilray was trading at less than half the price to sales number of Canopy when I last covered the name, so that gap closed quite a bit.

Street analysts are still fairly positive on Tilray. The average price target is currently $2.37, which implied nearly 30% upside from Monday’s regular session close. I should note, however, that the street average was over $3.30 a year ago, so analysts have cut their targets a bit, likely on this massive ongoing dilution. The after-hours rally gets shares closer to the street average.

Final thoughts / recommendation:

In the end, Tilray reported some decent results on Monday afternoon. The company beat top line estimates for the first time in three quarters, and delivered a solid adjusted bottom line beat. The company is working to get its costs down, and the balance sheet is improving nicely, albeit at a cost of significant dilution to shareholders over time.

For the moment, I am maintaining my hold rating on the stock. While there was some improvement in Q4 and the valuation is fair, the balance sheet just isn’t where it needs to be quite yet. I need to see how the revenue growth story plays out once some of these acquisition anniversaries are hit, and there’s still likely a bit of dilution ahead of us. When we see how these key items fare over the next couple of quarters, we can evaluate the rating again.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.