Summary:

- The electric vehicle (EV) industry in the U.S., including Rivian Automotive, has seen significant value destruction over the past year due to missed production targets, supply chain issues, and weakening consumer demand.

- Rivian has recently adopted the North American Charging Standard developed by Tesla, which could boost the industry as it allows EV buyers to use Tesla’s supercharger network.

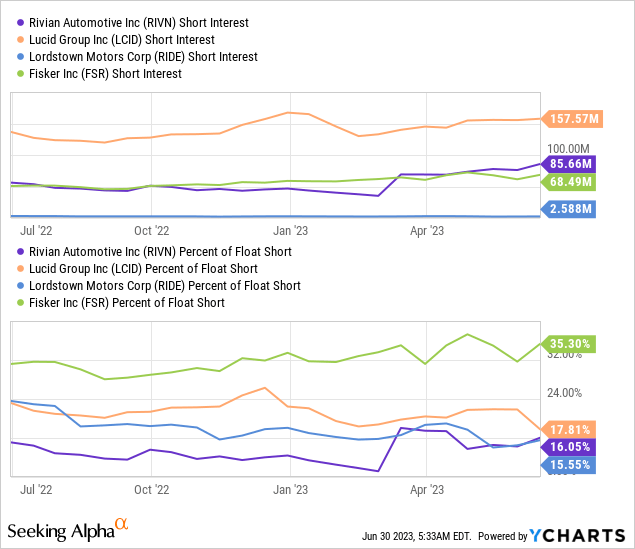

- Rivian’s short interest ratio has soared lately. About 17% of the company’s float is shorted.

- While I don’t recommend Rivian due to its high valuation, I believe Rivian could be a short squeeze candidate as 75% of the firm’s market cap consists of cash.

hapabapa

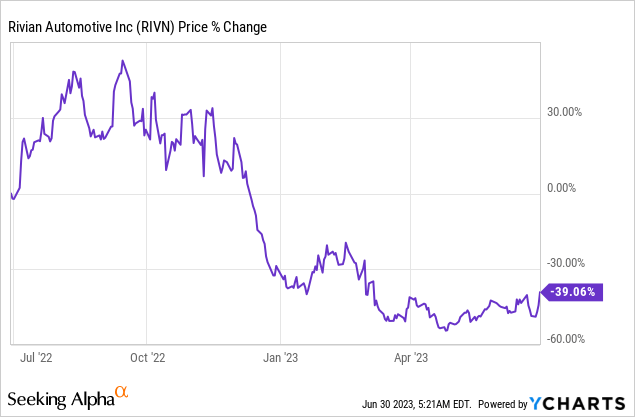

The U.S. electric vehicle industry in the U.S. has seen enormous value destruction in the last year as investors started to question the delivery realities of companies such as Rivian Automotive (NASDAQ:RIVN) and many others. Rivian Automotive’s share price has declined 39% in the last year and in April made a new low at $11.68. A number of factors have driven Rivian’s share price to new lows including waning EV demand and reduced production targets due to supply chain dislocations. Short-sellers have ramped up their exposure to Rivian as a result. Since Rivian has about 75% of its market cap in cash, the soaring short interest ratio potentially indicates that the EV company could be a short squeeze candidate!

EV industry experiences a shake-out, Lordstown files for bankruptcy

Shares of electric vehicle manufacturers have not exactly been strong performers in the last year, in large part because supply chain problems and logistical challenges have caused many EV makers to miss production targets.

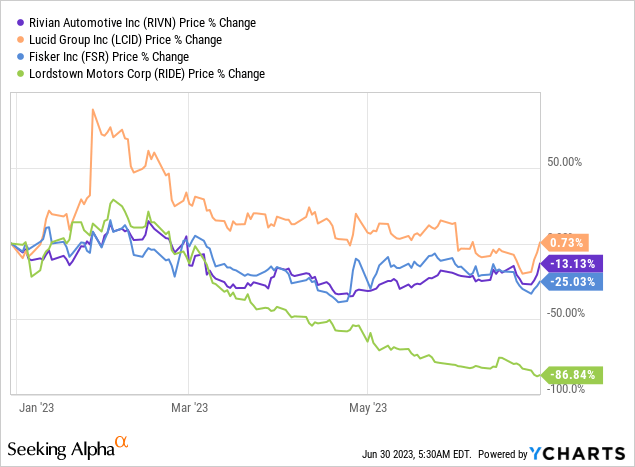

In 2023, a new issue started to affect the sector, weakening consumer demand, which has caused companies like Lucid Group (LCID) to no longer report reservation numbers. Another EV-focused company, Lordstown (RIDE) even filed for bankruptcy this week as the business ran out of cash and the company is now suing its contract manufacturer and investor Foxconn for $170M.

The bankruptcy of electric vehicle start-up Lordstown has not served the EV industry as a whole and companies like Lucid, Rivian or Fisker (FSR), which all have reported disappointing delivery numbers in recent quarters, have performed extraordinarily bad. Of all the companies mentioned here, only Lucid managed to squeeze out a positive YTD return of 0.73%, in part because the company hinted at entering the rapidly expanding Chinese EV market.

Rising short interest ratios for EV companies, soaring short interest for Rivian

The decline in EV market valuations has coincided with a massive increase in the short interest ratios of electric vehicle companies. Rivian currently has about 86M of its outstanding shares shorted which calculates to a short interest ratio (based on float) of 16%. Other EV manufacturers also have sky-high short interest ratios with Fisker currently having the highest: 35%.

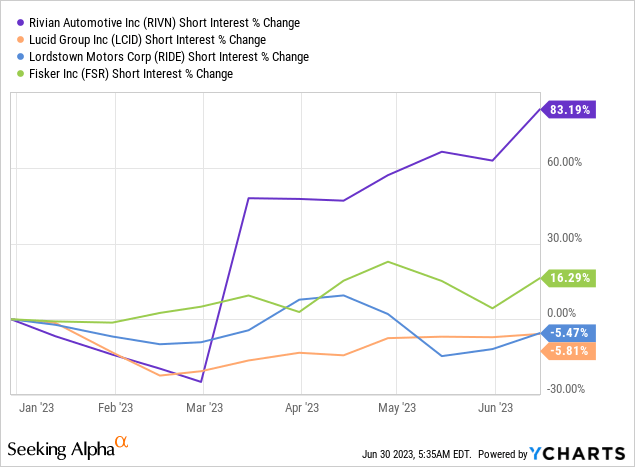

What stands out is that Rivian especially has seen a massive increase in its short interest ratio, a strong indication that a growing portion of the market believes that Rivian may have difficulties in meeting its production goals for FY 2023. Rivian’s short interest ratio has gone up the most in the industry group, YTD, by 83%… which is more than five times higher than Fisker’s.

The large increase in Rivian’s short interest ratio makes Rivian a potential short squeeze target, especially if the company reports strong Q2’23 earnings, confirms its FY 2023 production target or reports any other good news… such as the adoption of Tesla (TSLA)’s NACS charging standard.

Rivian adopts NACS charging standard, increasing appeal of Rivian’s EV portfolio

Earlier in June, Rivian said that it will join the North American Charging Standard which was developed by EV pioneer Tesla. Rivian joined the NACS charging standard after other companies in the U.S. adopted Tesla’s charging standard as well: Ford (F) adopted the NACS standard in May — Ford Hits A Homerun With Tesla Partnership — followed by General Motors (GM) in June, thereby allowing buyers of a new EV to use Tesla’s 12 thousand superchargers in the U.S. and Canada. The adoption of Tesla’s NACS charging port harmonizes the electric vehicle charging infrastructure in North America and makes the purchase of a Rivian EV more attractive from a consumer point of view. Since the announcement, shares of Rivian have revalued about 10% higher.

Rivian is still highly valued, but high short interest is a potential problem

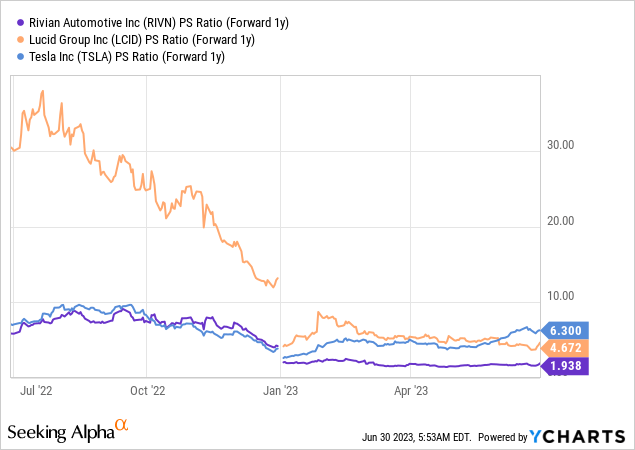

I have repeatedly written about Rivian and said that I consider the EV company to be overvalued, based off of where the company currently stands with its production: Rivian produced only 24,337 electric vehicles in FY 2022, although the company guided for a production volume of 25,000… which itself was lowered from 50,000 EVs earlier that year. Rivian is still highly valued with a P/S ratio of 1.94X. Although Rivian’s EV potential is not as expensive as Tesla’s or Lucid’s. However, given the enormous increase in Rivian’s short interest ratio lately, I actually see Rivian as a potential short squeeze candidate. This is the main reason why I am upgrading my sell rating to a hold rating.

There are risks with Rivian, but the balance sheet is not one of them

Rivian has a very strong balance sheet with cash resources of approximately $11.2B at the end of March 2023 which calculates to about $12 per share in cash (75% of Rivian’s market cap). Funding the EV ramp is therefore not a real risk that I see for Rivian. The biggest commercial risk, in my opinion, relates to Rivian’s production trajectory. Rivian lowered its production target from 50,000 EVs to 25,000 EVs in 2022 and could be at risk of having to lower its production guidance for FY 2023 if EV demand continues to weaken. For the current year, Rivian expects a doubling of production to approximately 50,000 EVs. A failure to meet this production target could result in a continual uptick in the short interest ratio.

Closing thoughts

Rivian has had its fair amount of challenges, including softening consumer demand and a slower than expected production ramp, but what the company doesn’t have is a cash problem. Rivian has the best balance sheet in the industry, in my opinion, and the company’s high cash per-share value limits further downside potential. Considering that I still believe shares of Rivian to be expensive, I don’t believe a company with 75% of its market cap tied up in cash is a promising short candidate. Quite the opposite: the massive increase in Rivian’s short interest ratio now makes the company a potential short squeeze candidate!

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of LCID either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.