Summary:

- Micron Technology, Inc. has been experiencing massive losses and a decline in performance, but the market has been kind to the stock.

- The company has cut spending and has been taking pricing action.

- The stock is facing heavy resistance at $70, and the company’s performance in fiscal Q4 will be crucial for its future outlook.

- Micron stock is likely to fall if this downturn is prolonged, which it may be.

ImagineGolf/E+ via Getty Images

One popular ticker among our traders and members remains Micron Technology, Inc. (NASDAQ:MU). Unfortunately, the company is experiencing some losses this year. It has been a palpable decline in performance. However, the market has been pretty kind to the stock, despite the lack of performance. Generally speaking, better days are ahead. Of course, there has been a massive tech rally in 2023 driven by the power, if not the euphoria from, the prospects of A.I. and what it means for the semiconductor industry. While better days are ahead, we could see price erosion again here in shares of Micron if it cannot achieve the low bar it has set for itself.

Micron has of course cut spending in various areas across the company to combat the decline in sales. Cutting expenses can help the bottom line, but we want to ensure it does not cut into growth. The company is raising prices to help its sales figures. This comes as we just saw semiconductor sales down 12% globally year-over-year, but up from July. Well, recently we got a nice update following Micron’s fiscal Q3 earnings, but the year-end fiscal earnings will be out in a few short weeks. In this column, we discuss the key metrics from Q3 and what you should watch for Q4.

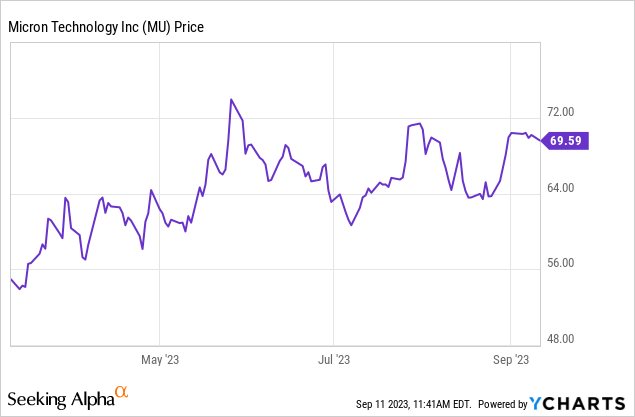

Micron stock seeing heavy resistance at $70

On the downside, Micron successfully held the $50 level, helped in large part by sector strength in our opinion. But on the upside, $70 has been a bit of a wall. The stock could break through if guidance is strong when earnings are reported. We think the company will eke out profits in the coming fiscal year, but for fiscal 2023, it has been a palpable downturn.

Folks, the key metrics have declined badly. It is a fact, regardless of if you are a bull or a bear. The company will lose money for the fiscal year. The fact is some companies are simply better in the space. But can Micron turn it around? The answer is a yes, and steps have been taken to preserve profit, as noted above. Both DRAM and NAND pricing were hit hard by the rather cyclical nature of the sector, but have since stabilized. Shares have been a bit rangebound. Let us talk about new expectations and what we are looking for here following the performance in fiscal Q3, and ahead.

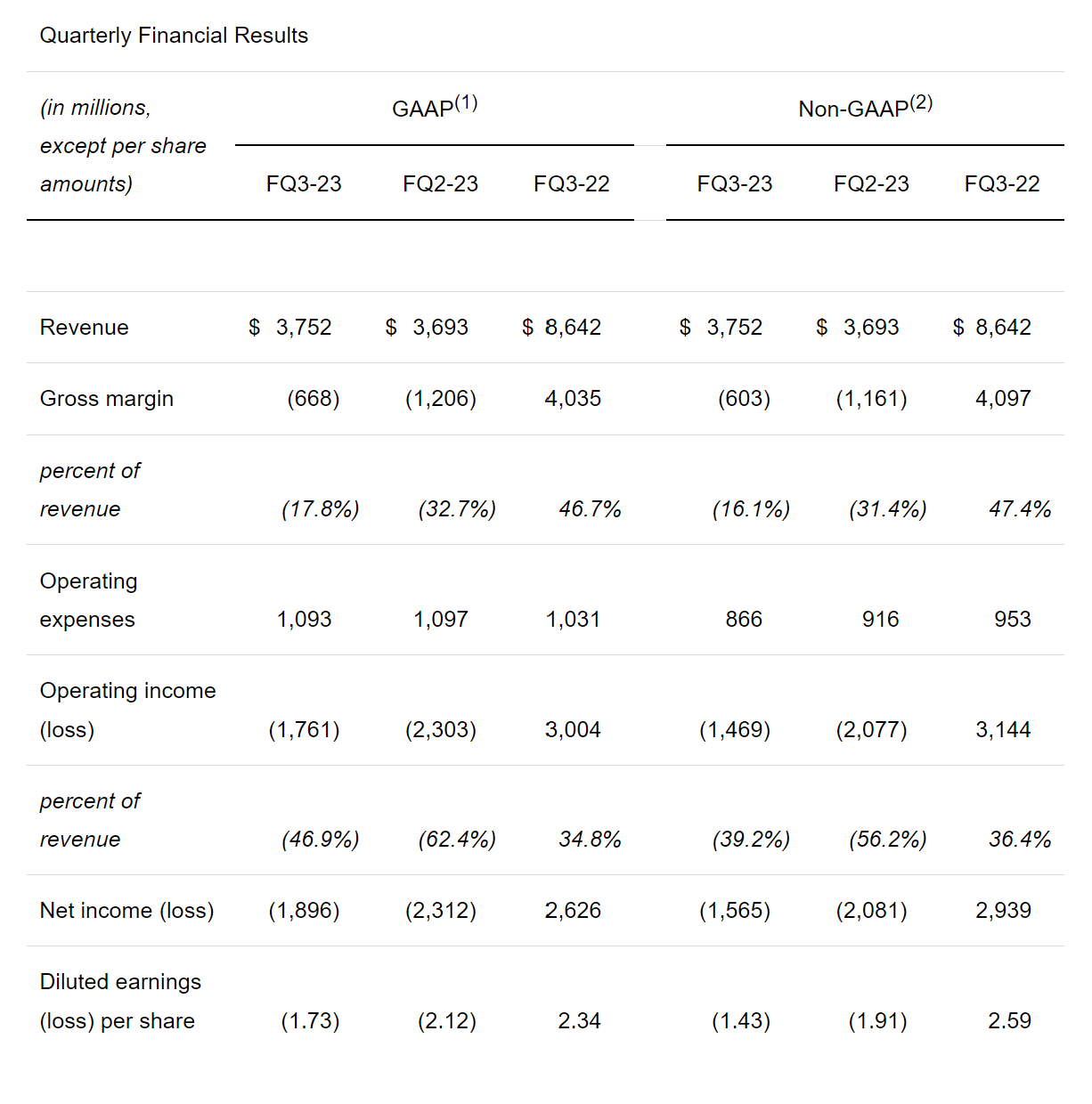

When the company reported its fiscal Q3, there were no surprises in the results really, although the company lost less money than expected. Revenues were expected to be around $3.68 billion while adjusted earnings per share were expected to be a loss of $1.57 per share. The company performed better than expected, with revenues that were $3.75 billion with adjusted earnings per share of a loss $1.43. So, that is poor performance, right? Yes, it is pretty bad. Although, it was expected and known that the quarter would be horrific.

Micron Q3 release

Micron Technology President and CEO Sanjay Mehrotra stated:

We believe that the memory industry has passed its trough in revenue, and we expect margins to improve as industry supply-demand balance is gradually restored. The recent Cyberspace Administration of China (“CAC”) decision is a significant headwind that is impacting our outlook and slowing our recovery. Longer-term, Micron’s technology leadership, product portfolio, and operational excellence continues to strengthen our competitive positioning across diverse growth markets, including AI and memory-centric computing .”

This hits some important points. First, results were above the midpoint of guidance, which was positive. Memory revenues have likely troughed. But the CAC decision is definitely adding to the downturn, and will prolong a meaningful recovery for the company, and by extension, the stock we believe. Other key results to be aware of are moves they are making with their expenses. CAPEX is huge. This is key. Inventory had been high, memory pricing is down, but stabilizing. Things are improving. To save money, CAPEX investments were just $1.38 billion, down from $2.5 billion a year ago, and down from $2.1 billion in the sequential quarter. That follows labor cuts, and other controls already taken.

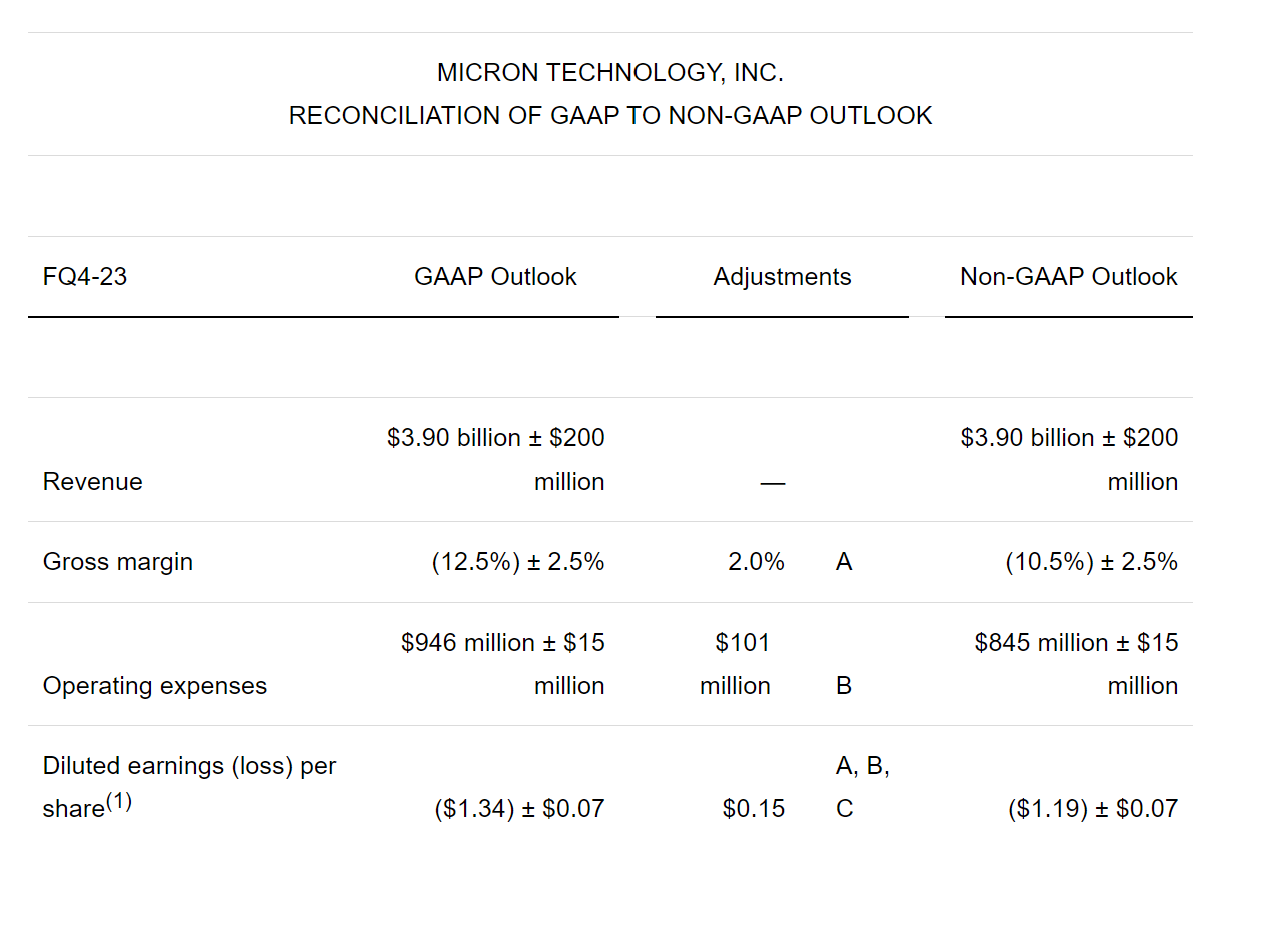

But we have a new set of expectations looking ahead, and that is why the stock is likely to falter, unless the next fiscal year’s guidance is strong. Right now, it is tough to see. For Q4, we think revenue hits $4 billion, with a loss per share of $1.30. These are extremely heavy losses still. The guidance is a touch more conservative but our outlook is based on pricing power and cost cutting that should help exceed the low bar being set.

Micron Q3 release

However, if it can deliver on these expectations and improve its outlook, then we will move higher. It is mostly that simple, but then, of course, you have to factor in the pain that stems from the overall market, which we do believe will be under pressure for a few more weeks in this seasonally weak period.

Fiscal Q4 looks like it is going to be rough for the company once again. Revenue will fall drastically from a Q4 last year where Micron $6.5 billion in revenue and EPS of $1.45. Truly, this downturn is eye-opening. Margins could break even, but are likely to be negative once again. When will it improve? Well it does appear revenues have bottomed, in looking to the last few quarters, we have stabilized and are edging higher. We have likely indeed seen the trough for the company. But how long will the company bleed out money? Tough to tell, but it could take until fiscal Q3 2024 for the company to turn a profit. However, if the recovery is prolonged, Micron may lose money all next fiscal year. The outlook when earnings are reported are very critical.

Despite the losses, Micron is still paying a dividend and repurchasing shares. Although, it has been seeing very negative cash flows, and has issued over $6 billion in debt this fiscal to raise some cash. Micron repurchased approximately $425 million in stock, and paid $378 million in dividends. It ended the quarter with cash, marketable investments, and restricted cash of $11.4 billion.

Fiscal 2024 is now underway, and we anticipate heavy losses for the first two quarters, with improvement in the back half of the year. That is our current view. However, if guidance suggests otherwise, that losses will continue, the stock is heading lower and will be an outright sell. But if management forecasts getting to break even and back to profit later in fiscal 2024, shares could break through the $70 ceiling and remain there. While this will be data dependent, guidance is pivotal.

MU is going through a downturn, which has happened before, and the stock will likely see more downside, especially if earnings or margins expectations are guided poorly for fiscal 2024. The fiscal third quarter suggests a trough in performance, but it is a question of how long this downturn continues. The serious cost-cutting moves and sector strength have helped preserve Micron Technology, Inc. stock as investors simply wait for the macro position to improve.

In closing, we certainly think there are better players and investments in the space, despite the fact that we do love to trade Micron Technology, Inc. stock. That said, we do embrace long-term investors using a buy-write strategy here to generate some income while building a position in Micron Technology, Inc. ahead of a possible late fiscal 2024 turnaround.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Be a Winner and Make Moves With our Team

You do not have to go it alone. Stop wasting time and join our community of 100’s of traders at BAD BEAT Investing.

- Access a professional analytical team, available daily during market hours.

- We have 4 different chat rooms

- Rapid-return trade ideas, medium, and long-term investments each week with crystal clear target entries, profit levels, and stops

- Stocks, options, trades, dividends, and market reads

- Money-back guarantee

- Education, tools, and conversation