Summary:

- Indonesia Energy has filed proposed terms for a $15 million U.S. IPO of its common stock.

- The firm is an oil exploration & production company with assets in Indonesia.

- INDO has produced unpredictable and high variable financial results, so I’m passing on the IPO.

Quick Take

Indonesia Energy (NYSE:INDO) has filed to raise $15 million in gross proceeds in a U.S. IPO of its common stock, per an amended registration statement.

The company is an exploration and production firm with assets in Indonesia.

INDO is a tiny company with widely fluctuating financial results. I’m avoiding the IPO.

Company & Technology

Jakarta, Indonesia-based INDO was founded in 2014 and currently holds two oil and gas assets through its operating subsidiaries in Indonesia, namely the Kruh Block, a producing block, and the Citarum Block – an exploration block.

The firm has also identified a potential third block located in the Rangkas Area.

Management is headed by Co-Founder, Director and CEO Dr. Wirawan Jusuf, who previously co-founded and served as a Commissioner of Pt. Asiabeef Biofarm Indonesia.

INDO acquired rights to the Kruh Block in 2014 and started its operations in Nov 2014 through its local subsidiary Green World Nusantara, under a Technical Assistance Contract [TAC] with Pertamina – Indonesia’s state-owned oil and natural gas corporation – until May 2020, after which operatorship of the block will continue as a Joint Operation Partnership [KSO] for 10 years until May 2030.

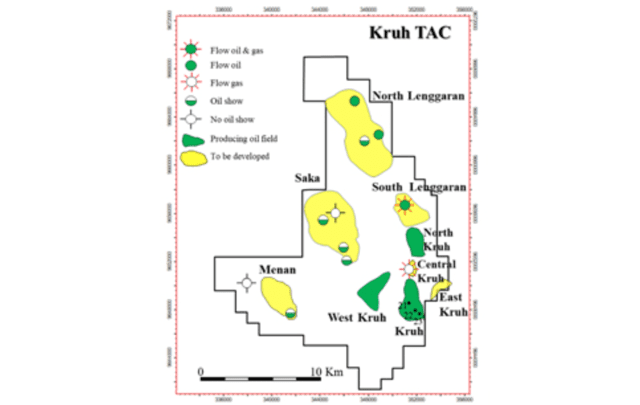

The Kruh Block, located 25 km northwest of Pendopo, Pali, South Sumatra and covering an area of 258 square km (or 63,753 acres), is capable of producing an average of approximately 9,000 barrels gross of oil per month.

Below is an overview map of the Kruh Block and its producing fields:

Source: Company registration statement

Since 2014, the company has increased its Kruh Block gross production from 250 Barrels of Oil Per Day [BOPD] in 2014 to 400 BOPD gross in early 2018, which management believes the company achieved by the drilling of three new wells and upgrade of the production facilities.

The Citarum Block covers an area of 3,924.67 square km (or 969,807 acres) and is located onshore in West Java, only 16 miles away from Jakarta, Indonesia’s capital.

INDO is focused on the acquisition of medium-sized blocks as they are mostly overlooked by major oil and gas exploration companies who compete with larger oil assets.

Market & Competition

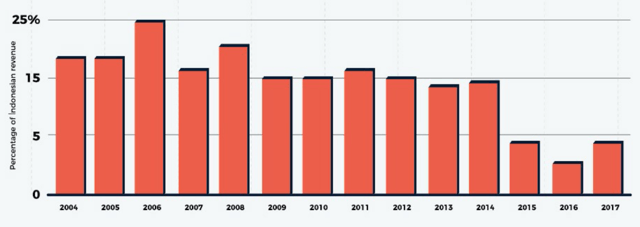

According to a 2018 market research report by The Asean Post, the Indonesian oil and gas industry accounted for nearly 25% of the country’s economy in 2006 and had decreased to 3% in 2016, as shown by the chart below:

The main factors driving market decline were falling demand for oil as well as an oversupply of the commodity, which resulted in a decline of prices per barrel from $115 in June 2014 to under $35 by the end of February 2016.

Moreover, investments for oil and gas exploration in Indonesia had fallen from $1.3 billion in 2012 to $100 million in 2016.

The country has launched initiatives to revitalize the sector, while the report cites its Energy and Mineral Resources Minister, Ignasius Johan, who forecasts $200 billion in investments over the next 10 years through incentives, including tax-free imports of drilling equipment and cost recovery.

Despite that, Southeast Asian oil analyst Johan Utama says that Indonesia’s constantly changing regulations inspire the feeling of an unstable industry, which would serve to drive investors away.

A PwC report titled Oil and Gas in Indonesia 2017 put a highlight on Indonesia’s challenge of depletion in oil resources and the availability of new reserves.

According to the International Energy Agency [IEA], Indonesia is the third-largest geothermal power producer in the world while the country’s Energy Ministry plans to increase the nation’s geothermal production capacity to 5,000 MW by the end of 2025.

Major competitors for the acquisition of new oil blocks include Pertamina, Indonesia’s state oil corporation, and other major oil and gas companies that operate in the country.

INDO’s recent financial results can be summarized as follows:

-

Variable topline revenue, contracting in the most recent period

-

Fluctuating gross profit

-

A swing to operating loss

-

Varying cash flow from operations – most recently negative

Below are relevant financial metrics derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Six Mos. Ended June 30, 2019 |

$ 2,197,833 |

-27.6% |

|

2018 |

$ 5,856,341 |

58.1% |

|

2017 |

$ 3,703,826 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Six Mos. Ended June 30, 2019 |

$ 884,637 |

-45.5% |

|

2018 |

$ 3,315,988 |

271.4% |

|

2017 |

$ 892,820 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

Six Mos. Ended June 30, 2019 |

40.25% |

|

|

2018 |

56.62% |

|

|

2017 |

24.11% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Six Mos. Ended June 30, 2019 |

$ (501,750) |

-22.8% |

|

2018 |

$ 143,384 |

2.4% |

|

2017 |

$ (1,552,466) |

-41.9% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

|

|

Six Mos. Ended June 30, 2019 |

$ (456,183) |

|

|

2018 |

$ 145,723 |

|

|

2017 |

$ (1,604,105) |

|

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Six Mos. Ended June 30, 2019 |

$ (200,605) |

|

|

2018 |

$ 1,920,219 |

|

|

2017 |

$ (182,737) |

Source: Company registration statement

As of June 30, 2019, the company had $6.2 million in cash and $8.5 million in total liabilities.

Free cash flow during the twelve months ended June 30, 2019, was $1.2 million.

IPO Details

INDO intends to sell 1.5 million shares of its ordinary shares at a midpoint price of $10.00 per share for gross proceeds of approximately $15.0 million, not including the sale of customary underwriter options.

It is customary for foreign domiciled firms to sell American Depositary Shares to U.S. investors as a convenience, so the lack of this element is a negative signal.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO would approximate $70.8 million.

Excluding effects of underwriter options and private placement shares or restricted stock, if any, the float to outstanding shares ratio will be approximately 20.0%.

Per the firm’s most recent regulatory filing, the firm plans to use the net proceeds as follows:

We plan to use the net proceeds of this offering primarily to fund the development of the Kruh Block and exploration of the Citarum Block as part of our strategy for adding new reserves and developing the field after discovery, and for general working capital and corporate purposes.

However, the registration statement has left blank the percentages of the net proceeds that the firm will devote between the two blocks.

Management’s presentation of the company roadshow is available here.

The sole listed underwriter of the IPO Aegis Capital Corp.

Commentary

INDO is seeking a tiny IPO transaction on U.S. markets at a challenging time for any company to go public, let alone an unknown Indonesian energy company.

Perhaps management has private investors lined up to buy the IPO so it can float its shares.

The firm’s financials are very spotty, with a high degree of variability even in light of the fluctuating price of oil in various markets.

Aegis Capital Corp. is the sole underwriter and there is no data on IPOs the firm has been involved with over the last 12-month period.

The production opportunity for the firm’s assets is interesting, so maybe INDO will hit a ‘gusher’ and prove me wrong.

In the meantime, I’ll be watching this IPO from the sidelines.

Expected IPO Pricing Date: To be announced.

Analyst’s Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis. Get started with a free trial!