Summary:

- Investors need to brace for a bumpy ride as Lucid’s FY23 production guidance falls woefully short, signaling the need for significant cuts in forward estimates.

- As macro headwinds remain uncertain and Tesla slashes prices, the company’s premium price point is a significant headwind.

- Lucid’s future is at stake as they could face a liquidity crunch by early 2024, leaving them high and dry without additional funding from the PIF or other stakeholders.

- Lucid’s profitability path could be further delayed as its production ramp cadence faces significant disruption.

David Becker

Lucid Group, Inc. (NASDAQ:LCID) delivered a disappointing report for its recent FQ4’22 earnings release, posting revenue and adjusted EBITDA below the consensus estimates.

However, the stunner came from its outlook for FY23, as CEO Peter Rawlinson and his team proffered a production outlook of just 12K vehicles at the midpoint of its guidance range.

Notably, it was well below the Street’s 21K estimate, suggesting that Lucid’s production ramp has suffered a significant setback. With analysts expecting Lucid to lift its revenue to $2.44B previously in 2023, investors need to expect a substantial cut, given its tepid outlook.

Therefore, it could dramatically slow down its ability to reach adjusted EBITDA profitability (previously projected to be in 2025), indicating more external financing will likely be needed before it could turn profitable.

Accordingly, management highlighted that it has $4.9B in total liquidity, which Lucid expects to be sufficient to tide it through “at least into the first quarter of 2024.”

Hence, investors will likely be looking at Lucid’s most significant shareholder, Saudi Arabia’s Public Investment Fund or PIF, to provide more funding as Lucid ramps production.

Notably, the PIF had raised its stake to 1.11B shares in FQ4 (or a 9.2% stake). The buyout rumor by the PIF that drove the hype that lifted its stock to unsustainable heights has cooled significantly.

As such, investors must remember not to chase hype, particularly such buyout rumors. Instead, focusing on execution will be highly critical for fledgling EV makers like Lucid, still struggling to move past its first 10K in annualized production.

We believe the significant miss against the 21K expected production guidance could send more investors fleeing, especially those who jumped in at the early January bottom.

Accordingly, Rawlinson highlighted production challenges, even though the supply chain disruption has abated. However, the company continues to face headwinds related to procuring the necessary automotive parts.

Management also stressed that it has a “marketing” issue, as the company plans to “broaden awareness.”

Coupled with a decline in reservations from 34K in FQ3 to 28K doesn’t augur nicely with its near-term outlook.

The company introduced its own “EV credits” scheme to bolster underlying demand as its line-up doesn’t qualify for the IRS’ scheme. However, the lack of positive commentary from management on the take-up suggests that Lucid could be facing pretty challenging underlying demand headwinds, possibly given its price point.

The company’s average selling price, or ASP based on its recent reservations update, increased to $96K from $94K previously, suggesting an improvement in the mix.

However, with the macroeconomic headwinds uncertain, and higher-end consumer spending could be hit as they traded down, Lucid’s premium price point could prove to be a significant stumbling block.

Bulls could argue that Tesla’s (TSLA) recent price cuts may not directly affect Lucid’s pricing strategies as they operate in different segments. However, despite that, Tesla has seen an improvement in its order flow. Therefore, we cannot rule out the potential for further trade-down by higher-end consumers with persistent inflationary headwinds.

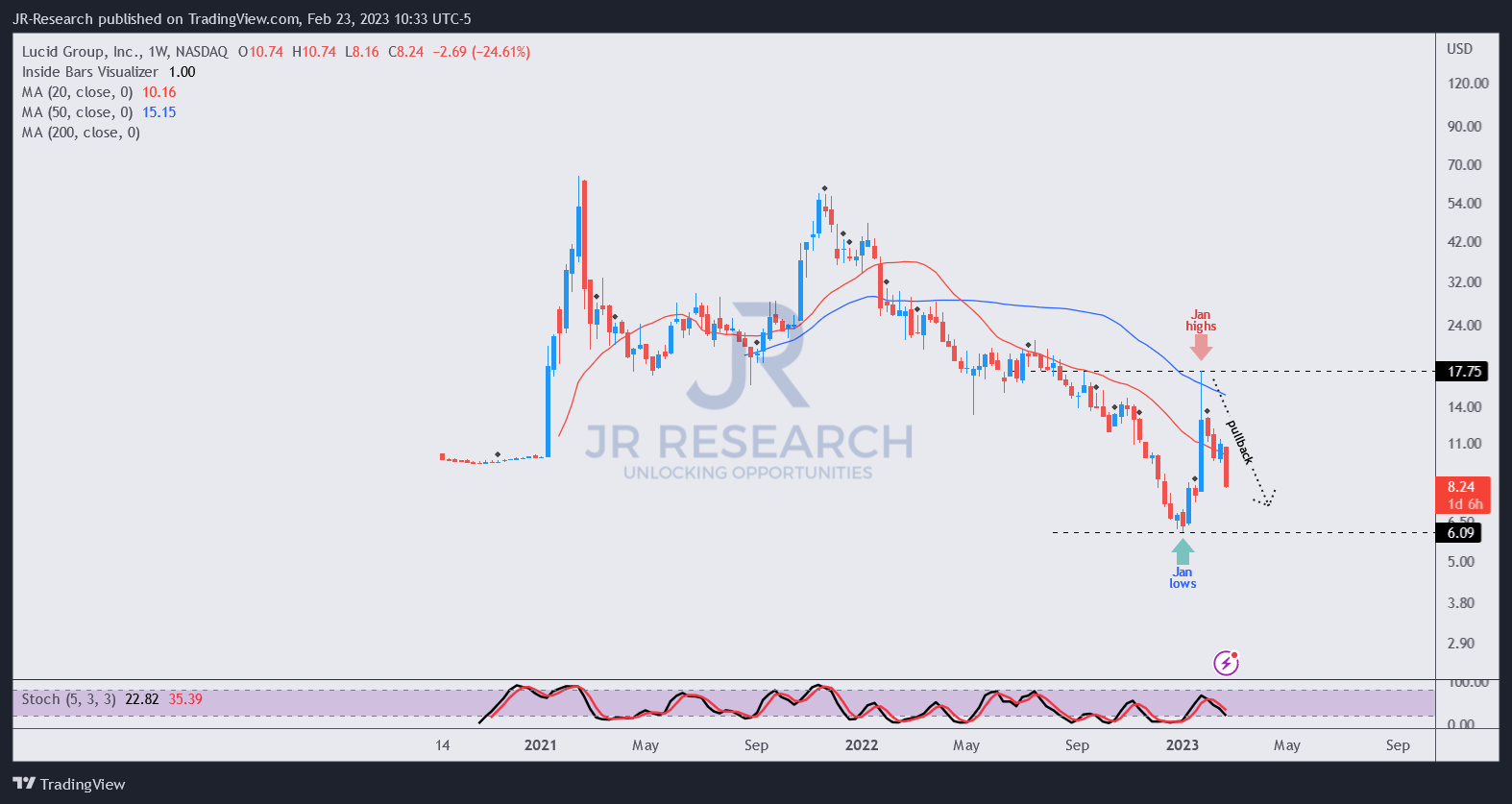

LCID price chart (weekly) (TradingView)

With that in mind, investors shouldn’t be surprised that LCID is down more than 17% at writing, as the market likely anticipated further estimates cuts by analysts, given its disappointing guidance.

However, the false upside breakout or bull trap that formed in early January had already rejected further buying advances. Therefore, the selloff this week merely continued the downshift over the past four weeks, as investors who bought the dips at the start of the year likely took profits astutely.

We believe short-sellers could also have reloaded, seeing the potential for a decisive breakdown of LCID’s momentum toward its January lows.

With the pullback in full swing, we encourage investors to continue waiting on the sidelines as it’s not time to buy the pullback yet. Constructive consolidation should be observed, indicating seller exhaustion before investors consider a potential speculative buying opportunity on LCID.

Rating: Hold (Reiterated, but on the watch for a rating change).

Disclosure: I/we have a beneficial long position in the shares of TSLA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Are you looking to strategically enter the market and optimize gains?

Unlock the key to successful growth stock investments with our expert guidance on identifying lower-risk entry points and capitalizing on them for long-term profits. As a member, you’ll also gain access to exclusive resources including:

-

24/7 access to our model portfolios

-

Daily Tactical Market Analysis to sharpen your market awareness and avoid the emotional rollercoaster

-

Access to all our top stocks and earnings ideas

-

Access to all our charts with specific entry points

-

Real-time chatroom support

-

Real-time buy/sell/hedge alerts

Sign up now for a Risk-Free 14-Day free trial!