Summary:

- Based on a FCF valuation analysis of 32 of the largest companies in the S&P 500, Meta is at least 30% undervalued.

- Meta Platforms continues to see engagement increase across its platforms, and more than 1/3rd of the global population utilizes its applications.

- META has some tailwinds including $40 billion of authorized buybacks which could boost EPS and a ban on TikTok which could be a revenue driver.

Kevin Dietsch

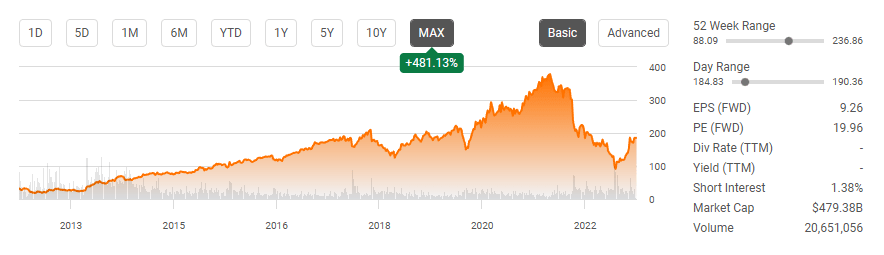

Meta Platforms (NASDAQ:META) was a market favorite over the past decade, appreciating by 1,192.92% from its IPO in June 2012 to the fall of 2021. Despite negative headlines and being hauled in front of congress and congressional committees, shares of META appreciated from $31.91 to $380.66. Over the next 13 months, from September 2021 to October 2022, the wheels came off, and META lost -76.94% of its value, falling from $382.05 to $88.09 for a loss of $293.96 per share. The downward decline was immense and unpleasant for many shareholders, such as myself. Things have been looking positive for META lately, as Mr. Zuckerberg has been making tough decisions regarding costs, slashing prices for VR headsets, and realigning his focus on profits. The market has been receptive, and over the past 4 months, shares of META have appreciated 104.12% as they have gone from $88.91 to $181.43 for an increase of $92.57 per share. Despite shares more than doubling, they are still off their highs by a considerable amount, and I feel shares are at least 30% undervalued and could finish 2023 well above $250 per share.

Seeking Alpha

META produced a solid Q4 which consisted of increased engagement

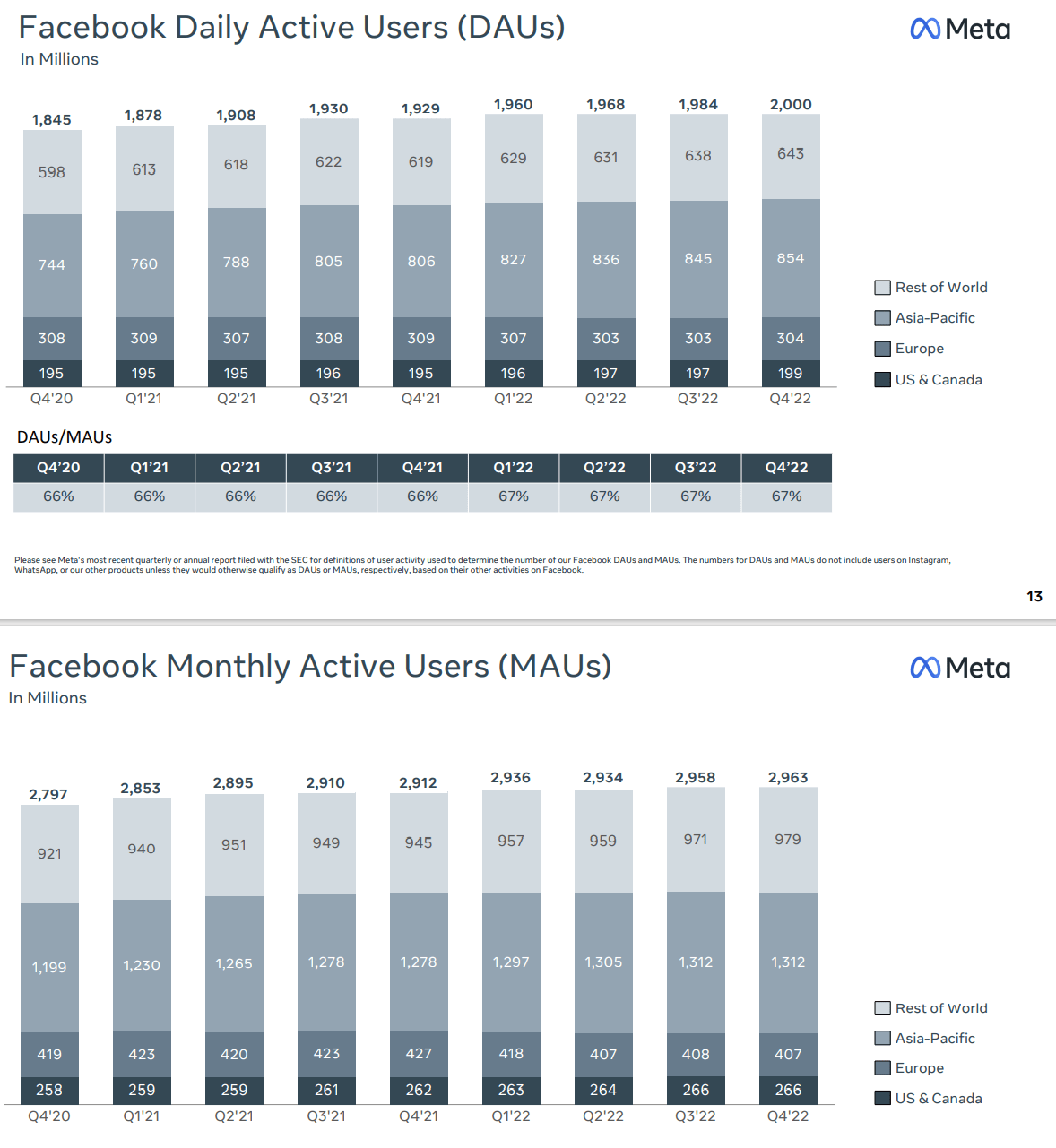

Facebook isn’t dead, Instagram isn’t slowing, and WhatsApp is still utilized. META reached more than 3.7 billion people monthly across its family of apps in 2022. Meta’s Family Daily Active People (DAP) increased by 1.02% QoQ to 2.96 billion people, while Family Monthly Active People (MAP) increased by 0.81% to 3.74 billion people. From an active user perspective, Daily Active Users (DAU) increased by 0.81% to 2 billion people, while Monthly Active Users (MAU) increased to 2.96 billion, up 0.17% MoM. There is no shortage of engagement across META’s family of apps, as more than 1/3rd of the global population utilizes its platforms each month. In Q4 2022, ad impressions delivered across META’s apps increased 23% YoY. In 2022 META saw its Ad impressions increase 18% YoY.

These numbers illustrate how embedded META’s family of applications continues to be throughout our civilization. More than a decade later of going public, engagement is still growing at META. META is a global brand that continues to play a critical role in how communication and connection is achieved in 2023. If there was a drop off in engagement, there would be a serious issue because that could correlate to lower revenue and earnings potential. That’s not the case , and over the previous 2 years, META has gained 155 million users. With the looming TikTok ban META’s applications could see a boost in engagement in both time spent using their platforms in addition to an increased user count in the U.S. This would probably provide a boost to their earnings potential as 46.27% of their advertising revenue ($52.58 billion / $113.64 billion) came from the U.S ad Canada in 2022.

Meta Platforms

META is taking its medicine and focusing on profitability

On the Q4 conference call, Mr. Zuckerberg was clear that 2023 would be the year of efficiencies. META closed out 2022 with a large round of layoffs and restructured some teams to optimize their operations. Mr. Zuckerberg went as far as to indicate that this would be the beginning of META’s focus ad not the end regarding efficiency. The next step would be flattening META’s org structure and removing layers of middle management in addition to deploying A.I. tools to boost productivity from engineering. META will also focus on capital allocation regarding CapEx ad be proactive about cutting projects that aren’t performing. Recently on March 6th 2023, a report was released that META is set to cut thousands of additional jobs as part of a newly planned round of layoffs. META had cut 13% of its workforce, roughly 11,000 people in November of 2022, and thousands of more employees will supposedly be let go as early as this week. META has reportedly asked directors and V.P.s for lists of employees that could be cut and are tied to financial targets senior leadership has put in place.

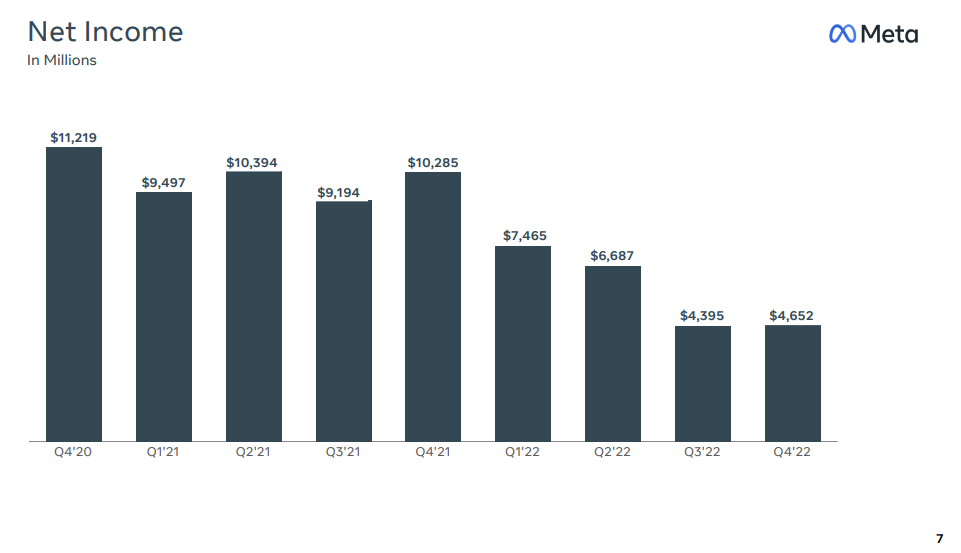

META is projecting that in Q1 of 2023, they will generate between $26 billion to $28.5 billion in revenue, which takes into consideration approximately 2% headwind in foreign currency due to exchange rates. In Q1 2022, META generated $27 billion in revenue, so if they are able to achieve $28 billion in Q1 of 2023, that would be a YoY increase of 3.7%. What’s interesting is that META has provided full-year guidance on the expenses side. META has lowered their total expense guidance from $94 billion to $100 billion to $89 billion to $95 billion due to slower anticipated growth in payroll expenses and cost of revenue. META has also lowered its CapEx spending from $34 billion to $37 billion to $30 billion to $33 billion. For all of the negative publicity in 2022, META was still wildly profitable, driving net income of $23.2 billion, which is a profit margin of 19.9%.

Currently, how large of a success VR/AR and the Metaverse will be is purely speculation. What isn’t speculation is that there are now over 200 apps running on META’s V.R. devices that have generated in excess of $1 million in revenue. META plans on bringing its discovery engine, ads, business messaging, and generative A.I. to the future platforms for the Metaverse. META has also cut the price of the Quest Pro to about $999 and reduced the price of the Quest 2 256 GB model to about $429. The Metaverse won’t be a winner take all situation, but it could be a winner-take-most scenario. META is a clear leader in the space, and with the amount of capital their allocating, Reality Labs could be a huge success in the future.

Meta Platforms

I believe META is undervalued by roughly -32%

built a model on how I like to determine a company’s fair market value. Some may agree, and some may not. I start with the total equity of a company. Total equity is simply total assets minus total liabilities. This is my baseline because if a company was to dissolve itself, theoretically, the total equity is what would be left for the shareholders to chop up among themselves after all liabilities are zeroed out. After the baseline for total equity is established, I look toward profitability, specifically FCF. I look at the closest peers, and similar-sized companies to find the average multiple on FCF the market is valuing companies at. Then I will add the total equity by the company’s current FCF multiplied by the market multiple to determine a fair value for the company to determine if it’s under or overvalued.

Steven Fiorillo, Seeking Alpha

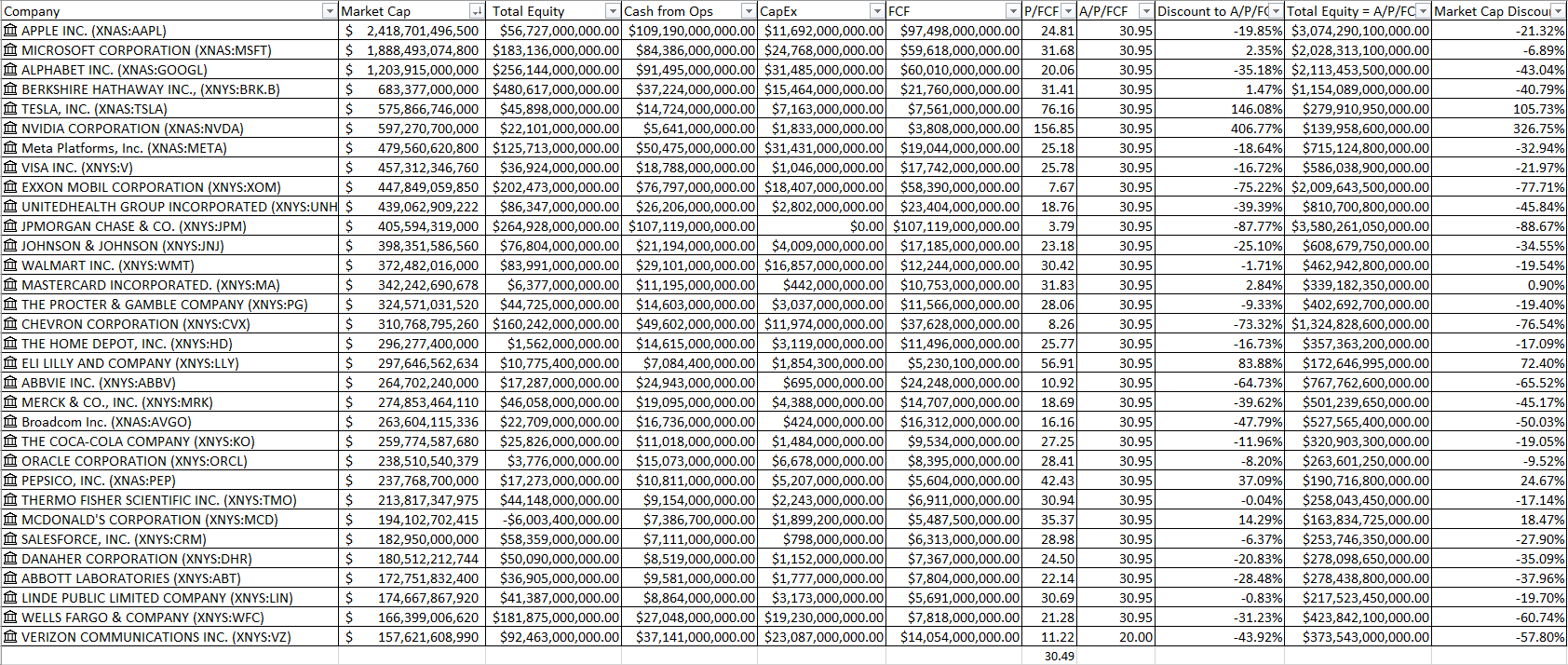

In META’s immediate peer group of Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Tesla (TSLA), and NVIDIA Corporation (NVDA), the average price to FCF is 55.79x. I didn’t use Amazon (AMZN) because they have negative FCF. META trades at the 2nd lowest price to FCF at 25.18x of this peer group. Using the average P/FCF plus equity, META should have a market cap of $1.19 trillion, making it -59.64% undervalued based on its current market cap. Now, I want to also look at META vs. the largest companies in the S&P 500, so I compared META in the same fashion to 32 of the largest companies. In addition to the immediate peer group I added Berkshire Hathaway (BRK.B), Visa (V), Exxon Mobil (XOM), UnitedHealth (UNH), JPMorgan Chase (JPM), Johnson & Johnson (JNJ), Walmart (WMT), Mastercard (MA), Procter and Gamble (PG), Chevron Corporation (CVX), Home Depot (HD), Eli Lilly (LLY), AbbVie (ABBV), Merck & Co. (MRK), Broadcom (AVGO), Coca-Cola Company (KO), Oracle (ORCL), PepsiCo (PEP), Thermo Fisher (TMO), McDonald’s (MCD), Salesforce (CRM), Danaher (DHR), Abbott Labs (ABT), Linde (LIN), and Wells Fargo (WFC) to my analysis.

Steven Fiorillo, Seeking Alpha

The larger peer group has an average P/FCF of 30.49x, significantly lower than the immediate peer group average of 55.79x. META currently trades at a -18.64% discount to the peer group average P/FCF as their P/FCF is 25.18x. When META’s equity is combined with the average P/FCF multiple it creates a market cap of $715.12 billion which puts its current market cap at a -32.94% discount. I have selected companies across each sector, and there is little to no reason in my mind why META should be trading at this large of a discount.

$40 billion in buybacks will increase shareholder value and should increase EPS

In Q4 of 2022, META repurchased $6.91 billion of their common shares, bringing their repurchases to $27.93 billion in 2022. META announced they were increasing their buyback authorization by $40 billion. With a current market cap of $479.56 billion, META would be repurchasing an additional 8.34% of its common shares. At the rate META repurchased shares in 2022, they could fulfill this repurchase authorization over the next 2 years.

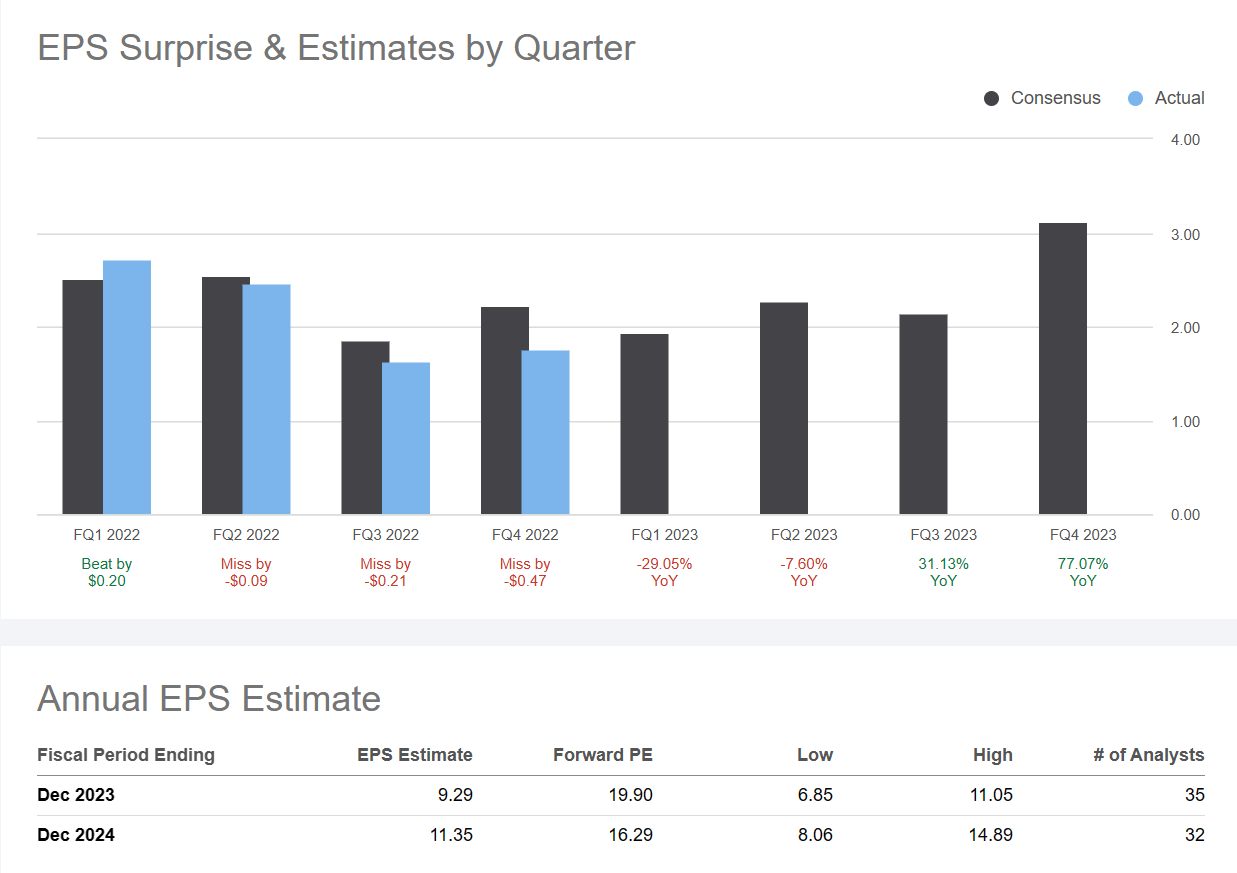

When people think about value they usually associate it with price per share. Another way to look at it is what your shares represent. In 2022, META generated $8.63 per share of EPS and had 2.61 billion shares outstanding. If META buys back 8.34% of the common shares and still generates the same earnings as they did in 2022, their EPS would increase to $9.68 without adding a single dollar of earnings. This is why buybacks are so powerful because they increase EPS and increase the amount of revenue and EPS that each share is entitled to, granted that revenue and earnings don’t decline YoY. The analysts are already estimating that META will generate $9.29 of EPS in 2023 and $11.35 of EPS in 2024. Depending on how quickly META repurchases shares, these estimates could be low and META could be setting up for some interesting earnings beats in the future.

Seeking Alpha

Conclusion

I believe shares of META are undervalued by at least 30%. When I look at the largest companies in the S&P 500, the average P/FCF is 30.49x, and META trades at 25.18x. META still generates over $20 billion annually of pure profit, and Mr. Zuckerberg has made it clear that profitability is front and center. Between cost efficacy measures such as layoffs and prioritization of projects in addition to $40 billion of additional buybacks, META could exceed analyst estimates for EPS, causing the share price to increase. If TikTok gets banned in the U.S it will create a huge tailwind for shares of META. As it stands, I think Meta is at least 30% undervalued prior to any growth in 2023. Engagement clearly isn’t declining, and META is an exciting name for the remainder of the year.

Disclosure: I/we have a beneficial long position in the shares of META, AAPL, GOOGL, TSLA, AMZN, XOM, KO, VZ, ABBV, ORCL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer: I am not an investment advisor or professional. This article is my own personal opinion and is not meant to be a recommendation of the purchase or sale of stock. The investments and strategies discussed within this article are solely my personal opinions and commentary on the subject. This article has been written for research and educational purposes only. Anything written in this article does not take into account the reader’s particular investment objectives, financial situation, needs, or personal circumstances and is not intended to be specific to you. Investors should conduct their own research before investing to see if the companies discussed in this article fit into their portfolio parameters. Just because something may be an enticing investment for myself or someone else, it may not be the correct investment for you.