Summary:

- Airbnb exceeds Q1 expectations with doubled net income and 18% revenue growth.

- Q2 revenue guidance falls short due to unfavorable exchange rates, causing a 7% drop in stock price, but core growth strategy remains intact.

- Initiating coverage with a cautious buy based on Airbnb’s healthy financials and strong management team, concerns arise over valuation and ability to navigate the economic cycle.

- My analysis specializes in identifying companies that are experiencing growth at a reasonable price. Rating systems don’t consider time horizons, risk profiles, or investment strategies. My articles aim to inform, not to make decisions.

Thomas Barwick

Investment Thesis

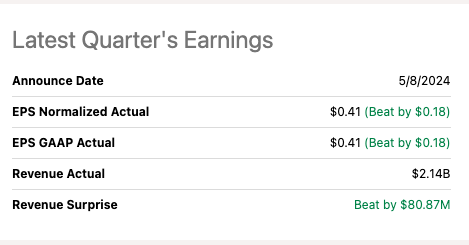

Airbnb (NASDAQ:ABNB) reported a strong quarterly results for the first quarter of 2024, exceeding expectations on both revenue and earnings per share. Net income more than doubled to $264 million, driven by a rise in revenue, which was up 18% to $2.14 billion. Nights and experiences booked also grew 9.5% YoY to $132.6 million, indicating continued strength in travel demand.

Seeking Alpha

Despite positive results, Airbnb forecast for the second quarter fell short of Wall Street expectations. Revenue is expected to be between $2.68 billion and $2.74 billion, which is lower than analysts’ consensus due to unfavorable exchange rates. This news caused Airbnb stock price to drop roughly 7% after the report.

Here is a breakdown of the company latest earnings performance:

- Financials: revenue up 18%, net income up 126%, adjusted EBITDA up 62% YoY

- Growth: Nights and experiences booked increased 9.5%, Gross Booking Value rose 12%, Gross nights booked in non-urban areas grew 10%

- Profitability: adjusted EBITDA margin rose to 20% in Q1, with a full-year target of at least 35%

- Challenges: Lower than expected revenue guidance for Q2 due to currency and Easter timing.

As an investor looking for companies with reasonable growth, Airbnb presents an interesting case. The company is experiencing solid growth in key metrics like bookings and nights booked. However, the recent dip in stock price and the weaker-than-expected revenue forecast for Q2 raise some concerns.

Ellie Mertz, Airbnb CFO, participated in the Bernstein’s Strategic Decision conference at the end of May. In this conference, they discussed Airbnb growth strategy including market expansion and user base growth, service improvements to streamline booking and communication tools, and building a strong host community.

I believe Airbnb’s core growth strategy remains intact and that the recent guidance highlights the potential impact of external factors in the economy like foreign exchange due to the higher interest rates in the US.

While Airbnb’s Q1 results were positive, their Q2 guidance fell short due to currency fluctuations. This underscores the importance of monitoring travel demands and currency impacts on their ability to achieve full-year goals.

I aim to find companies that are growing at a reasonable price and as you will read later, I find ABNB slightly overvalued; however, I believe in ABNB long-term potential. Their strong core strategy positions them for growth, and management’s experience inspires confidence. As the economic climate stabilizes, I expect them to achieve higher growth rates. Therefore, I’m initiating coverage with a cautious buy.

Management Evaluation

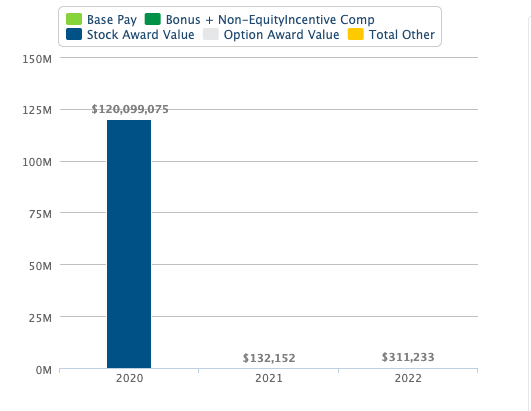

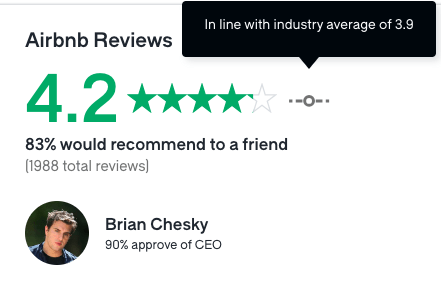

Brian Chesky, the co-founder and CEO of Airbnb, is the mastermind behind the company’s vision and strategy. His leadership has not only translated into strong financial performance for Airbnb, but also has generated positive morale at Airbnb based on Glassdoor reviews. The company itself also boasts industry-leading employee satisfaction ratings. An interesting aspect of Chesky’s compensation package lies in a large stock grant awarded in 2020. This grant, estimated to be worth $1billion over 10 years, ties his financial success directly to the long-term growth of Airbnb. This “high alignment” ratio is a clear sign of Chesky’s commitment to building a sustainable and successful company.

Salary.com

Ellie Mertz, a seasoned Airbnb veteran with eleven years at the company, has been promoted to Chief Financial Officer (CFO). She has taken the reins from Dave Stephenson, who is transitioning to a newly created role as Chief Business Officer in charge of generating growth for Airbnb. Mertz’s extensive experience positions her well; however, Stephenson’s legacy presents a significant challenge to follow. During his tenure as CFO, Stephenson oversaw a period of impressive financial growth for Airbnb, characterized by low debt levels and consistent growth in ROE. Mertz will leverage her deep understanding of the company as she strives to maintain this strong financial performance.

Seeking Alpha

Overall, Airbnb leadership is undergoing a shift. CFO Dave Stephenson transition to Chief Business Officer, focusing on growth with his experience. Mertz, an 11-year veteran, is promoted to CFO. While she inherits a strong legacy of continuous growth, I am confident on Stephenson guidance in his new role. Considering this and his ongoing influence, I am giving Airbnb management a “Meets expectations” until they prove their ability to navigate the current economic cycle.

Glassdoor

Corporate Strategy

Airbnb’s growth strategy is a multi-layered approach. They’re targeting new users in developing regions with growing internet access and middle class, aiming to convert existing users into hosts and expand their property listings. To improve user experience, build trust, and increase growth, they are constantly working to streamline booking and communication. As then new CFO mentioned during the earnings call, they are “optimizing the end-to-end guest flow for our core business” to drive growth:

We made improvements to filters. We’ve made improvements to search input, the search box, making the search box more prominent. So there are quite literally dozens and dozens of improvements that we’ve made. And I see hundreds of basis points of incremental growth just through essentially optimizing the end-to-end guest flow for our core business.

Looking beyond rentals, Airbnb is venturing into experiences and catering to group travel needs. At the core, they’re fostering a strong host community by simplifying the hosting process and offering tools to help hosts succeed. This not only benefits hosts but also keeps the platform attractive with a wider variety of listing for guests.

I have created a table comparing Airbnb current strategy to some of it current competitors in a previous article here, and I’m also updating it here:

|

Expedia (EXPE) |

Booking Holdings (BKNG) |

Airbnb (ABNB) |

Trip.com (TCOM) |

|

|

Market share (Accommodation Bookings) |

15% |

27% |

13% |

10% |

|

Corporate Strategy |

Focuses on bundled travel packages and brand diversification. |

Aggressive global expansion and marketing, focus on maximizing hotel partnerships and become a one-stop for all travel needs. |

Disrupting traditional hospitality with unique stays, expanding to experiences |

Focuses on Asia Pacific market, strong mobile presence, expanding vacation rentals. |

|

Competitive Advantage |

Extensive network of travel suppliers, brand recognition, loyalty program (OneKey) |

Largest online accommodation marketplace, strong mobile presence, efficient marketing. Strong financials. |

Unique lodging options, growing experiences marketplace. Strong financials. |

Strong brand recognition in Asia, competitive pricing, focus on mobile users. |

Source: From companies’ website, presentations, Seeking Alpha

Market share: Statista (2023)

Compared to competitors like Booking and Vrbo, Airbnb focuses on unique, individual listings, fostering a sense of community and local experiences. Booking offers a wider range of traditional hotel options than professional property management listings, and Vrbo has a smaller user base and recently went through platform migration. While all three platforms compete on user experience, pricing, and trust-building measures, Airbnb’s focus on unique experiences and disruption positions them well for specific travelers segments, potentially facing less competition from hotels for shorter stays.

Valuation

Airbnb currently trades at around $146.66, down around -7% since its last reported earnings on May 8th.

To assess its value, I employed an 11% discount rate, this rate reflects the minimum return an investor expects to receive for their investments. Here, I am using a 5% risk-free rate, combined with the additional risk premium for holding stocks versus risk-free investments, I’m using 6% for this risk premium. While this could be further refined, lower or higher, I’m using it as a starting point only to get a gauge for unbiased market expectations.

Then, using a simple 10-year two staged DCF model, I reversed the formula to solve for the high-growth rate, which is the growth in the first stage.

To achieve this, I assumed a terminal growth rate of 4% in the second stage. Predicting growth beyond a 10-year horizon is challenging, but in my experience, a 4% rate reflects a more sustainable long-term trajectory for mature companies that should be close to historical GDP growth. Again, these assumptions can be higher or lower, but from my experience I feel comfortable using a 4% rate as a base case scenario. The formula used is:

$146.66 = (sum^10 FCF (1 + “X”) / 1+r)) + TV (sum^10 FCF (1+g) / (1+r))

Solving for g = 14.5%

This suggests that the market currently prices ABNB FCF to grow at a rate of 14.5%. According to Seeking Alpha analyst consensus, FCF is expected to grow at an 11.43%.

Seeking Alpha

Therefore, I believe that despite ABNB strong earnings report, the stock might be a slightly overvalued. While the recent slowdown in FCF growth is a concern, it’s possible this is due to external factors like FX and the strengthening of the USD because of higher interest rates rather than a fundamental issue with the company’s core strategy. If this is the case, and their core growth strategy remains on track, FCF growth rates should rebound in the future.

Technical Analysis

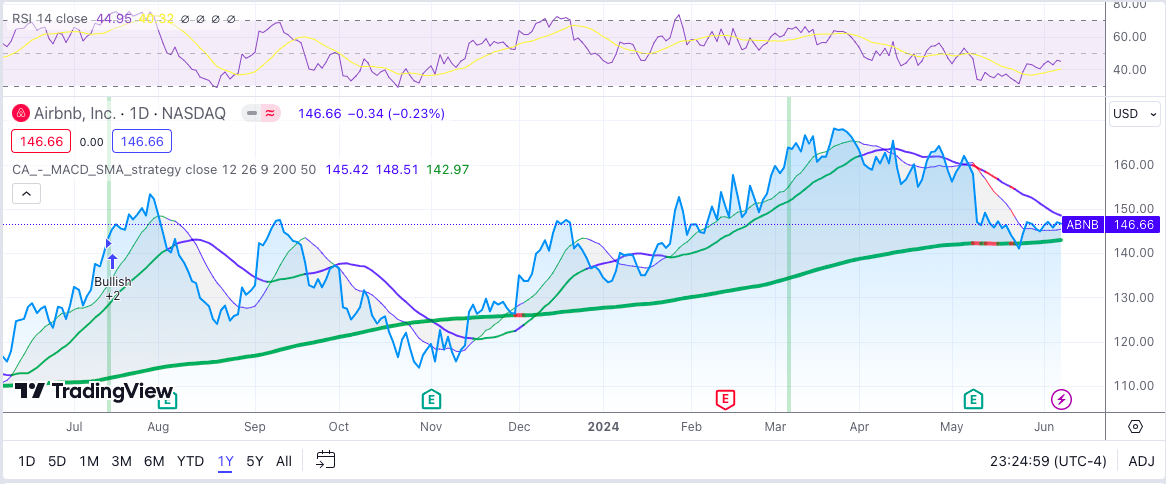

ABNB fell around 10% since its last reported earnings on May 8th. Its RSI is low at around 45, rebounding from oversold territory and having crossed its 14-day moving average of 40 and pointing to keep increasing, indicating that the stock might continue to increase in value.

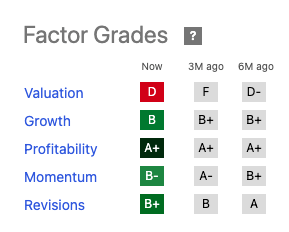

ABNB went public at the end of 2020 and due to the momentum at the time the stock hit its all-time high of $219 in February 2021; however, I consider its next resistance level at around $153; that’s a 5% move. Momentum according to Seeking Alpha is slightly positive:

Seeking Alpha

I believe ABNB should still be able to do well over the long term and that is why I am cautiously optimistic and rating the stock a buy as I will consider the shares on a weakness. I will review my investment thesis as needed.

TradingView

Next earnings are expected August 7th.

Takeaway

Airbnb core strategy of market expansion, user conversion to hosts, and service improvement positions them well for growth. Their diversification into experiences and group travel strengthens their appeal. While recent guidance fell short due to currency fluctuations, their leadership shift with former CFO Dave Stephenson’s ongoing influence inspires confidence. Despite potentially inflated valuations, Airbnb healthy financials, management, and intact core strategy makes it a cautious buy. The economic climate’s impact and the new CFO performance remain factors to monitor, but their core strategy holds long-term promise.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ABNB either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Rating systems don't consider time horizons, risk profiles, or investment strategies. My articles aim to inform, not to make decisions.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.