Summary:

- Home Depot’s latest quarterly update and outlook weren’t great, but the firm continues to have an enviable competition position.

- We like the company’s tremendous free cash flow generation and that it has consistently covered its cash dividends paid for years.

- We value shares modestly higher than where they are trading at as of this writing, and we view the company as a fantastic dividend growth idea. Shares yield ~2.8%.

Romanista

By Valuentum Analysts

Home Depot’s (NYSE:HD) latest quarterly results left a sour taste in many an investor’s mouth, but we’re not too worried. We believe the company’s positioning with respect to do-it-yourself-ers and professional contractors remains solid, and we expect that home improvement trends will remain strong. The COVID-19 pandemic, in our view, has fundamentally changed how consumers view their home. They simply need more work and living space. We’re huge fans of Home Depot’s strong free cash flow generation, as well as its ability to cover cash dividends paid with it. With that said, let’s dig into our work on this home improvement retailing giant.

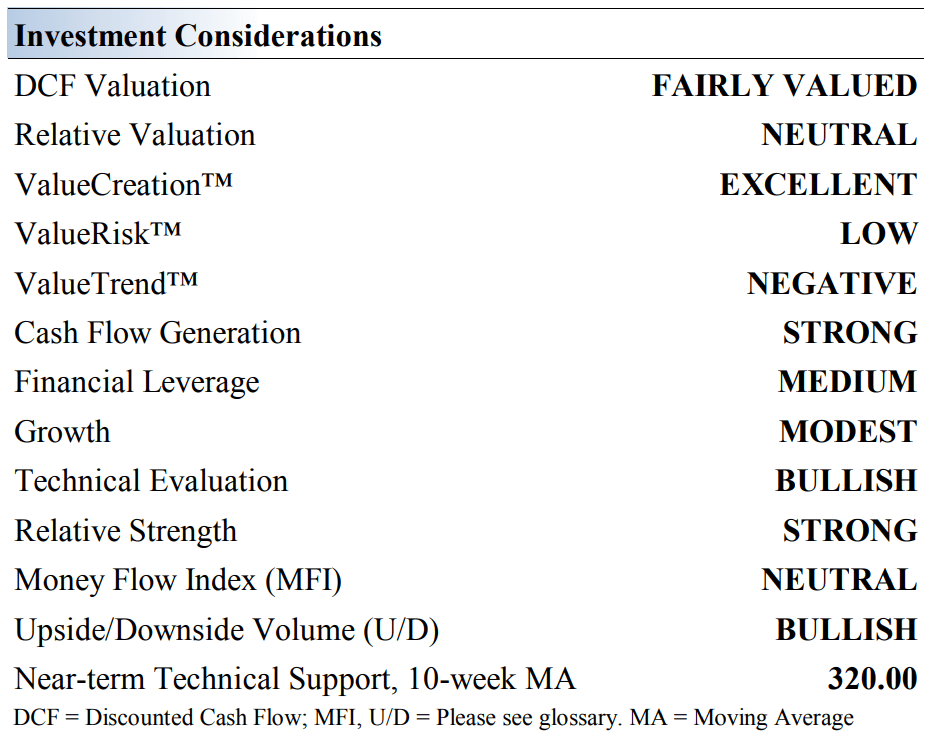

Key Investment Considerations (Image Source: Valuentum)

As many may already know, Home Depot is the largest home improvement specialty retailer in the world. The company sells building materials, home improvement as well as lawn/garden products. The company’s stores are huge and average ~104,000 square feet of enclosed space, with ~24,000 additional square feet of outside garden area.

Home Depot’s financial performance depends in part on the stability (and strength) of the housing, residential construction, and home improvement markets. The outlook for new home construction activity in the U.S. has weakened significantly of late, but for the most part, the housing market, in general, remains surprisingly resilient. We’ll talk more about recent trends later on in this note.

Home Depot recently bought HD Supply through an ~$8.0 billion all-cash transaction. This deal added to Home Depot’s exposure to the maintenance, repair, and operations (‘MRO’) space, a significantly fragmented market that the firm estimates is worth ~$55 billion. We look positively to increased federal infrastructure investments that will also support Home Depot’s outlook

Home Depot plans to focus more on its professional customers, where average tickets are substantially larger, with an eye towards growing its MRO business. The firm has also significantly improved its omni-channel selling capabilities by integrating its evolving digital presence with its expansive physical operations. Home Depot has placed a great emphasis on further improving its e-commerce business to support sales growth.

Cash Flow Valuation Analysis

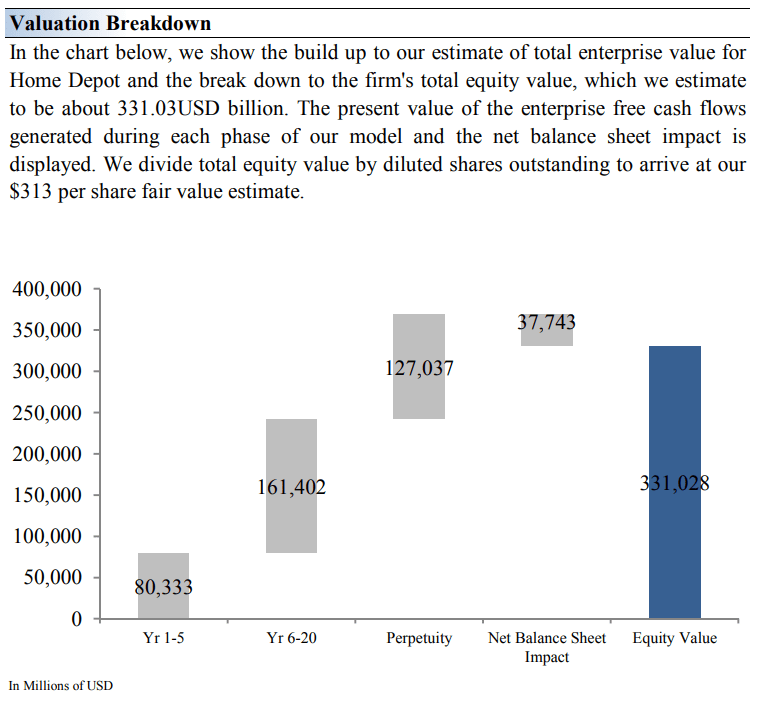

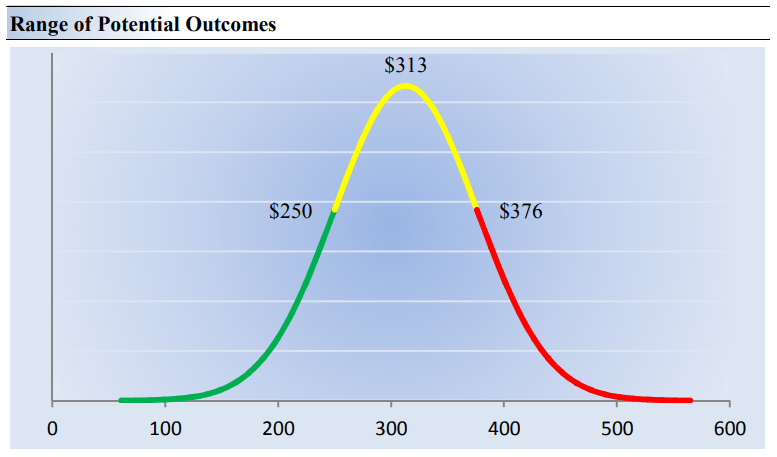

Valuation Breakdown (Image Source: Valuentum) Range of Potential Outcomes (Image Source: Valuentum)

On the basis of our discounted cash-flow valuation model, we think Home Depot is worth $313 per share with a fair value range of $250-$376. The margin of safety around our fair value estimate is driven by the firm’s LOW ValueRisk rating, which is derived from an evaluation of the historical volatility of key valuation drivers and a future assessment of them.

Our near-term operating forecasts, including revenue and earnings, do not differ much from consensus estimates or management guidance. Our model reflects a compound annual revenue growth rate of 4.3% during the next five years, a pace that is lower than the firm’s 3- year historical compound annual growth rate of 11.8%.

Our valuation model reflects a 5-year projected average operating margin of 15.6%, which is above Home Depot’s trailing 3-year average. Beyond year 5, we assume free cash flow will grow at an annual rate of 2.9% for the next 15 years and 3% in perpetuity. For Home Depot, we use a 8.7% weighted average cost of capital to discount future free cash flows.

Our discounted cash flow process values each firm on the basis of the present value of all future free cash flows. Although we estimate Home Depot’s fair value at about $313 per share, every company has a range of probable fair values that’s created by the uncertainty of key valuation drivers (like future revenue or earnings, for example). After all, if the future were known with certainty, we wouldn’t see much volatility in the markets as stocks would trade precisely at their known fair values.

Our ValueRisk rating sets the margin of safety or the fair value range we assign to each stock. In the graph above, we show this probable range of fair values for Home Depot. We think the firm is attractive below $250 per share (the green line), but quite expensive above $376 per share (the red line). The prices that fall along the yellow line, which includes our fair value estimate, represent a reasonable valuation for the firm, in our opinion. Right now, shares of Home Depot are trading at $297.

Latest Quarterly Results

Home Depot issued disappointing fourth quarter 2022 results on February 21. The update revealed that comparable store sales in the quarter fell 0.3%, while operating income tumbled 1.5% from the same period last year. Diluted earnings per share nudged 2.8% higher from the same period a year ago. Home Depot continues to work through a weakened consumer spending landscape as well as year-over-year comparisons that are difficult as a result of pandemic-driven demand.

Looking ahead to fiscal 2023, Home Depot’s sales guidance could have been better. The company believes that sales and comparable store sales expansion will be “approximately flat” for the fiscal year on a year-over-year basis, and an operating margin of 14.5%. The margin guidance incorporates the firm’s $1 billion in additional compensation to help with churn across its frontline employee base. For fiscal 2022 and fiscal 2021, Home Depot’s operating margin was ~15.3% and ~15.2%, respectively, so the forward guidance isn’t particularly great in light of levels of profitability it reached the past couple years. The company’s diluted earnings per share is also targeted to decline at a mid-single-digit clip during fiscal 2023. All told, Home Depot’s guidance for 2023 wasn’t particularly great given the resilience the firm has shown through all phases of the housing cycle.

The COVID-19 pandemic drove an increase in demand for home-improvement endeavors across the board. Millions of workers during the pandemic discovered that they preferred more space at home, whether living space or working space, and putting money in their homes held water given the work-from-home trends that were adopted for a long time after the onset of the COVID-19 pandemic. That said, many companies are asking employees to come back to the office, and with life largely getting back to “normal” for many, the amount of free time to do home improvement projects has become more limited. It’s also the case that consumer budgets have become largely tapped out, and excess savings built up during the pandemic may be almost completely depleted by the third quarter of 2023. Consumer credit card debt is also picking up aggressively. It’s looking more and more like fiscal 2023 may mark a period of transition for home improvement retailers as Home Depot and its rivals adjust to a post-pandemic demand environment.

Home Mortgage Rates on the Rise (30-year fixed rate = blue; 15-year fixed rate = green)

30-year fixed rate = blue. 15-year fixed rate = green. (Freddie Mac)

Though we haven’t really seen much yet, we think the home-buying market is likely to retrench aggressively this year (or next), particularly with mortgage rates approaching the high-single-digits. For the week ending February 16, the U.S. average weekly fixed rate mortgage for a 30-year mortgage was 6.32% and for a 15-year mortgage, it was 5.51%, according to Freddie Mac. Though still low historically speaking, these rates are now more than double levels of late 2020, where the 30-year mortgage rate fell below 3% and the 15-year mortgage rate was nearly 2%. Housing prices will likely fall considerably in the coming years, and frankly, we’ve been quite surprised at how slow the adjustment has been to this new reality. The National Association of Realtors, for example, wrote that “single-family existing-home sales prices climbed in almost 90% of measured metro areas – 166 of 186 – in the fourth quarter (of 2022). The national median single-family existing-home price increased 4.0% from one year ago to $378,700.” It stands to reason that higher rates will start to drive home prices lower based on affordability. Perhaps this will happen slowly at first, and then all at once.

Regardless, “the home” has become much more important the past few years as a result of COVID-19 and what the future of work may look like. Work-from-home trends have emerged as a result of the pandemic, and many employers are adopting a hybrid working environment. We expect the home improvement retailing industry, including Home Depot, to continue to reap the benefits of these dynamics as “the home” becomes a crucial part of the work environment, itself. Traditionally, there has been a stigma of working from home, but we don’t think this exists anymore, as times have changed. Employers have to strongly consider the needs and preferences of their employees, more than ever before, particularly in the current tight labor market. Though many consumers made material changes to their homes during the pandemic to accommodate the new working environment adding more space, this is likely in the early innings. We would not be surprised to see many workers seek larger homes outside of urban areas; suburban sprawl will likely continue.

Concluding Thoughts

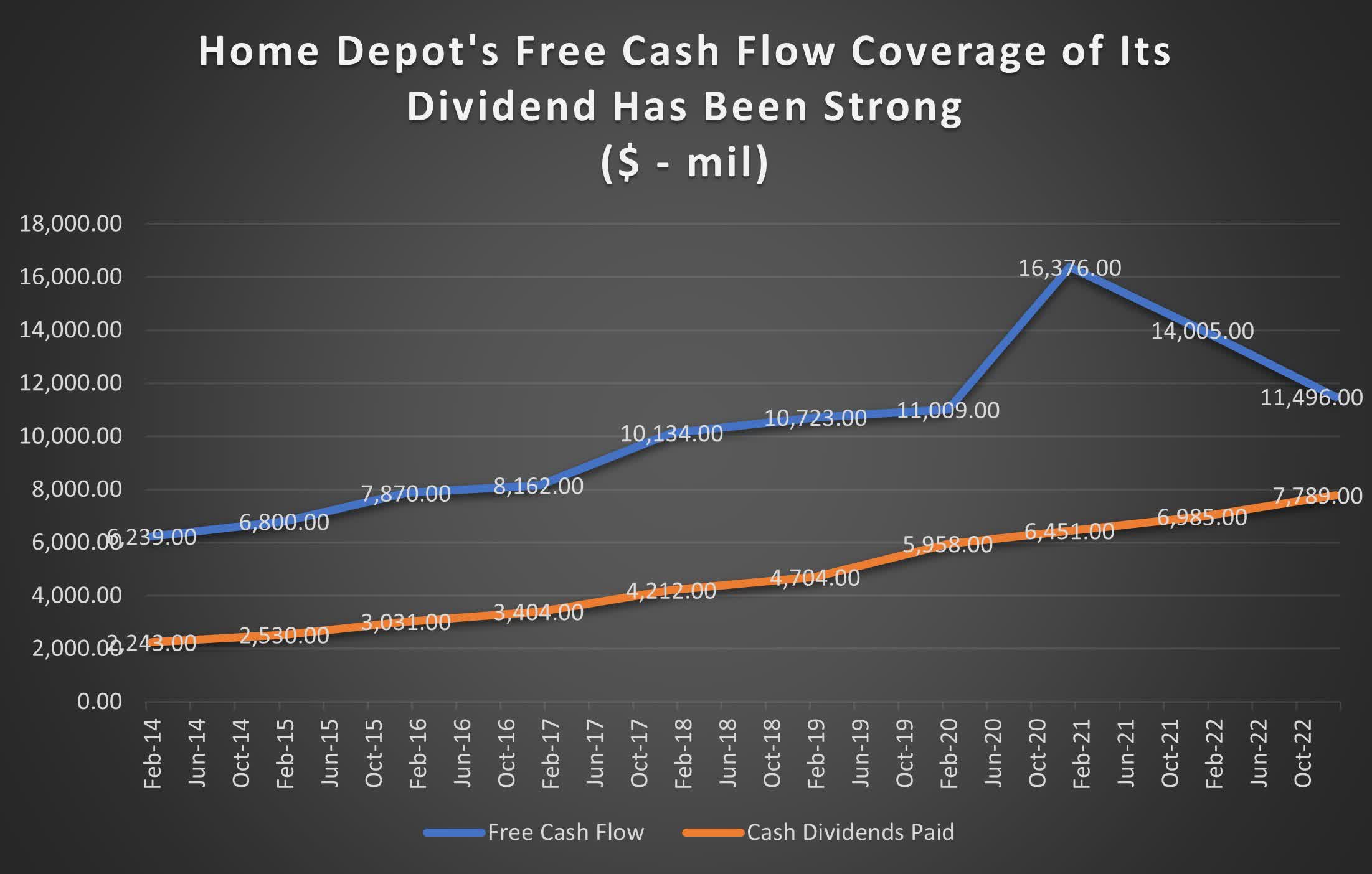

Home Depot’s Free Cash Flow Coverage of Its Dividend Has Been Strong (Data Source: Seeking Alpha)

Home Depot’s latest quarterly update wasn’t great, but we’re looking past fiscal 2022 and what could be a generally challenging fiscal 2023. We continue to like the home retailing giant as a solid dividend growth consideration in the long run.

The company’s free cash flow generation easily covered cash dividends paid during fiscal 2022, as it has for many years now, and that’s a trend we expect to continue. The big box home-improvement retailer recently upped its dividend payout 10%, to $2.09 per share, or $8.36 per share on an annualized basis. That higher dividend implies a forward estimated dividend yield of ~2.8%.

The company’s dominance in serving do-it-yourself-ers and professional contractors as well as its recent decision to bring HD Supply in-house should help it succeed during fiscal 2023 and beyond. Our fair value estimate of Home Depot stands at $313 per share.

This article or report and any links within are for information purposes only and should not be considered a solicitation to buy or sell any security. Valuentum is not responsible for any errors or omissions or for results obtained from the use of this article and accepts no liability for how readers may choose to utilize the content. Assumptions, opinions, and estimates are based on our judgment as of the date of the article and are subject to change without notice.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Brian Nelson owns shares in SPY, SCHG, QQQ, DIA, VOT, BITO, RSP, and IWM. Valuentum owns SPY, SCHG, QQQ, VOO, and DIA. Brian Nelson’s household owns shares in HON, DIS, HAS, NKE, DIA, and RSP. Some of the securities written about in this article may be included in Valuentum’s simulated newsletter portfolios. Contact Valuentum for more information about its editorial policies.