Summary:

- New CEO Ben Gagnon, previously Chief Mining Officer, brings detailed operational knowledge and transparency, but Board governance remains in question due to Riot’s influence.

- Q2 results were mixed; revenue fell due to April’s halving, but increased hash rate and BTC price helped mitigate losses.

- Bitfarms’ potential expansion into HPC/AI offers future growth, but current capex exceeds operating cash flows, and Riot’s control struggle adds uncertainty.

- For these reasons, it’s safer to treat BITF as a Hold.

John M Lund Photography Inc

Bitfarms (NASDAQ:BITF) is a Bitcoin (BTC-USD) miner I’ve covered twice now. The first time, I give a general summary of the company and my initial appraisal, and the second time I provided a follow-up after the release of Q1 2024 results.

Both times I rated BITF a Hold, citing a lack of positive free cash flow; potential for share dilution; the strained departure of their CEO in the spring; an attempted takeover by a rival, Riot Platforms (RIOT); and potential revenue loss from April’s halving event.

It also had it good points, such as their more efficient operating model, positive cash flows from operations, a decent cash balance, lack of debt, and better overall strategic sense of their business.

I still rate BITF a Hold, but new developments, good and bad, from the release of Q2 2024 results and afterward are worth an update to my thesis.

Leadership Changes

In Q2, Ben Gagnon was confirmed as the new, permanent CEO. Having previously served as the Chief Mining Officer, he’s no stranger to Bitfarms or its operations.

Q2 2024 Company Presentation

Moreover, I’ve quoted him before from earnings calls. I’ve found that he’s willing to give detailed answers to analysts that enhance investors’ understanding of the business and why the goals they set are important. In my view, he was a natural replacement for Morphy as CEO.

He is also replacing the interim CEO, Nicolas Bonta, who had taken the role as Chairman of the Board of Directors. On that note, Bonta, one of the company’s founders, has been removed from the Board. This is a result of the continued takeover attempts by Riot, and much of this occurred in the third quarter and even after the Q2 earnings call, which was August 9th.

The first thing worth noting is that Riot opened a suit against Bitfarms, appealing for three new directors on the Board. They also launched an activist website called ABetterBitfarms.com in early July.

ABetterBitfarms.com

The screenshot above speaks to Riot’s displeasure with the response to their takeover attempt. As I mentioned last time, Riot acquired 12% of the company’s shares, making them the largest shareholder. In turn, the Board announced a poison pill plan to dilute BITF with new issues if Riot ever exceeded 15% of the outstanding shares. As a result of the suit, however, the plan was overturned, resulting in a second that set a new threshold at 20%. Riot has since increased its stake in BITF to 18.9%.

Bonta’s removal as Chairman occurred on August 13th, after additional pressure from Riot. This follows the failure of Emiliano Grodzki, another co-founder, to win re-election to the Board at the annual shareholder meeting in May.

Thus, while I feel good about Gagnon as a new CEO, the governance of the Board is in question and shows Riot steadily improving its position, even ousting founders. This may result in a deal to acquire all of BITF, which is important to keep in mind as I review the financial results.

Q2 Results

Their second quarter wasn’t too bad, but it was affected by the halving in April.

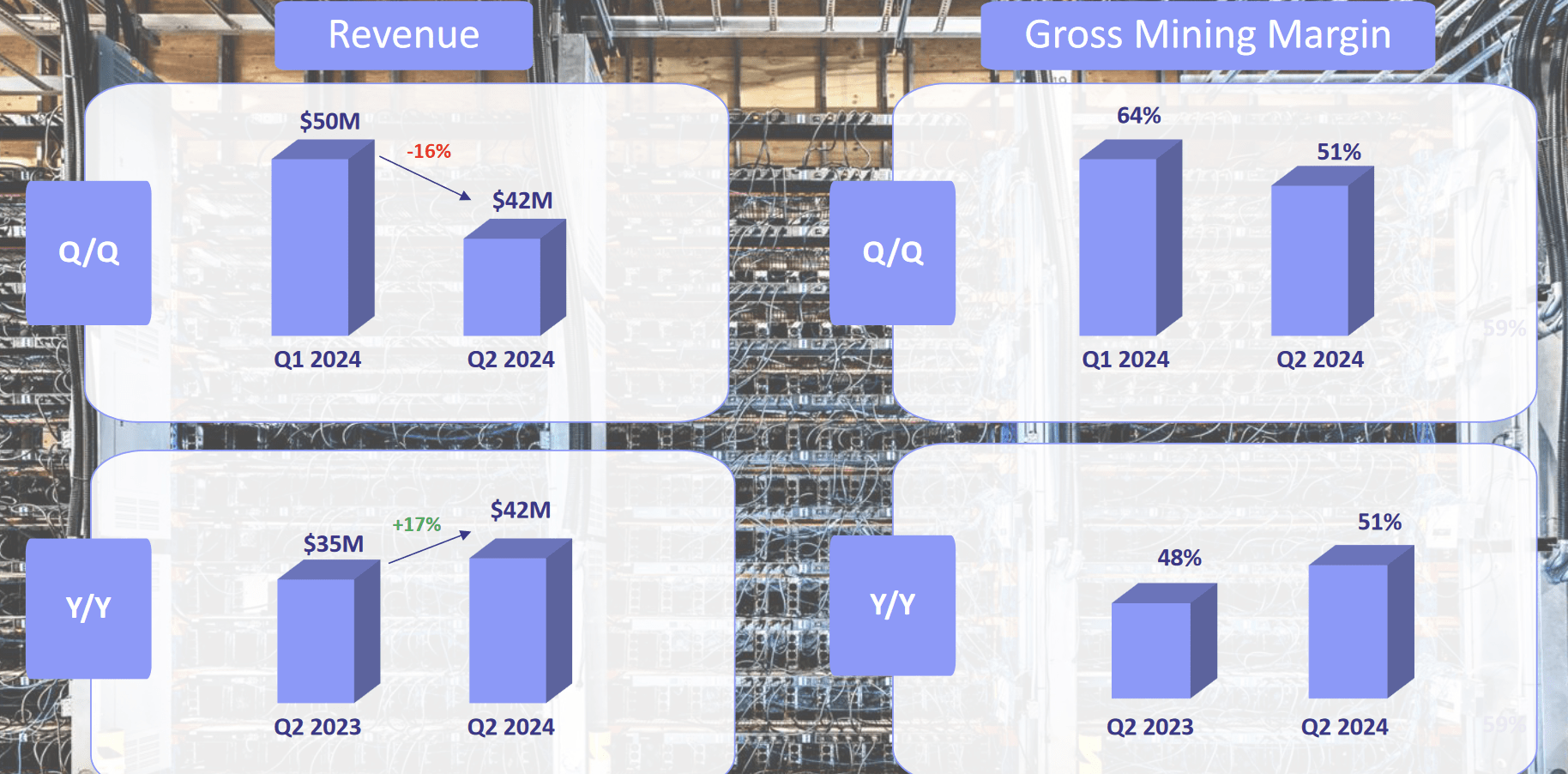

Q2 2024 Company Presentation

While revenue and margin showed improvements compared to year-over-year results, this was not true for quarter-over-quarter. Revenue fell from $50M to $42M. In the earnings call, CFO Jeff Lucas summarized the causes:

The change was due primarily to the decrease in block rewards following the April halving. During the quarter, we earned 614 Bitcoin, 35% fewer quarter-over-quarter, primarily the result of the halving and a 10% increase in average network difficulty.

Why only 16% less revenue for 35% percent less BTC mined? The main reason would have to be the favorable shift in its price.

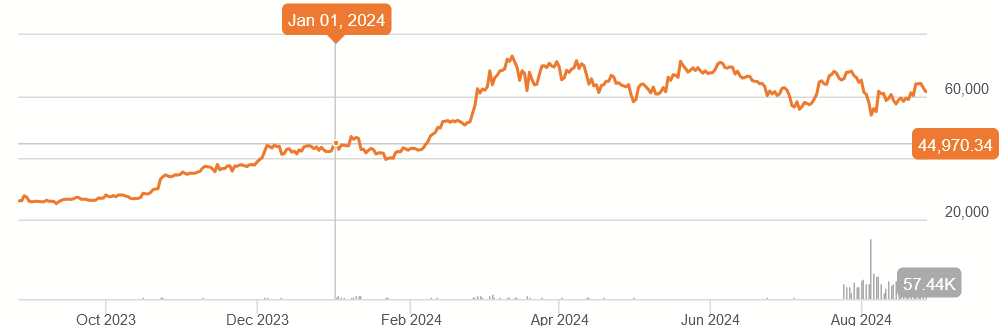

BTC 1Y Price History (Seeking Alpha)

With lower prices in much of Q1, Q2 results were enhanced despite the reduced volume, as the price as typically stayed around $60K.

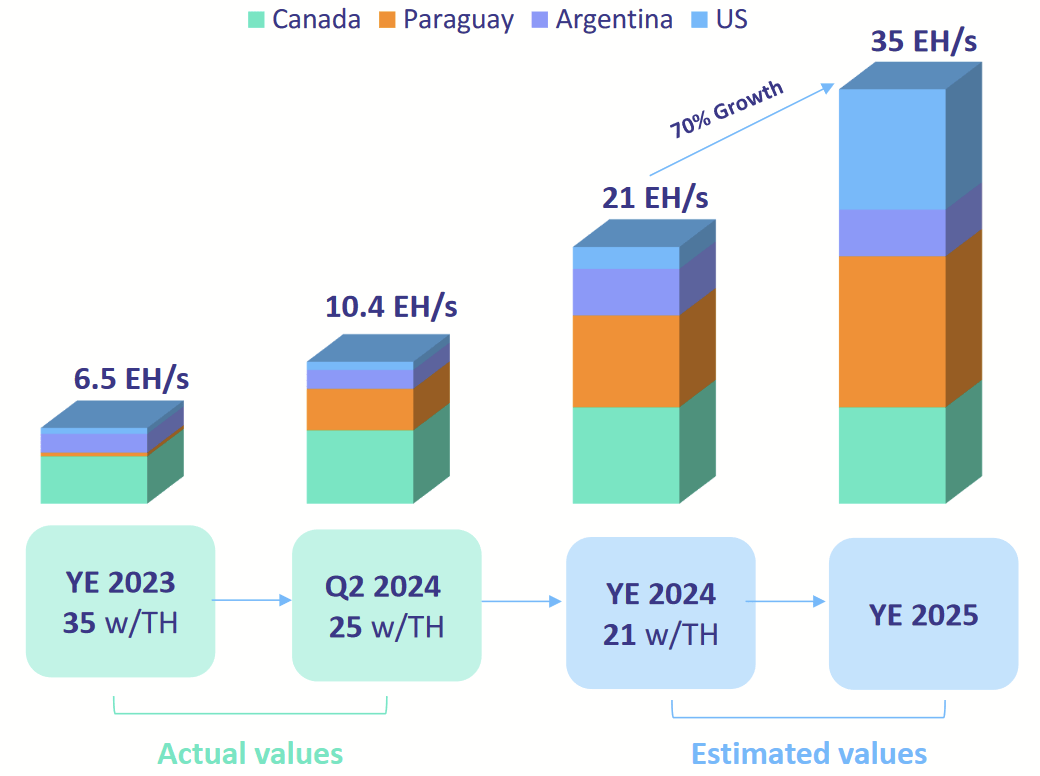

Q2 2024 Company Presentation

This has further been helped by their ability to increase their hash rate and maintain competitive BTC production. Currently they are projecting that they will be able to double their hash rate by the end of the year and more than triple by the end of 2025.

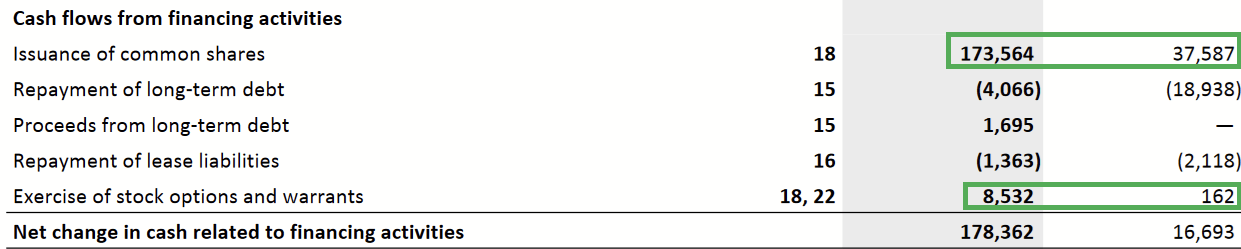

Cash Flow Statement (Q2 2024 Financial Report)

Operating cash flows from the six months ending June 2024 were up significantly compared the prior year, indicating their ability to scale effectively. Yet, significantly more has been spent on capex, as indicated in the traditional line item of property, plant, and equipment, up to $123M from $19M last year. We must, however, almost count the $31M spent on equipment prepayments. As I discussed last time, these pertain to miner option contracts, allowing BITF to lock in prices on future miner purchases, making them a component of capex.

Cash Flow Statement (Q2 2024 Financial Report)

As those impacts make free cash flow negative, the gap has been plugged by increased sales of new shares on the open market and employee options, up to $181M from about $38M last year. (Ironically, BITF may not need to declare a poison pill to dilute Riot.)

Q2 2024 Financial Report

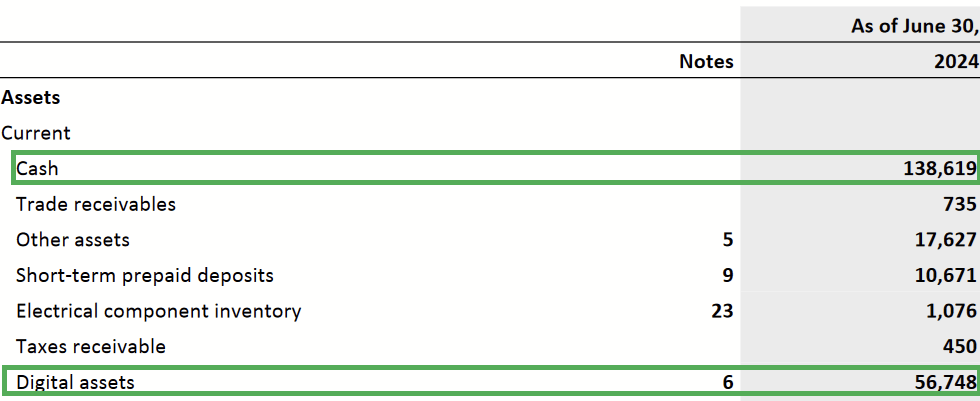

The balance sheet, meanwhile, shows about $195M in cash and crypto, providing what will likely be sufficient liquidity for the near term.

Potential for Other Segments

While Bitfarms is primarily a BTC miner, Gagnon spoke to his vision for growing the company, such that it will not depend exclusively on mining. Given their sites in Pennsylvania, he noted:

…the PJM grid is the largest wholesale electricity market in the U.S., offering abundant access to competitively priced, and flexible power that is attractive for multiple uses including Bitcoin mining, energy trading and even HPC/AI.

Q2 2024 Company Presentation

This is an interesting development, and it may ease the task of generating positive free cash flow. Of course, one has to wonder what makes them suited to this work when their focus has been mining. Gagnon had an answer for that, however:

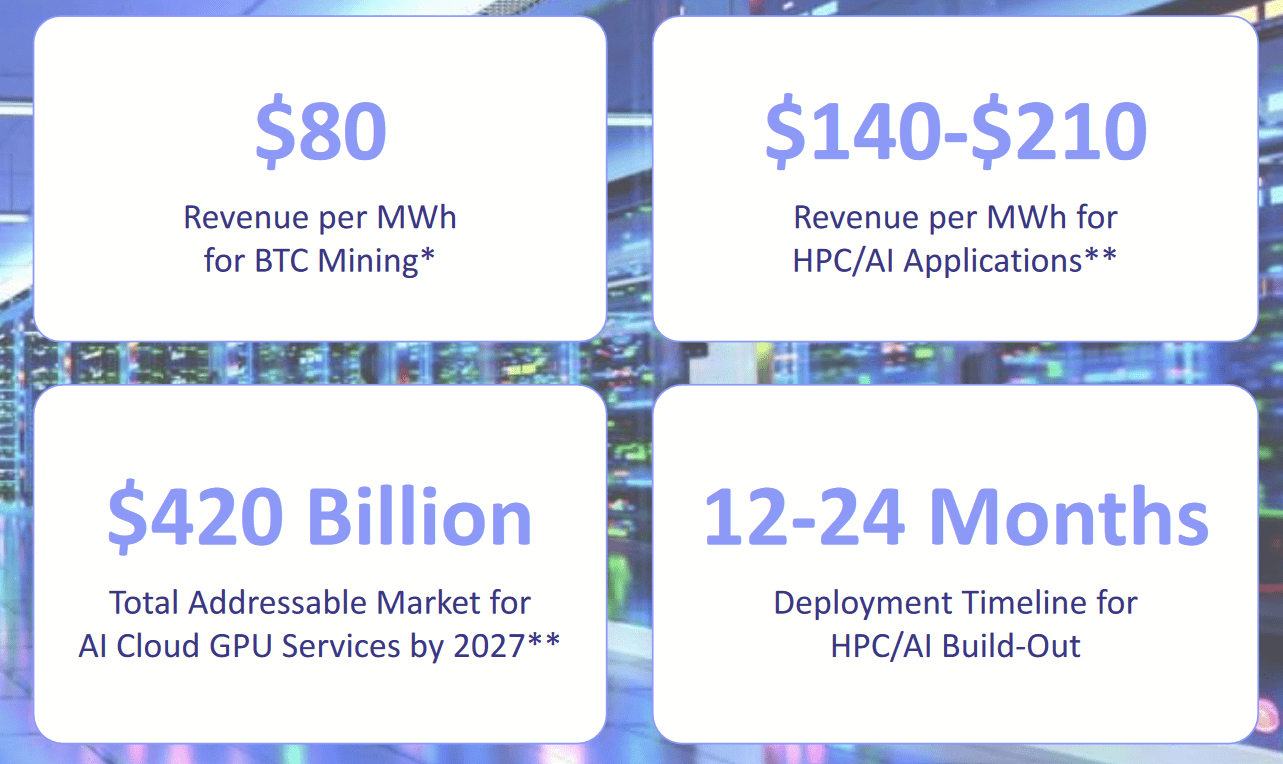

We own and operate a portfolio of high-quality energy assets that are currently monetized through Bitcoin mining. When we take a step back and look at how we get the most value and utilization out of our portfolio, we believe that HPC/AI has real potential. Recent HPC/AI deals are boasting revenues from approximately $140 to $210 per MWh these are potentially very attractive and stable high margin revenue streams not correlated to Bitcoin prices.

Of course, it will take a year or two before anything is realized here, so it’s difficult to comment on the actual financial potential, but it’s a reassuring sign to see that, despite the battle over control of the company, management still is thinking critically about its operations and sees potential that goes beyond the original vision of simply mining BTC.

Conclusion

The new vision to branch into HPC/AI adds more potential for positive, cash flows in the future, but that is a couple of years out. At the present moment, capex exceeds operating cash flows, and a struggle for control of the company is occurring. If Riot succeeds in taking it over or exercises further influence, then the company’s priorities could change entirely.

While many details changed since my last coverage, my overall judgment is mostly the same. As free cash flow remains negative, a market cap of $1 billion for that doesn’t give a margin of safety that is sorely needed here. Positive cash flows may not come close to that if and when they do occur. Even an optimistic thesis on the operations is complicated by the dispute with Riot.

For these reasons, I continue to think that BITF is a good miner can’t be rated better than a Hold.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.