Summary:

- Apple is the king of the hill when it comes to big tech companies, but shares are expensive today at 23.1x earnings.

- The company has maintained its impressive margins and balance sheet.

- Supply chain issues in China and issues with passive fund flows could spell trouble for Apple’s stock in 2023.

- The company bought back $90B in 2022, but the dividend yield of 0.65% isn’t much to get excited about despite consistent dividend growth and the low payout ratio.

- Investors who want to be long Apple should consider buying Berkshire Hathaway.

Shahid Jamil

It’s been a while since my last update on Apple (NASDAQ:AAPL), but I figured now was a decent time for an article as Christmas approaches. I haven’t owned the stock since late last year, but it’s a high-quality business that produces innovative high-quality products. In my January article, I focused in on why I would choose to get exposure to Apple through Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) instead. That would have turned out to be a pretty good trade, as shares of Apple are down over 20% YTD while Berkshire is basically flat.

Investment Thesis

Apple is business that has built a cult like following in the last decade with its products like the iPhone and MacBook. Apple stock has developed a cult like following as well as the company has grown to be the largest in the world with a market cap of $2.3T, providing massive returns for investors. It’s a high margin business with a rock-solid balance sheet, but there are a couple problems for the stock that I will be highlighting today.

The first is the supply chain issues with China, which is the company’s core manufacturing base. There have been issues with protests and the company is looking at options outside of China, but it has created uncertainty around the company’s supply chain in the near term. The other thing that could be a drag on Apple stock is the potential for ETF and fund outflows, many of which hold Apple as a core position.

Shares aren’t cheap today either at 23.1x earnings. That is well above its average multiple for the last decade, and growth isn’t projected to be very impressive over the next couple years. They have continued their massive buyback program, with another $90B in 2022. I’m curious to see if the 1% buyback tax that will go into effect in 2023 will have any impact on the program. The yield is small today at 0.65%, so it won’t draw many investors looking for current income, but they have a low payout ratio and have had consistent dividend growth for years. For me, Apple remains a watchlist stock for now, but I will be keeping an eye on the stock in 2023 to see if we get a better buying opportunity. Like I said in January, the best way to be long Apple right now is through Berkshire Hathaway.

A Quick Peek At The 10-K

Sales increased by 8% overall when compared to fiscal 2021, with the Mac and Services segments leading the way with 14% growth. Gross margin was up 1% for products to 36.3% and 2% for services to 71.7%, for an overall bump of 1.5% (to 43.3%). Net margins were down slightly (from 25.9% to 25.3%) on increased operating expenses and taxes. While that decrease isn’t ideal, Apple remains a high margin business, and the growth of the higher margin service segment to make up a larger portion of the business means they should be able to keep overall margins high.

Apple still maintains a rock-solid balance sheet and has an AA+ credit rating. Debt has come down a bit from last year, and they still have plenty of cash and securities on the asset side of the balance sheet. The debt is effectively all fixed rate and carries a low interest rate overall, ranging from 0.03% to 4.78%. The longest maturity is forty years out in 2062, which shows the bond market’s confidence in the company. I wouldn’t be interested in loaning money for that period of time due to inflation and other risks, but the so-called smart money is confident in Apple’s long-term future. Their balance sheet means they will be able to weather any storm in the near term, but one of the things that could impact Apple is problems with China and their supply chain.

Problems In China

I highlighted the supply chain issues in China in my May article on Apple, and I think it is one of the main risks with the stock today. They have been working to diversify their supply chain, but China is still going to be the foundation of their manufacturing capacity for the foreseeable future. A quick search brings up numerous articles on Apple’s supply chain and the potential issues facing the company.

Search Results (bing.com)

While large publications point out potential problems with Apple’s supply chain, another valuable resource are the recent Apple articles on Seeking Alpha highlighting the issue. I would recommend reading Cavenagh Research’s recent article as well as the article by Stone Fox Capital. Both articles touch on different valuable points related to the supply chain, and these articles happen to be the most recent bearish articles on the stock. Another potential speed bump for Apple’s stock is what happens in the future with passive fund flows.

A Potential Passive Flows Problem

One of the problems I see with Apple stock is what could happen with passive fund flows in ETFs and mutual funds over the next couple years. Some of the largest equity ETFs are the S&P 500 ETFs managed by the asset management giants like State Street (STT), BlackRock (BLK), and Vanguard. The SPDR S&P 500 ETF (SPY), iShares Core S&P 500 ETF (IVV), and the Vanguard S&P 500 ETF (VOO) hold nearly $1.5T in assets. These funds receive significant and consistent inflows from automatic retirement fund purchases as well as institutional and individual investors.

Big tech companies have been a huge beneficiary of these fund flows, with nearly a quarter of the index comprised of companies like Apple, Microsoft (MSFT), Google (GOOG) (GOOGL), and Tesla (TSLA). While the percentage of the index in big tech has likely come down over the course of 2022, it still makes up a significant chunk of the index today. I mentioned this in my January article covering Berkshire and Apple explaining why I thought it was a decent trade to sell Apple but maintain the exposure to the company through Berkshire.

Right now, $26.58 of every $100 purchased of an S&P 500 index goes straight into big tech. These index funds are technically diversified, but with over a quarter of the value in the top 8 eight tech companies, the index doesn’t get this concentrated very often. The last time it was this concentrated was in the 2000 tech bubble. Apple, as the largest piece of the index, sees nearly 7% of new money flows. This brings me to why I decided to sell my shares of Apple to buy Berkshire Hathaway.

– Quote from my January Article

While the inflows have been on autopilot over the last decade, one of the things that could spell trouble for Apple shares is what could happen if that reverses, and we start seeing outflows. The same cycle that saw Apple stock receiving a lion’s share of inflows would mean that the stock will see the most selling pressure from outflows. The indexes currently hold approximately 6.5% of their considerable assets in Apple stock. All these funds, as well as smaller S&P 500 ETFs and many other ETFs often hold Apple as the largest position in the ETF. One of the other main problems I see with Apple is the rich valuation.

Valuation

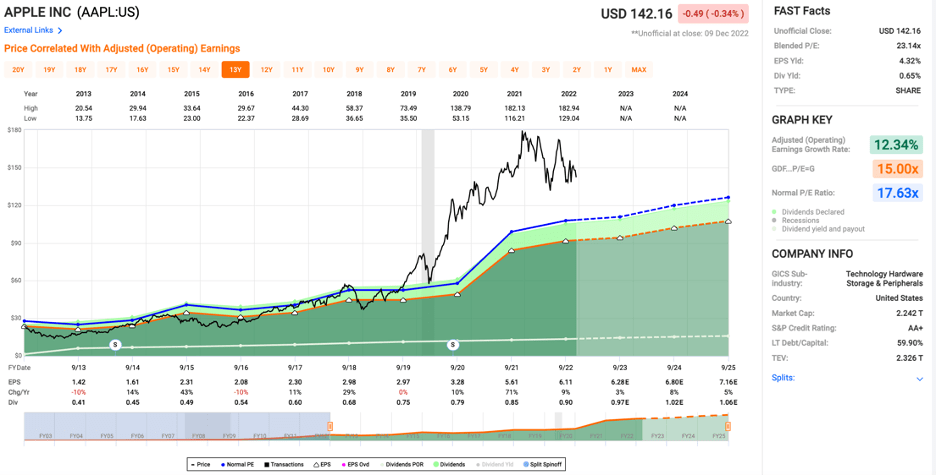

Many investors argue that Apple has earned its premium valuation, and I can understand why. It is a high margin business with a sticky product ecosystem, but I wouldn’t be buying today at the current $2.3T market cap. If we look at the last decade when Apple first started paying a dividend, shares are currently well above the average multiple of 17.6x. Shares have spent most of the last couple years well above the average multiple blue line, but I don’t see much in the way of margin of safety today at 23.1x earnings.

Price/Earnings (fastgraphs.com)

Could Apple surprise on the upside with earnings over the next couple years? Sure, but I think the supply chain problems and slowing economy could spell trouble for Apple’s earnings growth over the next couple years. After a closer look at Apple’s year end results, combined with the elevated valuation, I keep coming to the same conclusion that I did in January. If you want to own a piece of Apple, why not just own it through shares of Berkshire?

The Advantages Of Berkshire

I recently covered Berkshire in late November, including articles on the conglomerate’s three new equity stakes in Jefferies Financial (JEF), Louisiana Pacific (LPX), and Taiwan Semiconductor (TSM). I explained why Berkshire is a sleep well at night stock, and why I think the market cap will eventually be over $1T. I would recommend reading that article for an update on the equity portfolio and other factors with Berkshire.

One of the reasons I think the risk/reward is better for shareholders of Berkshire is the defensive nature of their business and subsidiaries. Apart from the large Apple holding, Berkshire has large positions in energy companies like Chevron (CVX) and Occidental Petroleum (OXY), as well as financials like Bank of America (BAC) and American Express (AXP), which should perform well in the next year or two in my opinion. On top of that, they also have the Energy subsidiary which should also do fine no matter what happens with the economy.

They also have large insurance operations and the BNSF railroad to anchor many other subsidiaries which contribute to the defensive and diversified nature of the company. You also get a company with billions in cash to put to work (or hold in bonds with rising interest rates), so I think they will have the ability to deal with an economic slowdown and they aren’t as exposed to supply chain issues or passive fund flows. By buying Berkshire instead of Apple, you get a more defensive and diversified holding than Apple at a better valuation.

Dividends & Buybacks

Apple has been the poster child for buybacks over the last decade, and it has managed to sustain solid dividend growth at the same time. In 2022, the company bought back 569M shares for $90B, an impressive feat, even for a company of Apple’s size. They have $60.7B remaining on the current authorization, and if recent history is any indication, the buybacks will continue at a rapid pace. I’m not a huge fan of the buybacks at this valuation and I would personally rather see larger dividend increases.

The yield isn’t much for investors looking for current income at 0.65%. They have consistently grown the dividend in the last decade, and they have plenty of room future raises with the low payout ratio (~15%) and cash on the balance sheet. I’m nitpicking here, but I think a better way to return capital to investors today is a larger dividend instead of buybacks. I’m fine with both, and I think that calculation would change if shares were at 15-18x earnings for example. They will also see a 1% tax on buybacks in the coming year due to the Inflation Reduction Act (a horribly named bill, by the way), so I’m curious if that starts to factor into the equation in 2023.

Conclusion

Apple is the king of the hill today when it comes to large cap tech stocks with its 2.3T market cap. It is a high margin cash cow with an impressive balance sheet, and the company has continued its massive buyback program. The 0.65% yield isn’t much, but it has consistently grown for years. These are all reasons to be bullish on the stock. However, I think these are outweighed by reasons to cautious today.

China has plenty of problems today, and with Apple’s supply chain operations in China, it could have a significant impact on the company in the next couple years. The other thing that could create selling pressure on Apple stock in the next couple years is the large funds and ETFs that hold Apple. The stock benefited over the past decade from massive and consistent inflows, but it will hurt the stock if this trend reverses and these funds are forced to sell shares. The last (and potentially most important) factor is the rich valuation at 23.1x earnings. With growth expected to slow, this is too expensive for me, and I don’t think there is a margin of safety today.

If you have owned shares for a long time, I don’t think it’s time to sell either. If shares run to $160 to above, I would start trimming, and if they head above $180, I would sell even more. One of the things that investors can do to offset the valuation risk but still get exposure to Apple is to buy shares of Berkshire Hathaway. The conglomerate owns a large Apple position along with many other stocks and subsidiaries. In my January article I argued that investors should consider selling Apple to buy Berkshire, and I think the same trade could make sense today. Even if you don’t want to sell Apple shares, investors putting new cash to work today should strongly consider buying Berkshire instead of Apple.

Disclosure: I/we have a beneficial long position in the shares of BRK.B either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.