Summary:

- Regulators will not let this deal pass easily but the possibility of a peaceful solution remains.

- FTC’s arguments look unfounded, Microsoft will have a clear advantage in court.

- CMA’s decision is a real threat to this deal.

- The deal going through one way or another remains my base case despite the concerns, MSFT & ATVI are Buys.

Chris Cook/iStock Editorial via Getty Images

Main thesis

The Microsoft (NASDAQ:MSFT) – Activision Blizzard (NASDAQ:ATVI) drama has been going on for a year as the watchdogs from the US, the UK, and the EU are still fighting for the game studio’s independence. Regulatory investigations are ongoing and the FTC has already publicly disapproved of the deal and filed a lawsuit. Now it all comes down to whether Microsoft can prove it’s not violating antitrust laws. I think that the chances for this are quite high, given the position of the corporation in the gaming market.

The fight with regulators

FTC case: unconvincing arguments that likely won’t work in court

On December 8, the Federal Trade Commission stated that it seeks to block the acquisition and released a complaint document. The whole complaint boils down to the fact that the FTC believes that if Microsoft gets access to the Activision Blizzard library, this could adversely affect competition in the gaming market. Nothing new. However, here the regulator tried to dive a little deeper, and then the whole thesis began to crumble in my opinion.

Let’s take a look at some of FTC’s claims.

Xbox Series X|S and PS5 consoles are the only high-performance consoles available today, and are considered to be in the ninth generation of gaming consoles. In contrast, Nintendo’s most recent console—the Nintendo Switch—is not a ninth-generation gaming console

The question immediately arises, based on what legal documents were the consoles divided into specific generations?

Retailing at $299.99, the Nintendo Switch is also less expensive than the Xbox Series X and PlayStation 5 consoles, both priced at $499.99

The FTC is taking into account the most expensive PlayStation and Xbox versions, but not the most expensive Nintendo (OTCPK:NTDOY) Switch (OLED version), retailing at $349.99.

While the Xbox Series S had the same retail price at launch as the Nintendo Switch, the graphical and processing capabilities of the Series S are much more aligned with the Xbox Series X and PS5 consoles.

In this particular case, we are talking about market share and competition, not computing power.

Due to their distinct offerings, Microsoft and Sony consoles appeal to different gaming audiences than the Nintendo Switch. While Xbox Series X|S and PS5 consoles offer more mature content for more serious gaming, Nintendo’s hardware and content tends to be used more for casual and family gaming.

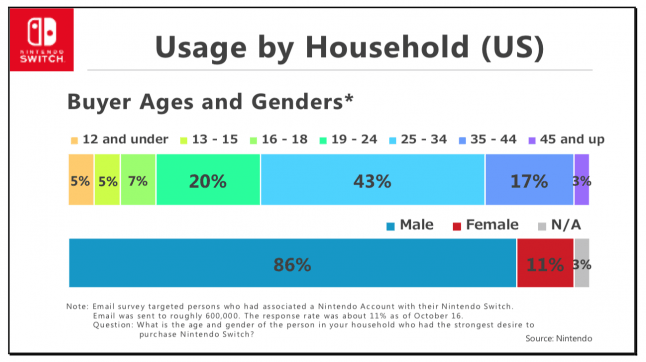

Firstly, this statement, like the previous ones, is not supported by any statistics. Secondly, 43% of Nintendo Switch users are men between the ages of 25 and 34. The Call Of Duty franchise is aimed at the same audience. The regulator itself said that the deal with Activision is beneficial only to Microsoft. However, with the release of CoD on the Switch, Nintendo will also be able to attract new users, but the FTC does not see the latter as a full-fledged player in this market.

nintendolife.com NewZoo

While Microsoft’s Xbox Series X|S and Sony’s PS5 consoles incorporate semi-custom systems-on-a-chip (“SoC”) designed by AMD, Nintendo’s Switch runs on a non-AMD SoC that is more closely related to a mobile device processor found in higher-end mobile phones and tablets.

By this logic, PS2 and Xbox, based on the fact that they had processors from different manufacturers, operate in two separate markets.

The third major gaming console available today, the Nintendo Switch, is highly differentiated from the Xbox and PlayStation consoles in significant ways. The Nintendo Switch, therefore, is not included in the Relevant Market.

That is, they simply made irrelevant arguments and based on the same arguments, they chose to not consider Nintendo a full-fledged competitor to both Microsoft and Sony.

Gaming PCs are distinct from High-Performance Consoles due to differences in price, hardware, performance, and functionality (i.e., where and when a game can be played), among other factors. Gaming PCs are therefore not included in the Relevant Market

There is no explanation at all of the position of the regulator, according to which gaming PCs are not included in the Relevant Market.

Another interesting point, as noted by the MLex investigative agency, it appears that the FTC was incorrect in this document about the guarantees that Microsoft gave to the European regulator in the ZeniMax deal (Bethesda’s parent).

Microsoft assured the European Commission (“EC”) during its antitrust review of the ZeniMax purchase that Microsoft would not have the incentive to withhold ZeniMax titles from rival consoles

Referring to the information received from the EU regulator, Microsoft never promised the regulator in the EU that it would not make Bethesda projects exclusive. This is an incredibly strong precedent that Microsoft’s lawyers can cling to if the antitrust authority made false arguments in a white paper outlining the reasons for disapproving the deal between the companies.

Summing up, the FTC simply just didn’t include two very important systems for the gaming industry in Relevant Markets. I think they brought unsubstantiated theses and concluded based on these theses, which led to a distortion of the overall picture in this market. In addition, it appears the regulator was incorrect in the complaint document. This is not something on which to build a lawsuit against the largest acquisition in the history of the IT sector.

CMA: The real threat to this deal

The FTC’s poor arguments certainly will play in favor of Microsoft in court. However, the US regulator might just rely on CMA to block it at this point. The thing is that it is almost impossible to overturn the CMA’s decision in London. If Microsoft finds any discrepancy, they apply to CAT (Competition Appeal Tribunal), which, in turn, does not have the right, under the Enterprise Act, to roll back the decision of the CMA, but only to force the watchdog to change some of the processes due to which they concluded. And yeah, these processes take a very long time.

The CMA will soon release a complaint document expressing its concerns. Unfortunately, the arguments themselves do not mean anything, so only the conditions that the regulator will offer matter. I think the deal will be considered anti-competitive but one that could be fixed through remedies. And this is where things can get ugly. The UK’s watchdog can offer behavioral remedies. It will be something similar to the 10-year agreements that Microsoft offered to Sony and Nintendo. However, there is a possibility that so-called structural remedies will be offered. This would mean that Microsoft would not get the assets it originally wanted. For example, Activision becomes an independent company, while Microsoft gets Blizzard and King. Or the corporation will be forced to sell Activision to a third party. None of the options might seem attractive to Microsoft, and indeed there is a possibility of abandoning this deal. In any case, I don’t believe the CMA will simply oppose and block the deal because it cannot be legally justified. In addition, the political factor is slightly reduced here, since the regulator is not yet in the war against big techs.

As for the European Commission, these two regulators are likely to cooperate and stick to the same rhetoric. The protest of the European Commission will look strange without the support of the CMA.

Microsoft & Activision stock

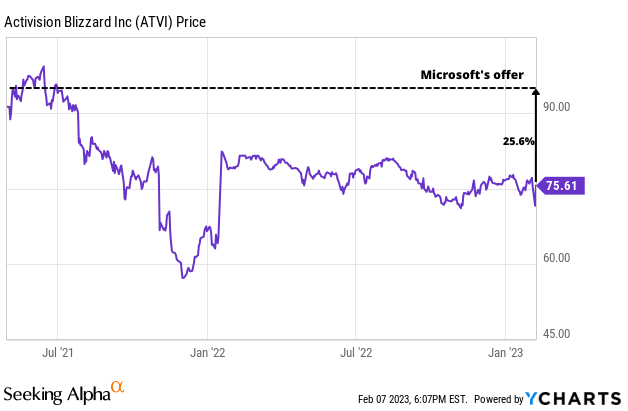

As for Activision Blizzard, here the thesis has not changed since the beginning of last year. There is an attractive arbitrage opportunity, with the stock having a significant downside if the acquisition is abandoned. However, given the company’s good results for the last quarter (bookings are up to $3.57B, up 43% from $2.49B in Q4 2021), the possible downside is decreasing. Besides, if Microsoft backs out of the deal, the company will get a breakup fee of $2-$3 billion, which they can send to buybacks. At the moment, the upside to $95 is 25.6%. Even taking into account the fact that the approval of the transaction may stretch until mid-2024, this arbitrage play still looks attractive.

YCharts

Concerning Microsoft, at this stage, Activision is not considered to be a part of the corporation’s gaming segment at all. There have been doubts about the deal before, and the forecasts of the company itself and analysts about future financial results still do not take into account the takeover of Activision Blizzard. The stock has been underperforming the broader market over the past few months, but that’s not related to the deal. If the deal does not go through, then Microsoft has practically nothing to lose, only legal costs and breakup fees. However, this is likely to cause resentment on the part of investors. At the same time, if the deal is approved, Microsoft could move closer to the current market leaders. In particular, in 2022, the company’s sales, taking into account the revenue of Activision Blizzard ($8.0 billion), may amount to about $24-25 billion against Tencent’s (OTCPK:TCEHY) $29.4 billion and Sony’s (SONY) $23.7 billion.

Conclusion

It is safe to say that relying on the common sense of regulators did not work. Well, now a bet on Activision is a bet on Microsoft’s ability to answer all of the FTC’s allegations, as well as a bet on reasonable suggestions from the CMA.

That said, I continue to believe that the deal can and will go through. Thus, MSFT and ATVI are both Buys.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.