Summary:

- Positive news in the early summer gave false hope in Arrival’s performance. It was dashed by reality during Q2 earnings call.

- Manufacturing issues prevailed and made Arrival restructure its business. However, announced “cost-cutting” plans do not decrease losses.

- I believe that the timing of the anticipated equity raise shows that the management is not confident in launching the first vehicles this year.

- I confirm my earlier view that investors should stay away from the stock. Otherwise, their pockets may get burned.

Bet_Noire/iStock via Getty Images

Many of us wanted to believe in Arrival (NASDAQ:ARVL). Its microfactory-based innovative concept was so good that we wanted it to become true. Unfortunately, despite some positive news in 1H 2022, recent company announcements dashed hopes for its revival. The company initiated business reorganisation. But my analysis shows that restructuring efforts do not decrease losses. Additionally, I don’t believe that the management is confident in the vehicle’s launch this year despite recent promises. In this article I will show why you should steer clear of Arrival until its first vehicles arrive.

The Phantom Menace

Despite all the bad news about Arrival, in the early summer there was an impression that the management had firmly gripped the business wheel and started turning the company in the right direction. Just before the Q1 earnings call, Arrival Bus achieved EU certification and received European Whole Vehicle Type Approval. Even some postponement of bus licensing to Q2 from Q1 did not seem critical. At the Q1 earnings call, the company announced that over 70% of certification tests had been completed and Arrival’s production roll-out was on track. It achieved progress with the skateboard platform and managed to assemble the cabin and hoop structure. Moreover, the management promised a successful completion of the licensing test within a quarter. The phantom menace of a vehicle launch seemed to be on the horizon, and the market cheered the positive news. From May 9th to May 13th, stock price increased by 24%. The next month, further positive news came in: the company had started delivering on its promises. On June 21st, Arrival announced the completion of the required functional and safety testing and confirmed its plans to start van production in Q3.

In spite of my skepticism and thoughts in the previous article – Avoid Arrival – Management Needs To Show Some Execution – even I got a new hope for some positive production ramp-up in Q3 and Q4 2022. When I went on a stroll with my dog, my mind was obsessed with last fall’s craziness around Lucid when its first vehicle roll-out was announced. I wondered if history would rhyme and something similar might happen at the market when Arrival starts production. I was aware that the market environment has changed since then; last fall, for example, the inflation was still “transitional.” But the successful production launch remains the successful production launch…

Occasionally, my optimistic hopes were ruined by the reality of Arrival’s performance. On July 12th, the management announced a reorganization of its business, explaining it as a decision to focus on production ramp-up in Q3 2022. To save money, Arrival planned to cut spending and employees by 30%. It was also rumored by Financial Times that Arrival would put a pause on its bus and car roll-out to focus exclusively on van production.

I considered the news positive for two reasons. Based on the analysis in my previous article, it was clear that Arrival would need cash in late 2022. Otherwise, it will lack funds in early 2023. Promised cost savings would have allowed Arrival to launch van production in Q3 in the UK (Bicester) and then in the US (Charlotte in Q4), sit out the negative market sentiment with sufficient cash, and raise equity when the proper time comes. I was even thinking of writing an article sharing my ideas to start a speculative long position. Yes, I still hoped for Lucid-like opportunistic craziness.

The second reason was that Proterra (PTRA), my portfolio company, would win a lot from postponed Arrival plans. Proterra specializes in bus production in the USA, and the alleviation of competitive pressure would be a strong opportunity for it. Besides, we should remember that Proterra’s strongest competitor in the bus sector, Chinese Company BYD (OTCPK:BYDDF), is excluded from state subsidies due to geopolitical tensions between the US and China. It would have been a very strong catalyst for Proterra. You can read more about it in the article Buy Proterra on Arrival’s Downs.

Revenge of the production issues

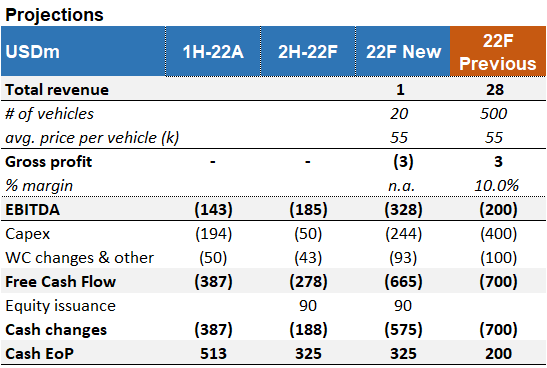

The Q2 earnings call overwhelmed me. The Financial Times was right in saying that Arrival was planning to postpone its bus and car production plans. But Arrival went further, joining the dark side by worsening its outlook. It was announced on the August 11th earnings call that management cut van roll-out to 20 vehicles. The new forecast abandoned Arrival’s July promise of starting production in the third quarter. Moreover, despite production cuts, the EBITDA loss remained incredibly high.

Before we go into details, let us turn to the Q2 earnings call transcript and look at how the management presented the new strategy.

So our capacity is reduced. Like instead of two factories, we do one, and we do this to save cash. […] The second one is actually the supply chain and the — how we’re receiving the parts. […] And the third one is we actually took a very conservative view because originally, we wanted to make, like, many shifts to push the volumes for the end of the year, but we are switching our mode to more preserving the cash, because like anything you do an extreme level, so it just costs more.

We got the note from Arrival that they were cutting down on their production to save on costs. Management assumed that the company lost money with every new vehicle before a certain production threshold was reached. The more cars were produced, the more money was burnt. Therefore, it would be better to produce 20 vehicles than 400. Such a roll-out would be sufficient enough to persuade investors in the credibility of the microfactory concept and would allow Arrival not to burn all of their cash in the “robotic furnace.” I understand such logic and find it the right step. Although microfactories can produce cars on a small scale compared with established car producers, they are still built for 10,000 vehicle production per year. Therefore, a 400 car roll-out would still not be sufficient to cover fixed costs. What surprised me was that such a production cut resulted in the new 2022 forecast implying a much higher EBITDA loss than the outlook provided a couple of months ago.

Author’s analysis

Earlier this year, Arrival expected an EBITDA loss of between $185 million and $225 million for the full year, but recently they projected a $175-195 million EBITDA loss in H2 2022 alone. I would like to repeat the statement because it is of utmost importance: a couple of months ago, Arrival expected to produce 400 vehicles and generate a $200 million EBITDA loss over the year. Now it plans to build 20 cars and generate over $300 million in EBITDA loss. Do we speak about cost savings? What maintains the costs so high? To answer this question, let us have a look at the cost structure.

In 1H 2022, Arrival spent $136 million on administrative expenses, which is almost 70% higher than the previous year. The company provided the following explanation:

The increase was driven by provisions for obsolete inventory (USD 14.9 million) and related purchase commitment penalties (USD 7.3 million), share based payment expenses related to new programs (USD 9.1 million), asset write-offs and other expenses related to our move from our Russia location and increased wage (USD 3.3 million), travel (USD 1.8 million) and consultative spend (USD 18.9 million) as the company readies for start of production.

$22 million were spent on inventory and other purchases that were no longer required for the manufacturing. I understood it in that way that Arrival ordered some parts that became unnecessary due to changes in the production process. Then the company spent $9 million on new programs. I expect these costs to go down in the 2nd half as the new programs were abandoned. Spending on consulting services for the production launch was the largest category explaining the increase. The key question is whether or not consulting services will be further required. Before we answer this, let me estimate which costs the production itself will incur.

Certainly, some vehicle roll-out in the 2nd half of the year would increase costs compared with the 1st half, but how much money does the production of 20 vehicles require? As Arrival uses innovative microfactory concept, it is challenging to estimate expenses precisely. But we can get an upper bound of the costs benchmarking Arrival against EV peers. For example, Rivian (RIVN) spent $243,000 COGs per vehicle in Q2-22, while its factory was utilized for 13%. If we take this figure as a conservative estimate, then COGs for production of 20 vans by Arrival would be around $4-5 million. Thus, the share of manufacturing costs will be minor in $200 million costs expected in the second year-half.

Therefore, the only explanation behind such high full-year costs is that expenses for an obsolete inventory and consulting spend will continue to be extremely high. I believe the company still needs money to adapt its manufacturing process before the first vehicles can be rolled out.

Arrival did not provide any update on the manufacturing progress in a Q2 earnings call. I guess there was just no good news to share. It seems to me that until mid-July, management still hoped to overcome the issues and therefore stuck to the expected production launch in Q3. Unfortunately, they did not solve these problems and therefore had to increase spending on calibrating the manufacturing process. Furthermore, I believe management is still not confident in the provided timeline and would like to get hedged in case of further delays. Let me explain how I’ve come to this conclusion.

ATM platform

At the Q2 earnings call, John Wozniak, Chief Financial Officer, stated that they established a $300 million ATM platform (ATM stands for at-the-market offering) to raise money.

Turning to our outlook. We ended Q2 with approximately $513 million of cash and cash equivalents, […] and today are establishing a $300 million ATM platform to sell equity into the market from time to time.

On Arrival’s website, it is said that this equity raise will be done in two steps:

Arrival expects to end the year with approximately $300-350 million of cash, inclusive of expected proceeds from the ATM proceeds of approximately $90 million this year and $210 million in 2023.

Let’s find out what an ATM platform means and if it is beneficial for Arrival. As the name suggests, an at-the-market offering allows a public company to raise modest amounts of capital over time by offering securities to the market. It gives flexibility to the company and allows it to raise money at the most attractive timing. ATM programs generally also have lower commissions and associated fees than offerings organised by investment banks (underwritten offerings). For example, less management involvement in the sale process is required. There are no special marketing events, known as road shows.

I would assume that Arrival could try to allocate securities among retail investors because small tranches are not usually sought by institutional investors. What puzzles me is the issuance timing. Arrival would like to get $90m proceeds still this year, meaning before the vehicle launch. Why would you issue equity when the sentiment about the company is so negative? Why not produce vehicles and raise equity leveraging on the positive news? I believe such a strategy would be wise if you do not believe in the vehicle launch and would like to get hedged for the bad news. The decision would ensure the company remains safe from even the worst possible outcome. Arrival’s inability to produce vehicles this year, amplified by the strapped cash, would mean a bankruptcy scenario for Arrival.

Valuation

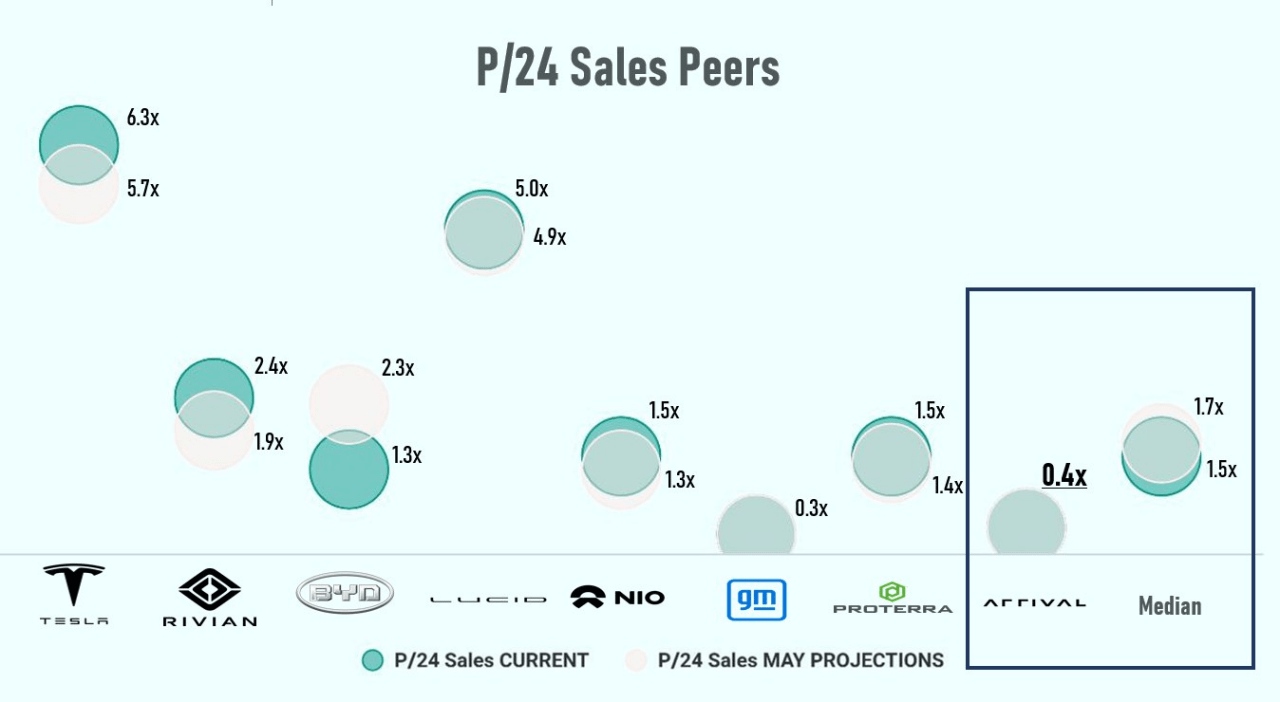

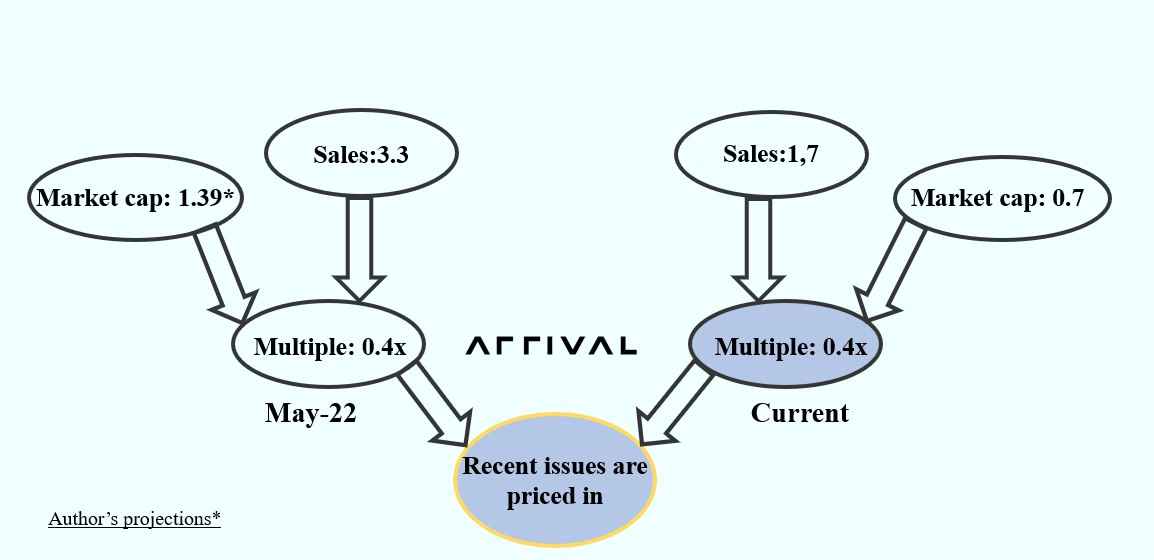

As for valuation, I will use the same peer group for Arrival I used in my previous articles and will rely on price to expected 2024 sales metrics for benchmarking. Arrival’s discount to the peer group average remained at about 75%, similar as in May.

Seeking Alpha, prepared by author

Although the company’s market capitalization halved over this time, its projected 2024 sales also halved. It resulted in a flat multiple. It is difficult to say if we should consider 0.4x or the peer average multiple as the basis for fair value. I believe it does not play a big role because it depends on 2024 sales that are barely unpredictable. A lot will depend on the successful vehicle roll-out this year and the liquidity situation over the next year.

Seeking Alpha. Prepared by author

Bulls say

Bulls may say that Arrival has already gone through its lowest point and all the issues it had suffered from are finally factored in the stock price. The business will be able to proceed and develop in line with its management promises. When putting this change into perspective, Arrival could benefit from its new cost structure and profit from its planned 30% savings. The ATM investment would help Arrival attract sufficient cash and accelerate production in the UK and the USA after a successful vehicle launch in Q4.

Conclusion

Although Arrival has already faced a lot of difficulties recently, I believe that there is a high probability that more negative news is to come. Announced cost cutting plans do not allow Arrival to reach a smaller EBITDA loss. Furthermore, the announced equity raise before the first vehicle roll-out worries me about the probable success of the production launch this year. So do I. The dark side clouds everything. Impossible to see the future.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.