Summary:

- This article addresses these key questions: Who are Palantir Technologies Inc. customers and why do they choose Palantir? What value does Palantir bring? Where is the company most focused on driving growth?

- Palantir’s strategy shift to AIP and Bootcamps is contributing to strong customer acquisition momentum in 2024.

- Despite strong momentum, even ambitious growth assumptions do not warrant Palantir’s current valuation. By every meaningful valuation metric, Palantir stock is overvalued.

JHVEPhoto/iStock Editorial via Getty Images

Prelude

I initiated coverage of Palantir Technologies Inc. (NYSE:PLTR) in January of 2024 with a Buy rating. Shortly after that article was published, Palantir released Q4 earnings which sent the stock rocketing upwards. Palantir is up over 40% since my initial coverage.

After covering Palantir initially, I opted for a strategy of slow and steady accumulation. I have been cost-averaging weekly, and it is growing into a more sizable chunk of my portfolio. It’s a core long-term growth holding for me. I don’t plan on selling any stock here.

My first article was a deep dive into the business fundamentals and financials of Palantir. The growth trends presented are extremely compelling and the business model is straightforward. Management is focused on execution, increasing the pace of customer acquisition, and growing Palantir’s TAM (total addressable market).

In this article, I’d like to focus on two key discussions: 1) the customer value proposition, and 2) valuation.

Customer Value Proposition

Who are Palantir’s customers and why do they choose Palantir? What value does Palantir bring? Where is the company most focused on driving growth?

These are questions I hope to equip you with answers to.

Customers

Palantir’s primary right to win exists in large enterprises with complex organizational and data structures. As the enterprise landscape has leaned deeper into the Web 2.0 modality of API interconnectivity and cloud computing, backend architectures have become increasingly complex and messy. Data lakes, data warehouses, on-prem servers, hybrid cloud… what does it all even mean?

For enterprises, Web 2.0 generally refers to digitizing at scale. Bringing their back-end (supply chain logistics, inventory management, accounting) and front-end operations (website, advertising) into a digital-native operating model. This is not new; it predates the cloud era for businesses that managed on-prem data centers. For many others, though, the era of cloud computing was the first opportunity to digitize their operations.

The cloud has powered enterprise digitization for over a decade, but the issue we are running into now is the complexity of managing these digital environments. Adding AI capabilities into the equation exacerbates this complexity.

Cyber World

Palantir simplifies this. With Apollo, enterprises can stitch together different data environments into the Palantir Cloud, this includes multiple cloud environments, on-prem data centers, and the edge. Apollo connects into Foundry or Gotham.

Gotham is mostly for government customers and businesses with vast swaths of highly sensitive data like financial institutions. Foundry is the common offering for enterprise customers. It functions as a central operating system for data.

What is an operating system for data?

Let’s abstract up another layer and ask: what is an operating system? Windows OS of course is the most pervasive, but Mac OS is quite common as well (Mac OS is actually just a repackaged Linux OS). Operating systems are the interface between the hardware and software that allows for the efficient use of hardware.

Think of a ceiling fan. If you want to change the fan setting from low to high: You could either 1) manipulate the electrical wires and turn off the ‘low’ setting wire and turn on the ‘high’ setting wire, or 2) you could click a button on the fan remote to switch the setting automatically. In example 1, this would be equivalent to using machine language to instruct your computer hardware how to operate. Example 2 is the equivalent of an operating system. An interface that sits between user and hardware.

Taking it one step further, the icons on the remote would be known as the “GUI” or “Graphical User Interface” – another key early development in the commercialization of computers. Even an extremely powerful OS like Windows would not be commercially viable if it didn’t have a sleek and simple GUI, allowing anyone to easily learn how to do what they need to do.

Back to Palantir.

Modern enterprises have various data sources and different end-users of data. Foundry syncs data sources with data storage to provide a single stream for all end-users to interact with their data. Business users can request analysis, and the analytics team can conduct that and present it back to business partners directly in Foundry. It’s meant to be usable and efficient for various end-users while simplifying the back-end architecture for IT managers.

Palantir’s newest product, AIP or Artificial Intelligence Platform, turbo-charges Foundry and Gotham by integrating AI through every step of the data funnel. AIP Bootcamps are short (typically 5 days) onboarding sessions to get Foundry + AIP setup for an enterprise customer.

Bootcamps are sending total customer count rocketing upwards, so Palantir is enjoying incredible momentum in customer acquisition and relationship deepening. Their existing software was the perfect use case for LLMs and AI-enhancement. Palantir was in the right place and the right time, and the results are starting to show this.

From the recent 10-K (amended for readability):

As of December 31, 2023, Palantir had 497 customers representing 35% YoY growth. Palantir software is currently used across approximately 80 industries around the world.

Of the $2.2 billion in revenue that we generated in 2023, 55% came from customers in the government segment, and 45% came from customers in the commercial segment.

Our business continues to have a global presence. In 2023, we earned 62% of our revenue from customers in the United States, and 38% from those abroad.

The average revenue for our top twenty customers during 2023 was $54.6m, and is up from 2022, when the average revenue from our top twenty customers was $49.4 million.

The 2023 strategy shift to pushing AIP and Bootcamps has accelerated customer acquisition markedly.

Let’s walk through a few real-world use cases for Palantir’s software, as presented in the recent AIPCon event.

Lennar Corporation (LEN)

Lennar is a home builder in the U.S. They purchase, prep, and then build on land. After building, they sell homes and home warranties. Throughout this workflow, they have complex bidding processes for the initial purchase and finished home sale and a complex supply chain to get raw materials to sites. They used Foundry to simplify the bidding process on homes, pulling in thousands of datapoints from emails to figure out who made the best offer, where they can negotiate, and ultimately make the best decision possible.

The presenter from Lennar noted that, while he worked at Tyson Foods, that Tyson used Foundry to save $700m.

Lowe’s Companies, Inc. (LOW)

Lowe’s is a major home improvement retailer in America. They have a complex supply chain as well, spanning all types of materials from steel to lumber, home appliances, outdoor and garden, and basically anything you may need for any home improvement project. They also offer a home services segment that helps customers manage home improvement projects start-to-finish. They had an outdated ERP, enterprise resource platform, that made it difficult to track projects and audit their home services call center. They have numerous projects flowing through this call center at different stages between planning, implementation, and completion.

In less than four months, they went from proof-of-concept to production with Palantir that greatly simplified their ERP and gave a simple, straightforward, and auditable solution for Lowes. It resulted in improved customer experience and better traceability of projects from start-to-finish.

Wrap-Up

Now, returning to our initial set of questions: 1) Who are Palantir’s customers and why do they choose Palantir? 2) What value does Palantir bring? 3) Where is the company most focused on driving growth?

We can answer with:

1) large enterprises with complex data environments, they choose Palantir because of quick time to market and seamless integration with existing architecture.

2) Palantir simplifies backend architectures and allows for cross-connection of multi-cloud and hybrid cloud environments. Palantir’s software brings operational efficiencies that lead to cost savings for enterprises.

3) Palantir is leaning heavily into AIP and Bootcamps to acquire and deepen relationships and drive growth moving forward.

With this understanding of the clear value proposition Palantir presents, let’s turn to the bearish side of the article: valuation.

Valuation

By far the most difficult aspect of Palantir’s investment case is the current valuation. In my initial article, I stated that despite relative overvaluation from a P/E perspective, the PEG ratio provided sufficient reason to believe Palantir presented a fair value at the $16-$17 price range. At the $24-$25 price range, the valuation discussion gets much more difficult.

Despite offering an extremely lucrative gross margin and strong growth prospects, Palantir still touts a ludicrous forward P/E of 76 at the time of writing and an abysmal full-year net margin of 7%. Notably, the Q4 report demonstrated strong margin expansion with net margin at 15%.

The headline of the Q4 report was growth in the commercial segment:

U.S. commercial highlights

- U.S. commercial revenue grew 70% YoY and 12% QoQ to $131m

- U.S. commercial customer count grew 55% YoY and 22% QoQ to 221 customers

- U.S. commercial total contract value (“TCV”) of $343 million, representing 107% growth YoY on a dollar-weighted duration basis

- U.S. commercial remaining deal value (“RDV”) grew 32% YoY and 28% QoQ

RDV is a really important metric for SaaS companies as it represents predictable future revenue streams. RDV growth was really strong, and the commercial segment is likely to overtake the government segment in Palantir’s FY 2024 report.

Despite this, Palantir’s full-year guidance doesn’t add much hope to the valuation debacle.

For full year 2024, we expect:

- Revenue of between $2.652 – $2.668b (18.9%-19.6% YoY growth)

- U.S. commercial revenue in excess of $640m, representing a growth rate of at least 40%.

- Adjusted income from operations of $834m – $850m.

- Adjusted free cash flow of $800m- $1b.

- GAAP operating income in each quarter of this year.

- GAAP net income in each quarter of this year.

A TTM P/S of 23.6 for a company guiding for 20% growth is an obscenely high valuation.

Let’s assume the company beats revenue guidance by a significant margin and reports full year 2024 revenue of $3b. Further, let’s assume net margin continues expanding and closes 2024 at 20% and net income reaches $600m for FY 2024. These are bold and ambitious assumptions, 34% revenue growth and more than a doubling of net income.

Even under this ambitious estimate, the current market cap of ~$50b represents a forward P/S of 16.67 and forward P/E of 83.

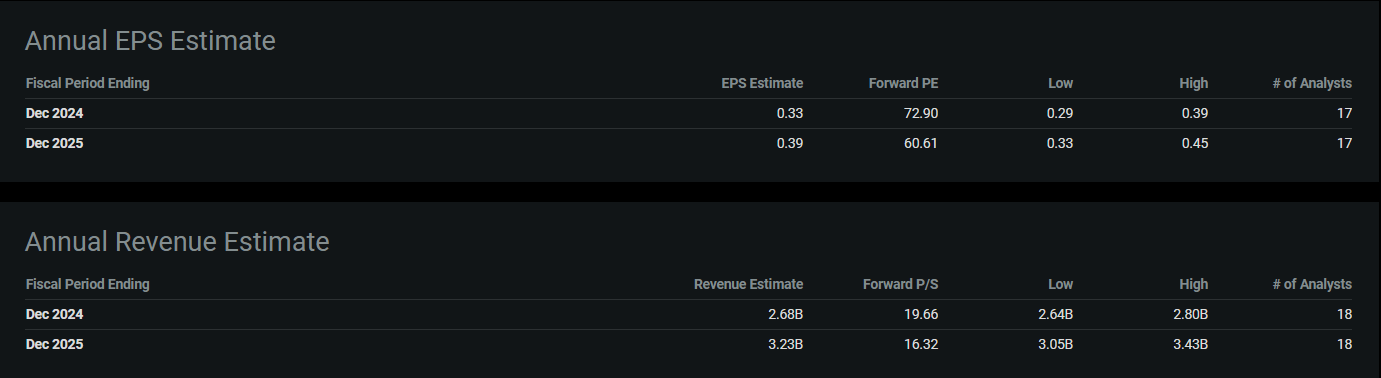

Looking toward 2025, let’s assume figure above the higher end of Wall Street estimates (from Seeking Alpha earnings estimates):

Seeking Alpha

I’ll assume 2025 EPS of $0.50, which represents ~$1.1b net income with the current number of shares outstanding. Let’s assume there’s further net margin expansion to 25%, this would represent ~$4.4b of revenue.

Again these are bold and aggressive growth assumptions, yet they still yield a forward P/S of 11.4 and forward P/E of 45!

Finally, the PEG ratio, which factors growth into valuation metrics, no longer suggests undervaluation. At the time of my initial article, Palantir’s forward PEG was below 1.0, suggesting it was undervalued for the growth opportunity it presented. This is no longer the case, with forward PEG rising now to 1.54. While this is still favorable compared to the sector median, it demonstrates that Palantir is no longer undervalued as it was at $16.

The current Palantir Technologies Inc. stock price is far too steep a price to pay even with bold growth estimates. For that reason, I am downgrading Palantir to a Hold. Management will need years of expectation beating growth and flawless execution to warrant the current valuation.

Closing Thoughts

While I believe the current valuation is too steep, I also believe Palantir is a fantastic growth opportunity with a strong product-market fit. U.S. commercial growth is what will power this company into the next decade and the growth prospects presented here are extremely compelling.

I do not recommend selling Palantir, as this is a great core holding for a long-term portfolio. Concurrently, I believe there will be much more attractive opportunities to buy this company in the future. Stay patient for now, the opportunity to accumulate more Palantir stock will present itself eventually.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of PLTR either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.