Summary:

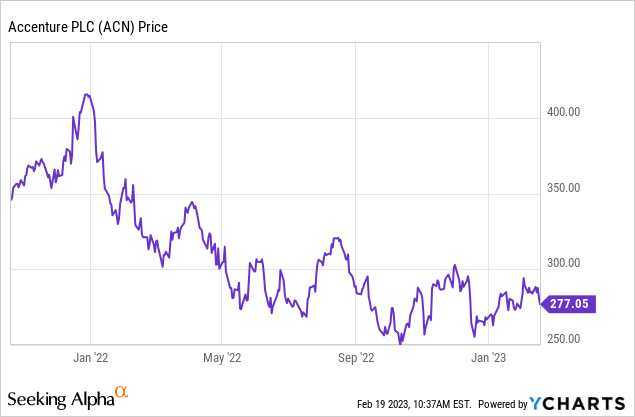

- Accenture is down over 33% from its all-time high in 2021.

- The company is facing macro headwinds but digital transformation should continue to be a strong tailwind.

- Latest financial results continue to be solid with EPS up 11%.

- Its current multiples have also come down a lot and are now trading below its historical average.

- I rate the company as a buy.

Maskot

Investment Thesis

Accenture (NYSE:ACN) has been a solid performer in the past decade with shares up over 270% during the period, significantly outpacing the S&P 500 Index which was up roughly 170%. However, it has been struggling in the past year, with the share price pulling back over 33% from its all-time high due to macro headwinds such as rising rates and elevated inflation.

I think this is a great buying opportunity for a long-term winner, as the company’s fundamentals remain strong. Digital transformation should continue to be a strong growth driver in the foreseeable future, and consultancy services should be resilient as businesses will always need to create value regardless of the economic condition. The company is also trading at a compelling valuation with multiples below its 5-year historical average. Therefore I rate ACN stock as a buy.

Digital Transformation

Accenture is a Dublin-based company with over 700,000 employees. The company offers technology and consulting services to customers around the globe. It helps clients overcome technological changes, improves their operations, and creates value. It is currently the largest public consulting company and serves over 75% of the Fortune Global 500.

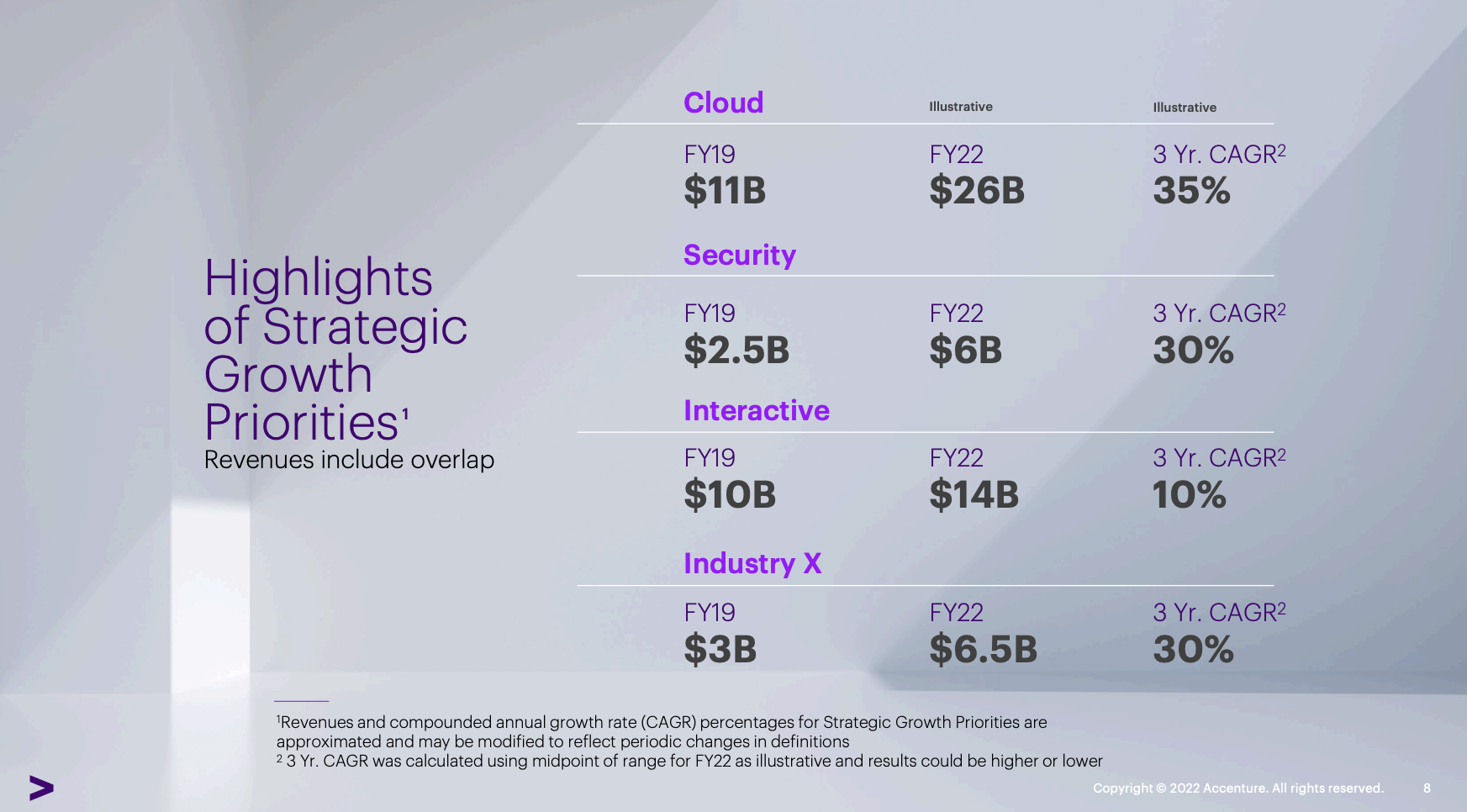

Technology services have been the company’s focal point, which now accounts for over 60% of total revenue, thanks to strong momentum in high-growth segments such as Cloud and security. For instance, revenue from Cloud has grown from $11 billion in FY19 to $26 billion in FY22, representing an extraordinary CAGR (compounded annual growth rate) of 35%.

Accenture

Digital transformation is one of the biggest trends of the century. It is a huge tailwind for Accenture as it significantly accelerates the pace of technological change. The recent pandemic also further boosted it as people saw how critical technology could be. For example, retail companies realized the importance of e-commerce during the pandemic as people are forced to stay home and there is literally no foot traffic in-store. This forces companies to adopt new technologies quickly in order to keep up with the world.

Despite recent progress, we are still only in the early innings and the opportunity is massive. Even after the pandemic, e-commerce still only accounts for roughly 19% of global retail sales, and the figure is estimated to grow to 25% by 2026, according to Statista. Another example is Cloud, which is becoming increasingly important as it vastly improves operation efficiency and creates immense value for companies. According to McKinsey, the market for Cloud is projected to reach $3 trillion by 2030, as adoption rates continue to grow rapidly. This in turn increases the demand for Accenture as large companies usually require professional help for onboarding new technologies.

Julie Sweet, CEO, on the opportunity of Cloud:

Cloud, a $26 billion business in FY ’22 grew 48%, with even stronger growth in Cloud First and continues to grow very strong double digits. In fact, we believe that the cloud continuum will become the new operative system for the future enterprise. Migrating to the cloud to drive efficiencies is just the first step. As we anticipated with our Cloud First strategy and investments, we are seeing our clients make significant investments to modernize, improve and innovate in the cloud, leveraging data and AI to drive new business value.

Accenture

Financials and Valuation

Accenture latest earnings result showed solid growth despite facing a challenging macro backdrop.

The company reported revenue of $15.7 billion compared to $15 billion, up 5% YoY (year over year). Due to the company’s global presence, revenue got impacted heavily by the strong dollar, revenue growth was actually 15% on a constant currency basis. The growth is driven by high demand from the resources and products industry, which grew revenue by 21% to $2.1 billion and 15% to $4.7 billion respectively (on a constant currency basis). Cloud and Industry X (digitization-related services) continue to see strong traction with high double digits growth YoY (the company did not disclose the exact figures).

The bottom line’s performance was also very solid. Operating income increased 7% YoY from $2.43 billion to $2.59 billion. The operating margin was also up 20 basis points to 16.5%. This is largely due to operating expenses being up only 4.4% from $2.48 billion to $2.59 billion, despite facing inflationary pressure. Diluted EPS was $3.08 compared to $2.78, representing an increase of 11% YoY.

The company’s balance sheet is extremely strong. It ended the quarter with $5.9 billion in cash and only $3.9 billion in debt. Thanks to this, the company has raised its quarterly dividend by 15% from $0.97 to $1.15, representing a forward yield of 1.62%. It also continued to buy back shares with $1.4 billion deployed during the quarter. The current remaining share repurchase authority was $4.9 billion, or 2.8% of the market cap.

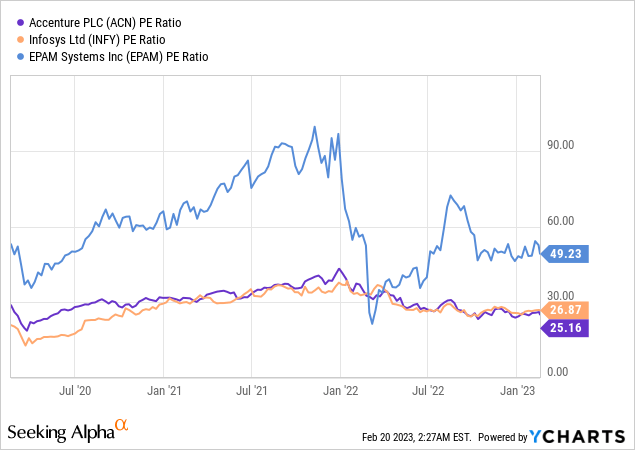

After the significant pullback, Accenture’s valuation is starting to look attractive. The company is currently trading at a P/E ratio of 25.16x which is very reasonable in my opinion. This represents a 12.8% discount compared to its 5-year historical average of 28.85x. The multiple is also below consulting peers such as Infosys (INFY) and EPAM Systems (EPAM), which are trading at a P/E ratio of 26.87x and 49.23x respectively, as shown in the chart below.

Investors Takeaway

I think Accenture’s current price point is compelling. Digital transformation is still in the early stages and should continue to be a strong growth driver for the company, especially in high-growth areas like cloud and AI. The latest financial performance was very solid with double-digit EPS growth, not to mention the tough macro environment we are in. The valuation has also come down a lot and is now below both peers and historical averages. I see decent upside potential and I rate the company as a buy.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.