Summary:

- Wall Street keeps assigning Google buy ratings with price targets as high as $160.0 per share and investors continue buying long-awaited dips despite the ongoing fall of the stock price.

- The company’s financials are also very strong, with a significant amount of cash on hand, high margins, and high ROE and ROIC.

- Google has several competitive advantages that have allowed it to become one of the most successful companies in the world.

- Nobody knows how the market will price the stock in the near term. There might be a better buying opportunity. However, Google stock is in the range which starts being compelling for investors focused on value.

Sean Gallup/Getty Images News

What Really Matters?

Alphabet (NASDAQ:GOOG)(NASDAQ:GOOGL) has been the name to own for many investors just lately. The stock rebounded with the broad market from the pandemic lows and buyers kept bidding and sending the stock price to new highs. However, the overall sentiment started deteriorating over a year ago. Since then Google’s share price has fallen ~40%. After infamous massive layoffs broadly covered by media, a rising competitor in a form of ChatGPT, and the most recent lower quarterly profit the environment around the company has substantially worsened. Nevertheless, Wall Street keeps assigning buy ratings with price targets as high as $160.0 per share and investors continue buying long-awaited dips despite the ongoing fall of the stock price. Is there more pain and a bleak future ahead or is it an investment opportunity of a lifetime?

The article focuses on the business and its long-term outlook. It’s not another piece dissecting various scenarios of how ChatGPT will disrupt Google’s business. The subject has been discussed in detail in the financial space. Yet, the development and outcome of the rivalry are completely unpredictable. What really matters is the fundamentals of Google’s business, its financial health, moat, growth, and associated risk. An assessment of these aspects together with conservative projections applied to a valuation model should result in a fair value for the company. It shall also give the reader an answer if Google is a business worth buying today for the current price from a risk-reward perspective.

Will A Recession Harm Google?

Multiple metrics are suggesting an upcoming recession. Investors are positioning themselves for a challenging time by adjusting their portfolios. It seems like Google was thrown into the basket together with risky, frequently unprofitable companies that can get seriously hit by an economic slowdown. However, it shouldn’t be the case for the advertisement giant. A recession can have both positive and negative impacts on Google’s business. Here are ways a crisis can adversely influence the company:

-

Decreased advertising spending: During an economic downturn, many businesses may reduce their advertising budgets as they try to cut costs. This could lead to a decrease in revenue for Google’s advertising business, which generates the majority of the company’s revenue.

-

Shifts in consumer behavior: A recession can lead to changes in consumer behavior, such as increased price sensitivity and a preference for value. Google may need to adjust its advertising and marketing strategies to accommodate these changes.

- Disruption: There can be unexpected major changes sparked by a recession that may include an emergence of new ad formats, stricter regulation, or a focus on privacy, which all may tame the company’s growth.

Yet, there are possible favorable outcomes that can boost Google’s performance. Promising developments may include:

-

Increased demand for cost-effective solutions: As businesses look for ways to reduce costs during a recession, there may be an increased demand for Google’s cost-effective solutions, such as Google Workspace and Google Cloud Platform. These services may become more attractive to businesses as they try to cut costs.

- Increased search traffic: During a recession, people may turn to search engines like Google to research products and services and find the best deals. This could lead to an increase in search traffic and revenue for Google.

A recession can have both positive and negative impacts on Google’s business, and the extent of these impacts will depend on a range of factors, including the severity and length of the recession and the company’s ability to adapt to changing market conditions.

Google’s Financial Health

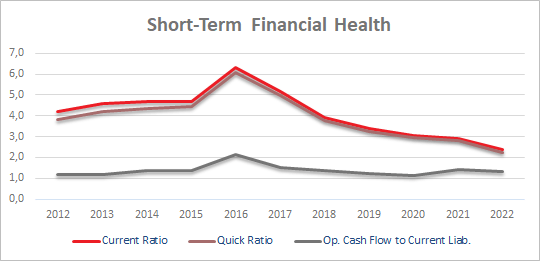

Nevertheless, Google faces the fear of a recession from a position of incredible strength and is well-prepared for turbulences. Metrics that serve as indicators of financial health include:

- Current Ratio of 2.38 – The current ratio is a type of liquidity ratio that assesses a company’s capacity to meet its short-term financial obligations, which are due within a year. This ratio provides investors with insight into how effectively a company can use its current assets to settle its current liabilities and other outstanding payments. A number above 1.0 is considered satisfactory.

- Quick Ratio of 2.22 – The quick ratio is a measure of a company’s ability to fulfill its immediate financial obligations and indicates its short-term liquidity position. This ratio evaluates a company’s capacity to settle its short-term debts using its most liquid assets. As for the current ratio, a value above 1.0 is desired for a healthy business.

- Operating Cash Flow to Current Liabilities of 1.32 – The operating cash flow ratio evaluates a company’s ability to satisfy its current liabilities using the cash generated from its operations. Essentially, it shows how many times the current liabilities can be settled using the net operating cash flow. In the case of Google, the company can cover all its current liabilities with around two-thirds of its annual operating cash flow which is impressive.

Google’s Short-Term Financial Health Ratios (Author – Financial Data From Seeking Alpha)

Google’s short-term financial health is one of the company’s strengths, especially when considering hard times in the near future. Furthermore, a firm’s well-being depends on its long-term stability which can be assessed by the following metrics:

- Debt to Equity Ratio of 0.1 – An optimal debt-to-equity ratio can vary depending on the industry, as certain industries tend to rely more heavily on debt financing than others. From the standpoint of lenders and investors, a high ratio suggests greater risk. In contrast, a lower debt-to-equity ratio, closer to zero, implies that the business has not relied extensively on borrowing to finance its operations which is the case of Google. However, a very low ratio may be seen as unfavorable. It may dissuade investors from investing in the company, as the business may not be maximizing potential profits or value that could be realized through borrowing and expanding operations.

- Debt to Capital Ratio of 0.03 – This metric quantifies the amount of debt a business utilizes to fund its ongoing operations relative to its capital, providing a measure of the proportion of debt utilized. In terms of risk, a lower debt ratio is deemed preferable. Google’s extremely low debt-to-capital ratio is another indication of the firm’s sound financial position built-up over the years.

- Total Liabilities to Total Assets of 29.9% – The ratio is a leverage metric that measures a company’s level of indebtedness relative to its assets. It provides investors with insights into the company’s financial stability. Google’s assets vastly outweigh its liabilities which sets the firm favorably for the future.

Long-term financial health metrics highly focus on debt which is reasonable. Since liabilities may not pose a threat in the zero-interest environment that businesses enjoyed over the last 13 years, the future may not look so rosy and the amount of debt may separate winners from losers. In other words, excessive amounts of liabilities will become a burden that some will not withstand. If borrowing costs keep increasing and such an environment persists, a company might find itself in a position of weakness that will force the management to take desperate measures. Yet, despair should never drive a decision-making process of a business. That’s why it’s crucial to analyze the company’s past performance and use this information to make reasonable projections of the unknown future.

Only when the tide goes out do you discover who’s been swimming naked.

– Warren Buffett

Is Google A Wonderful Business?

Most value investors search for great businesses. A great business must have a competitive advantage called also a moat among others. There is much more to what defines a wonderful company. However, having a strong moat can carry the business in bad economical times or under bad management.

The most important thing in evaluating businesses is figuring out how big the moat is around the business.

– Warren Buffett

Google has several competitive advantages that have allowed it to become one of the most successful companies in the world. Some of them are:

-

Brand recognition: Google is one of the most recognized and trusted brands in the world. Its name has become synonymous with the internet, search engines, and online advertising.

-

Technology and innovation: Google has invested heavily in technology and innovation, particularly in the areas of search algorithms, artificial intelligence, and cloud computing. This has allowed it to create products and services that are often more advanced and user-friendly than those of its competitors.

-

Data and analytics: Google has access to vast amounts of user data, which it uses to improve its services and offer more targeted advertising. This data also allows it to make better business decisions and stay ahead of its peers.

-

Scale and network effects: Google’s massive user base and network effects create a barrier to entry for competitors. The more people use Google, the more valuable its services become, making it difficult for competitors to gain a foothold in the market.

-

Culture and talent: Google has a reputation for being an innovative and exciting place to work, which has allowed it to attract some of the best talents in the tech industry. Its culture of experimentation and risk-taking has also contributed to its success.

Google’s moat stems from its ability to leverage its brand, technology, data, scale, and talent to create products and services that are difficult for its competitors to match. These are very powerful arguments to consider Google a wonderful company.

What Returns May Investors Expect?

Assuming that Google is a great business, it’s time to find out what investors can expect in terms of performance and future returns. Although the past doesn’t determine the future, it can give insights into how the business has been functioning and what the trends are. Financial Data that can give a bigger picture of the company’s financial history and at the same time serve as an indicator of future developments are:

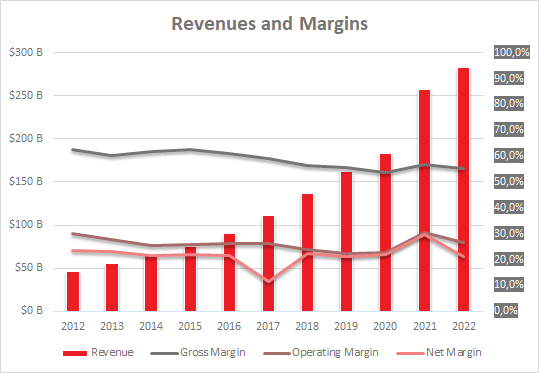

1. Revenues and margins.

Google’s Revenues and Margins (Author – Financial Data from Seeking Alpha)

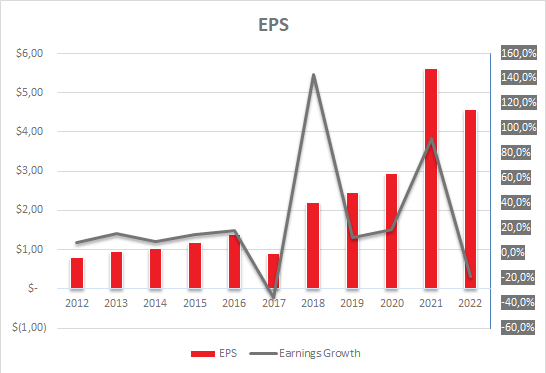

2. Earnings per share (EPS) and earnings growth

Google’s EPS and Earnings Growth (Author – Financial Data from Seeking Alpha)

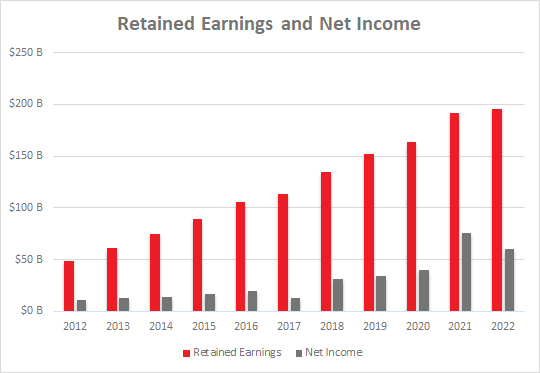

3. Retained earnings and net income

Google’s Retained Earnings and Net Income (Author – Financial Data from Seeking Alpha)

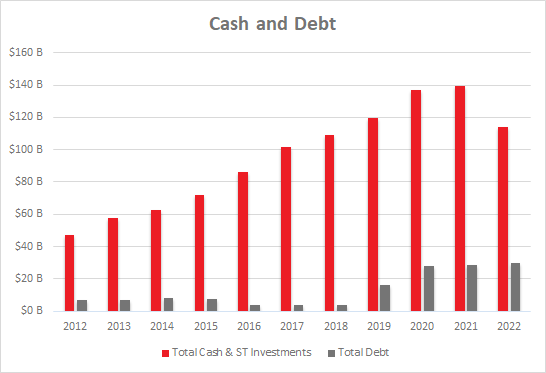

4. Cash and cash equivalents and total debt

Google’s Total Cash and Total Debt (Author – Financial Data from Seeking Alpha)

What becomes obvious after analyzing the plots is that Google has experienced strong revenue growth and has kept high margins along the way. Likewise, the company’s earnings have increased over 4 times in the period from 2012 to 2022. Net income growth has driven a boost of retained earnings which is a significant factor in evaluating a company’s financial condition. These earnings represent the accumulated net income that the company has retained over time, which gives it the capacity to reinvest in the business or distribute to shareholders. On the other hand, negative developments seen in the last years are a decrease in cash and cash equivalents and a major rise in debt when compared to 2018.

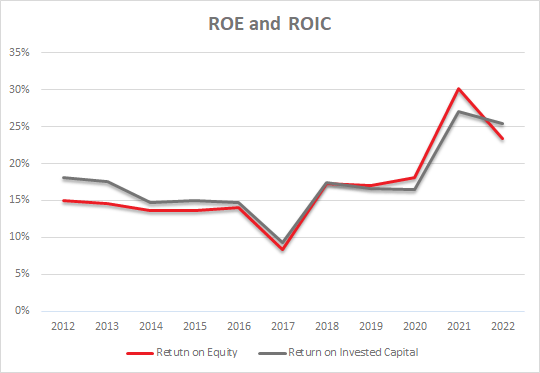

Two more metrics that make a business great and indicate high returns for investors are a high return on equity (ROE) and a high return on invested capital (ROIC). Fathers of value investing, Warren Buffett and Charlie Munger, referred to both on multiple occasions.

ROIC is a metric that evaluates the profitability percentage a company achieves by leveraging the capital from its equity and debt providers. It considers the complete capital structure of the business used to support its operations.

What we really want to do is buy a business that’s a great business, which means that business is going to earn a high return on capital employed for a very long period of time, and where we think the management will treat us right.

– Warren Buffett

ROE, on the other hand, demonstrates the company’s talent for converting equity investments into profits. Alternatively stated, it measures the earnings generated for every dollar of shareholders’ equity.

If you earn high enough returns on equity and you can keep employing more of that equity at the same rate — that’s also difficult to do — you know, the world compounds very fast.

– Warren Buffett

ROE was well explained by Stig Brodersen and Preston Pysh – the authors of the book Warren Buffett Accounting:

Let’s say you had the unique opportunity to purchase a money machine. The machine costs $100.000 to own. The machine is capable of printing $10.000 worth of money every year. This means an investment in the money machine would give you a return on equity of 10%. The cost of the machine is your equity and the profit from the printing is your net income. It’s truly that simple.

Google’s ROE and ROIC (Author – Financial Data from Seeking Alpha)

In the case of Google, both ROE and ROIC are high and have experienced strong growth since 2017. It’s encouraging from a value perspective and this trend confirms the overall positive assessment of the company. The last piece of the puzzle remains valuation which should give the answer if the great business is trading for a great price.

A great business at a fair price is superior to a fair business at a great price.

– Charlie Munger

Valuation

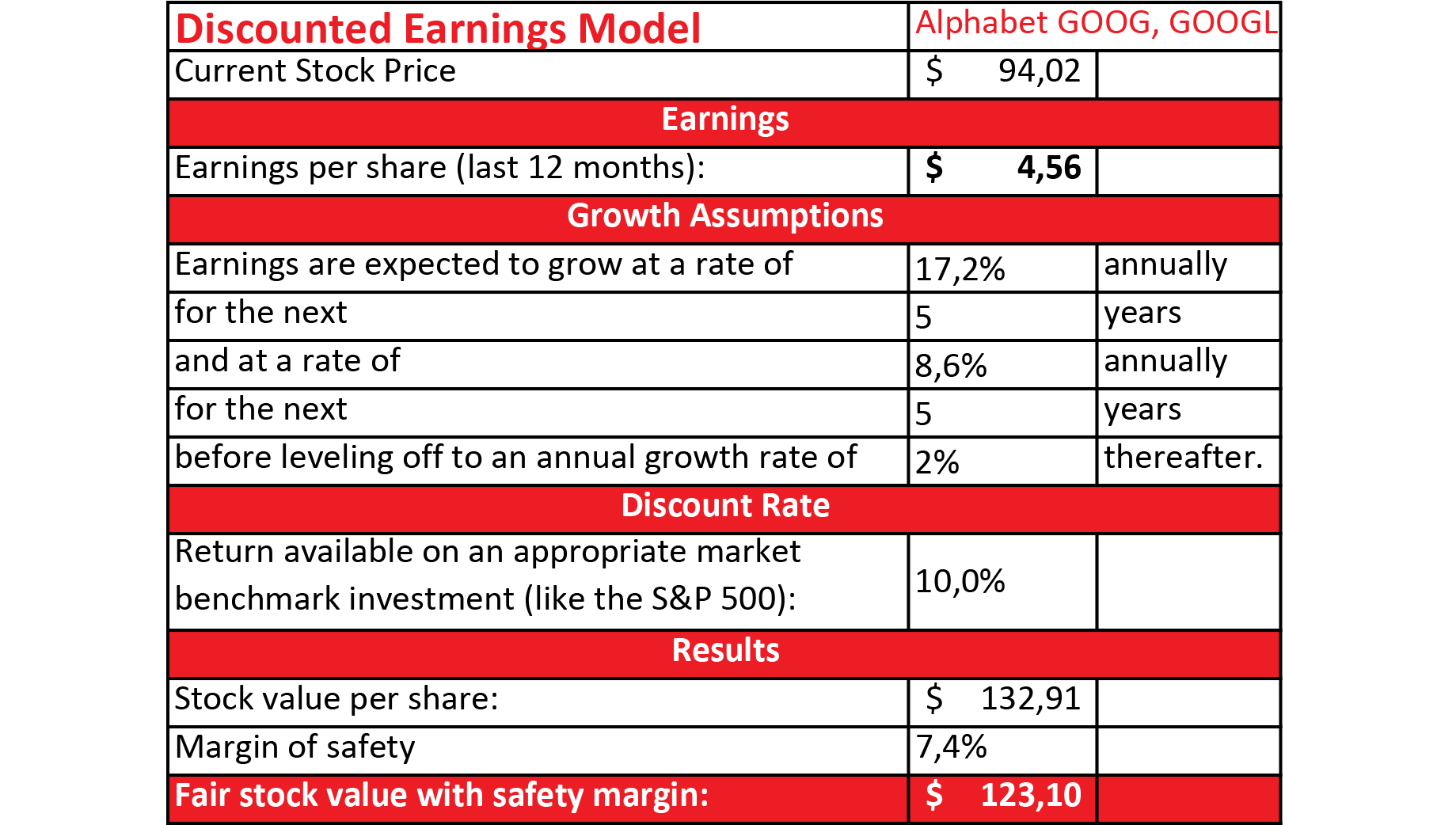

In the valuation process, two similar models with different inputs were utilized, both based on discounted earnings. The first model assumes:

- EPS growth of 17.2% in the next five years.

- EPS growth of 8.6% (half of what it was) for the following five years.

- EPS growth of 2.0% afterward into perpetuity.

- A discount rate of 10.0%

- A thin margin of safety of 7.4%. It was calculated based on the strength of the company’s short-term and long-term financial health.

Discounted Earnings Valuation Model (Author – Financial Data from Seeking Alpha)

According to the valuation, the fair price for Google stock is $123.1 which is substantially higher that the current share price. However, growth assumptions were quite optimistic. A good idea is to compare it with a different valuation model or with more conservative projections in order to come up with a price range.

The second valuation model also uses discounted earnings. The main difference is that this calculation utilizes an estimated terminal PE ratio the company will be trading at ten years from now. In this model, very conservative projections were used which could simulate a major negative impact of ChatGPT on Google’s growth. The input is as follows:

- EPS growth of 8.6% for the next ten years.

- A discount rate of 10.0%

- A terminal PE ratio of 9.0. A ratio of 9.0 should be applied to a company with no growth ahead.

A valuation with these grim assumptions returns an intrinsic value of $78.87 which is significantly lower than the previous one. A mean average can be taken in order to take both results into consideration. The final outcome is $100.99 suggesting that Google is slightly undervalued. Considering that the assumptions and the valuation deliver a reliable result, investors may expect a ~10.0% annual return for the next ten years.

Nobody knows how the market will price the stock in the near term. There might be a better buying opportunity. However, Google stock is in the range which starts being compelling for investors focused on value.

Conclusion

Assuming that Google continues to innovate and defend its competitive advantages, its outlook appears to be very positive. Google has a strong track record of innovation, and it invests heavily in research and development to maintain its position as a market leader.

One of Google’s biggest moats is its search engine, which dominates the market. Google has also made significant strides in areas such as artificial intelligence, cloud computing, and mobile technology, which should continue to drive growth and create new revenue streams in the future.

Additionally, Google has a diverse range of products and services, including Google Maps, YouTube, Google Ads, and the Google Play store, which provide a significant source of revenue and make it less reliant on any one product. The company’s financials are also very strong, with a significant amount of cash on hand, high margins, and high ROE and ROIC.

There are also potential risks and challenges that shouldn’t be neglected. These could include increased competition from other tech giants and new contenders like ChatGPT, regulatory challenges, and cybersecurity risks. However, as long as Google continues to innovate and adapt to changes in the market, it should be well-positioned for continued success in the years to come.

Disclosure: I/we have a beneficial long position in the shares of GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.