Summary:

- Micron Technology, Inc.’s fiscal Q4 revenues of $4.01 billion beat expectations, signaling a sales recovery in fiscal 2024.

- Non-GAAP gross margins improved sequentially, but still were negative at -9.1%.

- Micron’s revenue guidance for Q1 2022 exceeded expectations, but non-GAAP gross margins and losses per share were worse than expected.

James O’Neil

After the bell on Wednesday, we received fiscal fourth quarter results from Micron Technology, Inc. (NASDAQ:MU). The memory and storage leader had seen an early 2023 rally in shares stall out over revenue fears during a typical business down cycle as well as product restrictions from China. As it turned out, the quarter wasn’t as bad as feared, which should set things up nicely for a sales recovery in 2024.

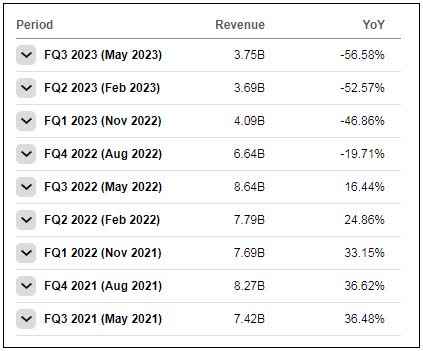

Over the years, we’ve seen a number of revenue cycles when it comes to Micron. The company’s latest one started a little over a year ago, when the top line peaked at more than $8.6 billion. As the graphic below shows, the next four quarters saw double-digit percentage declines for the top line over their prior year counterparts, with hopes going into this week being that fiscal Q4 would be the last quarter in the red.

Micron Revenue History (Seeking Alpha)

Management had guided to fiscal Q4 revenues of $3.9 billion, plus or minus $200 million. Analysts were expecting a little more than that midpoint, going into Wednesday at $3.93 billion. In the end, Micron came in with $4.01 billion, which was towards the upper end of the guidance range. It’s hard to celebrate a 39.6% plunge in your revenues over the prior year period, but I guess you can be a little happy when analysts were expecting a 40.9% plunge.

The other problem during these cycles is that margins and profits can take a massive hit. Micron reported non-GAAP gross margins of negative 9.1% in Q4, compared to a positive 40.3% a year earlier. The good news here is that as revenues rebounded a bit sequentially, non-GAAP margins did rise by 7 percentage points over Q3 levels. The reported margin figure for Q4 came in about 140 basis points above the midpoint of management’s guidance. On the adjusted bottom line, Micron reported a $1.07 loss per share, 11 cents better than the street was expecting.

Shares of Micron slipped a bit in the after-hours session, and that likely had to do with guidance. Management guided to revenues of $4.4 billion, plus or minus $200 million, which was nicely ahead of the street’s expectation for $4.21 billion. However, the non-GAAP gross margin range midpoint was negative 4%, while the street was looking for a slightly positive number. As a result, the non-GAAP loss per share that’s expected to be $1.07 was 15 cents worse than the street was looking for. I’ll note that Micron’s guidance was a bit conservative for Q4, so maybe we’ll see another beat three months from now.

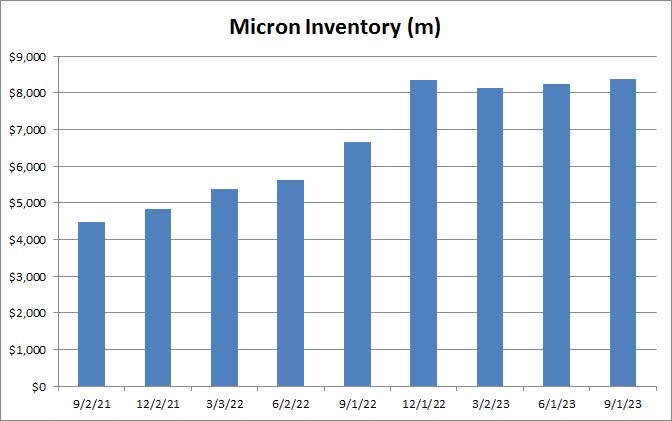

The other problem for Micron in these down cycles is cash flow. With the company racking up large losses, and this being a heavy capital expenditure space, the company swung to negative free cash flow of more than $6.1 billion for the fiscal year. Part of the reason is that inventory levels are a bit inflated at the moment, seen in the chart below, which was a more than $3.5 billion drag on cash generated from operations. A rebound in profits as well as a leveling off or perhaps even a drawdown in inventory should help cash flow trends significantly in the fiscal year that recently started.

Micron Inventory (Company Filings)

Shares of Micron peaked at nearly $100 before the latest revenue downswing started last year, eventually losing nearly half of their value before bottoming. At $65.50 in the after-hours session, the stock is now below its 50-day moving average, and just about $3 above the currently rising 200-day. I think the longer-term trend line could be a good level of support, and would be a great buying target should shares come down to it. The average price target on the street of more than $80 implies more than 20% of upside from current levels.

When Micron shares peaked, the company ended up doing a little more than $27 billion in revenues over the next four fiscal quarters. Factoring in the Q4 beat and Q1 guidance, analysts will likely be looking for about $21 billion in the current fiscal year. Applying the same price to sales valuation gets you a roughly $76 figure for Micron over the next year. If you go another year out, you could potentially see even more upside should revenues start to recover towards those $30 billion a year rates.

With revenues rising again and earnings and cash flow to follow, I’m giving a buy recommendation today for Micron during this current fiscal year. As CEO Sanjay Mehrotra said in the earnings release: “We look forward to record industry TAM revenue in 2025 as AI proliferates from the data center to the edge.” Micron just put in a revenue bottom, so I don’t see why investors would want to be overly bearish on the fiscal year. Industry pricing should also stabilize as supply levels are managed better in the coming quarters.

In the end, Micron announced a mostly decent set of numbers on Wednesday afternoon. Q4 revenues and earnings both beat Street estimates handily, showing that the sales bottom is definitely behind us. While margin guidance for the current period wasn’t great, revenue guidance was a positive surprise, so we should now be in the early stages of an up cycle for the overall business. With the current fiscal year showing much better results, I think Micron shares are worth looking at here, with my rating being even more positive if they trade down to the 200-day moving average.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.