Summary:

- PepsiCo’s Q4 results were solid. The ensuing sell-off offers a compelling opportunity to accumulate shares.

- The company’s long-term track record of positive EPS growth and strong management make it an attractive investment.

- PEP stock’s recent dip and fair valuation present an opportunity to buy a “wonderful company at a fair price”.

JHVEPhoto

I spent the weekend performing due diligence on PepsiCo (NASDAQ:PEP) after its Q4 report, and I came away impressed.

The quarter wasn’t perfect, but I think PEP offers a fairly compelling opportunity here to accumulate more shares.

I’ve owned PEP shares for years. I’ve added to this position regularly, and my overall cost basis currently sits at $106.84 (pointing towards gains of approximately 60%).

Currently, PEP is my 21st largest holding with a ~1.1% portfolio weighting. Because of the overall quality of this business, I’d be happy to push that allocation higher, up towards the 1.5-2% area.

Is this company exciting?

No.

However, it’s a proven compounder that has helped make investors rich for decades.

With that in mind, I’d be happy to own more of it and after the stock’s recent dip, PEP shares have risen up my watch list.

PEP rallied by 1.75% at the time of writing (February 12), closing at $170.61.

That’s essentially in-line with my updated fair value estimate of $172.

Therefore, PEP doesn’t offer much in the way of a margin of safety; however, after its -2% post-earnings dip, PEP is now trading at fair value and to me, this company falls into the, it’s acceptable to buy a “wonderful company at a fair price” category… a la, Warren Buffett.

I want to see what Coca-Cola (KO) does before the bell on the 13th before adding more shares of PEP here.

If KO experiences a post-earnings sell-off similar to PEP, they could end up being the more attractive option between the two (because PEP’s snacks category comes with more GLP-1 drug risk right now).

But if not, PEP trading with a 3%+ yield is a pretty attractive opportunity for me… especially after its 7.1% 2024 dividend increase announcement.

PepsiCo Q4 & Full-Year Results

Pepsi posted mixed results for the 4th quarter, beating Wall Street’s estimates on the bottom-line while missing consensus top-line levels.

PEP’s non-GAAP EPS came in at $1.78, beating consensus by $0.06/share.

The company’s Q4 sales totaled $27.85b, down 0.5% on a y/y basis, missing estimates by $520m.

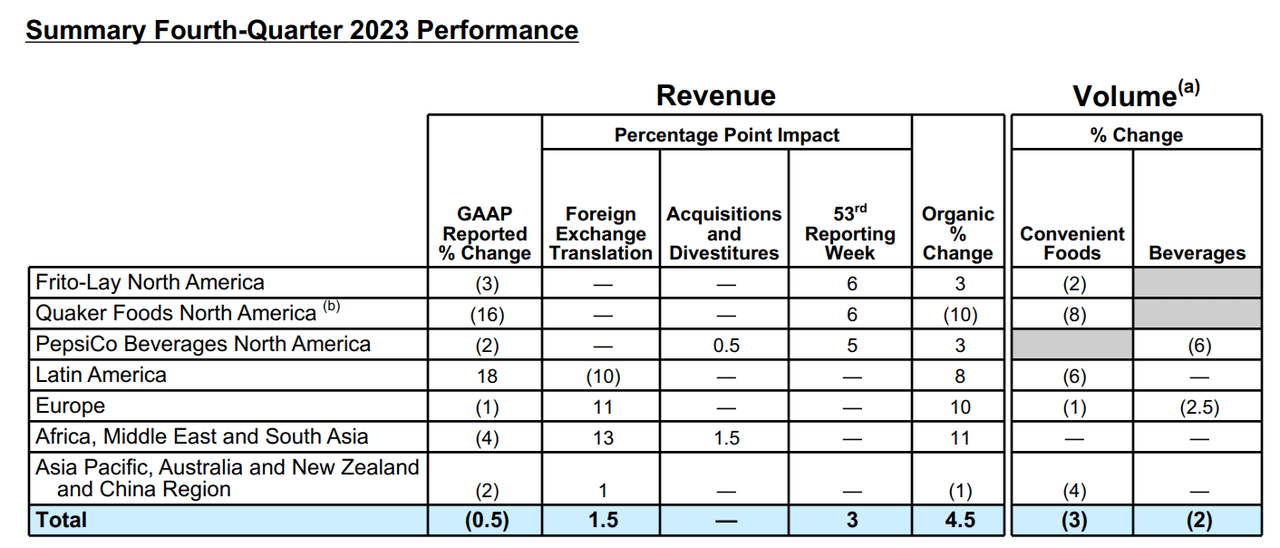

Overall, I thought the Q4 results were lackluster. Sales were down 0.5% and volumes were down in each of the company’s operating categories.

PEP Q4 ER

Despite these volume headwinds, PEP posted positive EPS growth because of its pricing power.

As you can see above, outside of its Quaker North America segment (which was experiencing one-time recall issues), the company’s organic pricing was up everywhere except for the Pacific region.

Overall, PEP’s pricing was up 4.5% during the quarter, more than making up for the single digit food and beverage volume losses.

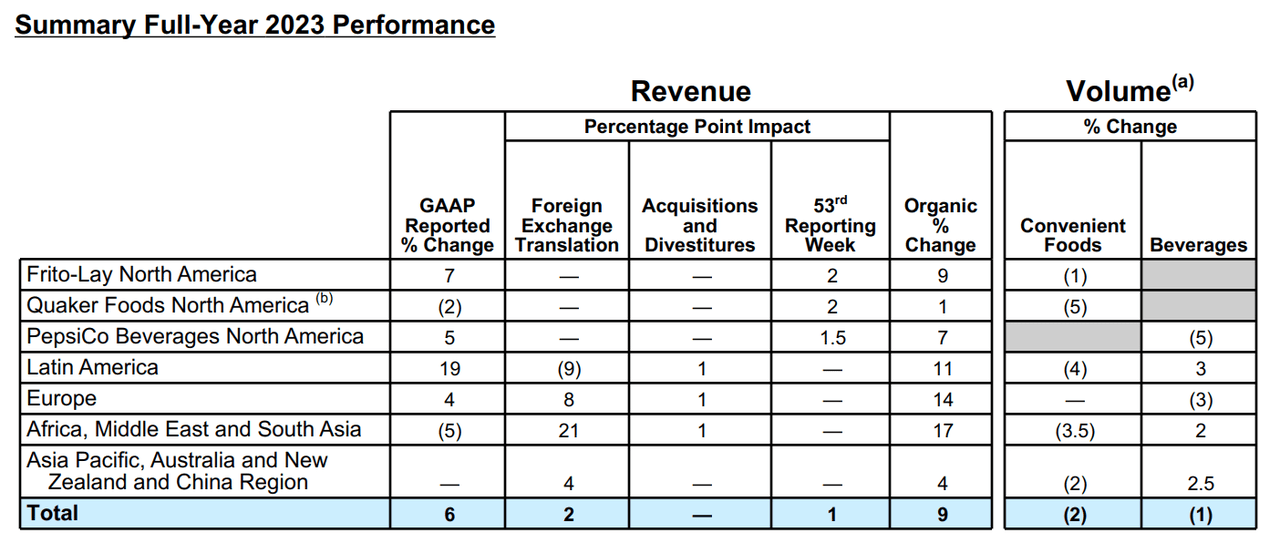

Looking at full-year results, we see similar issues (low single digit volume losses being overcome by 9% organic price increases).

PEP Q4 ER

Because of this trend, there are fears that this trend is unsustainable.

For PEP to continue to compound its bottom-line over the long-term, management is going to have to figure out ways to drive consumer demand higher and reignite volume growth across its portfolio.

Thankfully, this company has a strong track record of overcoming near-term hurdles.

PEP has posted positive annual EPS growth during 16 out of the last 20 years, after all.

Consistently, growth like that doesn’t happen by accident.

It happens because of strong, forward-looking management teams that are able to pivot when consumer trends shift.

Management discussed increasing marketing for the Frito-Lay, in particular, during Q4 (with plans to continue that spending into 2024).

They also mentioned that their supply chains across the snack categories are back up to 100% efficiency, and that should result in greater success/ROI from advertising dollars.

At the end of the day, any investment comes down to trust in a company’s management team to execute.

PEP continues to face headwinds in the snack space because of the health foods trend and the apparent pressure from rising obesity/weight-loss drug usage globally.

They’re also struggling to take market share from Coca-Cola in the international beverage race because of KO’s superior bottling/distribution assets across the globe.

But, I still think PEP is more likely than not to revamp its product portfolio over time and capitalize on its current brand equity to generate volume growth.

In the meantime, I think low-to-mid single digit organic pricing power can continue to bolster earnings.

A few percentage points of pricing gains, a few percentage points of volume growth, share buybacks, and a 3%+ dividend yield is a great recipe for success in the market.

Looking ahead, it still appears as though management is on track in this regard.

During the Q4 report, management provided investors with forward-looking guidance, stating, “For 2024, we now expect to deliver at least 4 percent organic revenue growth and at least 8 percent core constant currency EPS growth.”

Those EPS growth estimates are in-line with consensus, which is now calling for EPS of $8.15/share in 2024… or growth of 7% on a y/y basis.

High single digit growth is in-line with PEP’s long-term average.

During the last 10 and 20-year periods, PEP’s EPS CAGRs are 5.7% and 6.8%, respectively.

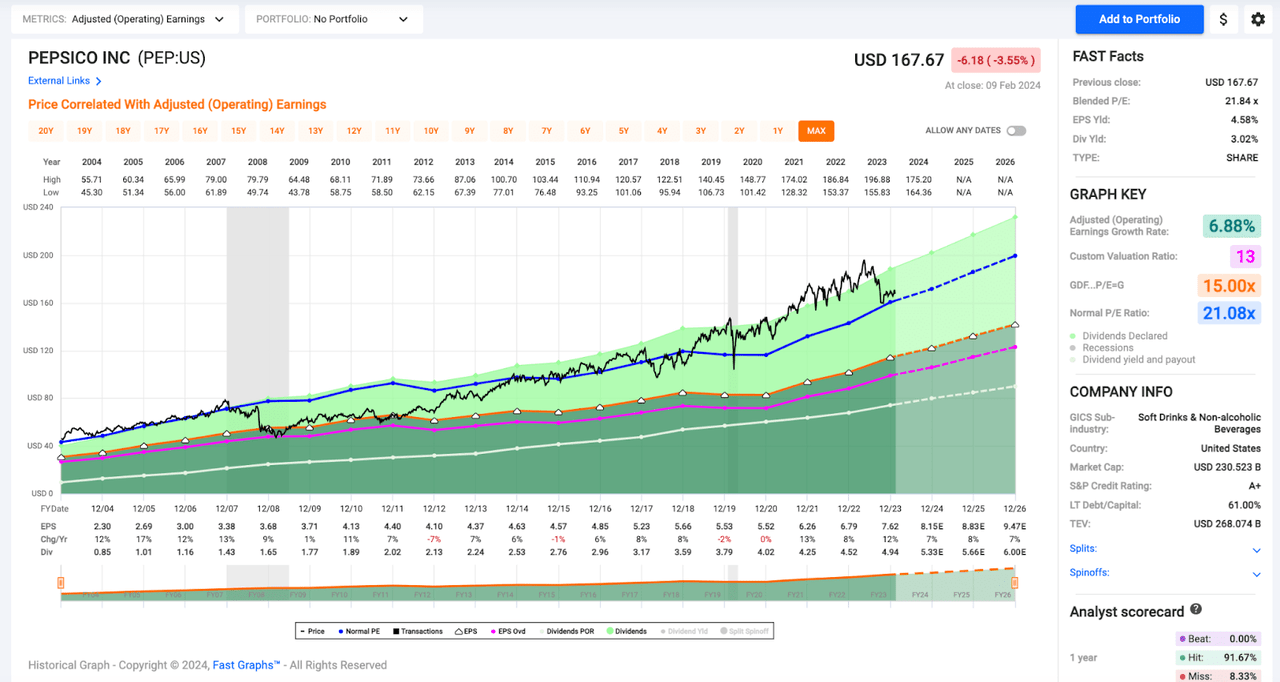

Looking at the stock’s historical P/E multiples, PEP is once again trading at a level that is line-line with its long-term averages.

And with that in mind, I think the stock’s recent pullback from the near-$200-level in the Spring/Summer of 2023 to the $170 area today represents an opportunity to buy more shares.

PEP Stock Valuation

Simply put, when we’re talking about a mature cash cow like this, when average fundamental growth rates align with average historical multiples, I tend to believe that the value being attached to shares is fair.

Over the last 20 years, PEP’s average P/E is essentially 21x.

Furthermore, as you can see on the chart below (looking at the blue line, which represents that 21x long-term average), outside of the Great Recession period (where PEP’s multiple dropped) and the post-COVID-19 period (where markets were hot), PEP shares have closely hugged that 21x level.

FAST Graphs

Obviously, the past cannot predict future returns. But, when I look at PEP and its peers, I think fair value lies in the 21-22x area and looking at the chart above, I could easily see PEP’s share price (the black line) follow that blue line (historical average) higher… just like it has for years.

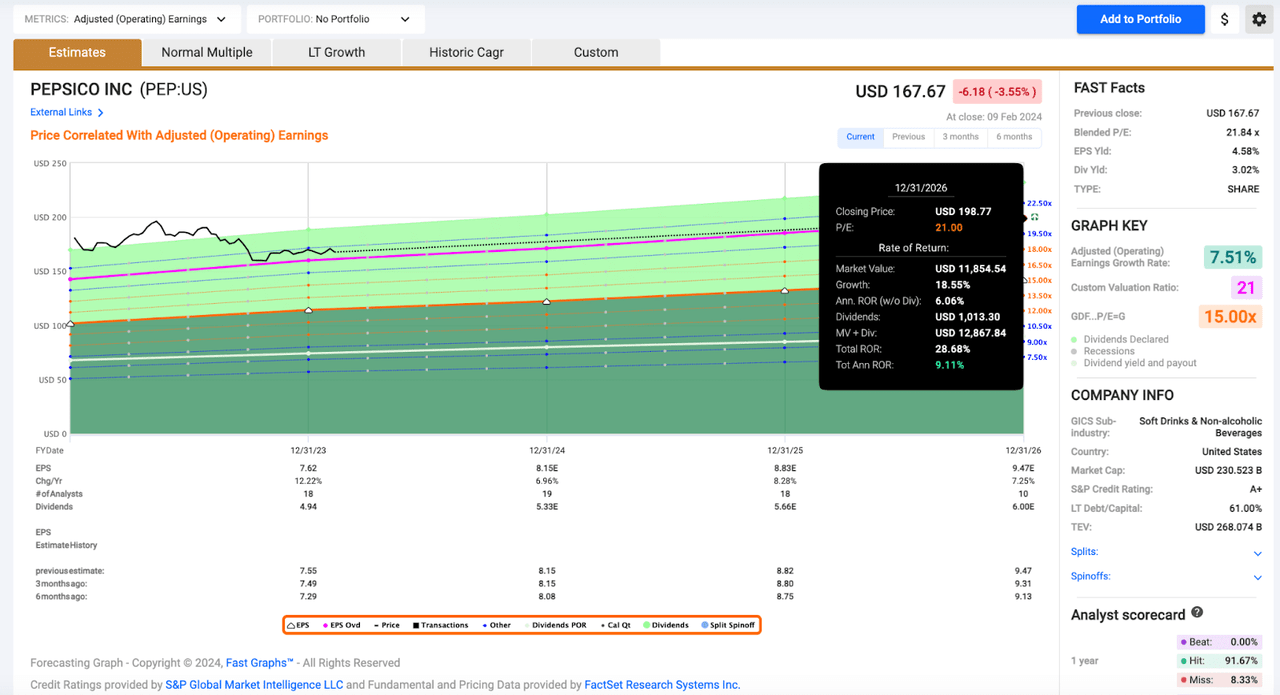

Assuming I’m right and PEP maintains a 21x multiple moving forward, then that $8.15/share 2024 EPS consensus and the stock’s forward dividend expectations represent high single digit total return CAGR potential.

FAST Graphs

Once again, 8-9% total returns moving forward aren’t exciting… but that does mean that investors are doubling their money every 8.5 years or so.

That sort of compounding potential combined with PEP’s low beta and very predictable cash flows make this a core holding for me (and many other investors).

This isn’t a get rich quick stock, by any means. But, as we all know, get rich quick schemes very rarely work out well.

Mature cash cows like PEP provide me peace of mind during bear markets and help to counterbalance some of the heightened volatility that my more growth-oriented investments bring to the table.

Companies like this are about peace of mind. I value sleeping well at night highly and therefore, adding to blue chips like PEP anytime they dip down to fair values remains a priority for me.

M&A Potential Represents Another Tailwind

Although Pepsi isn’t an overly exciting company, I think it could make a splash or two in the M&A markets to spice things up if it ever really needs to buy revenue growth.

I’d be remiss if I didn’t say that PEP already owns an ~8.5% stake in energy/fitness drink maker Celsius (CELH), which has been one of the hottest stocks in the entire market in recent years (CELH shares are up by more than 4,900% during the last 5 years).

CELH has experienced a bit of a pullback recently because of a Bank of America report highlighting slowing demand trends and a stagnating market share position for CELH and I hope that PEP is keeping a close eye on its share price.

Furthermore, CELH shares are extremely volatile due to the rather speculative nature of their valuation.

In the event of a macro pullback, I wouldn’t be surprised to see high-Beta CELH experience a significant double-digit pullback. And if that occurs, I’d love to see PEP pounce and try to buy out the rest of the company.

I don’t know if they’d admit it, but I’m sure that many Coca-Cola executives regret not buying all of Monster Beverage (MNST) when there were M&A rumors there about a decade ago.

Like PEP, Coca-Cola partnered with MNST, allowing the latter company to grow rapidly because of the strength of KO’s distribution/shelf space agreements.

KO owns ~20% of MNST shares… which has been a great investment. Monster shares are up by 345% during the last decade. But as a KO shareholder, I sure wish they owned 100%.

The caffeine race is really heating up as more and more data shows that younger generations are already addicted to it.

We’ve recently seen McDonald’s (MCD) roll out its CosMcs chain in an attempt to take share from coffee shops offering new-age caffeinated drinks.

The margins there are fantastic and consumers continue to show a willingness to pay outsized prices for fancy, colorful, fruity caffeinated drinks that trend on social media.

Well, I’d love to see PEP make a move to take share in the energy drink space, adding these (oftentimes zero sugar) offerings to their portfolio to help to offset the negative, health foods related trends hurting soda sales.

PEP has an A+ rated balance sheet, generated $9.1b of net income last year, and while they carry a relatively high debt load ($37.5b versus $10.5b or so of cash/cash equivalents), I think they could handle a CELH acquisition.

Frankly, I’d happily trade a few years or sub-par dividend growth for an asset like Celsius in the energy drink space.

I’m not going to hold my breath while I wait for this purchase to happen. Admittedly, this is entirely speculative. But, I really like the energy drink space, and I have to imagine that the KO/MSFT situation will be on the minds of PEP leadership if CELH experiences a deeper pullback.

PepsiCo’s Dividend Raise

As exciting as PepsiCo’s CELH stake and wonderful long-term EPS compounding record is, the #1 reason why I own this stock is its growing dividend.

Every year, PEP announces its upcoming annual dividend raise in its Q4 report.

This is confusing for many investors because technically, PEP hasn’t declared the dividend (and therefore, investing sites still show its old annual payment).

But, during the Q4 report PEP stated, “We also announced a 7 percent increase in our annualized dividend, starting with our June 2024 payment, which represents our 52nd consecutive annual increase, and we plan to repurchase approximately $1 billion worth of shares.”

The company continued, “The Company today announced a 7 percent increase in its annualized dividend to $5.42 per share from $5.06 per share, effective with the dividend expected to be paid in June 2024. This represents the Company’s 52nd consecutive annual dividend per share increase.”

So, once the Q2 payment is officially declared, we’ll be looking at that $5.42 annual payment, which would represent a ~3.2% yield relative to PEP’s current share price.

Give me a 3.2% yield growing at a 7% rate any day.

PEP’s 5-year DGR is 6.6%, so this raise is in-line with historical results.

It was also in-line with my 2024 expectations. Honestly, to me, a 3% yield with high single digit growth prospects is the perfect sweet spot between yield and growth.

Sure, 3% is lower than the ~5.2% yields that can be found on short-term bonds right now; however, this isn’t about yield in the present, but instead, its compounding potential.

A yield that is growing at a 7% rate will double every decade.

And as someone with a long-term investing horizon, a 3% yield growing at a 7% clip beats the pants off of a stagnant 5% yield.

Conclusion

PepsiCo’s Q4 results weren’t great, but they were solid.

And at today’s valuation, that’s enough for a blue chip like this.

The company is calling for continued high single digit EPS growth.

It just increased its dividend by 7%.

And looking at long-term data, at ~21x forward earnings, it’s difficult to find a more attractively valued defensive stock in the market today (many of these types of companies are trading in the 23-25x range).

I believe that the GLP-1 drug phenomena has resulted in this relative discount for companies like Pepsi that sell unhealthy drinks/snack foods; however, I think long-term demand destruction fears surrounding weight-loss drugs are overblown.

I wouldn’t be interested in buying PEP with a 25x forward multiple attached like it had during much of 2021, 2022, and some of 2023; however, 21x forward points towards fair value to me.

And as Warren Buffett says, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

That’s why you shouldn’t be surprised if you see me add to my PEP position in the coming days/weeks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of A, AAPL, ABBV, ACN, ADP, AMGN, AMZN, APD, ARCC, ARE, ASML, AVB, AVGO, BAH, BAM, BEPC, BIPC, BIL, BLK, BN, BR, BTI, BX, CME, CNI, CP, CPT, CRM, CSCO, CSL, DE, DHR, ECL, ELV, ENB, ESS, SPAXX, GOOGL, HON, HSY, ICE, ITW, JNJ, KO, LHX, LMT, MA, MAIN, MCD, MCO, META, MKC, MO, MRK, MSCI, MSFT, NKE, NNN, NOC, NVDA, O, ORCC, OTIS, PEP, PH, PLD, PLTR, QCOM, REXR, RSG, RTX, SBUX, SHW, SPGI, TMO, TD, TXN, USFR, UNH, V, VLTO, WM, ZTS either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Dividend Kings helps you determine the best safe dividend stocks to buy via our Master List. Membership also includes

Dividend Kings helps you determine the best safe dividend stocks to buy via our Master List. Membership also includes

- Access to our model portfolios

- real-time chatroom support

- Our “Learn How To Invest Better” Library

- Exclusive trade alerts from Nicholas Ward

Click here for a two-week free trial so we can help you achieve better long-term total returns and your financial dreams.