Summary:

- Algonquin just cut its dividend to common shareholders by 40% for a rightsized 5.4% forward yield.

- This was on the back of interest expenses up 62% year-over-year during its fiscal 2022 fourth quarter and against a total debt position of $7.55 billion.

- Algonquin equity units offer a better way to go long the commons with an interim 13.89% yield on cost.

pedrosala/iStock via Getty Images

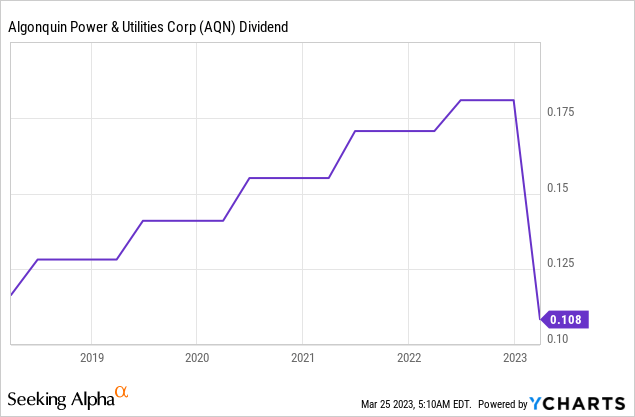

Algonquin Power & Utilities (NYSE:AQN) last declared a quarterly dividend payout of $0.1085 per share, a huge 40% decline from its prior payout for what’s now a 5.4% forward yield. This broke with what has been an uninterrupted record of dividend raises since Algonquin went public on the NYSE in 2016. The Oakville, Ontario-based company had been public on the Toronto Stock Exchange since 1997.

The cut was forced by the still rising Feds funds rate against a net debt position that stood at $7.55 billion as of the end of its last reported fiscal 2022 fourth quarter. This drove interest expenses during the quarter of $81 million, up sequentially from $75 million and from $50 million in the year-ago comp. The previous dividend at $0.1808 per share formed 82% of fourth quarter adjusted net earnings of $0.22 per share. Hence, the company was forced to rightsize its payout against the specter of further 25 basis points rate hikes.

Tangible Book Value And Asset Sales

Whilst a 40% dividend cut for a utility company is material, management stated the move will help them maintain their investment grade BBB credit rating. A move to junk on the back of a deteriorating balance sheet and outsized pay-outs would radically impact their access to affordable debt.

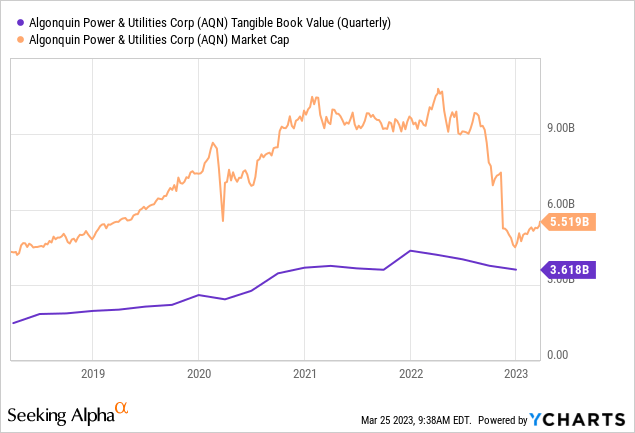

The company’s tangible book value has been declining since the start of 2022 on the back of the marked rise in the Feds funds rate. Tangible book value is critical to protecting the yield and this fell to $3.62 billion during the fourth quarter from $4.37 billion in the year-ago comp. It will be in a state of flux as Algonquin moves to dispose of certain assets to reinforce a balance sheet that held cash and equivalents of $57.6 million as of the end of its fourth quarter. Whilst shares still trade on a premium to tangible book value, this gap has slimmed on the back of the dividend cut.

Algonquin sold its ownership interest in a portfolio of US and Canadian wind farms for cash proceeds of $357.6 million and is targeting $1 billion in additional sales in fiscal 2023 to repay debt and fund opportunistic growth. The company recorded dual beats for its fourth quarter with revenue of $748 million, a 26.4% increase from the year-ago quarter and a beat by $44.46 million on consensus estimates. Non-GAAP EPS of $0.22 beat consensus estimates by $0.02 and was an increase of 5% over the year-ago figure. However, Algonquin expects its 2023 net EPS to be $0.55 to $0.61, this would be significantly below consensus estimates of $0.70 and would be a decline of 13% versus EPS of $0.69 for 2022. Algonquin is in a state of flux but EPS whilst declining remains healthy against the current dividend as we approach the end of the rate hikes.

Chasing Yield With The Equity Units

Algonquin Power & Utilities Equity Units (NYSE:AQNU) offer a $3.875 annual coupon for a 13.89% yield on cost against a $27.90 price per unit. This is around 850 basis points greater than the yield on the commons. The coupon is comprised of two components. The first is a 1/20 ownership interest in a 1.18% senior note. The second is a contractual obligation to convert your equity units to Algonquin’s common shares no later than June 15, 2024. This pays 6.57% to form the aggregate 7.75% coupon rate on the $50 face value of the equity units.

QuantumOnline

Essentially, you’re purchasing a security for $27.90 that will pay you $0.96875 quarterly up until the middle of June next year when your equity units convert to Algonquin’s common shares. This will likely be at a conversion rate of 3.3333 shares per unit with the common shares currently at $8 per share, under the lower $15 per share conversion ratio. This conversion ratio shifts to 2.7778 shares per unit in the now unlikely scenario Algonquin is trading at or greater than $18 per share.

I think this offers a better investment profile than buying the commons with what’s now a quarterly yield of 3.47% paid out for each of the next five quarters until conversion. Total payments of $4.84375 can be expected from now till conversion for an aggregate return of 17.36%. However, this will convert to equity at a price of $8.37 per share, a 4.36% premium to the current market price. Adjusting the expected aggregate return down for this premium still provides a rate of return that is in excess of the yield on the commons to set up the best way to go long Algonquin.

Critically, prospective investors should be aware that they’re locking in $8.37 as a conversion price per share if purchasing the commons now. If the commons declines further then the premium paid to the actual market price next year would increase, the opposite happens if the commons rally. I’m neutral on taking a position in the company but if I did the equity units should offer the most optimal security to do so.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.