Summary:

- Micron is the fourth largest supplier of DRAM, which is an essential component of PCs and data centers, and it is even used inside Nvidia’s leading GPUs.

- The company reported a top and bottom line miss for Q2, FY23 which has been driven by the cyclical downturn in the industry.

- A positive is its cloud revenue looks to have bottomed out and its mobile business reported solid revenue growth of 44% sequentially to $945 million in Q2, FY23.

- Micron seems to be overlooked by the market as an “AI stock” despite AI servers using up to eight times more DRAM when compared to traditional servers.

- Micron is poised to benefit from the CHIPS act with a $40 billion plant in the U.S. expected to be built by 2029.

naphtalina/iStock via Getty Images

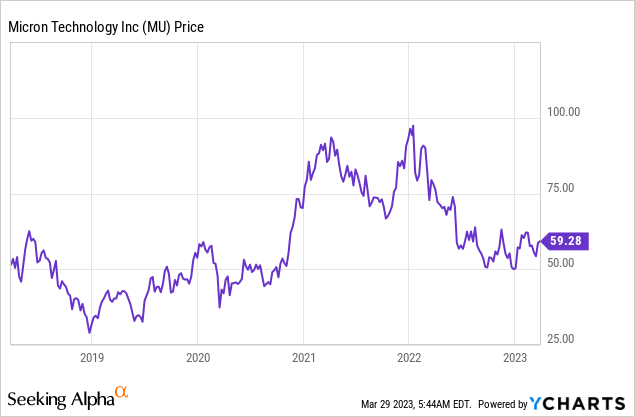

Micron (NASDAQ:MU) is the fourth-largest semiconductor company in the world and the third largest supplier of DRAM or Dynamic Random Access Memory. This is an essential component for all computers, from your average PC to data center computing infrastructure. Therefore, as the world continues to become more digitized, Micron is poised to benefit. In fact a study by McKinsey forecasts the semiconductor industry to reach a value of $1 trillion by 2030. The industry is going through a major downturn right now, but history suggests this is cyclical by nature. Micron also is expected to benefit from the growth trends in the AI industry. According to Micron’s management, an average AI server uses up to eight times as much DRAM content and three times as much NAND (Micron’s other major product) than a traditional server. Therefore Micron is in a strong position to benefit, which the market doesn’t seem to have digested, as its stock price is down over 39% from its high in January 2022. In this post, I’m going to break down the recent financial results for Micron, before diving into the industry trends and my valuation and forecasts for the stock, let’s dive in.

Mixed Financials

Micron reported mixed financial results for the second quarter of FY2023. Its revenue was $3.69 billion which missed analyst forecasts by $13.63 million and declined by an eye-watering 52.6% year over year. This may seem terrible at first glance but we should keep in mind the memory and semiconductor industry is currently going through a demand downturn, after a previous boom, which even resulted in a shortage in the latter half of 2021. The good news is the industry tends to be cyclical by nature and thus I don’t believe this is a permanent issue.

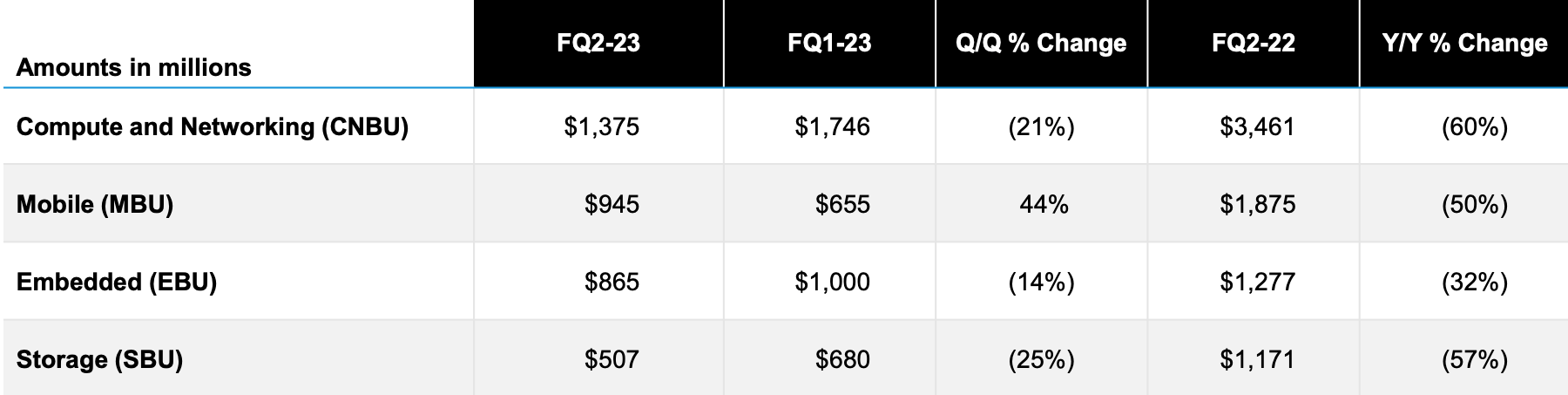

Breaking revenue down by segment, Compute and Networking [CNBU] generated $1.375 billion in revenue which declined by 60% year over year. The PC industry is going through the aforementioned cyclical downturn, but a positive is Micron’s management has forecast increased bit demand in the second half of 2023, according to its earnings call. It should also be noted that many people are chasing Nvidia stock right now due to its strength in both high-performance graphic cards (GPUs) and AI (which I will discuss more about later). However, I discovered that Micron’s 16GB GDDR6X is a key component of Nvidia’s GeForce RTX 4080 GPU.

Micron powers Nvidia (Author Research Nvidia datasheet)

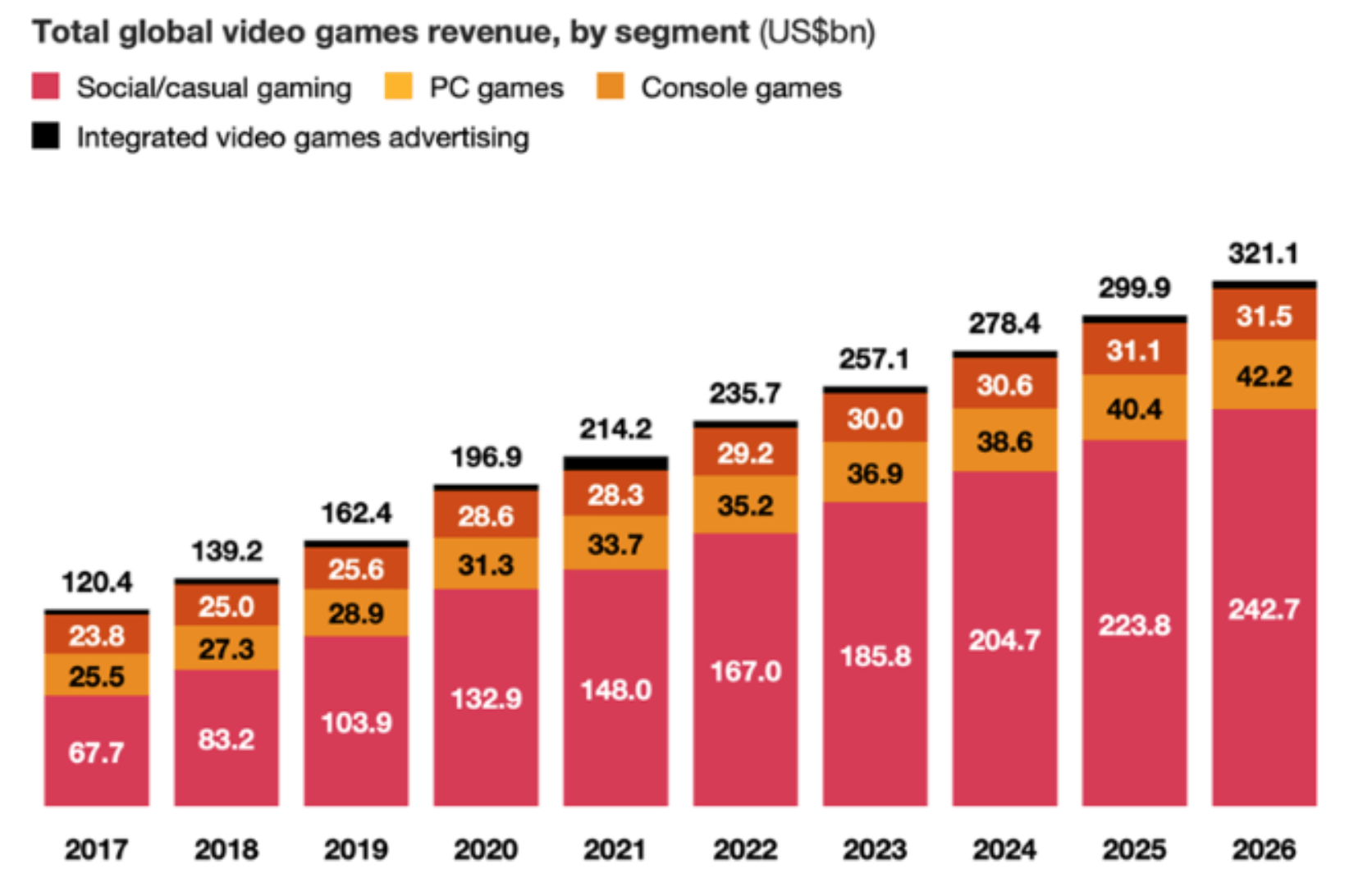

The global gaming industry was valued at $235.7 billion in 2022 and is expected to reach a value of $321.1 billion by 2027, according to a PwC report. Therefore as the gaming industry rebounds (and continues to grow), I expect Micron to benefit.

Gaming industry (PwC)

AI Opportunity

Micron provides DDR5 RAM [D5] which is specifically designed for data centers and has demonstrated up to an 85% increase in system performance, over the prior DDR4. This product also is specifically designed to maximize the performance of High-Performance Computing, big data, and Artificial Intelligence workloads. Micron’s CFO believes its data center revenue “bottomed” in this quarter (Q2,FY23) and sequential improvements should be seen throughout the rest of the year. By the end of 2023, the company expects customer inventories back at “healthy levels”. This expected rebound is partially driven by the huge excitement and forecasted growth in the AI industry.

An AI server can have up to 8x as much DRAM content and 3x as much NAND. This is because AI workloads have a tendency to be more memory intensive. Therefore Micron is poised to benefit, as I alluded to in the introduction.

According to Micron’s data sheet, the product also offers 36% greater efficiency, which is huge. In a recent (2023) interview with Bill Gates and Microsoft’s CTO on AI, Gates stated improving energy efficiency of AI processes was a “huge challenge” and north star for many companies. Therefore Micron is on trend, which is a positive.

Micron also is working on its third generation of High Bandwidth Memory (HBM3) to benefit from these AI growth trends. Its competitors Samsung and SK Hynix are little further ahead in this regard as their products. SK Hynix provided the industry’s first HBM3 to Nvidia in 2022 and Samsung’s Icebolt is already in mass production.

A positive is Micron has started mass production and shipments of its fastest PCIe Gen4x4 NVMe SSD which has high performance with AI and high performance computing [HPC] workloads.

Let’s also not forget about the general Cloud industry which was valued at $480 billion in 2022 and is expected to grow at a rapid 19.9% compounded annual growth rate, reaching a value of $1.7 trillion by 2029.

Mobile Recovery

Micron’s Mobile Business has started to recover well and reported $945 million in revenue for Q2,FY23, which was up 44% sequentially, despite being down 50% year over year. Management expects customer inventory to improve throughout the year, with growth in DRAM and NAND shipments in the second half of the fiscal year 2023.

And finally, its Embedded Business revenue was $865 million which was down 14% sequentially and thus doesn’t seem to have fully bottomed yet. This was mainly driven by the aforementioned weakness in consumer markets. However, this was partially offset by ~5% YoY revenue growth in the automotive segment. I have solid hopes for the automotive industry as companies such as Nvidia and Qualcomm have reported that as their fastest-growing segment (on a percentage basis).

Micron Revenue Business (Micron)

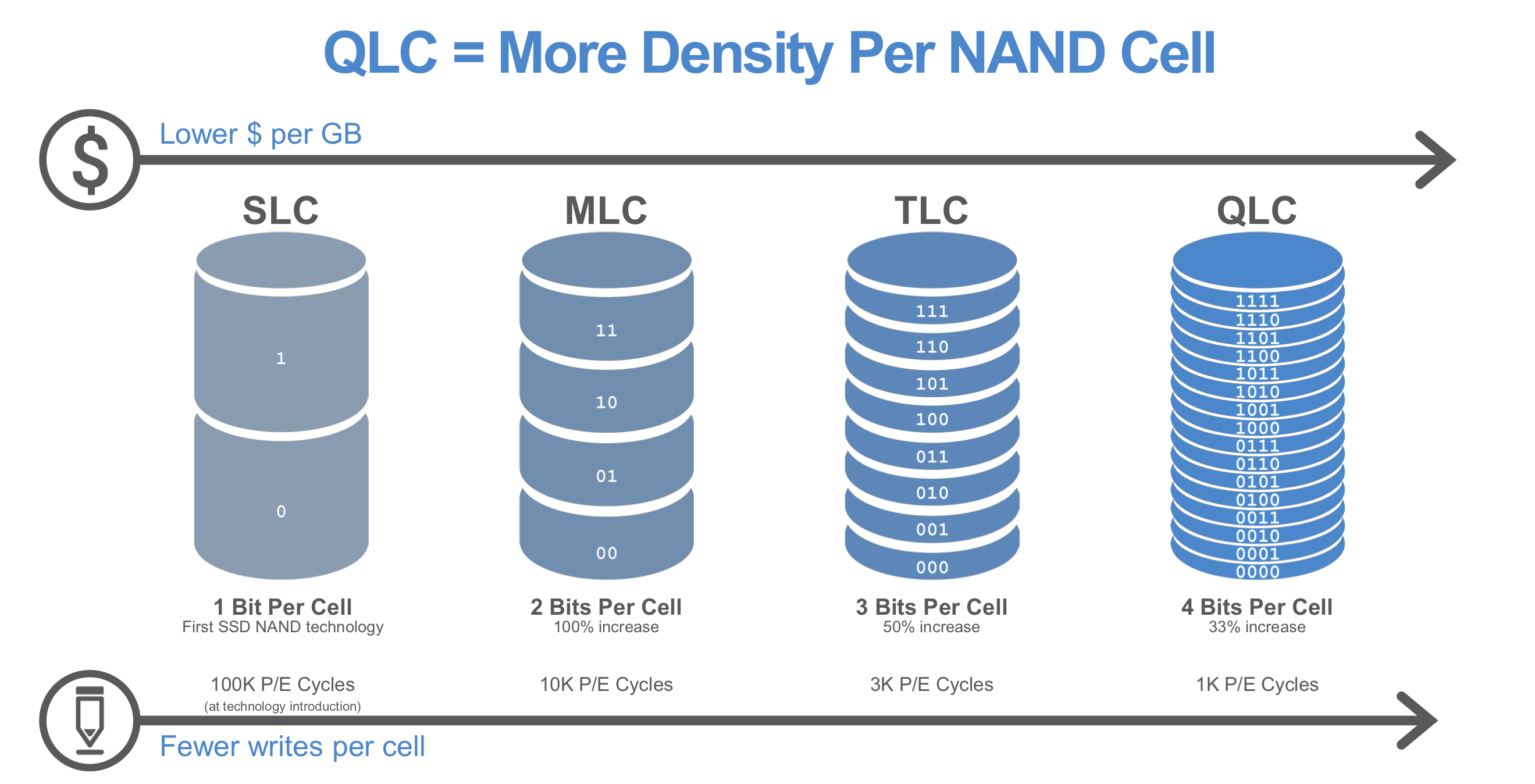

Micron reported $507 million in Storage revenue for Q2,FY23, which was down 25% sequentially, due to weakness in the NAND market which results in a mid 20% decline in the average selling price. A positive is this offset slightly shipments which increased by mid to high single-digit percentage range. Therefore this shows demand is starting to recover, but there’s just over supply in the industry, which will take some time to work through. Another positive for Micron is the company was the first in the industry to ship QLC NAND which now makes up ~20% of production volume as of Q2,FY23. This is important as QLC or (Quad Level Cell) NAND offers greater storage density, lower cost per bit, and faster read speeds than prior architectures, such as TLC (Triple-Level Cell). In other words, Micron’s products are “better, faster, cheaper” which is the prime selling point for most electronics.

QLC NAND Benefits (ANANDTech)

Expenses and Margins

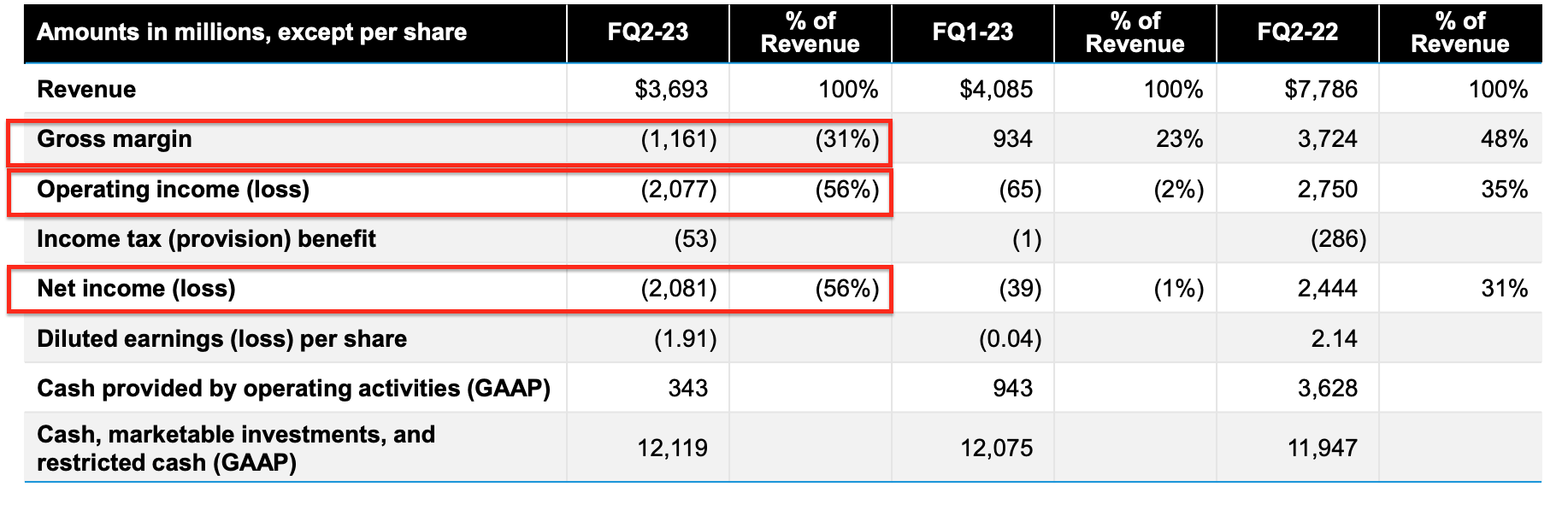

Micron reported gross margin of negative 31.4% for Q2,FY23, which was down substantially from the positive 48% in the prior year. This was mainly driven by a $1.4 billion inventory write-down. The only silver lining is this was a “non cash” write down, driven by projected selling prices falling below the cost of inventory. The company also reported a substantial operating loss of $2.1 billion which was also impacted by the aforementioned inventory write-down. A positive is Micron’s overall operating expenses actually reduced by ~$80 million sequentially to $916 million in Q2,FY23, as management has made it a strategic priority to cut costs where possible.

Micron Profitability (Q2,FY23 Non-GAAP)

Micron reported cash flow operating of $343 million for Q2,FY23, which was down from the $943 million in the prior quarter. Micron has announced a 40% reduction in its capital expenditures for the full fiscal year of 2023 to ~$7 billion and the company is scaling back the production of both its DRAM and NAND in order to help improve supply dynamics. The good news is other players are the industry also are reducing production, which could result in a faster market recovery by 2024.

Moving onto the balance sheet, Micron reported $12.1 billion in cash and investments. Management did increase its liquidity with $1.9 billion extra in long-term debt, which brought the total debt to ~$12.3 billion. Overall I think this is prudent given the backdrop and as its long term it should be extremely impacted by the higher interest rate environment, which I personally believe is “short term” (until inflation is squelched). Micron’s weighted debt majority is 2029 and thus it’s in a solid position.

Valuation and Forecasts

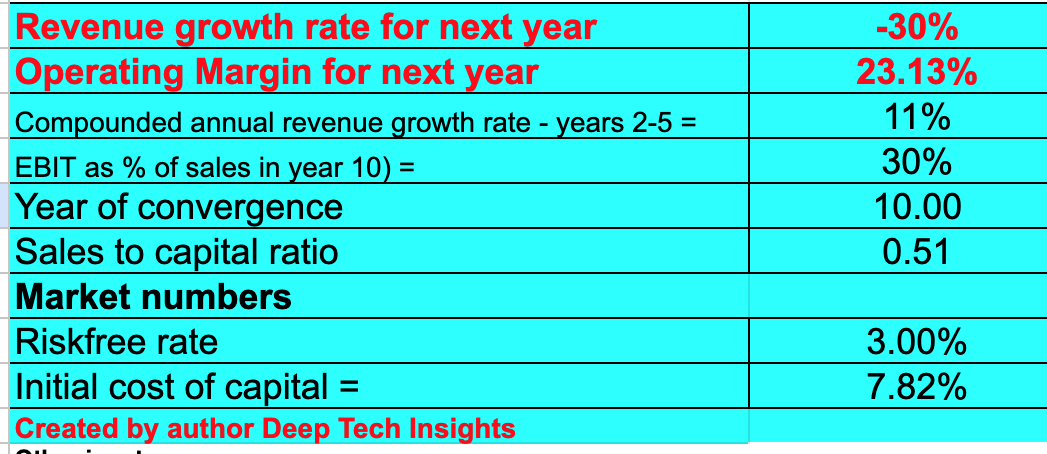

In order to value Micron I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast negative 30% revenue growth for “next year” or the next four quarters in my model. I expect this to be driven by the lower demand dynamic (and high inventory), which should start to improve towards the latter half of the calendar year 2023. This is in line with management’s forecast of 5%, growth in DRAM, and low teens growth in NAND volume for 2023. As mentioned prior, Cloud revenue looks to have bottomed out in Q2,FY23 and thus is poised to turnaround by the end of the calendar year.

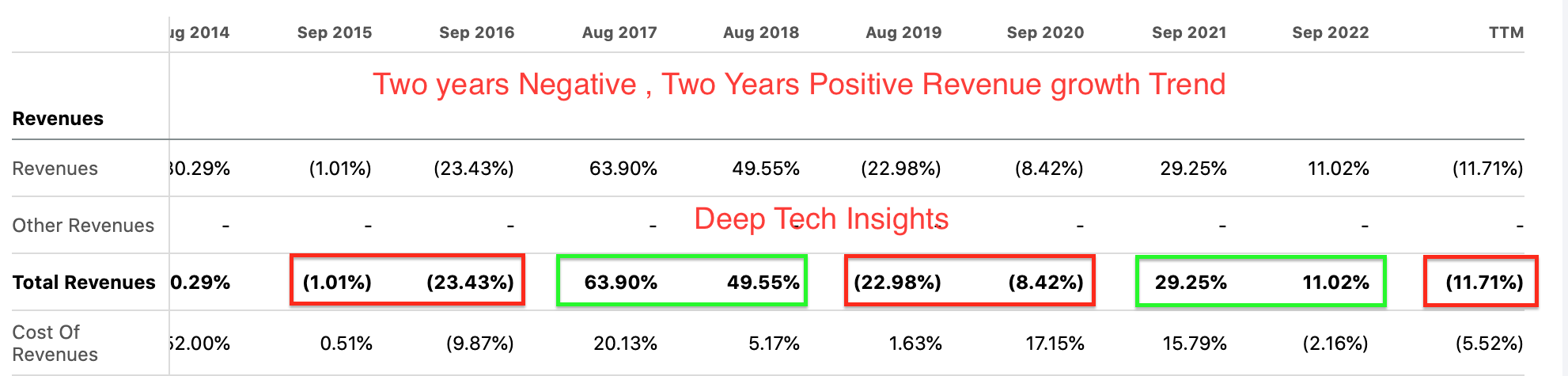

Looking at historical data, I have found that Micron usually reports two years of negative revenue growth, followed by two years of positive growth etc. This is normal for a company in a cyclical industry. From the data, it now looks as though we are part way through the “cyclical process” and thus another 18 months of negative revenue growth wouldn’t be a surprise until a strong recovery.

Micron Cyclical Revenue (Trend Annotations by Author Deep Tech Insights)

In years 2 to 5, I have forecast this growth to rebound by at least 11% per year which is a similar growth rate achieved in the fiscal year of 2022, (quarter ending September 2022). Given the industry trends (AI, Cloud, Automotive computing) it would not surprise me if Micron achieved faster growth rates of 50% during its next rebound cycle. However, when valuing companies I prefer to be conservative.

Micron stock valuation 1 (Created by author Deep Tech Insights)

To increase the accuracy of my valuation, I have capitalized R&D expenses which has boosted net income. In the short term I expect margins to remain challenged as oversupply will keep average selling prices depressed. Management is expecting a further inventory write down of ~$500 million in Q3,FY23. The good news is the company is aggressively cutting costs and has increased its headcount reduction target from 10% to 15%. Management has guided for operating expenses below $850 million for Q4,FY23, which would be a further improvement over the $916 million reported in Q2,FY23.

Over the next 10 years I have forecast a 30% operating margin. This may seem bold but it is really just a return to its prior margin of ~32% reported in the fiscal year 2022.

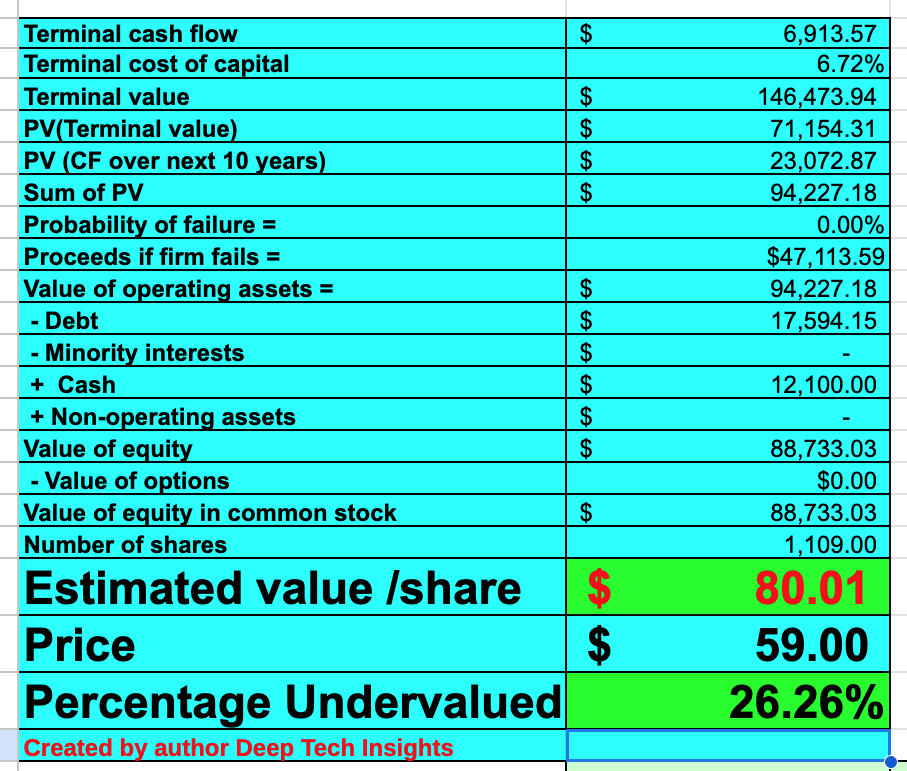

Micron stock valuation 2 (Created by author Deep Tech Insights)

Given these factors I get a fair value of ~$80 per share, the stock is trading at ~$59 per share at the time of writing and thus it is over 26% undervalued, with my conservative forecasts.

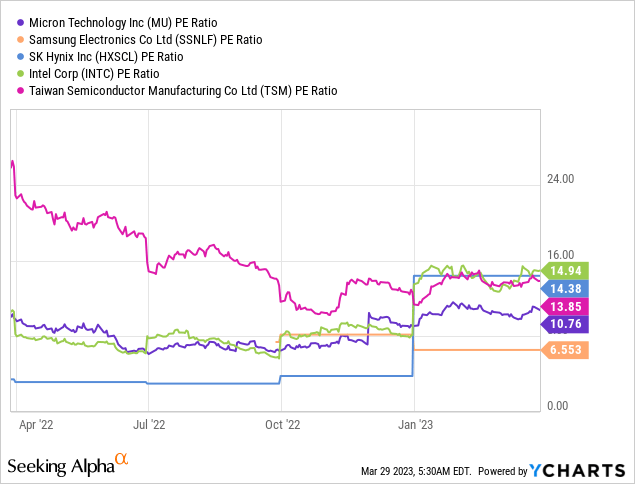

The stock also trades at a Price to earnings [P/E] ratio = 10.64, which is ~23% cheaper than its 5 year average. This metric is also at the low end relative to its Semiconductor industry peers, as you can see on the chart below.

Risks

Recession/Cyclical demand

Many analysts have forecast a recession for 2023, which is expected to start later than initially expected. Therefore the cyclical decline in the semiconductor industry could drag on longer than initially hoped for.

Final Thoughts

Micron is a tremendous technology company that’s poised to benefit from the need for DRAM and NAND, driven by computing, the cloud and AI. The company is facing headwinds from the cyclical downturn in the industry, but long term its poised to bounce back stronger than ever. Management has prudently cut costs and this is not the first downturn the industry has faced. Given my valuation model and forecasts indicate the stock is undervalued intrinsically I will deem it to be a great long-term investment.

Disclosure: I/we have a beneficial long position in the shares of MU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.