Summary:

- Micron Technology’s 16% stock drop post-Q2 guidance miss is driven by weaker NAND and mobile orders, not AI-related issues.

- Despite short-term challenges, Micron’s AI and data center DRAM markets remain robust, with strong demand from Nvidia and potential from AMD.

- The company’s forward P/E ratio is significantly below the sector median, presenting a unique buying opportunity with a 108% upside potential.

- Micron’s future growth is anchored in AI-driven memory demand, expected to offset legacy business weaknesses and drive substantial long-term value.

BING-JHEN HONG/iStock Editorial via Getty Images

Investment Thesis

Micron Technology (NASDAQ:MU) fell 16% following earnings, with their Q2 2025 revenue guidance of $7.7 billion to $8.1 billion missing estimates and driving the selloff. This was well below analyst expectations of $8.97 billion. Similarly, earnings-per-share guidance of $1.43 fell short of the $1.93 consensus estimate. This means that the company will enter the new year with a negative quarter-over-quarter growth. For a firm riding the AI wave, this appears to be a setback on the AI narrative.

Except, ironically, it wasn’t.

Most of the miss on guidance was driven by lower than expected NAND sales and mobile order weakness. It has almost nothing to do with the AI boom.

In essence, this is not a sign that the overall AI trend that has been powering the long run growth in the company is slowing. Micron can still take advantage of high-margin AI and data center markets for future growth.

With this, Micron has strong demand in their key AI division going forward due to their sold out FY 2025 DRAM supply with Nvidia (NVDA). With Nvidia’s now launched Blackwell platform, Micron can also capture additional market share, given Nvidia is still struggling to secure enough of Samsung’s HBM memory chip. Talks here are rumored to be ongoing. This means (for now) Micron continues to be the main game in town.

As AI adoption accelerates, Micron’s supply chain partnerships and HBM technology should insulate them from secular trends in other parts of their business. With this, (and despite the earnings miss), I think the current market sell-off means shares are now a strong buy.

Why I’m Doing Follow Up Coverage

To be clear, I was optimistic going into Micron’s Q1 earnings because of their key advantages in AI DRAM that should continue to kick off strong sales even as the overall AI sector changes, particularly as the world of AI has shifted from pre-training compute to post-training inference.

There is still a lot of potential growth for the company as the evolution in AI models now demands increased memory capacity.

Initially, I did not plan to do this follow-up coverage right after the earnings release. However, the market’s reaction via a sharp 16% drop made me believe this move was uncalled for. The sell-off was triggered primarily by disappointing Q2 2025 guidance. In my opinion, as we dive into why this guidance was poor, this does not align with Micron’s long term growth fundamentals.

In essence, the poor guidance was the result of their legacy business underperforming. As an investor, we are betting on the future. The future for Micron is in AI. This is still strong.

With this, the purpose of this follow-up coverage is to highlight the disconnect between the market extreme pessimism after earnings, and the company’s core AI strength (which really has shown no signs of change).

Q1 Review & Why I’m Still Bullish

Overall, Micron put up a strong $8.71 billion in revenue in Q1 2025, up from $7.75 billion in the previous quarter, $4.73 billion in the same period last year and slightly beating expectations of $8.70 billion. As I mentioned before, it was the company’s Q2 revenue guidance of $7.9 billion that was short of Wall Street’s $8.97 billion consensus expectation. Analysts have pointed to the ongoing slump in NAND and mobile memory markets, along with weak PC upgrade demand.

Their Q2 EPS guidance was set to $1.43 against at consensus of $1.93, or a $0.50 difference. For Q1, EPS came in at $1.79. This beat estimates of $1.77/share.

Despite this, as noted by Micron’s EVP Sumit Sadana in their Q1 2025 earnings call, management remain optimistic in the face of their current headwinds:

HBM growth continues on a good trajectory. Data center overall revenue trajectory continues to be robust. While we do have some near-term moderation in data center SSD after a lot of growth in the past quarters, the overall data center revenue trajectory remains very robust and we expect that to underpin our performance through fiscal and calendar 2025 and so those are the positives.

And of course, we spoke about the near-term issues related to market environment, seasonality, NAND related challenges. So those are some of the headwinds. The mix and data center growth and overall DRAM robust results is what is helping us ensure that the margin for rest Q2 is still fairly similar to what we have in F Q1 in terms of 100 basis point only delta despite some of these headwinds we mentioned in some of the other areas.

Beyond the headwinds in what I am calling their ‘legacy business’, Micron feels confident that advanced AI agents will scale up DRAM usage industry-wide and help Micron find new use cases for their DRAM in both vertical market applications in consumer and enterprise sectors. Micron expects HBM’s total addressable market (TAM) to grow over six fold from $16 billion this year to more than $100 billion by 2030. That’s incredible. Micron is in a position to grab a huge chunk of this accelerating market.

Valuation

After the 16% selloff in shares, Micron continues to trade at a valuation that’s still significantly below the sector median forward price-to-earnings ratio. The company’s forward P/E is now at 12.00, well below the sector median of 24.96. This represents a steep discount of 51.93%.

While the company anticipates softer performance over the next few quarters in their consumer division due to near-term challenges, they expect a return to growth for consumer in the second half of fiscal 2025. In a press release, CEO Sanjay Mehrotra said:

Micron delivered a record quarter, and our data center revenue surpassed 50% of our total revenue for the first time…while consumer-oriented markets are weaker in the near term, we anticipate a return to growth in the second half of our fiscal year. We continue to gain share in the highest margin and strategically important parts of the market and are exceptionally well positioned to leverage AI-driven growth to create substantial value for all stakeholders.

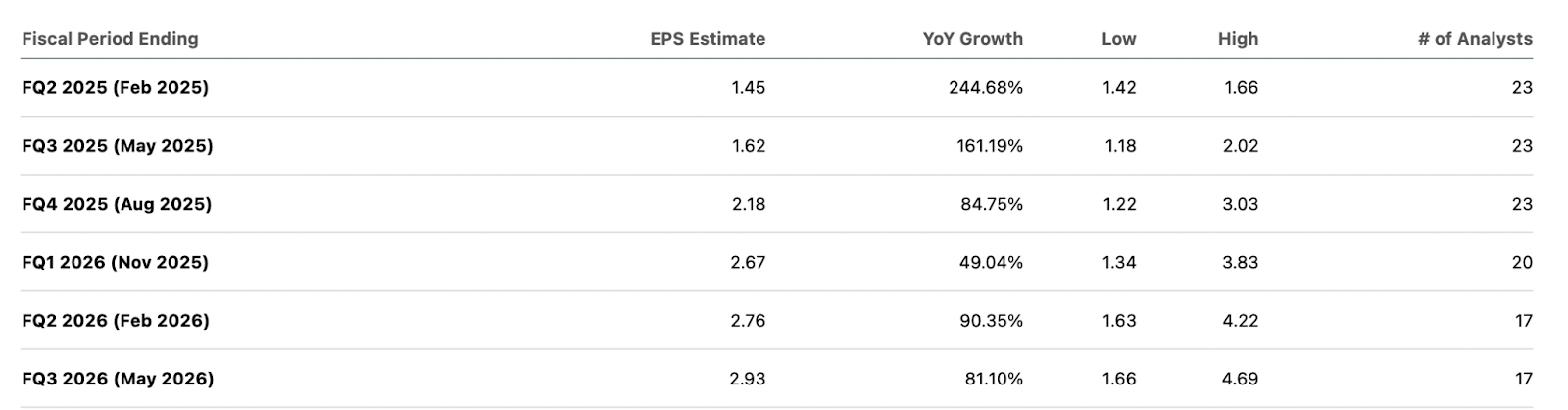

If we actually dive into overall EPS growth over the next few quarters, we can see that growth overall is still set to be incredibly strong.

Forward EPS Estimates (Seeking Alpha)

Really, I think this is a unique opportunity. It’s rare we get to see a company with such strong forward EPS growth trade for just a 12x forward P/E.

The company is trading for such a conservative valuation (I believe) due to market expectations that DRAM growth in data centers will slow (or decline). While AI models are certainly changing (and with it GPU demand) core memory usage should really only go up from here.

With this, if we saw shares converge on the sector median forward non-GAAP P/E ratio, this would represent a 108% upside.

Risks

I think the biggest risk facing Micron is that their legacy business has began to drag as artificial intelligence orders continue to be strong. EVP Sumit Sadana also acknowledged this on the earnings call, focusing on PCs:

The average age of the PC has become pretty long in the tooth, and it is ripe for an upgrade. And as people look to keep their PCs for a number of years, they will look to ultimately future proof the hardware specs, which is why we believe that even with very modest unit volume growth, the mix improvement that will come from higher memory content in these PCs will be a positive driver in 2025.

But the delay in that upgrade cycle means that our calendar ’24 PC shipment forecast at the unit level for PCs at our end customers has been reduced and is now very flattish year-over-year in calendar ’24, so that has been one driver. The other is that definitely the inventories that we had highlighted in the last earnings call, that we expected by spring would become healthier at our customers, that inventory and inventory reduction as well as the seasonality of CQ1, those are continuing impacts. Some impact coming from the moderation.

To offset this delay in PC shipments (that Micron should eventually benefit from via memory sales), the company should be able to benefit from accelerating trends in GPU design that tell me their AI DRAM business could get even stronger.

In May, Nvidia announced their accelerated product roadmap, with the aim of releasing AI-focused GPUs annually to reflect changing hardware requirements.

This is an immense tailwind for Micron, particularly for DRAM sales inside GPUs like Blackwell, which demand this higher DRAM capacity that I mentioned in the earnings preview. With increased memory needs, Micron really has a unique scenario where the TAM of the overall GPU market may see its growth slow, but DRAM sales should accelerate due to the much higher demand for memory. It’s a great spot to be in.

On the legacy business side, we’re also seeing key advances in compressing large language models (LLMs) for local deployment, which is increasing the mobile and PC use cases for Micron memory.

This could be a game changer as local model deployment is the key to a PC and smartphone upgrade cycle. Using algorithms such as CALDERA, it’s now far more feasible for advanced LLMs to now run on consumer devices, including smartphones, enabling real-time, on-device inference. This will help accelerate PC sales as well. Firms like Microsoft have been anticipating a bump in PC sales for the past year. So much so, Microsoft earlier this year invented a new ‘AI’ key on PC keyboards as a sort of ‘hot key’ to prompt LLMs.

By expanding their AI market from just cloud-based GPUs to edge computing (through these compressed LLMs), this tells me that memory demand should pick up on PCs and mobile devices. The whole industry has been anticipating a surge in mobile and PC orders driven by AI use cases. With high-powered LLMs getting compressed, we might finally have the catalyst we need.

Bottom Line

While Micron’s shares have fallen 16% after issuing their Q2 guidance, I continue to believe the company has an impressive future. We have to pay close attention to the details here because most of this miss reflects ongoing challenges in the NAND and mobile markets, alongside weaker demand for PCs. AI-related memory demand continues to offer a silver lining in this case. In my opinion, that’s the part of the company we should be betting on.

In essence, this sell off really doesn’t dissuade me from the core thesis on Micron. The company’s strong AI and data center DRAM markets remain intact, and this should quickly balance-out the unfavorable consumer-oriented markets that are weighing on short-term quarter-over-quarter growth.

Because their AI memory supply remains robust, particularly with their partnership with Nvidia, I still feel really confident they have consistent demand for HBM products (and even more upside if other GPU makers like Advanced Micro Devices (AMD) pick them as a vendor). AMD may become a potential customer at this point for their HBM offering, especially given the note from management in the earnings presentation that they have “…commenced high-volume shipments to our second large HBM customer.” I am incredibly optimistic about this.

With this, I continue to believe this selloff is noise. As long as AI DRAM is strong enough to offset any legacy business weakness, I continue to believe shares are a strong buy.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AMD either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Noah Cox (main account author) is the managing partner of Noah’s Arc Capital Management. His views in this article are not necessarily reflective of the firms. Nothing contained in this note is intended as investment advice. It is solely for informational purposes. Invest at your own risk.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.