Summary:

- Tesla, Inc.’s prices for the most expensive models have been reduced.

- This is obviously a problem for the EV maker’s profit margins.

- A recession is near, and the EV market is not going through its best days.

- Tesla stock is ridiculously overvalued.

- I would not recommend to short sell Tesla stock, either.

jetcityimage

Tesla, Inc. (NASDAQ:TSLA) stock has gained since my last article. Yet, the recent banking crisis and, most importantly, the fact the company was forced to decrease its Model S and Model X prices make me somewhat concerned. I mentioned in my previous article that as a popular stock, Tesla might well rise in value. However, the fundamentals were not there and are even worse now. But let me explain this later on.

Tesla’s news

Let me first mention that Model S and Model X models are considered to be luxurious. In my view, electric vehicles generally are considered to be premium-class goods. Indeed, it is much cheaper to buy a used car powered on normal petrol than it is to buy an electric vehicle (“EV”). But Model S and Model X are more expensive than other cars produced by Tesla. The demand for such premium goods produced by Tesla is normally inelastic to price cuts. Let me explain.

Higher-income, environmentally cautious consumers that also like Elon Musk’s brand are likely to be Tesla’s potential customers. They want to buy a higher-class good and are not prevented from doing so even if the price of this good rises somewhat. But recently Tesla’s management even had to decrease the prices of its higher-class cars twice. To me, this signals a substantial fall in demand. And the management is doing the best it can to somehow mitigate the situation.

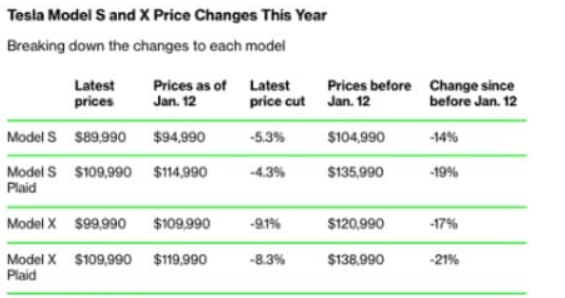

Oilprice.com

Please have a look at the table above. Before January 12, Tesla’s Model X Plaid used to cost $138,990. Now its price is only $109 990. This is Tesla’s most expensive model, and the costs to produce it are also the highest of the whole product range. The prices for other models were also substantially cut.

Obviously, this means that Tesla’s profit margins should fall even lower. The impact of these price cuts on long-term demand still remains to be seen.

The investor’s presentation also signaled that Tesla did not provide specifics about the company’s new models. There is nothing tragic about a conservative company not coming up with new products and outstanding innovations every year, indeed. But in order to compensate for this, it has to be a very stable cash cow to provide real value for its investors. Tesla, however, positions itself as a high-growth company but has not recently come up with any innovations. Instead, a lot has been said about the company’s past achievements.

The industries Tesla operates in

I would rather agree with the thesis that the industries Tesla operates in, namely electric vehicles, energy storage, and artificial intelligence, all have a bright future. After all, the green energy trend is very popular in many countries. Climate-conscious consumers are all of Tesla’s existing and potential customers. However, there are too many unknowns, in my opinion.

The whole electric vehicle market is facing fairly thin profit margins. But it is still quite strange to say that only Tesla would be the one to gain as soon as the whole sector manages to lower the costs and boost the revenues. I know many Tesla fans expect Elon Musk’s company to become the next Apple (AAPL) in terms of profitability and cash reserves. They also say Tesla would maintain its leading market position and become a cash cow. But too many assumptions are made here.

A relatively small proportion of Tesla’s business is indeed devoted to energy storage. Obviously, quite little revenue is generated by this. Although this business division has been showing excellent growth, the company reportedly postponed its solar roof installations. Moreover, in autumn 2022 one of its Megapack batteries caught fire at a power storage site in California.

As concerns Tesla’s artificial intelligence technologies, the company is not monetizing these just yet. It has splendid projects to use AI to cut production costs, but these plans have not come true just yet. Moreover, artificial intelligence technologies are quite new and we cannot accurately predict just how profitable they may be for Tesla. Yet, the valuations take these mega-plans into account.

Macroeconomic risks for Tesla stock

The risks for Tesla stock are obvious, in my view, now when the banking system is not going through its best days. TSLA is a typical glamorous and overvalued stock. It is rising during fair days and is doing bad when the global economy is suffering. The Fed still predicts one more interest hike this year in spite of the whole banking turmoil. All investors, myself included, would not do well in that case. But particularly at risk are companies that are not very profitable. Also, stocks that are overvalued would not do particularly well. The most obvious example is that of TSLA stock. I will explain this in the next section of my article.

Valuations

Tesla’s stock is still overvalued in spite of the fact it is trading sufficiently below its all-time highs.

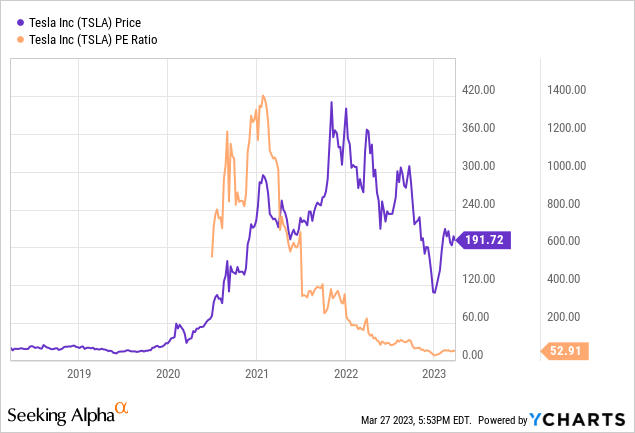

Let’s start with the company’s price-to-earnings (P/E) ratio history.

Sure, compared to what it used to be before, TSLA stock seems to be excellent value for money. But a P/E of 53 is unreasonable, even for a high-tech company with a bright future.

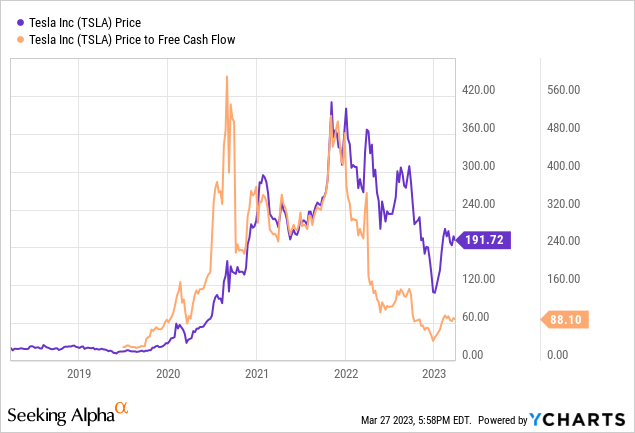

The same is true of the company’s price-to-free cash flow (P/CF) ratio.

The current P/FCF of 88 is extremely high, especially given the fact the company’s cash position has improved.

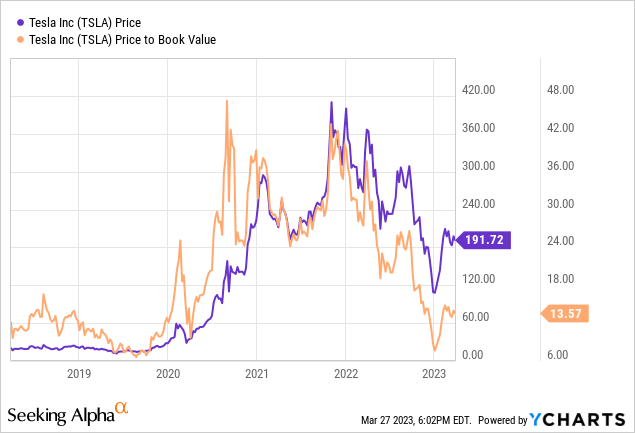

To finish off my valuation analysis, let me also show you Tesla’s price-to-book (P/B) ratio graph.

Just a friendly reminder that a “good” P/B ratio should ideally be between 1 and 3. Tesla’s is almost 14.

So, TSLA is extremely overvalued, especially if we assume a recession is near.

Risks to my thesis

- The first risk is the fact Tesla stock is very popular and many investors seek opportunities to add to their positions.

- The Fed will start easing, thus preventing recession. This is obviously bullish for all companies, not just Tesla.

- Tesla will become the “next Apple” in terms of debt, cash, profitability, and market size. However, it is still a risk to pay so much money for a company that is forced to substantially reduce its profit margins and is facing so much competition.

- After all, the company’s cash position has improved. The revolving credit facility has been extended and Tesla’s credit rating is finally one notch above junk.

- Tesla has some new technologies, including artificial intelligence and smart production innovations. I gave the company credit for these in my previous article.

Conclusion

Overall, Tesla, Inc. is being forced to cut its pricing even for the most luxurious models, which is quite a worrying sign. TSLA stock is overvalued. We might face a recession in the near future, which would mean even more downside for both Tesla’s EV business and its stock price. At the same time, I would not short-sell TSLA stock, either, given Tesla’s cash and debt improvements. So, overall, I remain cautiously bearish on TSLA stock.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.