Summary:

- Since the Cominarty vaccine is now arguably relegated to something similar to the seasonal flu shot with an expensive $130 retail price tag, it is unsurprising Mr. Market is bearish on the PFE stock.

- The generic Paxlovid may also temper some of its top-line, as witnessed with AbbVie’s Humira, which experienced a -25.9% impact in the international market.

- However, the COVID-19 windfall has also contributed to its robust balance sheet and aggressive M&A activities, bolstering its pipelines ahead.

- Therefore, assuming an upward rerating, PFE could hit our price target of $55.79, suggesting a 27.40% upside potential from current levels.

koto_feja

The Covid Reset Is Right – Though Overly Pessimistic

With the worst of the COVID-19 pandemic now over, Pfizer Inc (NYSE:PFE) may have a challenging 2023 indeed. The stock had already retraced by -19.6% since its recent peak in mid-December 2022, nearing its 52-week low of $41.45.

The situation was further destabilized by the disappointing FQ4’22 earnings and FY2023 guidance, pointing to the reduced demand for COVID-related products, significantly worsened by the tougher YoY comparison.

As a result of the reopening cadence globally, we speculate that market sentiments surrounding the Cominarty vaccine may be downgraded to the optional bivalent COVID-19 shot from 2023 onwards, similar to that of the influenza vaccines.

CDC had estimated that 51% of the US population received influenza shots in 2022, which cost an average of $21.10 each. However, with the guidance of up to $130 per Cominarty dose (free with private insurance or government-paid insurance), it remains to be seen if PFE may benefit from retail demand moving forward.

The uncertain macroeconomics may also pose some headwinds, with tightened discretionary spending through 2024. For now, demand for PFE’s booster shot had been declining, from 22M in the first six weeks of 2021 to 14.8M in the first six weeks of the bivalent rollout in 2022, despite the provision of free vaccines from government subsidies.

Assuming a similar cadence, it is no wonder that market analysts expect to see a notable decline in the company’s top-line performance from 2023 onwards.

Notably, the pharmaceutical giant obtained the US FDA fast-track designation on the combined COVID-flu vaccine by November 2022. However, the competition will be intense indeed, against Moderna’s (MRNA) COVID-flu vaccine in Phase 1 clinical trials and COVID-flu-RSV in Phase 2 trials. Novavax (NVAX) is similarly working on its COVID-NanoFlu combination candidate already in Phase 1/2 trials.

In addition, with generic drugmakers looking to sell versions of PFE’s Paxlovid for $25 or less (only in lower-income countries), it remains to be seen how its business will be affected, since the branded therapy cost the US government approximately $530.

We posit that it may likely experience similar effects as AbbVie’s (ABBV) Humira, which had reported a decline in revenue by up to -25.9% for international markets. In this particular case, Mr. Market may have been right about the COVID reset.

Will Mr. Market Upgrade PFE’s Forward Execution?

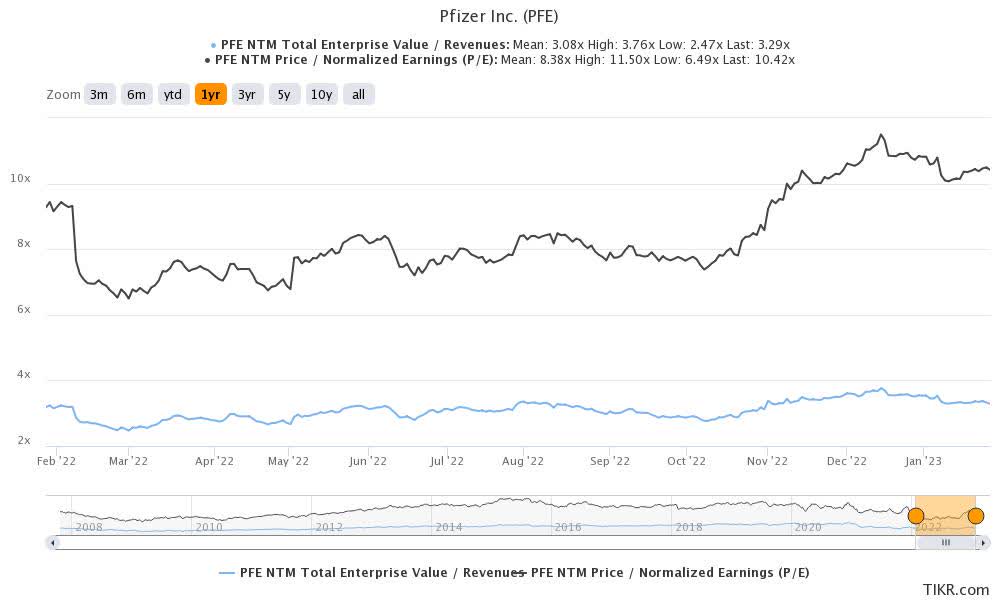

PFE 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

PFE is currently trading at an EV/NTM Revenue of 3.29x and NTM P/E of 10.42x, lower than its 3Y pre-pandemic mean of 4.66x and 13.51x, respectively. Otherwise, it is higher than its 1Y mean of 3.08x and 8.38x, respectively. Based on its projected FY2024 EPS of $4.08 and current P/E valuations, we are looking at a moderate price target of $42.51.

There are many ways of looking at this really. PFE had previously reported an annual EPS of $2.97 and P/E mean of 14.23x in 2019, prior to pandemic levels of $6.48 and 11.12x in 2022, respectively. Interestingly, the stock also currently trades lower compared to its peers, such as Merck & Co (MRK) at 15.44x, MRNA at 33.49x, and Vertex Pharmaceuticals (VRTX) at 20.07x.

For now, PFE’s discounted valuation is likely attributed to the patent cliff from 2025 onwards. The management has guided a normalization in the top line to ~$52B by 2025, excluding the contribution of COVID revenues then. That is a big difference, from 2022’s guidance of between $99.5B and $102B, with $56B attributed to the COVID contribution. Furthermore, the company may lose approximately $17B of annual revenue from the loss of exclusivity by the end of the decade, helping to explain Mr. Market’s pessimism thus far.

However, we are more optimistic, since the global success of PFE’s Cominarty vaccine has significantly boosted its balance sheet to $36.13B in cash by the latest quarter, growing by 372.8% compared to FY2019 levels of $9.69B. This translates to net debt levels of $867M in the latest quarter, against FY2019 levels of $43.75B. Combined with its $2B of stock repurchased and $8.92B of dividends paid out (+2.2% YoY) over the LTM, we reckon that Mr. Market has been overly critical.

Furthermore, PFE had been embarking on aggressive M&A activities significantly aided by the COVID-19 windfall, bolstering its pipeline at the same time. Notably, the company acquired Arena Pharmaceuticals for $6.7B, Array BioPharma for $11.4B, Therachon for $810M, Trillium Therapeutics Inc for $2.22B, Global Blood Therapeutics for $5.4B, Biohaven Pharmaceutical for $11.6B, and ReViral for $525M.

This is on top of PFE’s multiple collaborations with Clear Creek Bio, Valneva, among others. The management now guided non-COVID revenues of up to $84B by 2030, suggesting an excellent normalized CAGR of 6.8% between FY2019 and FY2030, against the pre-pandemic levels of -0.7% between FY2016 and FY2019.

Interested readers may refer here for an in-depth analysis of its clinical pipelines. In short, PFE has now expanded its working pipeline with 15 new programs since 2019’s level of 97 programs, with more likely to come from the M&As in the intermediate term.

Therefore, assuming a moderate upward rerating of PFE’s P/E valuations to normalized levels, we may be looking at an improved price target of $55.79. This mirrors market analysts’ more bullish target of $53.71 as well, suggesting an excellent 19.06% upside potential from current levels.

While the bulls may have suggested even more optimistic numbers of over $60s, PFE’s pipeline would need to prove itself with regulatory approvals and top/bottom line contributions first. For now, the company is only expected to report FY2030 EPS of $3.68 despite the projected net income of $23B, partly attributed to the forecasted share count growth from the current 5.61B to 6.2B.

The story is naturally different for MRK despite the similar market cap of $280B and projected net incomes of $24B, since the company currently boasts a tighter share count of 2.53B, which may consequently trigger an improved FY2030 EPS of $9.38.

On the other hand, if PFE were to release a similar blockbuster therapy with expanded applications and extended patent expiries like MRK’s Keytruda, we may naturally witness another upward rerating in its P/E valuations. This suggests a price target of $63. Only time will tell, since 27 of 112 pipelines are already at the Phase 3 clinical trial stage.

Pending successful clinical trials and accelerated US FDA processes, the PFE management guided up to 19 approvals over the next eighteen months. These may, therefore, temper some of the COVID-19 deceleration in the intermediate term.

As a result, we are rating the PFE stock as a Buy now, with the caveat that it should lower the long-term investor’s dollar cost average accordingly. That strategy would provide investors with an improved margin of safety, made sweeter by the projected dividends of $1.78 by FY2025. Those that nibble now would be looking at a decent yield of 4.06%, against its 4Y average of 3.63% and sector median of 1.29%.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The analysis is provided exclusively for informational purposes and should not be considered professional investment advice. Before investing, please conduct personal in-depth research and utmost due diligence, as there are many risks associated with the trade, including capital loss.