Summary:

- I continue to consider McDonald’s as a high-quality company.

- However, reflecting on no/little growth, a rich valuation, and a competitive yield when investing in US treasuries, I have a hard time arguing why McDonald’s is a ‘Buy’.

- Anchored on fundamentals, I calculate a fair implied share price for MCD equal to $213.74/share.

Justin Sullivan

Thesis

I have previously argued that McDonald’s (NYSE:MCD) is neither a growth stock nor a value stock. But a quality stock. And the company’s December quarter confirmed the thesis: In Q4 2022, McDonald’s neither grew attractively nor did the company post attractive profitability as compared to the firm’s equity value. However, as expected, earnings remained resilient despite the ongoing macroeconomic challenges.

Reflecting on McDonald’s Q4 and overall 2022 results, I continue to believe that MCD stock is a ‘Hold’ at best – given valuation concerns. Personally, I value MCD stock with a residual earnings model and calculate a fair implied share price of $213.74.

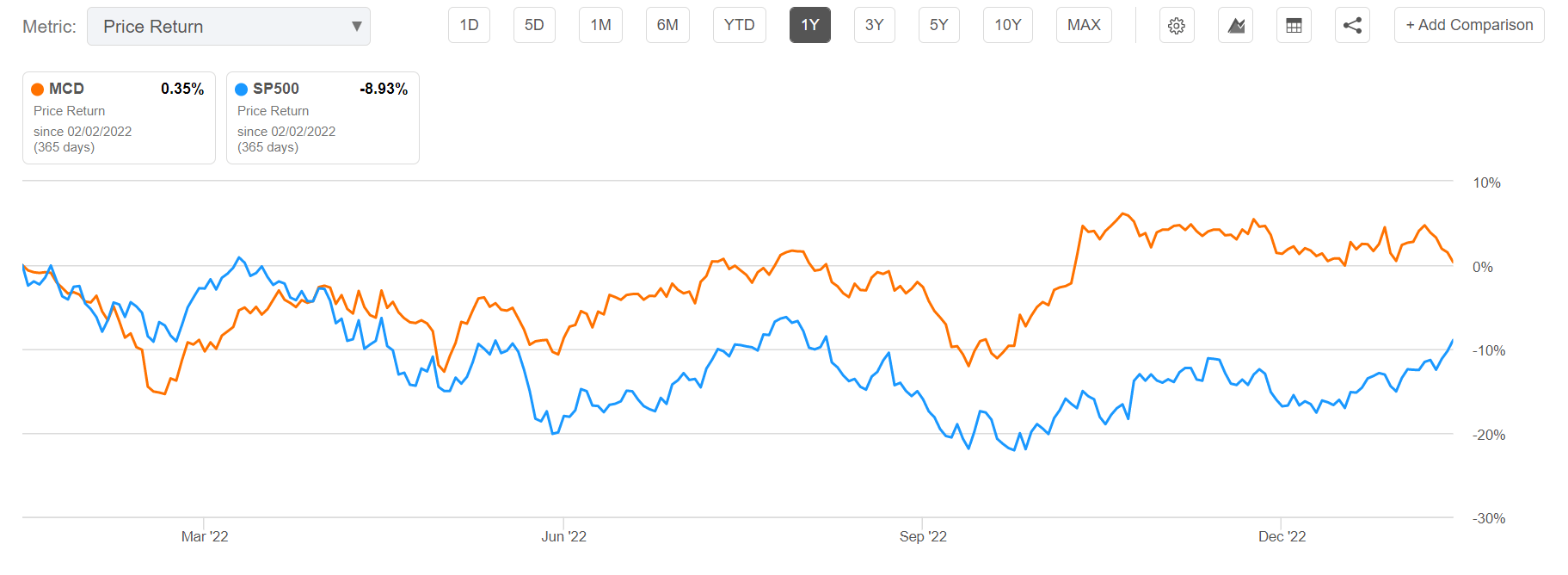

For reference, McDonald’s continues to protect investor capital in times of equity markets stress: MCD trades approximately flat for the past twelve months, as compared to a loss of close to 9% for the S&P 500 (SPY).

Seeking Alpha

McDonald’s December Quarter

As expected, McDonald’s delivered a solid performance in the December quarter, despite a challenging macroeconomic backdrop. During the period from September to end of December, MCD generated total revenue of about $5.9 billion, reflecting a topline contraction of approximately 1% as compared to the same period one year earlier. With regards to profitability, the firm generated close to $2.6 billion of operating income, as compared to $2.4 billion in the period of 2021, a 16% year over year growth. Similarly, net earnings increased by about 19% year over year, to $1.9 billion ($2.59/share).

MCD Q4 reporting

Notably, McDonald’s beat analyst consensus estimates for Q4 with regards to both revenues and earnings. According to data collected by Refinitiv, analysts had estimated about $5.75 billion of revenues ($180 million beat), and EPS close to $2.45/share (14 cents beat).

Closing A Solid 2022

For the FY 2022, the world’s leading fast food brand recorded $23.2 billion of group revenues and $9.3 billion of operating income. After accounting for interest and tax expenses, earnings netted $6.2 billion. While the result is considerable, I would like to point out that as compared to 2021, revenues remained approximately flat, while operating income and net earnings decreased by about 10% and 18% respectively.

McDonald’s closed FY 2022 with a somewhat levered balance sheet: As of December 31, the company recorded $2.6 billion of cash and cash equivalents/ short term investments, as compared to approximately $48 billion of total financial debt. However, reflecting on $7.4 billion of operating cash flow, the financial leverage should be easily sustainable, in my opinion.

Difficult To Argue An Investment Thesis

The problem I am having with MCD stock is that it is difficult to argue an investment thesis for the world’s leading fast food brand. To simplify, I could see three possible arguments that support a thesis–value, growth, safety–neither of which makes MCD stock a preferred choice.

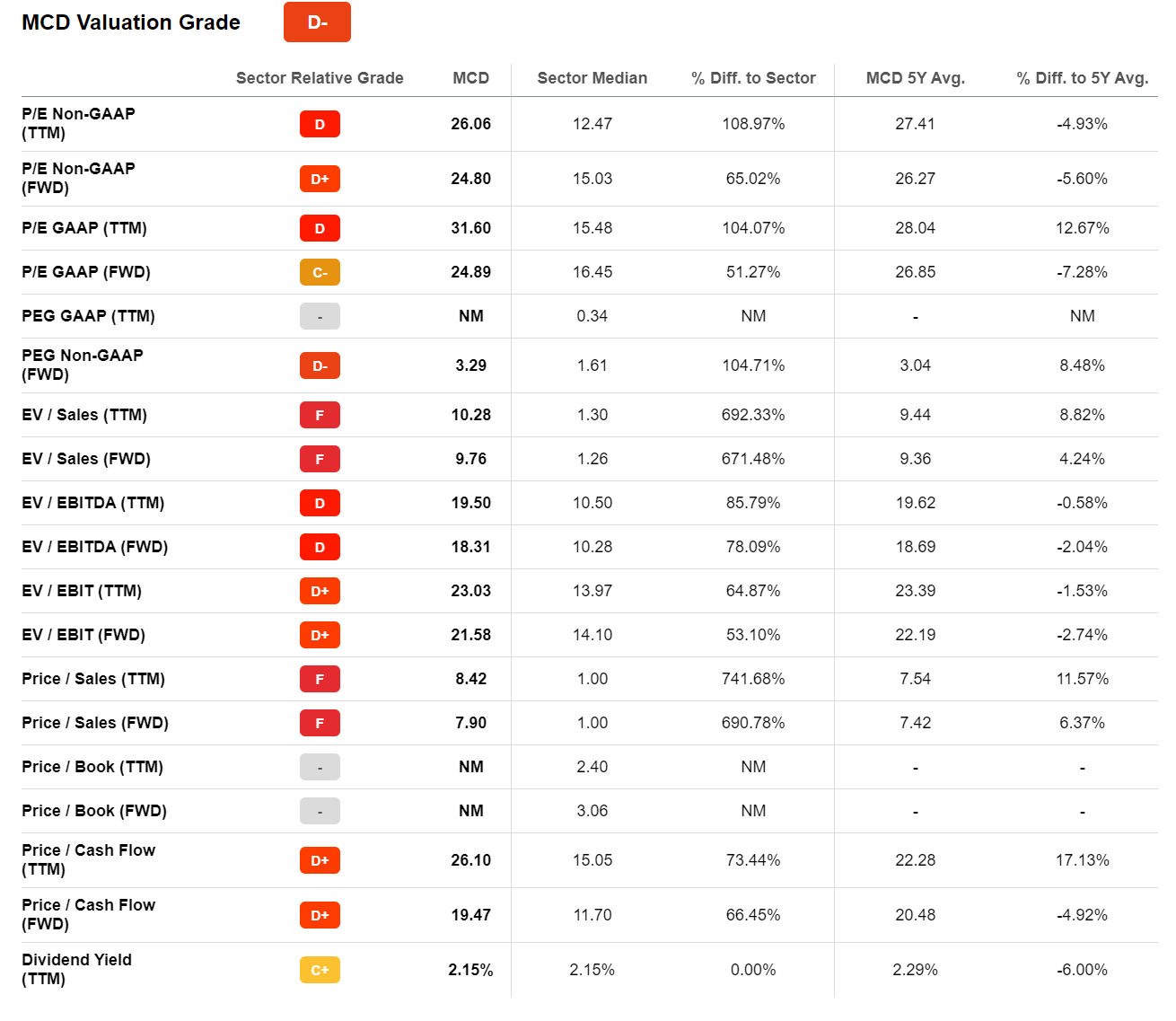

First, let’s discuss value: Priced at a FWD EV/EBIT of approximately x21, which is represents a 51% premium to the sector median, McDonald’s earnings are certainly not priced cheap. But independent of earnings, a similar argument can be structured for the company’s sales and book value metrics.

Seeking Alpha

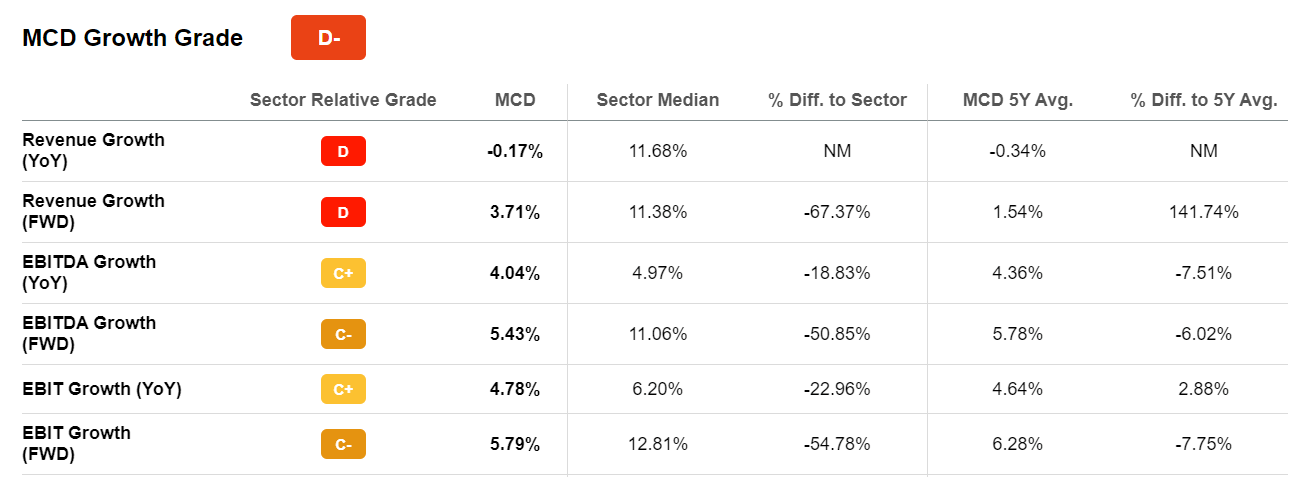

McDonald’s rich valuation may be justified in context of above-industry growth. Growth, however, is not one of McDonald’s strength. In fact, during the past five years, McDonald’s has expanded topline at a negative 0.35% CAGR. In addition, McDonald’s profitability has expanded at rates below the relevant industry median, with McDonald’s 5y EBIT growing at a 4.64% CAGR, as compared to a 6% CAGR as the industry average.

As a reminder, in 2022 as compared to 2021, McDonald’s revenues and net earnings were flat and decreased by 18% respectively.

Seeking Alpha

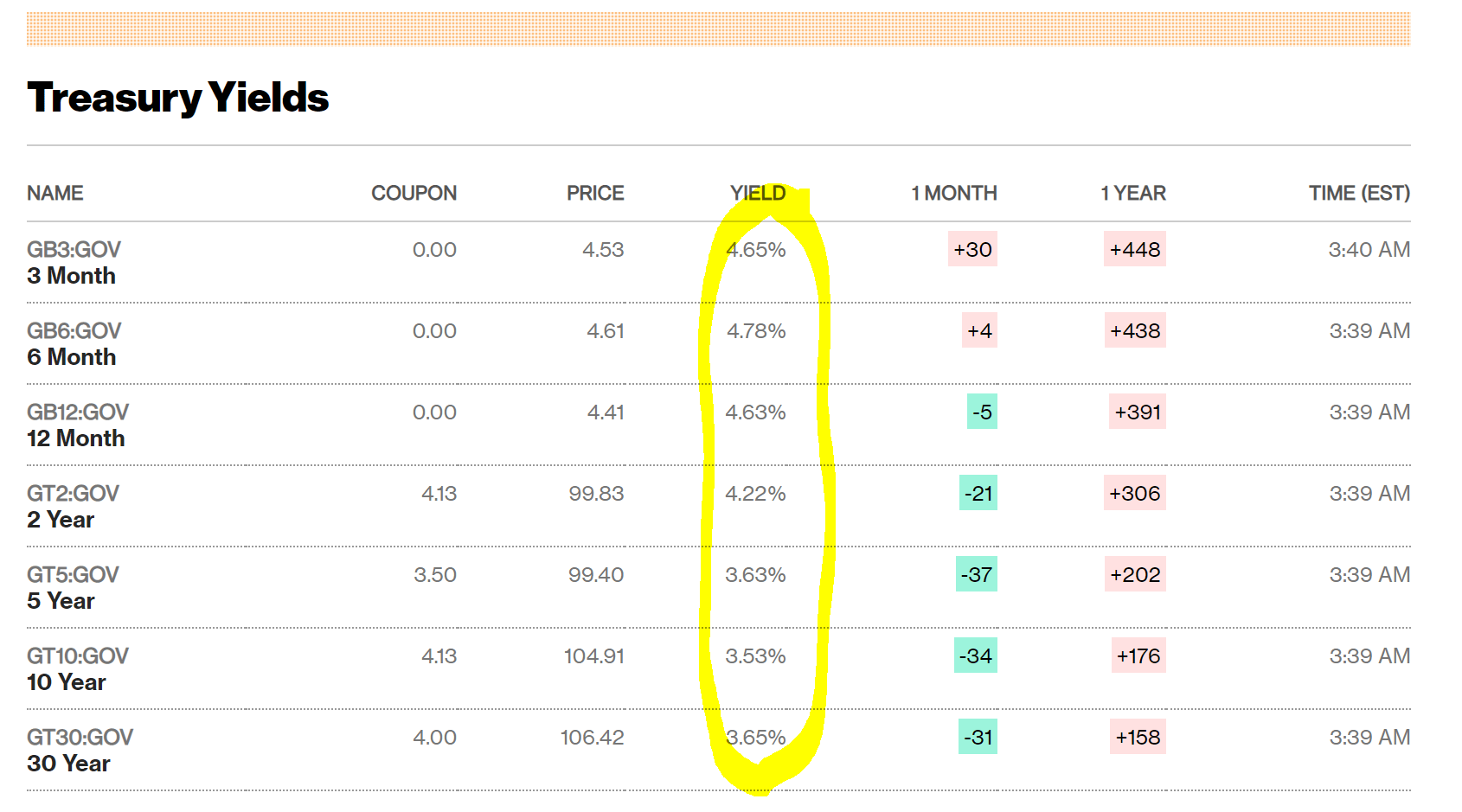

Finally, McDonald’s valuation premium would be justified if an investor considers paying for an earnings safety premium. However, if we assume that McDonald’s equity return is the ratio of shareholder distributions divided by market cap, then we can calculate MCD’s equity yield at 4.4% (2022 distributions composed of $4.2 billion of dividends, and $3.9 billion of share repurchases, as compared to a $182 billion market capitalization). With that frame of reference, investors should consider that the risk free rate, as defined by the US treasury notes, currently offers a yield equal to what McDonald’s offers. And thus, paying for McDonald’s safety premium is arguably not a very sophisticated choice.

Bloomberg

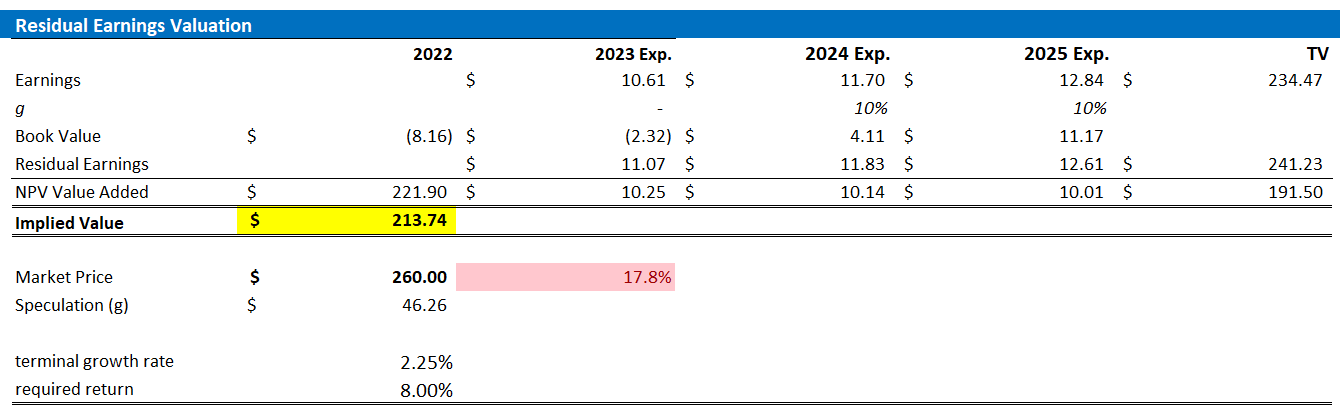

Valuation: Set Target Price at $213.74

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my MCD stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor MCD’s cost of equity at 8%–reflecting the quality thesis.

- For the terminal growth rate after 2025, I apply a 2.25%, which is approximately in line with long-term nominal GDP growth.

Given these assumptions, I calculate a base-case target price for MCD of about $213.74/share, which implies that MCD could be overvalued by as much as 17.8%.

Analyst Consensus EPS; Author’s Calculation

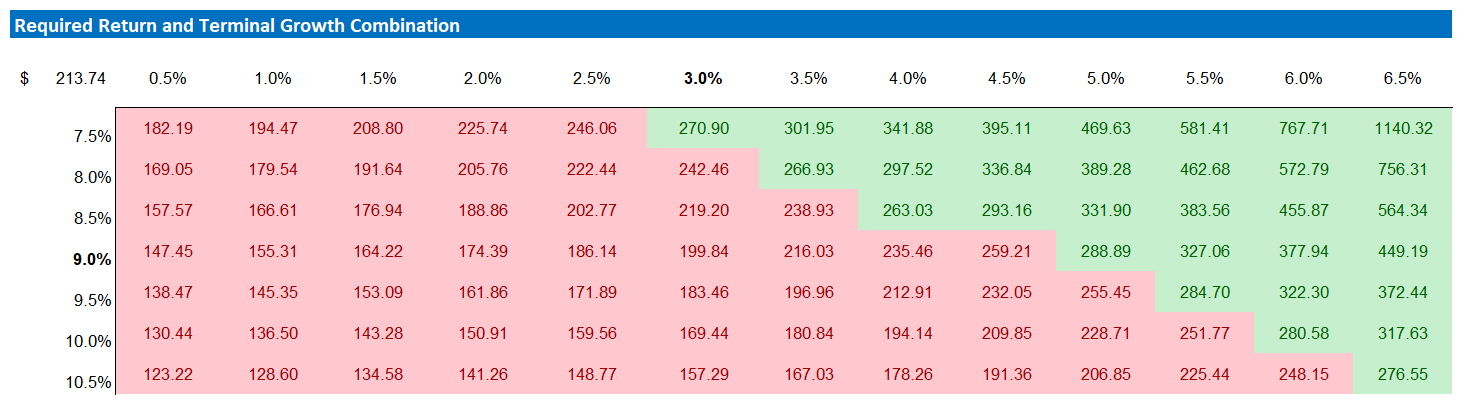

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of MCD’s cost of equity and terminal growth rate, I have constructed a sensitivity table.

Analyst Consensus EPS; Author’s Calculation

Conclusion

I continue to consider McDonald’s as a high-quality company. However, reflecting on no/little growth, a rich valuation, and a competitive yield when investing in US treasuries, I have a hard time arguing why McDonald’s is a ‘Buy’. Moreover, looking at McDonald’s fundamentals and expected earnings through 2025, I calculate a fair implied share price for MCD equal to $213.74/share. In my opinion, McDonald’s is a ‘Hold’ at best.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: not financial advice