Summary:

- NIO still has significant growth potential in the medium term as interest from retail and international investors returns to China.

- NIO’s increasing deliveries, improved liquidity, and positive seasonality make it appealing to growth-oriented investors.

- Risks include the uncertain macro environment in China, NIO’s unprofitability and need for capital injections, and the inability to value the stock using conventional methods.

- Despite some risks, I’m sticking to my medium-term speculative “Buy” rating on NIO.

Andy Feng

Investment Thesis

I’ve been covering NIO Inc. (NYSE:NIO) stock for quite a long time here on Seeking Alpha. Since November 2022, I’ve been quite bearish, but then I changed my stance to “Neutral” at the beginning of December 2023 and then issued a “Buy” rating (as a speculative idea) in early March 2024. Unfortunately, my latest bullish thesis hasn’t played out yet, but I still believe I was close to marking the local bottom in NIO’s price. I think NIO still has significant growth potential in the medium term, especially as interest from retail and international investors returns to China.

Why Do I Think So?

I’d like to start from the end of the above paragraph and explain my thesis from the positioning perspective (the increasing interest of various types of investors in China as a region for investment). In the past, I repeatedly wrote in my articles about Alibaba (BABA) and other Chinese stocks that, despite the attractive qualities of the Chinese stock market – the valuation multiples and companies’ ability to generate high free cash flow, among other factors – the Chinese assets were cheap for a reason. This is due to the slowing growth and contraction in the Chinese economy.

The growth that many have written about for decades has significantly slowed down in recent years. As Wall Street Journal wrote in mid-January this year, the global export demand is softening as the global economy is projected to slow this year. In addition, many Chinese families, who suffered for years under the restrictions of the pandemic and received no direct financial support from the government, have become cautious about spending in the face of the weak labor market.

WSJ

However, China managed to exceed expectations with its growth in the last reporting quarter, giving investors renewed hope; it’s possible that the Chinese economy is not as dire as recently believed.

CNBC

The reliability of the statistics from China can be interpreted in various ways. The fact is, however, that according to Bloomberg’s data and the indices it calculates, interest in Chinese assets has increased significantly recently – I found it out from a recent analysis by Richard Excell [Stay Vigilant newsletter]:

Flying right through the improving area and into the leading quadrant are China, commodities, silver, gold, FX carry and the UK.

It looks like many institutional investors, often referred to as “smart money“, have begun to return in large numbers to assets they have recently sold – this repositioning suggests that there is a significant bullish catalyst at play that could further drive and support the current recovery of certain Chinese stocks (at least in the medium term).

In my last article on NIO, I pointed out that most institutional funds have underweighted Chinese equities after their collapse in recent years (meanwhile Europe has been relatively stable and America has grown phenomenally). In my opinion, this creates a more than favorable environment for mid-term growth. After several years of lagging, the Chinese economy is now starting to show signs of recovery (or rather, clearer signs of stability than previously expected). So given the low positioning and the capital flow that has already begun, there is reason to believe that Chinese investments have every chance of outperforming their Western competitors.

Why am I coming back to the NIO stock amid the above background?

In fact, the Chinese stock market has numerous representatives who are undervalued or have unique qualities that are attractive to value investors. However, NIO’s unique catalysts should make it primarily appealing to growth-oriented investors – in combination with the favorable conditions mentioned earlier, these catalysts offer the chance of mid-term recovery.

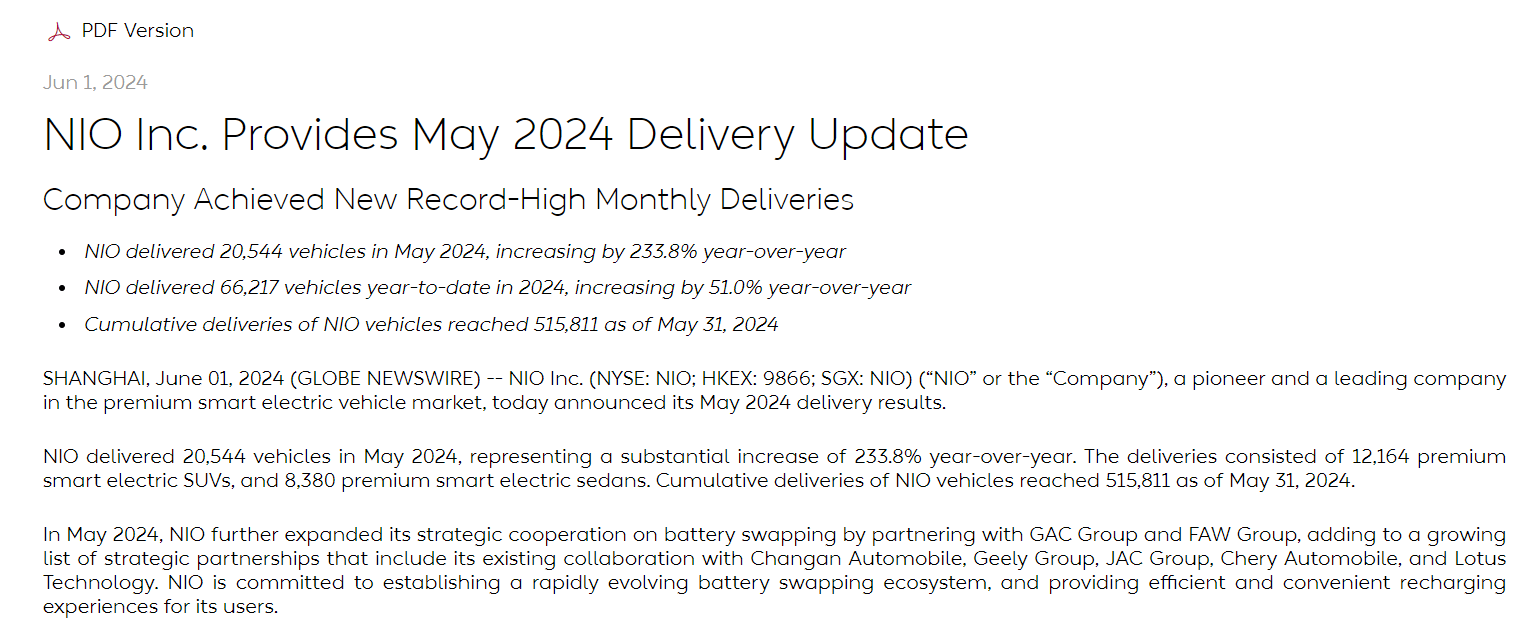

First, NIO continued to increase its deliveries at a phenomenal pace. On June 1, 2024, the company announced that it had achieved a new record of 20,544 vehicle deliveries in May 2024, an increase of 233.8% compared to the previous year – this brings the total deliveries in FY2024 to 66,217 (+51.0% YoY). Cumulatively, NIO has delivered 515,811 vehicles as of May 31, 2024. Deliveries in May included 12,164 premium smart electric SUVs and 8,380 premium smart electric sedans. In addition, NIO has expanded its battery swap partnerships and is now working with GAC Group and FAW Group alongside existing partners such as Changan Automobile and Geely Group (OTCPK:GELYF) to enhance the battery swap ecosystem and charging experience for users.

NIO’s IR materials

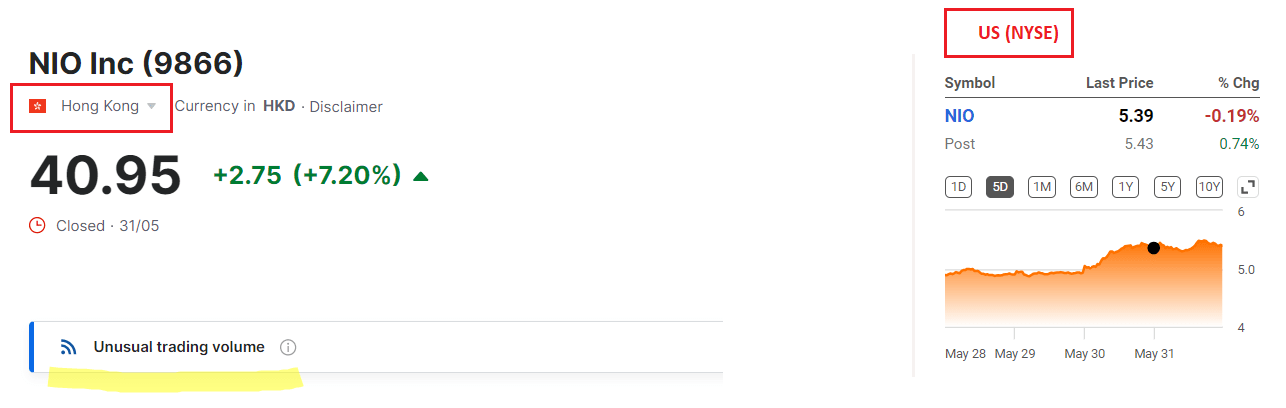

In my opinion, this is a pretty significant achievement, and it was only in anticipation of this news that NIO’s shares in Hong Kong “sharply surged”, as Seeking Alpha News reported before the closing bell on May 31, 2024. But NIO stock only reacted with gains in Hong Kong, while we saw absolutely no reaction on the American market (NYSE).

Seeking Alpha, Investing.com, the author’s compilation

I expect the American market to adjust to Hong Kong and NIO stock will continue to rally to at least match the growth in Hong Kong as the news is already a fact.

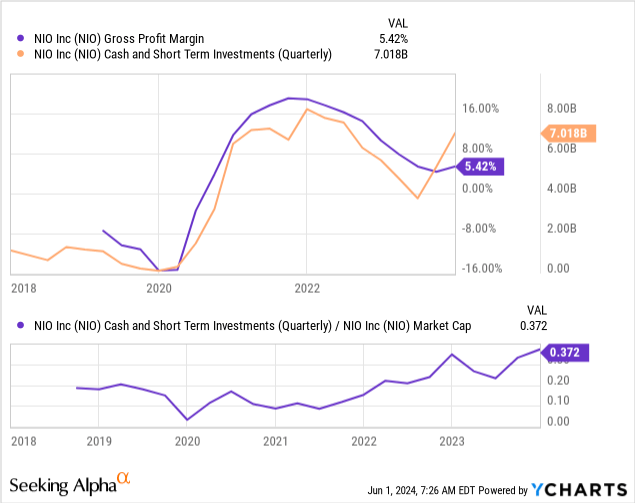

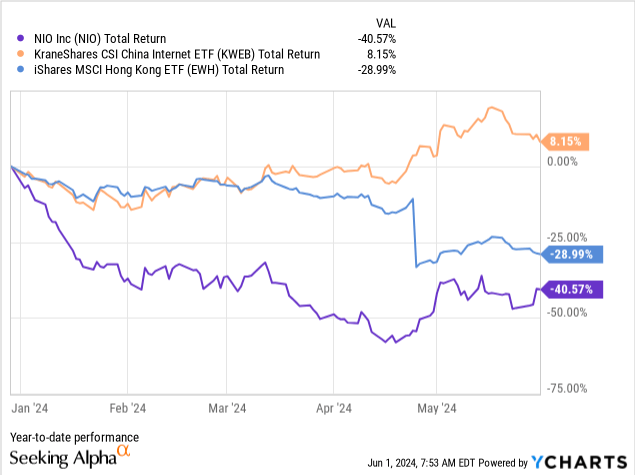

The second point: based on the data from the last quarter, we have seen that the company’s liquidity has improved quite well and the gross margin is showing the first signs of improvement – I have illustrated this graphically below with YCharts.

The cash cushion on the company’s balance sheet is 37.2% of total market capitalization, which is the highest in the company’s history (this is due to the continued decline in the stock amid the rising cash balance). If NIO doesn’t raise additional capital anytime soon, investors won’t be diluted – it should theoretically make NIO a less risky stock from a fundamental perspective. In my opinion, this is an additional incentive for growth that few market participants are talking about today.

Overall, if you examine the company’s current financial position, its assets have never been higher in its public history. As of December 31, 2023, NIO’s total assets exceed $16.5 billion, marking a 17.8% increase from the previous quarter – this amount is ~147.2% of the NIO’s market cap, which is exceptionally high for a growth-focused company. In my subjective opinion, this speaks volumes about the company’s future ability to monetize as the business scales.

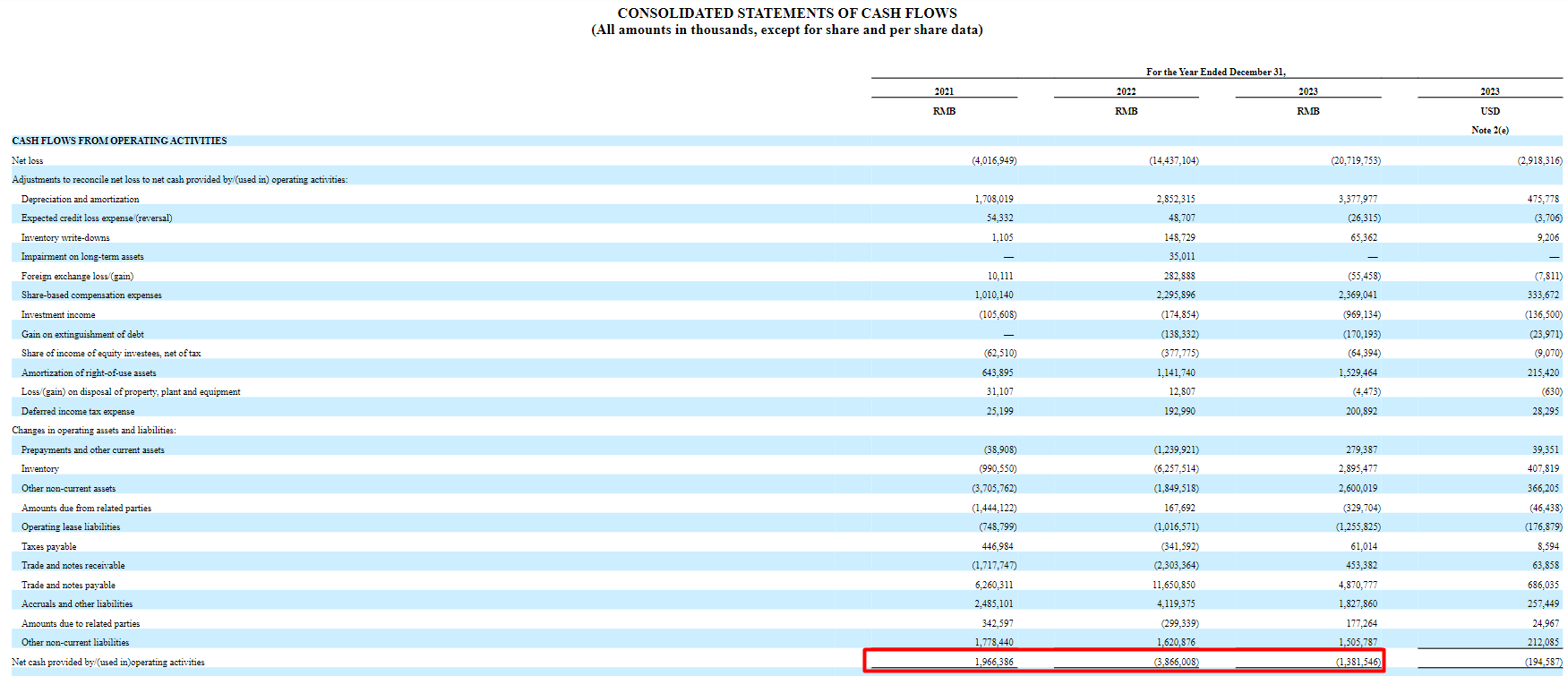

Regarding the trend in operating cash flow, in 2023 the company managed to reduce its cash outflow by nearly threefold – this represents a significant improvement within just one year, in my view:

NIO’s 20-F, the author’s notes added

If NIO can continue this trend, it will serve as an additional fundamental catalyst for a recovery in the stock. As mentioned earlier, the company’s assets already exceed its market cap. The cash on its balance sheet accounts for >30% of its market cap as well. Due to a recent financing round, I see no immediate liquidity issues.

The market is primarily demanding that NIO maintains its business growth rate and becomes cash flow positive, possibly even before it turns a net profit on paper. We’ll see, but I’m more optimistic about NIO’s prospects here than I was just a few months ago.

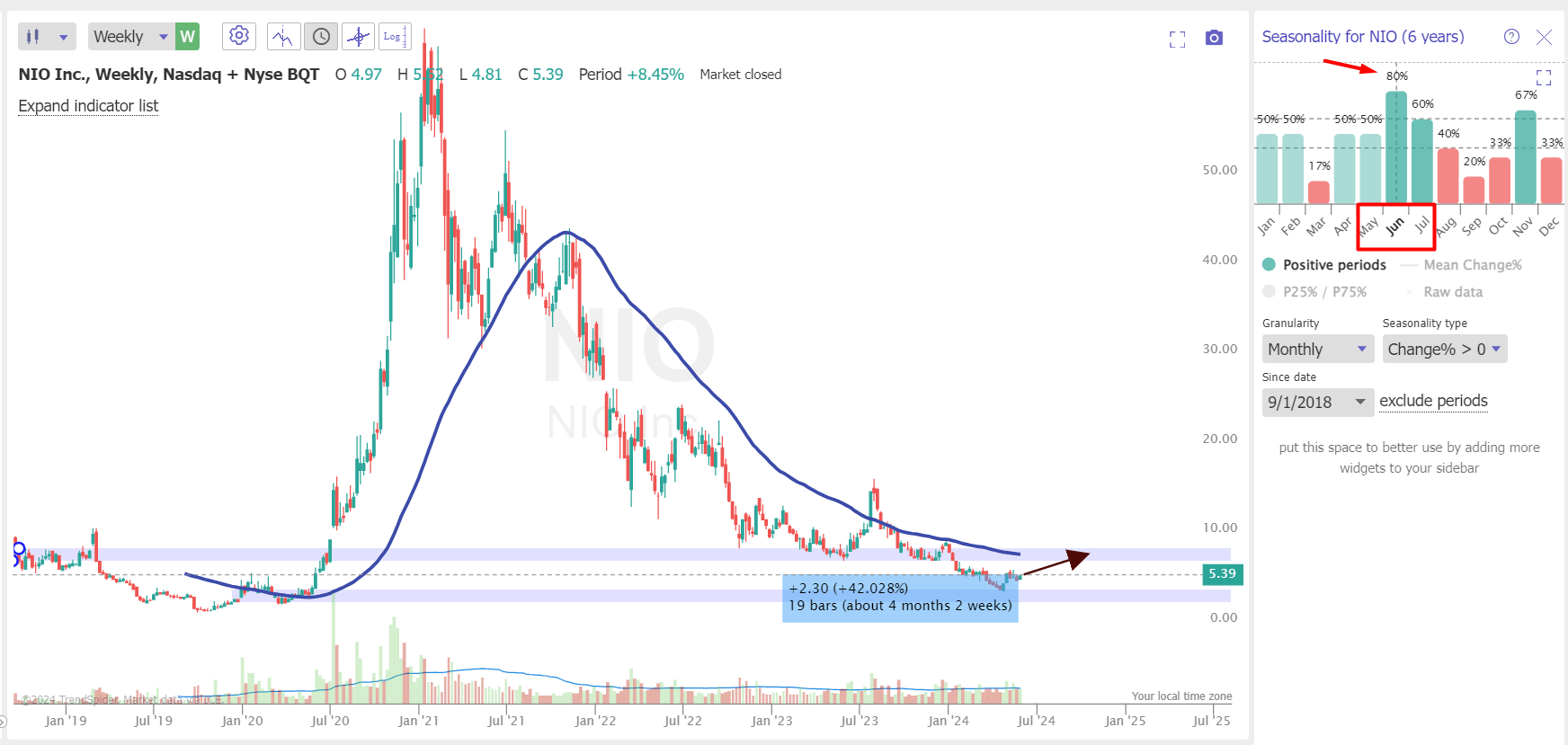

The third reason why I remain relatively bullish in the medium term is seasonality and technicals. Take a look at the chart from TrendSpider below:

TrendSpider Software, NIO weekly, the author’s notes added

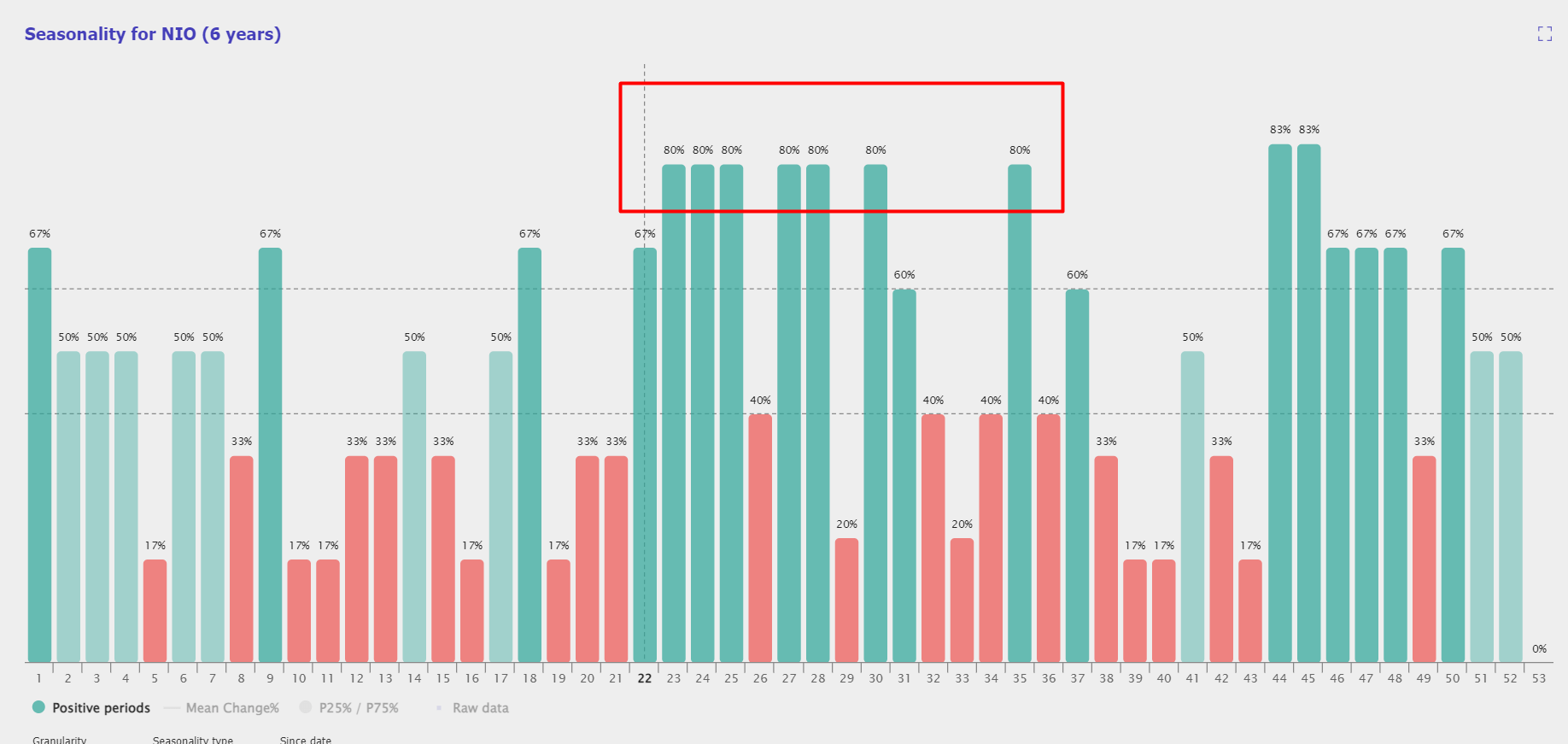

We are now entering the summer, when NIO historically has the highest statistical chance of appreciation so to speak. June is seasonally the best month for NIO stock with an 80% success rate. If we look at more detailed data on seasonality, we see that the next few weeks are statistically likely to be the most successful for NIO of the entire year:

TrendSpider Software, the author’s notes added

Statistics of this kind are not the main strong argument for my thesis. But it fits perfectly with the fundamental and macroeconomic catalysts I outlined above. If we assume that we will see a return to the 52-week moving average in the medium term thanks to the positive factors I see, then NIO can easily gain more than 40% in the summer months.

I think that NIO can’t be valued using conventional methods, as the company has no positive earnings and no EBITDA, and the sales-related multiples are not sufficient to draw a reliable conclusion. Nevertheless, the fact that nearly 40% of capitalization is in cache and deliveries continue to grow significantly year-over-year seems to me to justify a 40%+ growth potential (as indicated by technicals and seasonal data).

Where Can I Be Wrong?

In fact, there are a whole series of risk factors for my thesis – let me touch on the most obvious ones.

First, I assume that the improving macro environment in China, or the expectation that the mortgage crisis there has bottomed out, should lure Western investors back to Chinese assets. But this could be a fallacy as it is by no means certain that a) the crisis is over and China will return to a period of stable GDP growth and b) NIO will be a good pick as it is already lagging far behind the major benchmarks, although it has recently started to catch up.

The second risk lies in my reasoning about improving the fundamentals. NIO remains a deeply unprofitable company that constantly needs new capital injections. There is a risk that the company will quickly “wipe out” any beginnings of recovery growth in its stock quotes by announcing a new share capital issuance – this is a risk I cannot rule out and simply ignore.

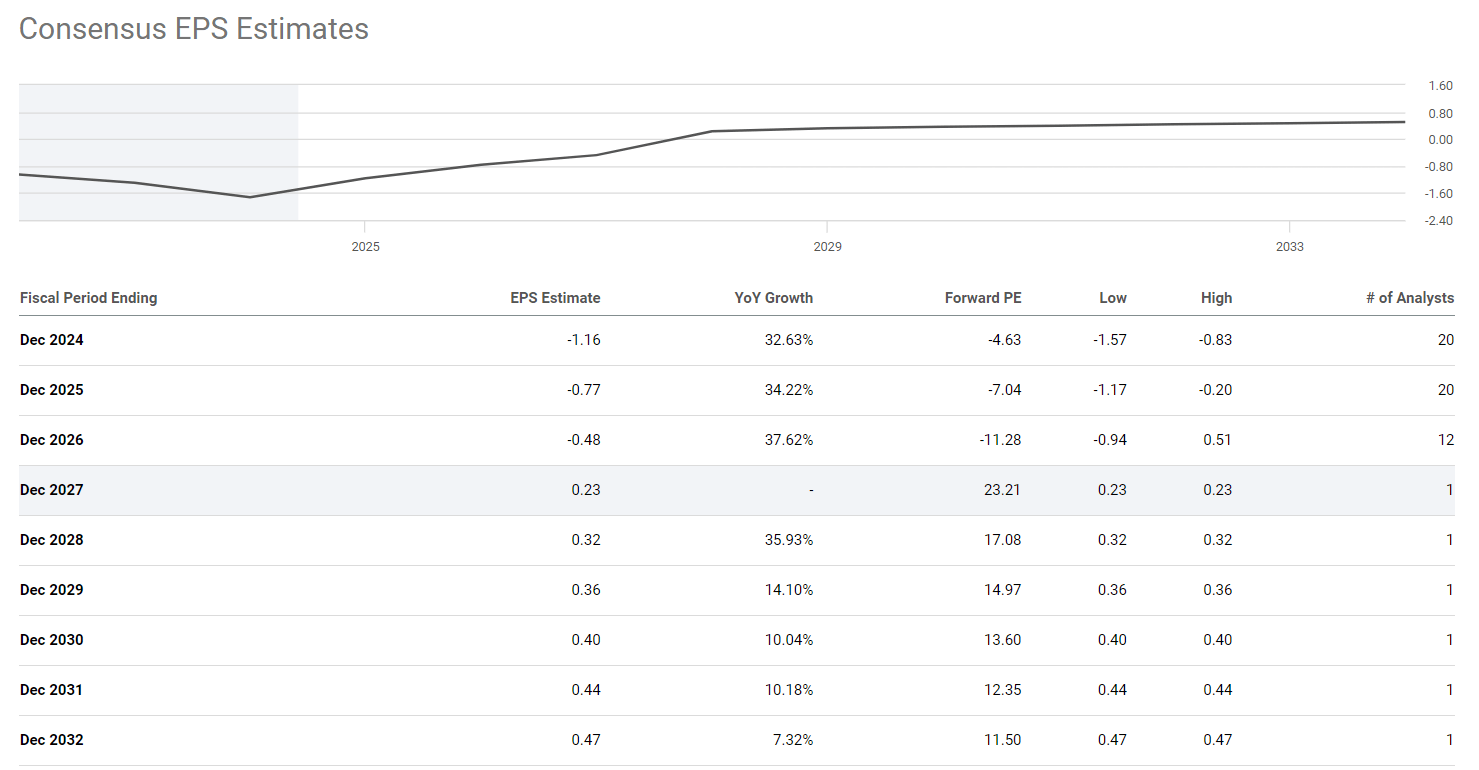

The third risk is that the lack of positive EBITDA does not allow us to value NIO as financial theory recommends. This is a characteristic of a growth stock, but in any case investors will have to wait another 3 financial years before they see the first positive P/E ratios.

Seeking Alpha, NIO

Concluding Thoughts

Given the above risks, I reiterate my belief that NIO today is primarily a speculative idea. Yes, its fundamentals seem to be improving, as does valuation (rising cash-to-market-cap is a good indicator here). But in the longer term, uncertainty remains high. As NIO’s seasonality is very positive and the technicals point to an imminent turnaround, I’m sticking to my medium-term speculative “Buy” rating.

Thank you for reading!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in NIO over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Hold On! Can’t find the equity research you’ve been looking for?

Now you can get access to the latest and highest-quality analysis of recent Wall Street buying and selling ideas with just one subscription to Beyond the Wall Investing! There is a free trial and a special discount of 10% for you. Join us today!