Summary:

- Meta’s stock has come back roaring since bottoming in November.

- Estimates have gone up consistently across the board.

- At 16 times 2024 earnings, the stock may still be undervalued.

- Technical indicators are in favor of further short-term upside.

Kira-Yan

What a turnaround it has been for Meta Platforms Inc.’s (NASDAQ:META) stock over the last 4 months. Since losing about 75% from its peak to about $88 in November 2022, the stock has gained more than a 100% in 4 months and nearly 50% Year-To-Date.

In hindsight, I made one perfect call on Meta’s bottom when the company announced its layoffs and one not-so-perfect call on downgrading the stock after it bounced almost 50% in two months. Since the downgrade article, Meta’s stock has gone up another 30%. To be fair (to myself), this 30% run was largely buoyed by the company’s stock buyback news. Anyway, my recent score on Meta is 1 each. So, this article may serve as the tie-breaker and I am providing five reasons below as to why I am upgrading Meta Platforms stock to a “Buy” rating. Let us get into the details.

Estimates Looking Up

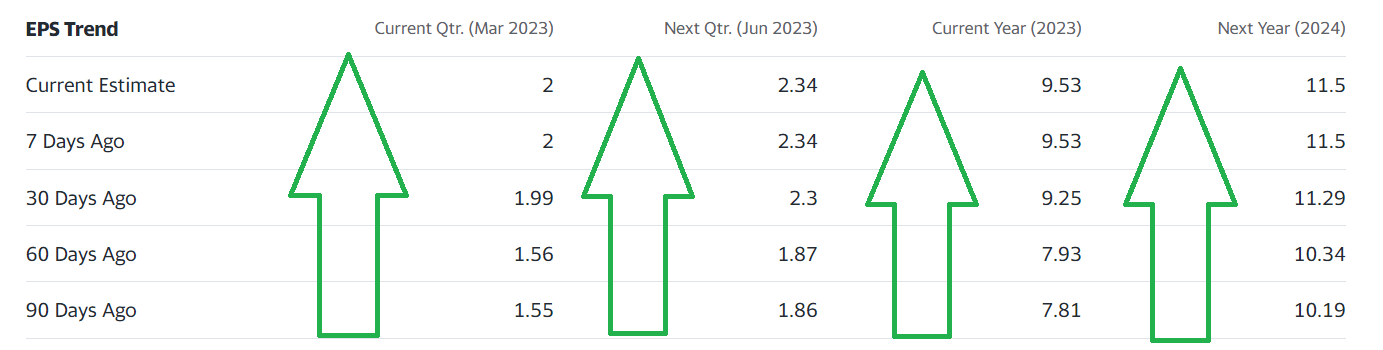

When I downgraded the stock to a “Hold” in January, FY 2023’s EPS estimate was $7.88. That number has since gone up to $9.53 as shown below. That’s a 20% increase. In addition, FY 2024’s estimates currently stand at $11.50, which indicates a forward multiple of 16 based on the current stock price. 16 times 2024’s multiple doesn’t sound that bad, especially when you consider the S&P 500 is currently trading at a multiple of 22 with earnings expected to be down for this year at least, if not next year too.

The upward EPS revision is across the board as shown below.

EPS Estimate (Yahoo Finance)

Macro Looking Up

Of all the sections in this article, this one is the most flaky as inflation and The Fed are playing cat and mouse with the market. Sometimes, within the same week, we get rallies or sell offs depending on how the CPI, PPI, and Jobs numbers come out and more importantly how those numbers are deciphered by each regional Fed president who may speak to the media. While Atlanta Fed’s comments sent the market higher on Friday, San Francisco’s comments over the weekend call for more tightening.

But what is undeniable is that peak inflation is almost definitely behind us. While it may take some months and even years for The Fed to reach its 2% inflation target, strong companies tend to turn around first, which seems to be the case with Meta’s 2023 and 2024 estimates getting stronger as days go by.

Further Cost-Cutting

Meta’s initial 11,000 layoffs made the headlines last year and rightly so. At that time, the company indicated no more layoffs will be needed. However, rumors are swirling around that the company is planning more layoffs, with a special focus on flattening the organizational structure, reducing the number of layers between CEO Mark Zuckerberg and the interns. This may not be a bad idea as most large corporations tend to get fat in the middle (well, who doesn’t?).

“Meta plans to push some leaders into lower-level roles without direct reports, flattening the layers of management between Meta CEO Mark Zuckerberg and the company’s interns, according to a person familiar with the matter…”

The report also talks about the company finding cheaper ways on projects it doesn’t want to cut off entirely. While Meta’s Communications director denied the story, another spokesman from the company said this:

“We closed last year with some difficult layoffs and restructuring some teams,” Zuckerberg told investors earlier this month. “When we did this, I said clearly that this was the beginning of our focus on efficiency and not the end.”

I don’t know which version is true as of now but I tend to believe there is no fire without smoke, especially around large corporations like Meta Platforms. As a shareholder, any efforts to cut down on excesses is welcome, especially given how bloated many tech companies became in the last few years.

TikTok and Advertising

U.S House recently passed a bill that now gives President Joe Biden the power to ban TikTok entirely should he choose to. With about 30 States having banned TikTok already, a Federal level ban may not be as powerful as a fresh ban on all 50 States. But the passing of the bill is nonetheless a positive sign for Meta as the company is expanding on its Reels features including increasing the length of Reels to up to 90 seconds and enabling creation of templates to churn out content similar to recently watched Reels.

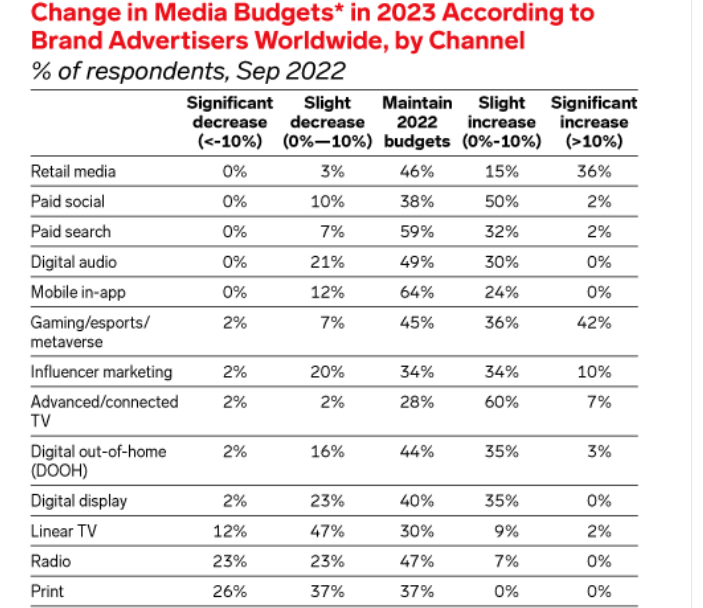

While advertising in general is expected to slow down in 2023, Meta’s Q4 earnings showed advertising revenue declined by “just” 4%. In addition, several factors are in favor of Meta and other companies that heavily rely on advertising as covered in this report.

- 54% of companies plan to increase their marketing budget, while 29% expect to remain flat. That means only about 15% of companies are expecting to reduce their advertising budget.

- 66% of the marketing budget is allocated to digital channels, which favors the likes of Meta and Alphabet (GOOG) (GOOGL) heavily.

- Finally, the table below shows most of the reduction in budgets hits the more traditional mediums like Print and Radio. In particular, paid social, paid search, and mobile-in-app spending are either expected to remain the same or slightly increase in 2023. This is in sync with Meta’s 2022 Q4 numbers, with only a slight decrease but not as bad as feared.

2023 Marketing (insiderintelligence.com)

Technical Indicators

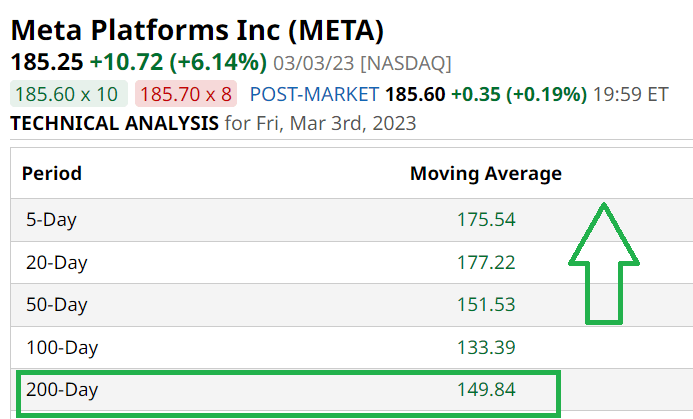

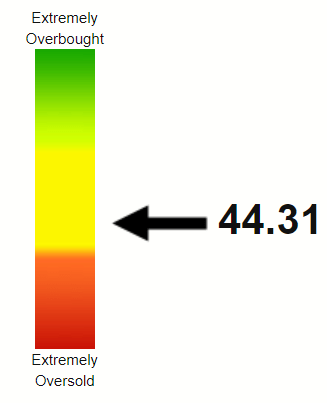

From a technical perspective, Meta’s stock is trading well above the all important 200-Day moving average, suggesting a new strong base has been established for the stock to build on. Equally as important is the fact that the stock has managed to break away from all the commonly used moving averages without getting overbought. The current Relative Strength Index (“RSI”) of 44 confirms this while also indicating more room to the upside before the stock becomes overbought.

Meta Moving Avgs (Barchart.com) META RSI (Stockrsi.com)

Conclusion

In hindsight, I was clearly too early to press the “Hold” button on Meta Platforms, Inc. However, Meta has many factors going in its favor currently including a more disciplined approach, improving estimates, improving technicals, and improving macroeconomic conditions.

While Meta deserves a premium for higher growth prospects in general, the company undoubtedly faces challenges as it tries to find the next growth driver while navigating issues around reduced advertising budgets. In short, I am in agreement with the Median price target of $215 as things stand now, as that would push Meta’s forward multiple based on 2023’s forward EPS to about 22, which should bring it in line with the market’s multiple.

Disclosure: I/we have a beneficial long position in the shares of GOOG, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.