Summary:

- BOX’s guidance was a little light, causing a sell-off in the stock.

- The company’s Suite strategy is working, but the macro backdrop is difficult.

- I’d stay on the sidelines for now and look for a better entry point later.

ronstik/iStock via Getty Images

Box, Inc. (NYSE:BOX) has done a nice job transforming its business over the years and its Suite strategy is paying off. However, the stock looks appropriately priced against a difficult macro environment from which it is not immune.

Company Profile

BOX is a cloud content management platform that allows customers to securely manage the entire content lifecycle, from the moment a file is created to when it’s shared, edited, published, approved, signed, classified, and retained. The content can be uploaded and accessed from anywhere on any device with both internal and external partners.

The company also offers offer more than 1,500 pre-built integrations with multiple partners including Microsoft, IBM, Salesforce.com, Apple, Google, Slack, Adobe, Palo Alto Networks, Okta, and Zoom, among others. The Box Platform also allows IT teams and third-party developers to extend the power of Box across their applications and build custom content experiences.

In the fall, the company announced a number of collaboration tools, including Box Canvas and Content Insights. Canvas is a virtual whiteboard, while Content Insights allows users to understand how the content is being consumed, how often, how much, which days, and by whom.

Earlier, Box got into the e-signature space with Box Sign. The product comes from its acquisition of SignRequest in 2021.

The company has been focused on building out multiple products and then bundling the entire platform in a suite. In Q4, over 90% of its suite sale in large deals was from its latest offering called Enterprise Suite.

Discussing its Suite strategy last fall at the Citi Global Tech Conference, CEO Aaron Levie said:

On the go-to-market front, we took the multiproduct platform expansion that we drove and really simplified how we brought that platform to our customers. So that was really our Suites strategy. So instead of going to customers and saying, “Would you like to buy Box plus our governance module or plus our advanced security module,” we now go in and say, “Would you like to buy the full Box platform that will do everything from security, workflow, collaboration, e-signature, all in a single bundle, and again, kind of meaningfully more cost-effective than buying those solutions separately from different vendors?”

The company sells its service as subscription, with fees based on things like the number of users and functionality deployed. Contracts are generally for one year, but can be for as little as one month up to three years.

Quarterly Results

For the quarter, BOX recorded revenue of $256.5 million, up 10% year over year. On a constant currency basis, revenue was up 15%

Billings rose 6% to $357.1 million, while remaining performance obligations at the end of January were $1.25 billion, a 16% increase versus last year.

Adjusted gross margins came in at 78.5%, up 340 basis points. The company credited “continued efficiencies from our infrastructure strategy and the impact of higher price per seat due to strong suites adoption” for the improvement.

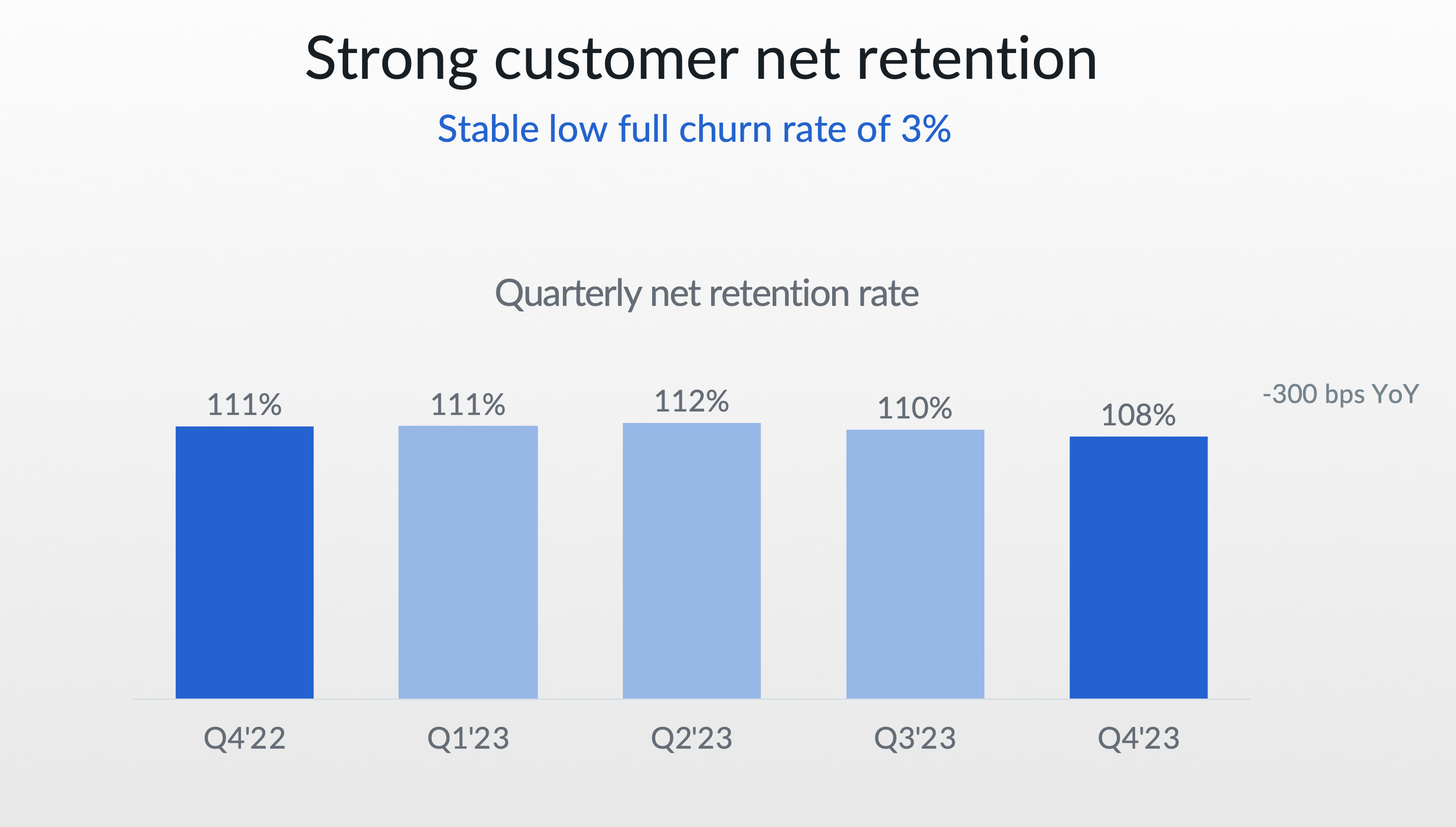

Customer net retention was a 108% for the quarter. The company said the number was pressured by lower customer headcount and more budget scrutiny.

Company Presentation

The company generated $74.7 million in free cash flow in the quarter, and $238.4 million for fiscal 2023.

In Q4, BOX repurchased 300,000 shares for approximately $9 million. For the full year, it bought back 10.2 million shares for approximately $267 million.

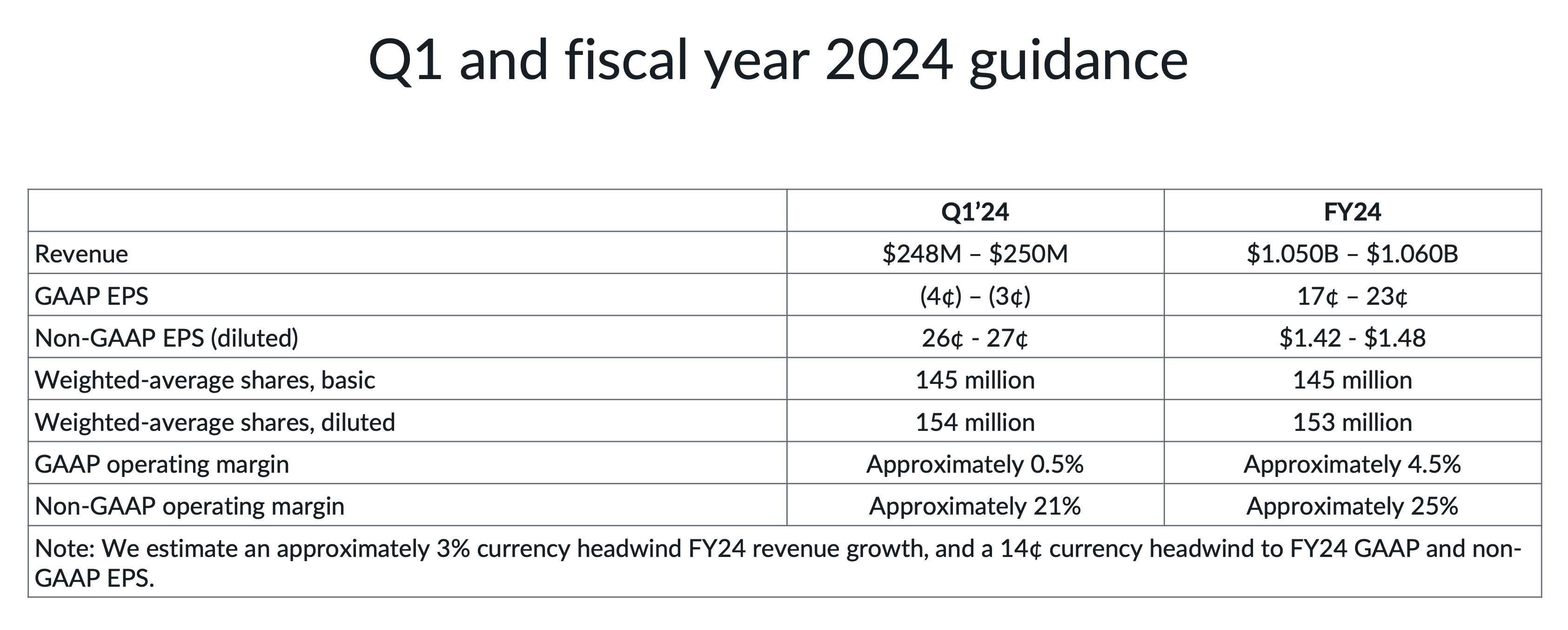

Looking ahead, the company guided for F24 full-year revenue of between $1.05-$1.06 billion and adjusted EPS of between $1.42-$1.48. Analysts were looking for revenue of $1.08 billion and EPS of $1.45. For FQ1, the company forecast revenue of between $248-$250 million with EPS of 26-27 cents. Analysts were looking for revenue of $256 million and EPS of 27 cents.

Company Presentation

On its earnings call, CFO Dylan Smith said, “With respect to our FY ’24 expectations, we have factored in the current macroeconomic challenges into our guidance and our current expectations are for this environment to persist throughout FY ’24.”

Opportunities

If you haven’t followed BOX in a while, you might remember it simply as a cloud storage and content sharing company. That is no longer the case, as the company now brings to the table a full suite of content management, collaboration, e-signature, governance, and security features. The company has done a great job of transforming the business since it went public, and innovation should continue to be a driver.

BOX Original Product (BOX S-1)

The company has also transformed its go-to-market strategy as well. When it IPO’d it used to a freemium model where after users hit a limit they would be prompted to upgrade. These free users were a drag on margins. At the time of its IPO, it has 32 million users but only 44,000 paying clients. Today, the company uses a direct sales force that is selling a much more comprehensive product suite, and free user costs as a percentage of revenue are minimal.

Suite deals are now the company’s bread and butter, and it had a 72% attach rate in Q4, while about 46% of its revenue came from suite subscriptions. The company is selling more and more large subscription suite deals, and it had nearly 1,650 customers with $100,000 or greater contract values at the end of FY23.

Discussing Suite penetration on its earnings call, Smith said:

So that’s an area that we have been very pleased with the momentum. So certainly, kind of Suites adoption where we are at the moment is ahead of what we had expected a year ago. So certainly, from a timing standpoint, we would expect to reach that kind of 50% plus milestone sooner than we thought a year ago, and we’ll certainly provide more details as we get into the longer term thinking at our Analyst Day. And then in terms of where we see Suites headed, as optimistic as ever that steady state the significant majority of our revenue is going to be coming from Suites customers.”

Risks

Even SaaS companies like BOX are not immune to a weakening economy. For one, potential customers are being much more diligent and deliberate with regards to their tech spending. In a more cautious macro environment, an offering’s ROI needs to be much clearer. As such, decisions can often take longer and contracts initially be smaller.

In fact, the company added new language in its 10-Q Risk Factors during Q3, adding: “During the third quarter of our fiscal year 2023, we began to see an impact from additional customer scrutiny being placed on larger deals due to the economic environment.”

Tech and other companies have also been reducing their workforces. Given that fees are often tied to the number of users of a product, less employees can lead to lower fees when it comes time for renewal. The tech industry has been the first industry to really start reducing headcount, but you are also starting to see it in other sectors, such as financials.

Valuation

SaaS companies are generally valued based on a sales multiple given their high gross margins and the companies wanting to pump money back into sales and marketing to grow.

On that front, BOX is valued at a EV/S ratio of about 4.5x based on its FY 24 (ending January) guidance after its earnings sell-off. Based on the FY25 sales consensus of $1.2 billion, it trades at a EV/S multiple of 4x.

By comparison, Dropbox (DBX) trades at a 3.5x EV/S ratio, although it is growing revenue slightly more slowly.

Conclusion

BOX shares were down about -14% intraday on its earnings report, as its results and guidance failed to impress investors. Results were mostly in line, while guidance was a bit light.

On the positive front, the Suite strategy is working, and driving its results. The attach rate is high, and the penetration is coming in ahead of initial projections. However, the macro is tough, and companies are just being more frugal and laying off workers, which isn’t a great environment for much of SaaS.

The current sales multiple for the stock, meanwhile, seems pretty reasonable given its expected growth in a difficult market. I like the transformation the company has undergone, and would continue to watch the name for a potential entry point.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.