Summary:

- Q4’s free cash flow improved a little but the dividend still seems in danger.

- Consider selling cash-secured puts at a strike price you like.

- I explain why $20 is an interesting entry point.

JasonDoiy

I’ve been biding my time to write this article with the intention of giving Seeking Alpha readers a bit of respite from Intel Corporation (NASDAQ:INTC) articles. Since the company’s awful Q4 results, Seeking Alpha and other sites have been buzzing with Intel articles. I wrote this article a couple of months ago arguing that Intel’s dividend looked in danger using Free Cash Flow based dividend coverage. With the latest results in our rearview mirror, it is time to see if the red-alert still applies. Let us get into the details.

Why Free Cash Flow over EPS?

When evaluating dividend coverage, most investors and analysts tend to look at earnings per share (“EPS”). I prefer free cash flow (“FCF”) as a better indicator of financial health for these reasons:

- Earnings tend to be up and down depending on rare events and write-offs.

- Earnings are more prone to GAAP-related fluctuations.

- Cash flow is king.

Intel’s Cash Flow Got A Little Better

Let us see how Intel’s dividend coverage looks after its most recent quarterly (Q4) result.

- Total shares outstanding: 4.14 Billion

- Current quarterly dividend per share: $0.37

- Quarterly FCF required to cover dividends: $1.5318 Billion

- FCF in Q4: $2.004 Billion. That looks a lot better than during the Q3 review.

- Payout ratio using FCF: 76%.

Sometimes, a single quarter’s numbers may be exaggerated on either side. So, let us run the same numbers above based on a 12-month period (January 2022 to December 2022).

- Total shares outstanding: 4.14 Billion

- Current annual dividend per share: $1.48

- Annual FCF required to cover dividends: $6.1272 Billion

- Total FCF for the last 4 quarters: -$9.617 Billion. Ouch! As bad as this looks, this is once again better than how the trailing 12 month FCF looked during the Q3 review.

- Payout ratio using 4 quarters’ FCF: NA.

To summarize the cash flow situation, although things improved marginally in Q4, the larger concerns are still intact. It is hard to see Intel affording its current dividend payout unless things turn around drastically for the business.

What’s an Investor To Do?

A recent Seeking Alpha article makes the case for buying Intel lower between $15 to $20. While I agree I wouldn’t recommend buying at $30, I don’t see a fall all the way to $15 yet. But $20 looks like a plausible play if the right strategy is used. And that strategy is to sell cash secured $20 puts as explained below. This ensures that you don’t eternally wait for a magical entry point that may never arrive while ensuring you don’t go all in buying shares at $30 right now.

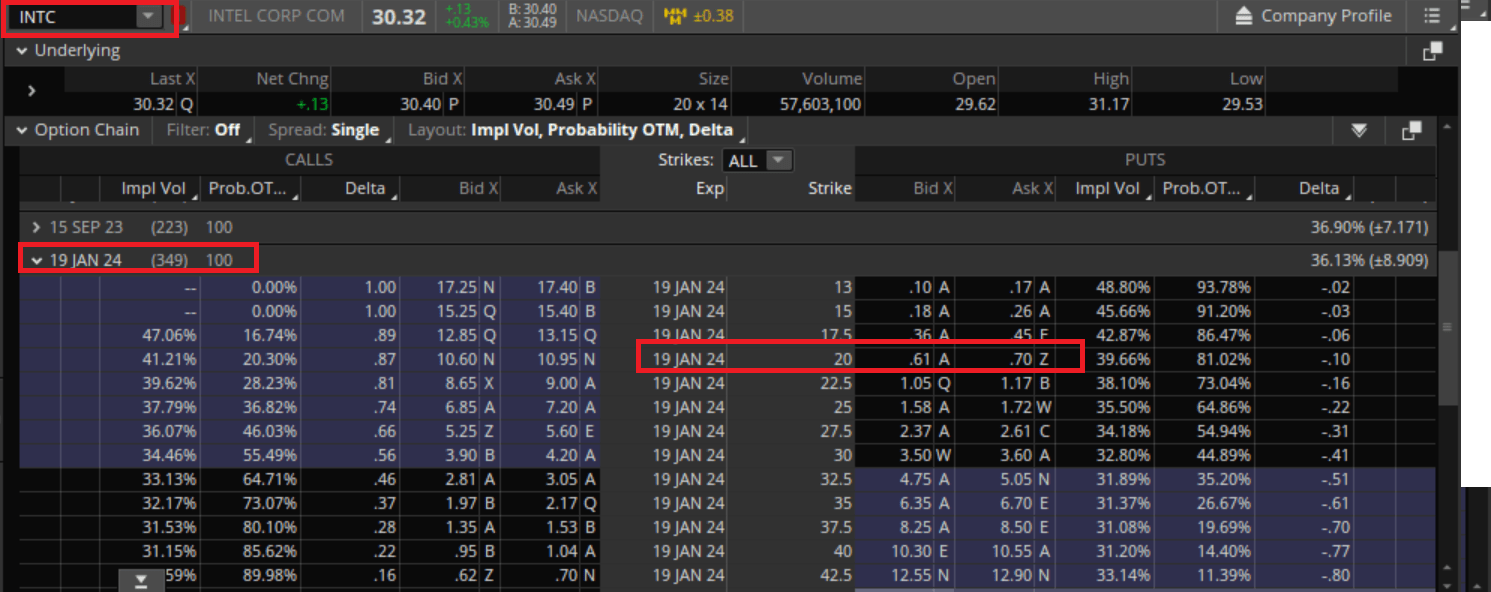

Intc Options Chain (Think or Swim)

Key data points

- Strike Price: $20

- Expiration Date: January 19th, 2024, about a year from now.

- Premium: Since the expiration of this chain is far off, the spread between bid and ask is quite large. Let’s assume $0.65 as the premium for this exercise.

In simple words, the put seller collects $65 immediately to buy 100 shares of Intel at $20 if the stock reaches $20 or below by January 19th, 2024.

What’s the expected return and possible outcomes?

Return: The premium collected ($65) for setting aside $2,000 represents a 3.25% return for a year. At this time, the market assigns an 81% probability that Intel remains above $20 by expiration.

Outcome #1: If Intel stays above $20 by the expiration date, the option seller just retains the premium mentioned above. The option seller will not be obligated to buy the shares.

Outcome #2: If Intel goes below $20 by the expiration date, the option seller will be forced to buy 100 shares at $20, irrespective of where the stock trades at that time. Keeping the premium netted in mind, the average cost, in this case, will be $19.35 ($20 minus $0.65).

Outcome #3: As an option seller, one can “buy to close” anytime instead of waiting till the expiration date. That may be appealing to those who have the time and patience to play short-dated options many times over. But we typically let the option expire before choosing another chain (or another stock).

Outcome #4: Let’s say the stock price plummets below $20 before the expiration. In this scenario, the premium you got paid when selling the put will be lower than the price you’d need to pay to “Buy to close” in outcome #3. Let’s say you don’t want to get assigned yet but at the same would like to remain in the game to acquire Intel lower. Then “rolling” your cash secured put is an option.

Why $20 Looks attractive?

I covered some of three points below in an article last year and those points largely apply here too.

- Yield: While I expect Intel to reduce its dividend, I don’t expect a full blown elimination. Let’s say the dividend gets cut by half to 74 cents/share a year. At $20, the yield will still be close to 4%, which is nothing to laugh at even in the current high interest rate environment. And this dividend and resulting yield look much more affordable as shown in the Free Cash Flow section above.

- Valuation: Using 2024’s expected earnings of $1.88, $20 would represent a multiple of 10. This is appropriate for a company in the midst of an ever-going turnaround with no end in sight.

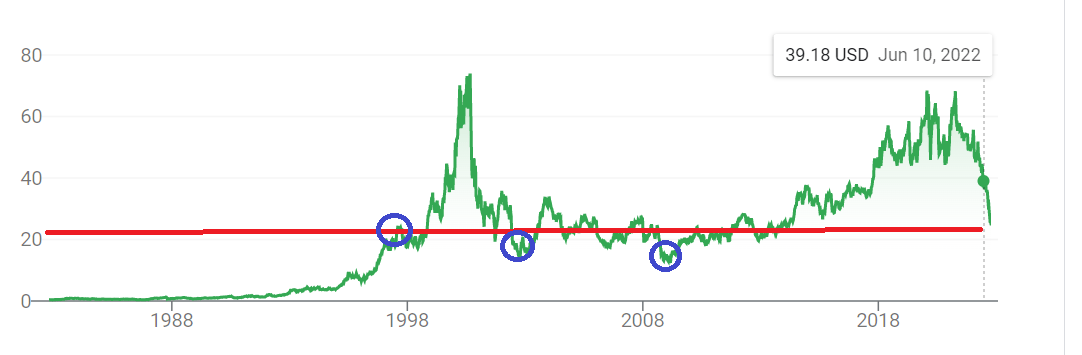

- Generational Lows: While things look bad for Intel now, it is hard to see things going to the nadir experienced during 2008 Financial crisis or the COVID peak. Those were the last two times Intel reached $20 or below.

Intc Chart (Google Finance)

Potential Risks and Conclusion

Intel’s risks as a fundamental story is well known at this point. The company’s cyclical nature notwithstanding, the current woes are exaggerated by the ebb resulting from post-COVID fall in demand. As a result, Intel’s earnings estimates over the next five years (-25%/yr) are some of the worst in the overall market, not just the semiconductor sector. The yield has often been cited as a reason to own Intel but that looks very much in danger as shown above.

Despite these troubles and the recent awful earnings, Intel is up 13% YTD and it is hard to justify this. But that doesn’t mean you just wait for it to go to a price point you may never see. Selling puts offers a nice solution to stay in the game while not going all in immediately. But please know there are various option chains (expiration dates, strike prices, premium combination). Please pick one that seem to best fit your goals.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.