Summary:

- Loup Ventures’ Gene Munster came out with guns blazing as he put forward his $250 price target for AAPL.

- However, investors should note that Munster also suggested a $250 PT in an update in January 2022.

- Based on Apple’s FY23 EPS estimates, it would suggest an next-twelve-months earnings multiple of nearly 40x.

- Does it make sense to value AAPL at 40x earnings?

Michael M. Santiago

Apple Inc. (NASDAQ:AAPL) bulls might have breathed a sigh of relief as the Cupertino company’s primary iPhone Pro series contract manufacturer Foxconn (OTCPK:FXCOF), has raised its production capacity to “90% of anticipated peak capacity.” In addition, its manpower staffing has also normalized to 200K, which forebodes well for its Q2CY23 (quarter ending March 2023).

With Apple slated to report its FQ1’23 (quarter ended December 2022) earnings release on February 2, we believe the market has already de-rated it, given the production malaise late last year.

Hence, AAPL bulls could argue that the Tim Cook-led company should be due for a rebound after notching a 1Y total return of more than -30%, underperforming the S&P 500 (SPX) (SPY).

We believe Apple and its manufacturing partners should be accorded significant credit for recovering its production in time for China’s Chinese New Year festivities. Given the supply chain disruptions and COVID resurgence due to its rapid reopening, many businesses have been blindsided. It has also affected the supply chain of its auto industry, including its NEV leader BYD Company (OTCPK:BYDDF).

Hence, CEO Tim Cook’s operational prowess as Apple’s former COO has been tested, even as Apple is expected to continue diversifying its production capacity out of China.

Interestingly, Loup Ventures’ Gene Munster put forth his prediction of AAPL reaching “$250 by next year.” We noted that it had received considerable attention in the Seeking Alpha community and believe it’s appropriate to shed more light on whether his valuation assessment makes sense.

Munster’s optimism is predicated on his view that AAPL’s NTM P/E of 20.4x (10Y average: 17.6x) is too low relative to companies like Coca-Cola (KO), which last traded at an NTM P/E of 25.4x (10Y average: 22.3x).

However, investors need to consider that this isn’t the first time that Munster has proclaimed his AAPL $250 price target (PT). Accordingly, Gene and the Loup team emphasized in a January 2022 note that AAPL should be worth $250, based on “2022 investor euphoria.”

Critically, Loup Ventures projected for AAPL to post FY23 EPS of $7, with an implied earnings multiple of 35x. What was the prognostication based on? Loup Ventures mentioned investors should be excited over the company’s progress in the “metaverse and autonomy,” which we addressed in our previous updates.

But, Munster clarified in his recent commentary, highlighting that he “has not based his current view on the stock on those new categories.”

So, what does that mean? In our assessment, Loup Ventures is likely one of Apple’s most fervent bulls. With the Street’s FY23 consensus EPS estimates of $6.2, Munster’s previous $7 projections suggest a potential outperformance of nearly 13%! But, Does it make sense?

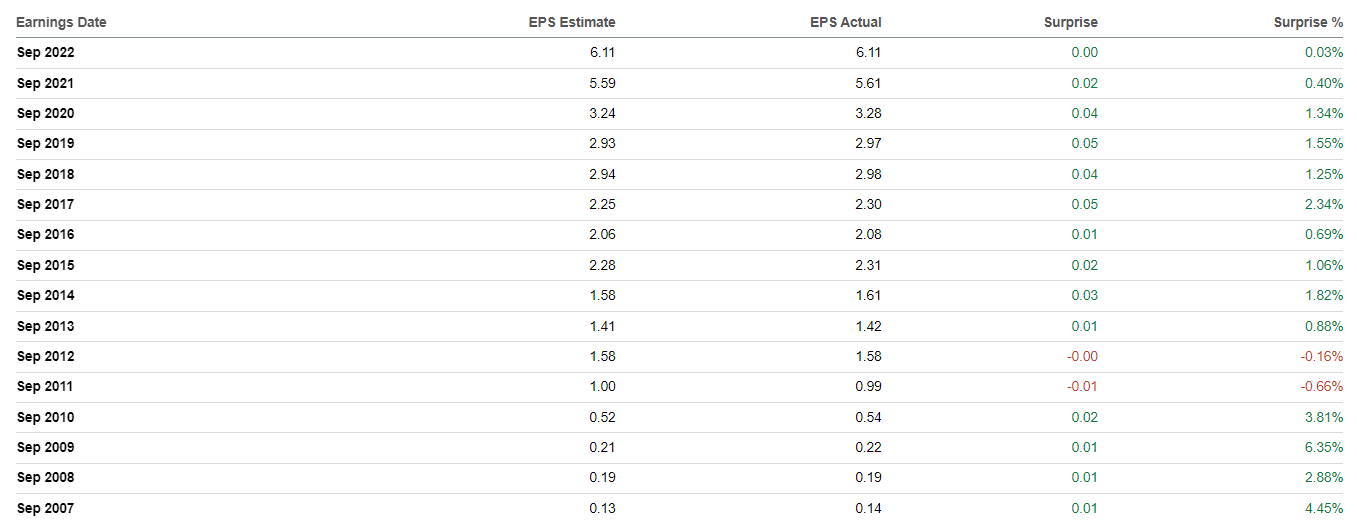

Apple earnings surprise by FY % (Seeking Alpha Premium)

As seen above, Apple has never posted a double-digit earnings surprise since 2007. Moreover, Wall Street average estimates have come pretty close to Apple’s reported EPS figures (within a 2% difference) over the last five FYs.

Accordingly, Apple is projected to report $7.2 in EPS in FY25, suggesting that Munster’s optimism could be overstated.

Notably, the market would need to re-rate AAPL’s earnings multiple to more than 40x to reflect a $250 PT by the end of FY23 (implied upside of about 100%). With AAPL posting a 10Y total return CAGR of 22%, we implore investors not to get overexcited by Loup Ventures’ “bombastic” commentary.

Moreover, what could drive his optimism if Munster is not expecting Apple’s mixed reality device and Apple Car to come to fruition over the next few years?

Investors euphoria? Or another wave of over-optimistic bulls rushing to buy Apple’s deep pullback from its highs in 2022?

AAPL’s overvaluation has significantly dragged its performance, even though it outperformed Amazon (AMZN) and Tesla (TSLA) in 2022. Hence, investors have largely stuck with Apple, believing its execution, brand, and gatekeeper power could continue to lift its buying sentiments, despite tepid revenue growth estimates.

With operations in Foxconn’s Zhengzhou facility likely normalized, investors now need to assess whether China’s consumption recovery could help it to recover or take further share against its Android peers in 2023.

Why does it matter? With Europe likely in a recession and the US potentially heading into one this year, China’s recovery momentum could be critical for Apple.

China accounted for nearly 19% of Apple’s FY22 net revenue. In favor of the bulls, Apple’s market share in China’s premium segment has remained robust. According to a recent report, Apple lifted its market share in China by 1% in 2022 to 22%, despite the consumer spending headwinds.

Therefore, Apple’s stickiness with Chinese premium consumers could see it gain more share as Apple upgrades to TSMC’s (TSM) 3nm process node for iPhone 15. Notably, it could also provide further traction for Apple among its global premium customers as Qualcomm (QCOM), and MediaTek (OTCPK:MDTKF) are reportedly reticent to commit to 3nm production, given the expected weakness in consumer tech spending.

Hence, Apple’s desire and commitment to stay on top of its closest competitors could help extend its lead and protect its pricing leadership. Therefore, we believe suggestions of Apple needing to adjust the pricing for its 2023 iPhone 15 series are likely premature, as Apple’s experience in China has proved. Even in a battered year for the Chinese economy, Chinese consumers have continued to trust Apple’s iPhone as their premium selection.

Hence, the critical question is whether investors consider AAPL’s marked retracement has de-risked its near-term risks. As the market is forward-looking, we believe market operators have likely anticipated a relatively weak FQ1 release, seeing downside risks to the consensus estimates.

But, the critical question is whether there could be demand destruction in FQ2 onward if the global economy continues to weaken. We believe it’s too early to tell, although its iPhone’s structural demand seems robust, as seen in its ability to gain share in China in 2022.

So, we believe the main challenges facing Apple likely aren’t fundamental. Instead, we assessed that AAPL’s relative valuation could continue to hamper its upward recovery if macroeconomic headwinds worsen.

However, a stronger-than-anticipated uplift from an earlier peak in China’s COVID cases (predicted to be in late January) could help Apple to regain momentum faster. As such, there could also be upside surprises to the Street’s estimates, which have likely not reflected a strong recovery.

Hence, while we believe the AAPL’s momentum is still skewed to the downside, its reward/risk seems relatively well-balanced for now. However, if AAPL were to fall further to the $100 levels and get supported robustly, it could be an interesting zone for buyers waiting on the sidelines to ponder.

Rating: Hold (Reiterated)

Disclosure: I/we have a beneficial long position in the shares of TSLA, AMZN either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Do you want to buy only at the right entry points for your growth stocks?

We help you to pick lower-risk entry points, ensuring you are able to capitalize on them with a higher probability of success and profit on their next wave up. Your membership also includes:

-

24/7 access to our model portfolios

-

Daily Tactical Market Analysis to sharpen your market awareness and avoid the emotional rollercoaster

-

Access to all our top stocks and earnings ideas

-

Access to all our charts with specific entry points

-

Real-time chatroom support

-

Real-time buy/sell/hedge alerts

Sign up now for a Risk-Free 14-Day free trial!