Summary:

- Samsung Electronics has moved to begin to “meaningfully” cut chip production, combined with an optimistic outlook of demand for PCs and Smartphones.

- SK Hynix, Micron, Western Digital, and Kioxia had already begun cutting production.

- The move by all companies to curtail production to reduce high inventory and adjust production depending on demand, fueled hopes for a memory chip industry recover in the 2H.

DNY59

Major memory companies have now announced their CY first quarter earnings. All have echoed that they are making concerted efforts to cut production, signaling the possibility that prices of DRAM and NAND will end their decline.

In this article, I present the latest data supplied by Micron (NASDAQ:MU), Samsung Electronics (OTCPK:SSNLF), and SK Hynix (OTC:HXSCL) and provide my analysis of the industry in 2023.

Micron

Micron announced in November 2022 that in response to market conditions, the company is reducing DRAM and NAND wafer starts by approximately 20% versus fiscal fourth quarter 2022. These reductions will be made across all technology nodes where Micron has meaningful output.

In fact, during Micron’s recent fiscal Q2 2023 earnings call, Micron stated that it expects industry bit supply growth for DRAM and NAND in calendar 2023 will be below demand growth, which will help improve supplier inventories as supply demand balance is expected to gradually improve.

For calendar 2023, Micron expects industry demand growth in the low-teens percentage in NAND. Micron reported data center customer inventories should reach relatively healthy levels by the end of calendar 2023.

Micron’s expectations for calendar 2023 industry bit demand growth have moderated to approximately 5% in DRAM and low-teens percentage range in NAND, which are well below the expected long-term CAGR of mid-teens percentage range in DRAM and low 20s percentage range in NAND. The reduction in calendar 2023 demand is due to a degradation in end market demand. Micron expects that improving customer inventories will support sequential bit demand growth for DRAM and NAND through the calendar year. China’s reopening is also a positive factor for calendar 2023 bit demand.

Samsung Electronics

Q1 2023

Samsung Electronics reported Q1 2023 Revenue of KRW 63.75T (-18.0% YoY). Deteriorating earnings at the memory division due to industry slowdown was the main culprit behind the large-scale decline in overall profits.

DRAM shipments fell 11% QoQ and ASP grew -14% QoQ, reflecting the slowdown in demand for server and storage applications. The demand sluggishness is linked with reduced enterprise IT spending.

In the case of DRAM, the focus has been on preparing for the mass production of D1b products based on EUV lithography and that preparation for mass production is almost at the completion phase. This year, Samsung is planning to go to mass production within the year with the D1b based 32-gigabit DDR5 product to try to lead the industry. NAND shipments climbed 3% QoQ and ASP grew -18% QoQ.

Q2 2023

Samsung’s sluggish earnings are expected to continue into 2Q 2023, with DRAM ASP to slide 7% QoQ. NAND ASP are projected to fall 8% QoQ.

A demand recovery is likely to be limited by conservative investments, mainly from hyperscalers, and continued inventory adjustments by customers. Memory inventory should also turn to decline after peaking in 2Q 2023.

- For mobile and PC, set build demand is expected to improve with the launch of new smartphones and PC promotions; and the shift towards high-density trends based on price elasticity is likely to continue.

- For server, content-per-box is projected to grow as the transition to high-core CPUs will accelerate. In 2H23, hyperscaler investment should resume, given rising peak utilization rates at data centers.

SK Hynix

Q1 2023

SK Hynix posted an operating loss of KRW3.4tr on sales of KRW5.1tr (-34% QoQ) for 1Q23.

DRAM bit growth continued on a downtrend, but demand for high-capacity products such as high bandwidth memory (“HBM”) chips remained solid. DRAM shipments slipped 20% QoQ and ASP fell 19% QoQ.

SK will invest for mass production readiness of 1b nanometer DRAM fabricated at the 10nm node.

SK will also invest for mass production of 238-layer NAND. NAND shipments for Q1 2023 slid 15% QoQ and ASP dropped 10% QoQ. The company expects hyperscaler data center investment continued to drop, and smartphone and PC sales remained sluggish.

In Q1, NAND shipments slid 15% QoQ and ASP dropped 10% QoQ. The declines in shipments and ASP were below the industry averages thanks to the firm’s preemptive output cuts and inventory strategy. In 1Q23, North American hyperscalers’ data center investment continued to drop, and smartphone and PC sales remained sluggish.

Q2 2023

For Q2 2023, I forecast DRAM shipment growth of +11% QoQ and ASP a growth of -7% QoQ, and NAND shipment growth of +10% QoQ and ASP growth of -8% QoQ.

SK Hynix expected bit growth in the second quarter to offset the drop in the first quarter of double digits. The company cited the change in customer purchase patterns, where some customers are buying more chips in the second quarter in preparation of market recovery during the second half of the year. SK Hynix was also receiving customer queries on whether memory chip prices will increase after hitting bottom.

DRAM

Table 1 shows DRAM metrics for Micron, Samsung Electronics, and SK Hynix.

The Information Network

Chart 1 shows DRAM bit shipments from Q1 2016 – Q1 2023, illustrating that MU is outperforming competitors.

The Information Network

Chart 1

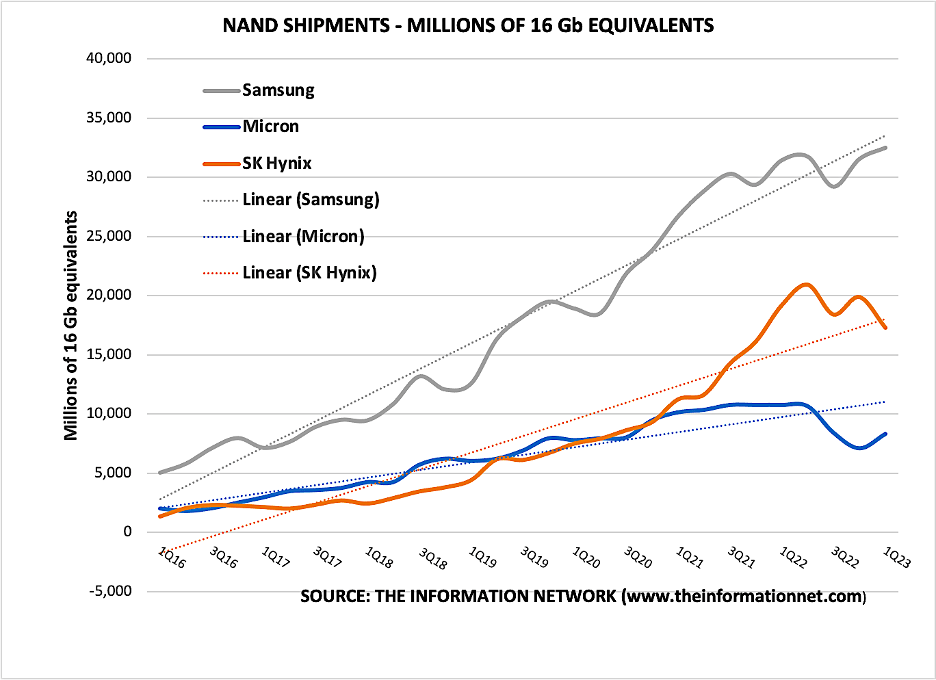

NAND

Table 2 shows NAND metrics for Micron, Samsung Electronics, and SK Hynix.

The Information Network

Chart 2 shows NAND bit shipments from Q1 2016 – Q1 2023, illustrating that MU is outperforming competitors.

The Information Network

Chart 2

Investor Takeaway

I noted in my March 7, 2023 Seeking Alpha article entitled “Micron: A Bad 2022, A Dire 2023, A Positive 2024,” that recovery in memory won’t start until CY Q3 2023 (Micron’s fiscal Q4 2023). According to that thesis, Micron is still two quarters away from improved financial metrics.

Consumer electronics products PCs and Smartphones have shown minimal improvement in demand with the opening of China. Unfortunately, end-user inventory work downs have worsened for hyperscaler companies, along with continuing inventory work downs for PCs and smartphones.

Inventories at fabrication plants also appear to be rising despite production cuts across the industry. These poor fundamentals are not only weighing on the company’s second quarter results, but also create further meaningful ASP and margin degradation in fiscal Q3.

Chart 3 shows quarterly unit shipments for Smartphones (blue bar) and PCs (orange bar) from Q1 2022 to Q4 2024. Here we can see that shipments will reach a low in Q2 2023 and begin showing positive QoQ growth in Q3 2023. These data are according to our report entitled Hot ICs: A Market Analysis of Artificial Intelligence (AI), 5G, Automotive, and Memory Chips.

The Information Network

Chart 3

Metrics and responses provided by Samsung and SK Hynix in the past week corroborate my thesis quoted above.

I rate MU a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

This free article presents my analysis of this semiconductor sector. A more detailed analysis is available on my Marketplace newsletter site Semiconductor Deep Dive. You can learn more about it here.